Hello,

Enclosed is a very simple long only moving average cross over strategy. There are more sophisticated MA strategies elsewhere on this forum however, I have opted to keep it simple in this version.

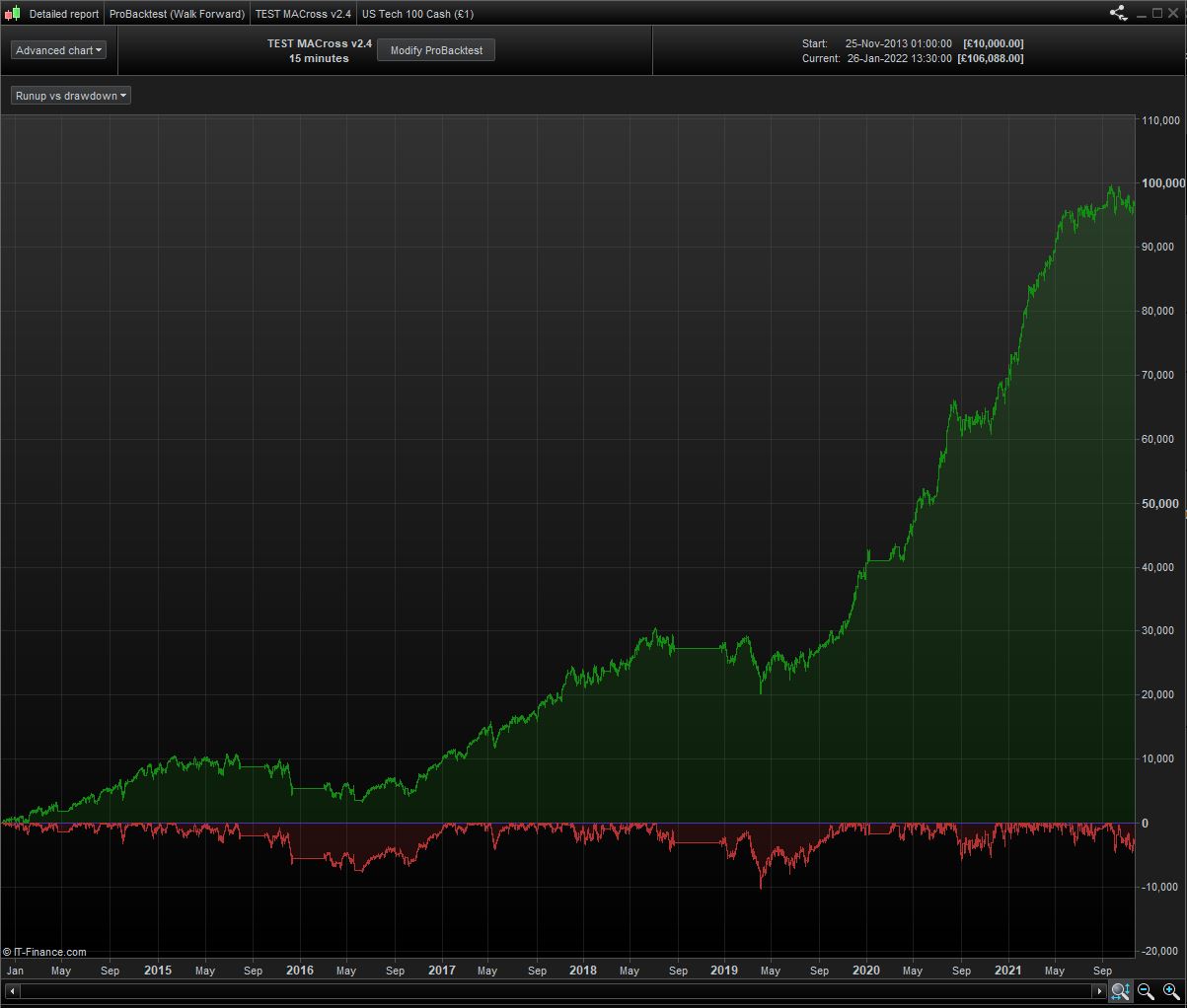

It uses a higher time frame filter to to identify an upward trending market and trades on the 15 min time frame based on an MA cross. It has been developed and optimized on 50k bars as part of a limited feasibility test, then run without any alterations on the full 200k bars and it’s still standing which shows some promise. Needs further development, draw down remains a challenge.

With thanks to robertogozzi for his break even trailing stop logic, grazie mille – https://www.prorealcode.com/topic/breakeeven-trailing-profit/

Welcome all feedback, edits and expertise – thank you and happy testing.

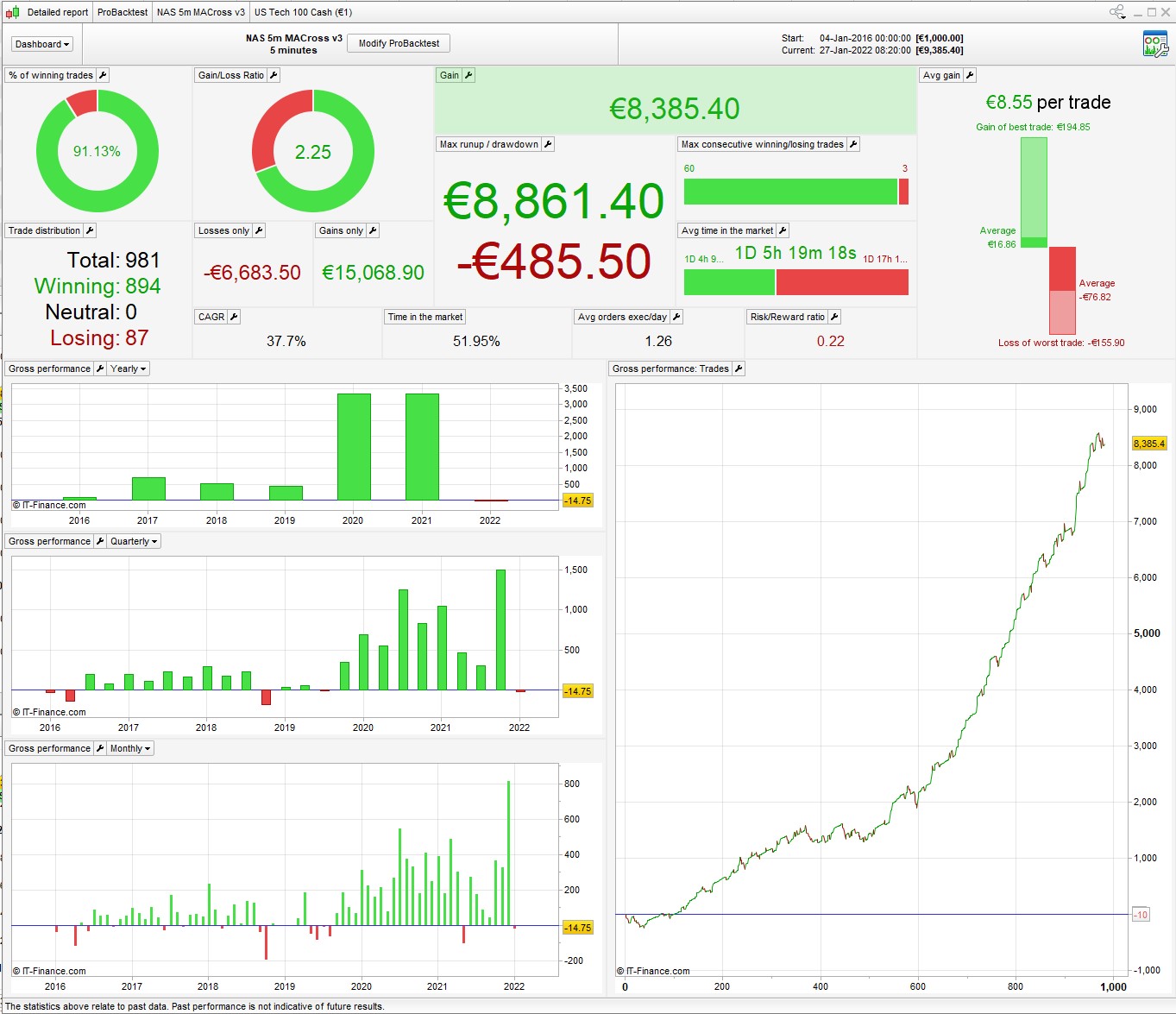

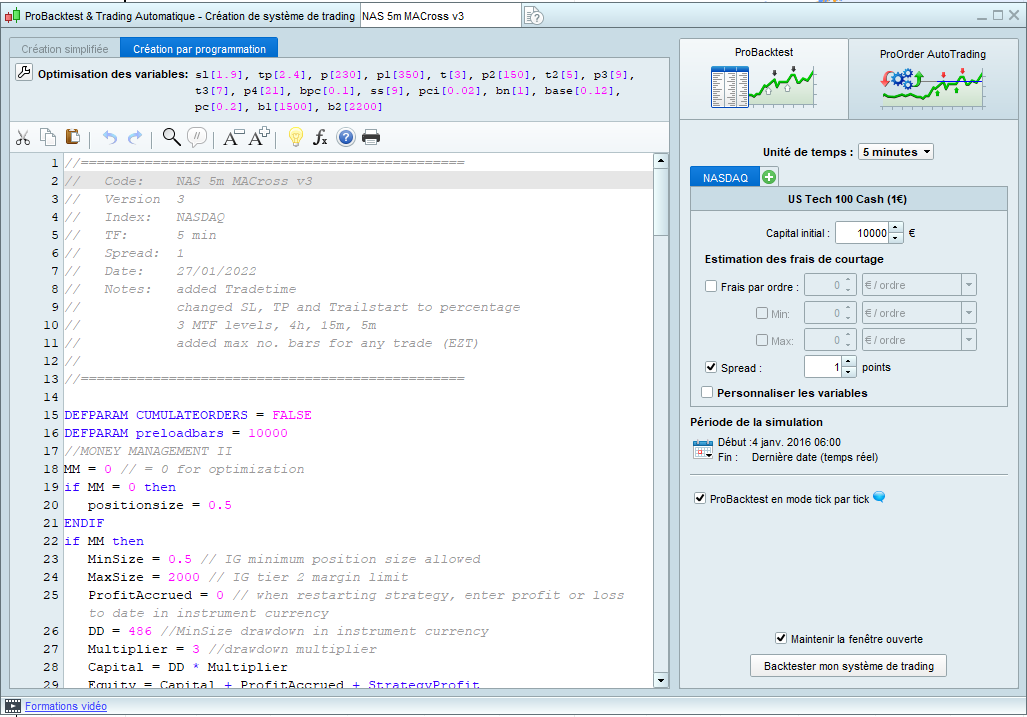

Here’s a 5m version that could be worth trying. Position size = 0.5

Optimized on a 6 year backtest, needs to run on Demo for several months of OOS testing.

I added Tradetime, changed the SL, TP and trailstart to %, added another TF

Note that I’ve tested this with a spread of 1, as I fail to see the logic of jacking up the spread for a backtest. The lowest spread for the NAS is approx 0.008 % of the tradeprice. 6 years ago a spread of 1 would have been around o.022 %, which is completely unrealistic – it wouldn’t have been that high. Raising it to 3 further distorts this.

Best would be an option to enter spread as % (also position size) but PRT haven’t got there yet.

Maybey too much Curvefitting?

you can re-optimize for the full 11 years if you feel like it.

i started out working on 1m bars but it seemed a bit dead before 2016 so I just used the last 6 years.

I’m more interested i what it does over the next 6 months than what it might have done in 2010.

Best would be an option to enter spread as % (also position size) but PRT haven’t got there yet.

What a great suggestion to be put forward to PRT … 🙂

https://www.prorealtime.com/en/contact?suggestion=1

thanked this post

@nonetheless: I’m totally with you. I’m now testing my strategies over 200000bars to see if they work. Then I optimize to last year(M5 = 75000bars) and use this. I have found that 25000bars are enough to achieve good results. A clever man here, Nicolas, Roberto or Grahal, once said… you can optimize over the full time to achieve average results and be protected from nasty surprises… or regularly readjust the strategy to always adapt to the current market situation to adjust. I think the latter works quite well.

I’ve just optimised over 200 bars only at 15 sec TF! 48 trades in 3 hours!

I am trying to get a System that will make money during this volatile madness on DJI from 14:30 to 16:00.

I’ll let you know how I get on!! 🙂

Don’t worry, in the SP500 I’m only just winning. Either stop everything and wait or move the SL further away. But then I get a stomach ache.

Test MACD Nasdaq M15

I refer to this simple strategy, which was last optimized in September. Doesn’t look so bad in today’s turbulent times.

https://www.prorealcode.com/topic/test-macd-nasdaq-m15/#post-178105

I refer to this simple strategy, which was last optimized in September. Doesn’t look so bad in today’s turbulent times.

Hi phoentzs

I like the MACD strategy you posted, it has performed well in volatile markets. Nice work, congrats

I’m surprised myself. I created some more optimized variants. All performed worse than this one after optimization. What does that tell us? The simplest is the most robust.

hello, I hope everyone is fine,

I have maybe some stupid question :

1) you tried on an instrument ( US Tech 100 Cash (1€) ) at 1€ a point, but on the Backtest you only buy half a point ?

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 0.5

ENDIF

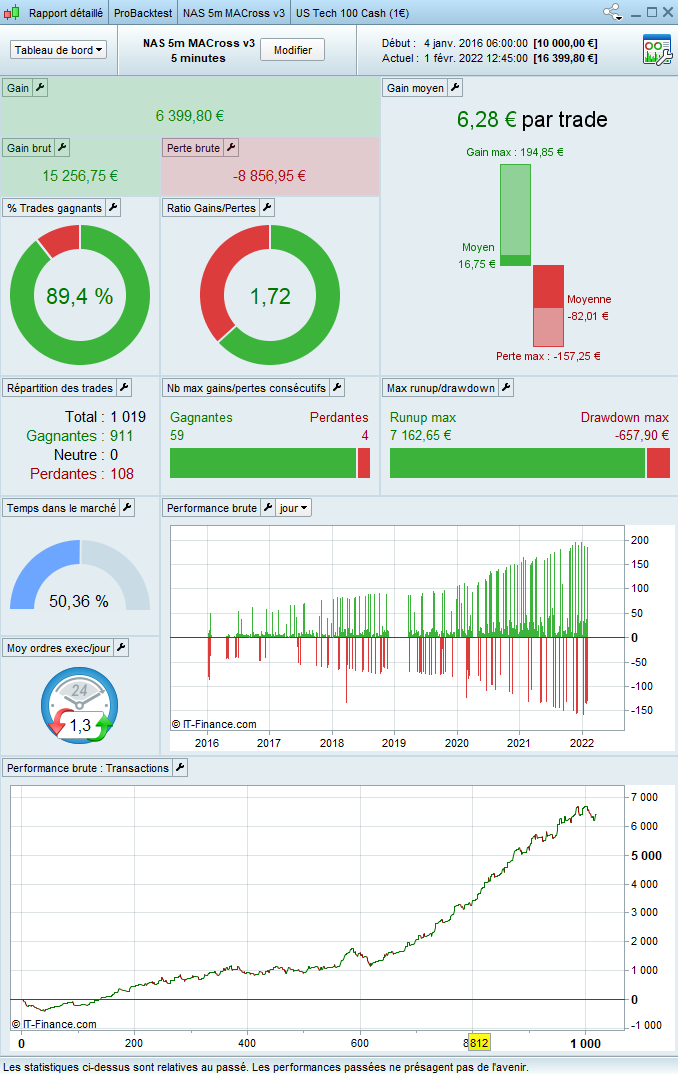

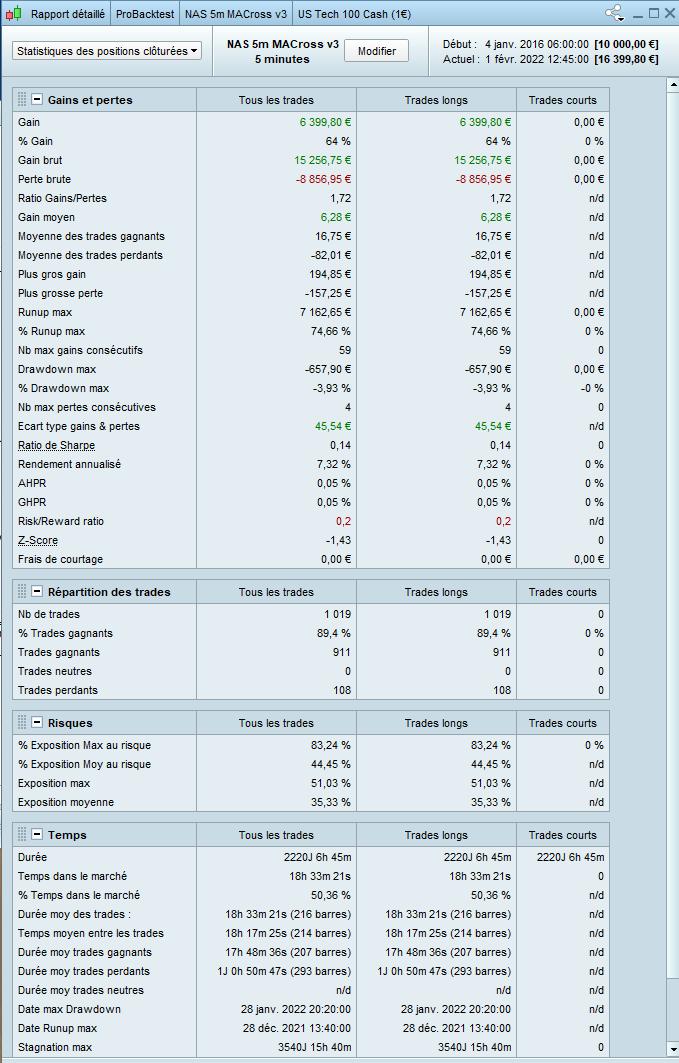

2) I do the same Backtest with 10K and the gain result is : 6399,80€ it’s mean a win % of 64% (fees included by spear of 1) on the first equity ?

I advice you don’t surprise yourself with backtest, or maybe to be sure of the robustness of your code, test Long on some sample down trends and see how it reacts or maybe try with Walk Forward strategy, and I totally agree with you the simpler the better

on the Backtest you only buy half a point ?

I do backtests at the minimum position size, in this case 0.5 pp

This is partly because the M0ney Management is based on the max drawdown @ min position size (line 26)

As for your further comments, my basic attitude is that no matter how good a backtest might look, I assume that it’s completely wrong and totally unreliable, will probably crash and burn.

Run it for months in demo, study the entries and exits – see if it behave the way you expected.

This one got off to a good start yesterday, 4 winning trades, ~400 pts.