AE

AEParticipant

Senior

Thanks Paul,

I will try to improve a version to use in DAX and SP500 by myself.

About your version, who can you know that your version is not overfitted? How did you do to avoid it?

Thanks

Paul

PaulParticipant

Master

Hi AE,

To have old results before my findings; use 4.1p version;

set holiday to 0, set usetimecriteria to 0, adjust starttime to previous values

the combination of so many parameters & settings means it’s all heavily curve-fitted! Every rule you add adds to that.

AEParticipant

Senior

Thanks Paul, I will check your strategy in demo account. It looks really incredible!

offtopic: Paul, I see you can run backtesting with 200k. Could you please run my strategy with your backtesting in DAX 1 minute? (attached)

Thanks again and sorry

Thanks Paul, I will check your strategy in demo account. It looks really incredible!

offtopic: Paul, I see you can run backtesting with 200k. Could you please run my strategy with your backtesting in DAX 1 minute? (attached)

Thanks again and sorry

Interesting…maybe you should open a new topic for that and explain how it works?

Hi Paul, Hi Emanuele,

Thanks @volpiemanuele for this version of Money Management but to be honest it’s not easy to understand.

@Paul, don’t you mind to tell us which last version do you use on this strategy? Maybe in V3? Or one of the 4 snippets of the library?

Thanks in advance for your help.

Gregg

Hi Paul & Emmanuele, it’s Gregg again 🙂

Unfortunately we can’t edit our replies. So forget my last message, I’ve studied your MM code Emmanuele and I think I understand the most part of it.

Can I ask you how you choose which one of the 5 strategies? I tried each and I’m not sure which factor I have to consider in priority. Maybe the % Drawdown max? Maybe the Max quantity of volume for avoid margin?

Have you some advice? Are you more confortable with one of your MM strategy? Thanks

PaulParticipant

Master

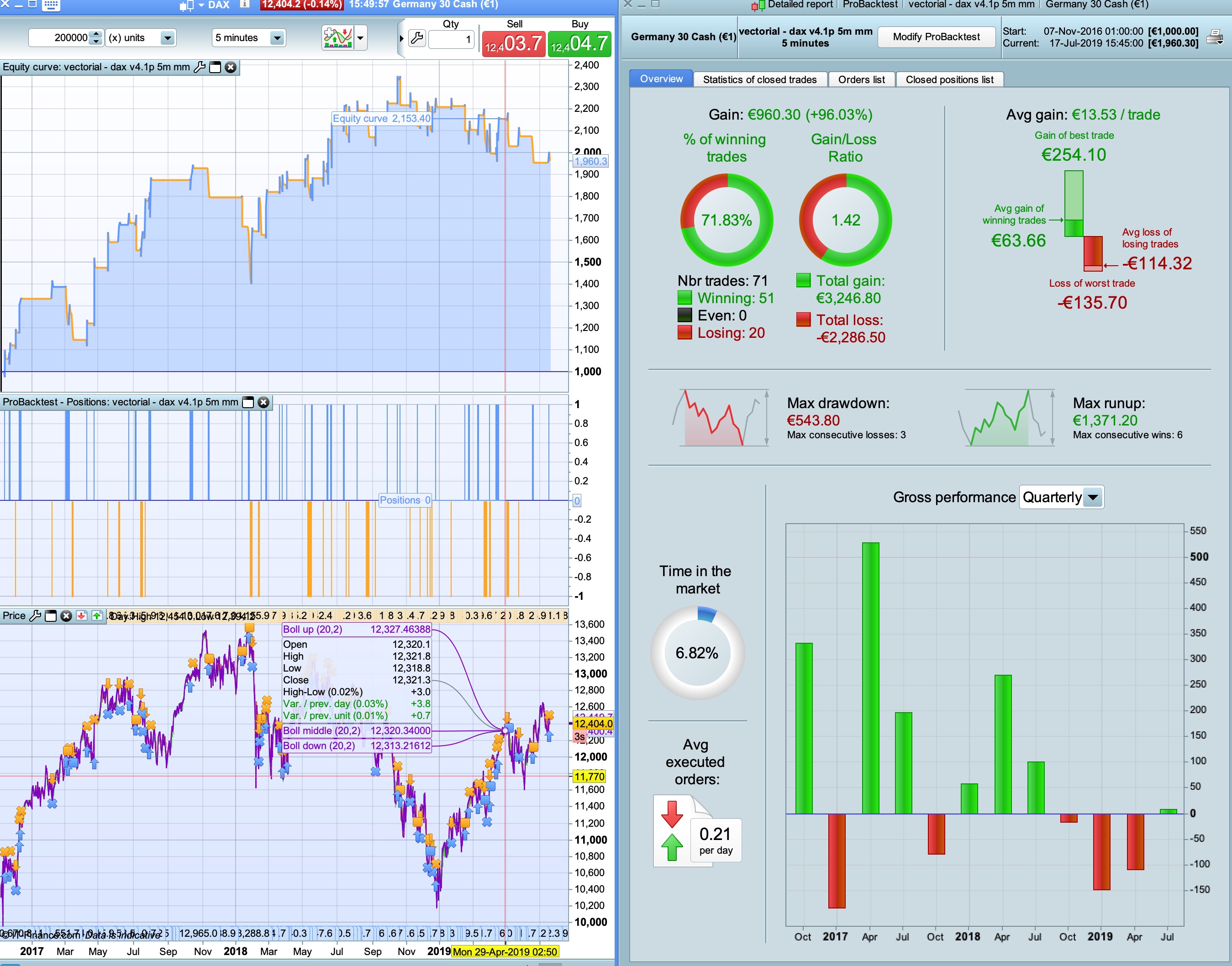

@Gregg one way I find MM interesting but my choice personally, if you trust a strategy, double it with a slightly different version with different values & exit times.

For this strategy I’am a bit wary because of the big stoploss 2% and the flattening out at the top right now. Especially with a stoploss of 1%.

Another way to look at this strategy, divide it into three segments, morning trade, luchtrade, and afternoontrade. Then the morning strategy don’t get out on a signal after say 113000 but runs on ts/bb/sl. In the morning session you see a quite a big drop and is an indication that the quality entry can be poor. But if you trade the full tradingtime and have an opposite signal then you don’t notice that poor entry really in a backtest.

As it is, winning >80% with over 200 trades with a good avg gain and equitycurve makes it a difficult choice.

PaulParticipant

Master

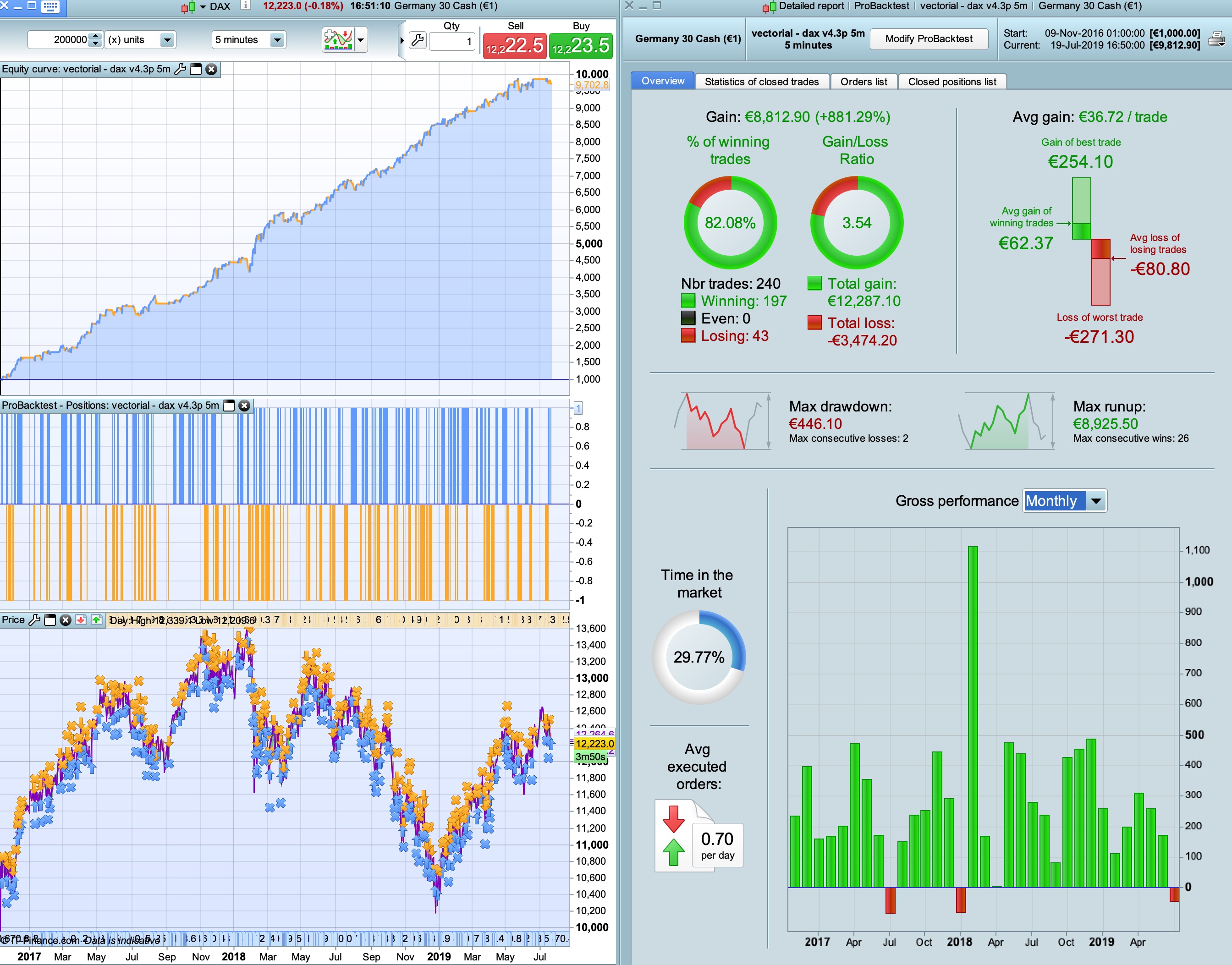

let’s do that again with a 1% stoploss (post above with 2%)

@gregg In this period I’m in Holiday and I have access to my mail only in the afternoon.

There are 5 type of MM:

CONSECNOCYCLE = 0 // The system enters the position of x lot and at each gain increases by x lot and at the first loss it returns to x lot

CONSECSICYCLE = 1 // The system enters the position of x lot and at each gain increment of x lot and at the first loss returns to x lot or in the case of N trade (so they will all be positive) returns the size to x lot

CUMULASICYCLE = 0 // The system enters the position of x lot and at each gain increases by x lot and at each loss -x lot but after a cycle of N trade (regardless of whether loss or gain) returns the size to x lot

traditional = 0 // trade only a fixed position that you chose.

percentage = 0 // % risk combined with capital and stop loss

You should do several back tests with the different types of MM and try to understand what is best for you. In my opinion, there is no better objective choice than another … it is a subjective choice.

Thank you @paul for your advice. But do you mean by that that we should only take the afternoon part of this strategy? That morning and lunch time are not good enough? or decrease the profit? Yes indeed, very difficult to find, mix and choose all these parameters.

And thanks @volpiemanuele for your Money Management details. It appears very clearly for me now. Except that, as I said to Paul, it’s difficult to choose 🙂 Enjoy your holidays and all my gratitude to answer me during these free days for you 🙂

PaulParticipant

Master

Hi all,

below it’s based on 4.1p without MM.

The difference to the test above; close a trade morning trade on opposite signal i.e. lunch or afternoon-time. sl/tp/ts are always active regardless the time.

This was out of curiosity. If you would trade all 3 trading-schedules separate, results seem to be +10%-15% more that just the default 0955-1745 trading-schedule.

I’am not sure, but if trading the 3 schedules the margin required may be only for 1 because in theory there is no overlapping. Something to check.

@Gregg Just saying be careful. Have a look a the adjusted code & do a few tests to compare.

PaulParticipant

Master

v4.3p as used in above test

hi,

what’s the difference between version 4.2 and 4.3 ? Thanks

PaulParticipant

Master

skip 4.2p which uses code below

// reset at start

if intradaybarindex= 0 then

tradeday = 1

endif

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

longtradecounter= 0

shorttradecounter = 0

tradecounter=0

endif

pclong = countoflongshares < 3 and longtradecounter < 10 and tradecounter < 5

pcshort= countofshortshares < 3 and shorttradecounter < 10 and tradecounter < 5

Above was an experiment because of MM to reset the counter differently but it had better results. I won’t use it again.

PaulParticipant

Master

v4.3p has more options as 4.1p.

About overlapping positions. It could overlap when running at the same time 3 versions (morning,lunch,afternoon).