I leave the sale on the Marketplace to the Swedes… 😉 Well, a little more than 1 trade a day, short ends every day and long on Friday at the latest. There are actually no long-term trades.

Good idea – think I’ll wait to pay for the Nordic version of this code posted here too :)!

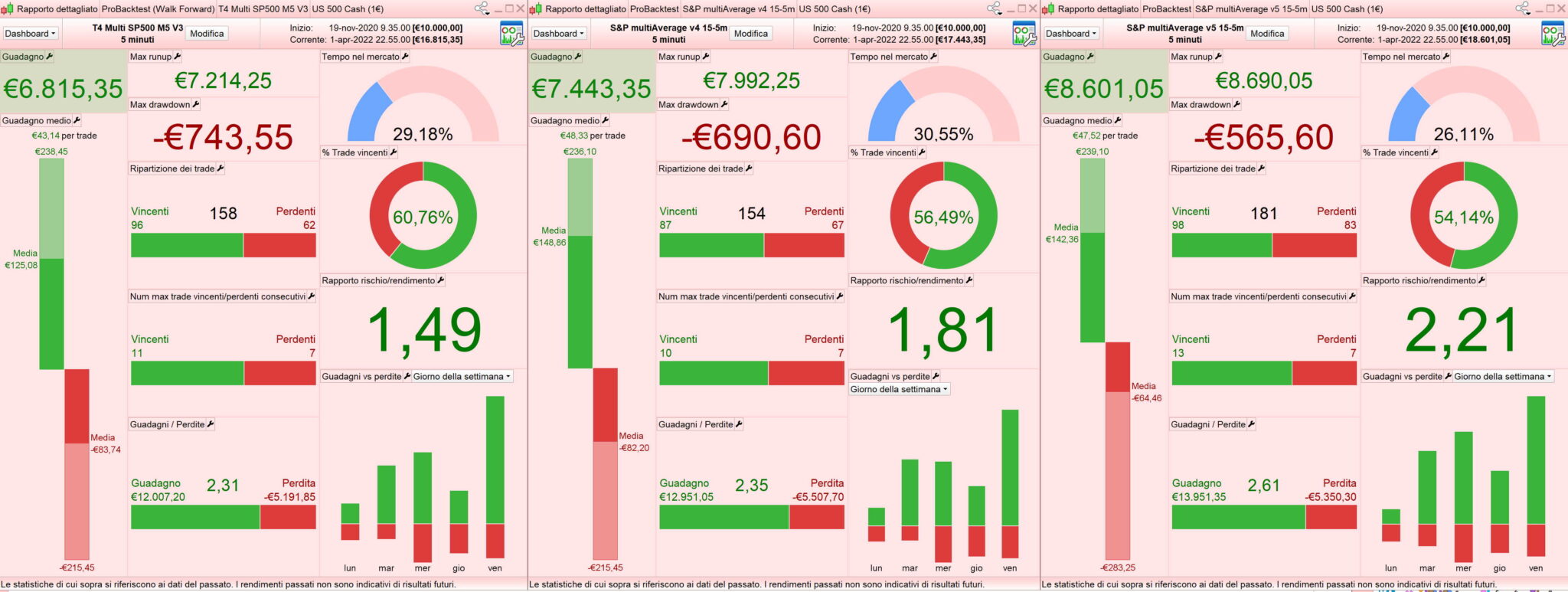

I have modified my previous version (v4) in order to reduce the DD. In this version (v5) the longterm average (480 weekly) has been replaced with two weighted averages and has been added a filter to avoid operations in a market with low volatility (image below : 100k)

//TS MULTIAVERAGE SP500 v5 - CFD 1 euro - Spread 0.6

defparam CUMULATEORDERS = false

positionSize = 5

//---------------------------------------------------------------------------------------

timeFrame(15 minute, updateOnClose) //TF 15 minutes

c1L = close > average[500,2](close)

c1S = close < average[450,2](close)

avg1 = average[15,0](close)

avg2 = average[55,0](close)

avg3 = average[14,1](close)

avg4 = average[20,1](close)

c2L = avg1 > avg2

c2S = avg3 < avg4

avgTrigger = average[5,0](close)

c3L = avgTrigger crosses over avg1

c3S = avgTrigger crosses under avg1

//---------------------------------------------------------------------------------------

timeFrame(default) //TF 5 minutes = DEFAULT

//------------------------------------------------

period = 110 //low volatility filter (MauroPro)

minLevel = 10 *pointsize

amplitudeRange = highest[period](high)-lowest[period](low)

cMinRange = amplitudeRange > minLevel

//-------------------------------------------------

cLong = c1L and c2L and c3L

cShort = c1S and c2S and c3S

cLongExit = c1S

cShortExit = c1L

//--------------------------------------------------------------------------------------

ONCE buyTime = 110000

ONCE sellTime = 213000

ONCE buyTimeShort = 150000

ONCE sellTimeShort = 213000

//--------------------------------------------------------------------------------------

if time >= buyTime and time <= sellTime then //LONG POSITION: TECHNICAL ENTRY

if cLong and cMinRange then

buy positionSize contract at market

endif

endif

if longOnMarket and cLongExit then //LONG POSITION: TECHNICAL EXIT

sell positionSize contract at market

endif

//----------------------------

if time >= buyTimeShort and time <= sellTimeShort then //SHORT POSITION: TECHNICAL ENTRY

if cShort and cMinRange then

sellshort positionSize contract at market

endif

endif

if shortOnMarket and cShortExit then //SHORT POSITION: TECHNICAL EXIT

exitShort positionSize contract at market

endif

//----------------------------------------------------------------------------------------

if longOnMarket then //SL & TP Exit

set stop %loss 1.7

elsif shortOnMarket then

set stop %loss 0.5

endif

if longOnMarket then

set target %profit 1

elsif shortOnMarket then

set target %profit 1

endif

//------------------------------------------------------------------------------------

if time = 223000 then //time Exit

//sell at market

exitShort at market

endif

if time = 225500 and dayOfWeek=5 then

sell at market

exitShort at market

endif

//--------------------------------------------------------------------------------------------

DirectionSwitch = (LongOnMarket AND ShortOnMarket[1]) OR (LongOnMarket[1] AND ShortOnMarket) //TrP Exit (Gozzi

IF Not OnMarket OR DirectionSwitch THEN

TrailStart = 40 // Start trailing profits

PointToKeep = 0.2 // 20% Profit percentage to keep when setting BreakEven

StepSize = 5 // Point to increase Percentage

PerCentInc = 0.2 // 20% PerCent increment after each StepSize Chunk

RoundTO = -0.5 //-0.5 rounds always to Lower integer, 0 defaults PRT behaviour

PriceDistance = 6* pipsize //minimun distance from current price

maxProfitL = 0

maxProfitS = 0

ProfitPerCent = PointToKeep //reset to desired default value

SellPriceX = 0

SellPrice = 0

ExitPriceX = 9999999

ExitPrice = 9999999

ELSE

IF PositionPrice <> PositionPrice[1] AND (ExitPrice + SellPrice) <> 9999999 THEN //go on only if Trailing Stop had already started trailing

IF LongOnMarket THEN

newSlL = PositionPrice + ((close - PositionPrice) * ProfitPerCent) //calculate new SL

SellPriceX = max(max(SellPriceX,SellPrice),newSlL)

SellPrice = max(max(SellPriceX,SellPrice),PositionPrice + (maxProfitL * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ELSIF ShortOnMarket THEN

newSlS = PositionPrice - ((PositionPrice - close) * ProfitPerCent)

ExitPriceX = min(min(ExitPriceX,ExitPrice),newSlS)

ExitPrice = min(min(ExitPriceX,ExitPrice),PositionPrice - (maxProfitS * pipsize))

ENDIF

ENDIF

ENDIF

//---------------------------------------------------------------------------------------------------------------------------------------------------

IF LongOnMarket AND close > (PositionPrice + (maxProfitL * pipsize)) THEN //LONG positions

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

profitL = (close - PositionPrice) / pipsize //convert price to pips

IF profitL >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - profitL) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = PointToKeep + (PointToKeep * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

maxProfitL = max(profitL * ProfitPerCent, maxProfitL)

ENDIF

ELSIF ShortOnMarket AND close < (PositionPrice - (maxProfitS * pipsize)) THEN //SHORT positions

profitS = (PositionPrice - close) / pipsize

IF profitS >= TrailStart THEN

Diff2 = abs(TrailStart - profitS)

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO))

ProfitPerCent = PointToKeep + (PointToKeep * (Chunks2 * PerCentInc))

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent))

maxProfitS = max(profitS * ProfitPerCent, maxProfitL)

ENDIF

ENDIF

//--------------------------------------------------------------------------------------------------------------------------------------------------------------

IF maxProfitL THEN //LONG positions - Place pending STOP order when maxProftiL > 0 (LONG positions)

SellPrice = max(SellPrice,PositionPrice + (maxProfitL * pipsize)) //convert pips to price

IF abs(close - SellPrice) > PriceDistance THEN

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

SELL AT Market

ENDIF

ENDIF

IF maxProfitS THEN

ExitPrice = min(ExitPrice,PositionPrice - (maxProfitS * pipsize)) //SHORT positions

IF abs(close - ExitPrice) > PriceDistance THEN

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

EXITSHORT AT Market

ENDIF

ENDIF

//------------------------------------------------------------------------------------------------------------------------

@MauroPro

Thank you. This is also a good option. I can see that this strategy structure seems to offer a lot of possibilities. The main filter is a bit slower, is that better? I’m not at the computer right now… could you please post the long/short split?

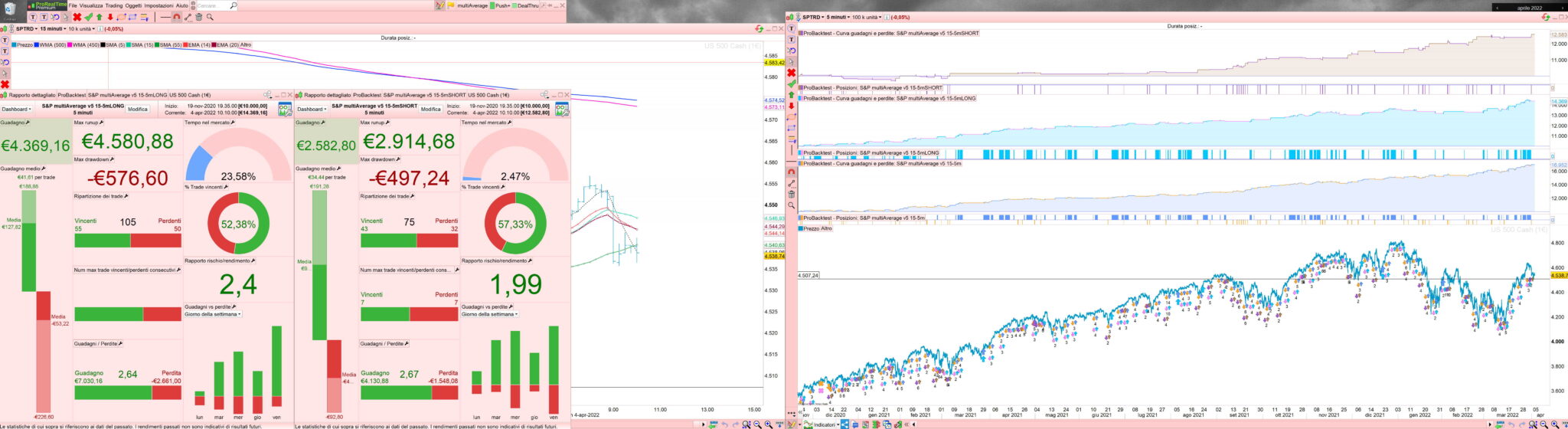

Here are the separate long and short parts of the TS.

Hi Phoentzs, the test was done with 4 contracts and not 5 as the original (I had put four to better split the operations and I forgot to change the positionSize).

I also have noticed that the system remains short for a very little time.

I had the feeling with my tests too. I think it’s because a fast trailing is responsible in the short. And not to forget, every evening shorts will be closed. I found that the index recovered overnight very often and then an open short position is not good.

Hello,

Sorry I ‘m new, and I try to back test this bot NAS -5- MA Cross-V3, and after the 15th of February 2022 none position, the Bot stop until today. Maybe somebody have a answer or maybe somebody can help me. In advance thank you.

Regards

Chris

It would be worth you trying one of the other Systems off the List – View All Attachments – at the top left of this page … see if you get the same limitations re dates etc?

The one CRISRJ refers to is Attachment 5, so I’m suggestig he tries, maybe Attachment 15?

Dear GraHal,

In first thanks a lot for your quick reply.

To be honest I try all the systems but this bot is very good and he never took position (now more of one year) and I don’t understand why, I try to check the code and with my level I see nothing is the reason why I ask for the experts.

Regards

Cris

Have you tried another bot? If yes, which one? The bot’s filters are designed for two things. Set the trend once and then keep the bot out of trouble and sideways phases. Maybe it’s because? There haven’t been many longer trends this year. But I can’t imagine that there was no trade at all. Maybe trading time? The bots are set to German time. Could you please post the relevant code?

Here’s the code …

CRISRJ is correct … no trades at all after 16 Feb 22!

//================================================

// Code: NAS 5m MACross v3

// Version 3

// Index: NASDAQ

// TF: 5 min

// Spread: 1

// Date: 27/01/2022

// Notes: added Tradetime

// changed SL, TP and Trailstart to percentage

// 3 MTF levels, 4h, 15m, 5m

// added max no. bars for any trade (EZT)

//

//================================================

DEFPARAM CUMULATEORDERS = FALSE

DEFPARAM preloadbars = 10000

//MONEY MANAGEMENT II

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 0.5

ENDIF

if MM then

MinSize = 0.5 // IG minimum position size allowed

MaxSize = 2000 // IG tier 2 margin limit

ProfitAccrued = 0 // when restarting strategy, enter profit or loss to date in instrument currency

DD = 486 //MinSize drawdown in instrument currency

Multiplier = 3 //drawdown multiplier

Capital = DD * Multiplier

Equity = Capital + ProfitAccrued + StrategyProfit

PositionSize = Max(MinSize, Equity * (MinSize/Capital))

if positionsize > MaxSize then

positionsize = MaxSize

endif

PositionSize = Round(PositionSize*100)

PositionSize = PositionSize/100

ENDIF

//Tradetime

//adjustment for American Daylight Savings time

ADLS =1

if ADLS then

DLS =(Date >= 20100314 and date <=20100328) or (Date >= 20101031 and date <=20101107) or (Date >= 20110313 and date <=20110327) or (Date >= 20111030 and date <=20111106) or (Date >= 20120311 and date <=20120325) or (Date >= 20121028 and date <=20121104) or (Date >= 20130310 and date <=20130331) or (Date >= 20131027 and date <=20131103) or (Date >= 20140309 and date <=20140330) or (Date >= 20141026 and date <=20141102) or (Date >= 20150308 and date <=20150329) or (Date >= 20151025 and date <=20151101) or (Date >= 20160313 and date <=20160327) or (Date >= 20161030 and date <=20161106) or (Date >= 20170312 and date <=20170326) or (Date >= 20171030 and date <=20171105) or (Date >= 20180311 and date <=20180325) or (Date >= 20181028 and date <=20181104) or (Date >= 20190310 and date <=20190331) or (Date >= 20191027 and date <=20191103) or (Date >= 20200308 and date <=20200329) or (Date >= 20201025 and date <=20201101) or (Date >= 20210314 and date <=20210328) or (Date >= 20211031 and date <=20211107) or (Date >= 20220313 and date <=20220327) or (Date >= 20221030 and date <=20221106) or (Date >= 20230312 and date <=20230326) or (Date >= 20231029 and date <=20231105) or (Date >= 20240310 and date <=20240331) or (Date >= 20241027 and date <=20241103)

If DLS then

Tradetime = time >=133000 and time <200000

elsif not DLS then

Tradetime = time >=143000 and time <210000

endif

endif

if not ADLS then

Tradetime = time >=143000 and time <210000

endif

//Long Entry Filter

Timeframe(4 hours)

FMA1 = average[p,t](typicalprice)

FMA2 = average[p1,t](typicalprice)

cb1 = FMA1 > FMA2

//cs1 = FMA1 < FMA2

Timeframe(15 minutes)

cb2 = close>average[p2,t2](typicalprice)

//cs2 = close<average[p2,t2](typicalprice)

Timeframe(Default)

//Long Entry Criteria

MA1=average[p3,t3](typicalprice)

MA2=average[p4,t3](typicalprice)

cb3 = MA1 crosses over MA2

//cs3 = MA1 crosses under MA2

// Conditions to enter long positions

If Tradetime and cb1 and cb2 and cb3 Then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

// Conditions to exit long positions

//if longonmarket and positionperf>0 and cs3 then

//sell at market

//endif

// Conditions to enter short positions

//If close <= Lowest[Sbars](OPEN) then

//Buy PositionSize CONTRACTS AT MARKET

//ENDIF

// Stops and targets

//slvalue=close[1]/153*1.6

//graph slvalue

//

//tpvalue=close[1]/88*1.6

//graph tpvalue

SET STOP %LOSS sl

SET TARGET %PROFIT tp

// Break even and trailing stop

// https://www.prorealcode.com/topic/breakeeven-trailing-profit/

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

ts = (tradeprice*pc)/100 // % trailing start

TrailStart = ts //30 Start trailing profits from this point

BasePerCent = base // 0.200 20.0% Profit percentage to keep when setting BerakEven

StepSize = ss //10 Pip chunks to increase Percentage

PerCentInc = pci // 0.100 10.0% PerCent increment after each StepSize chunk

BarNumber = bn //10 Add further % so that trades don't keep running too long

BarPerCent = bpc // 0.100 10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 5 * pipsize //IG minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN

//LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN

//SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF (longonmarket and barindex-tradeindex(1)>= b1 and positionperf>0) or (longonmarket and barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf>0) or (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf<0) then

exitshort at market

endif

endif