NAS-5m-MACross-v4.1-L1.itf contains 216 lines of code.

NAS 5m MACross v4.1 L contains 288 lines of code.

Maybe there is good reason?

Oh Yes There is a very good reason :’D , i did a mistake by replacing a lot of lines by what @nonetheless have gave me. Thanks for the notice.

Also i did remove the MM code.

If i correct that, the code will be : ( no spread, MM off, 2000 capital)

// opt: 01/03/2022

//=======================================================================

DEFPARAM CUMULATEORDERS = FALSE

DEFPARAM preloadbars = 10000

//Money Management

positionsize=1

//Tradetime

//adjustment for American Daylight Savings time

ADLS =1

if ADLS then

DLS =(Date >= 20100314 and date <=20100328) or (Date >= 20101031 and date <=20101107) or (Date >= 20110313 and date <=20110327) or (Date >= 20111030 and date <=20111106) or (Date >= 20120311 and date <=20120325) or (Date >= 20121028 and date <=20121104) or (Date >= 20130310 and date <=20130331) or (Date >= 20131027 and date <=20131103) or (Date >= 20140309 and date <=20140330) or (Date >= 20141026 and date <=20141102) or (Date >= 20150308 and date <=20150329) or (Date >= 20151025 and date <=20151101) or (Date >= 20160313 and date <=20160327) or (Date >= 20161030 and date <=20161106) or (Date >= 20170312 and date <=20170326) or (Date >= 20171030 and date <=20171105) or (Date >= 20180311 and date <=20180325) or (Date >= 20181028 and date <=20181104) or (Date >= 20190310 and date <=20190331) or (Date >= 20191027 and date <=20191103) or (Date >= 20200308 and date <=20200329) or (Date >= 20201025 and date <=20201101) or (Date >= 20210314 and date <=20210328) or (Date >= 20211031 and date <=20211107) or (Date >= 20220313 and date <=20220327) or (Date >= 20221030 and date <=20221106) or (Date >= 20230312 and date <=20230326) or (Date >= 20231029 and date <=20231105) or (Date >= 20240310 and date <=20240331) or (Date >= 20241027 and date <=20241103)

If DLS then

Tradetime = time >=h1-10000 and time <h2-10000

elsif not DLS then

Tradetime = time >=h1 and time <h2

endif

endif

if not ADLS then

Tradetime = time >=h1 and time <h2

endif

//Long Entry Filter

Timeframe(4 hours)

FMA1 = average[p,t](typicalprice)

//FMA2 = average[p1,t](typicalprice)

cb1 = FMA1 > FMA1[1]

//cs1 = FMA1 < FMA2

Timeframe(15 minutes)

M15 = average[p2,t2](typicalprice)

cb2 = (close>m15)

//cs2 = close<average[p2,t2](typicalprice)

Timeframe(Default)

//Long Entry Criteria

MA1=average[p3,t3](typicalprice)

MA2=average[p4,t3](typicalprice)

cb3 = MA1 crosses over MA2

//cs3 = MA1 crosses under MA2

//Stochastic RSI | indicator

lengthRSI = lr //RSI period

lengthStoch = ls //Stochastic period

smoothK = sk //Smooth signal of stochastic RSI

smoothD = sd //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

cb4 = K>D

// Conditions to enter long positions

If Tradetime and cb1 and cb2 and cb3 and cb4 Then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

SET STOP %LOSS sl

SET TARGET %PROFIT tp

// Break even and trailing stop RTS

IF Not OnMarket THEN

// when NOT OnMarket reset values to default values

ts = (tradeprice*pc)/100 // % trailing start

TrailStart = ts //30 Start trailing profits from this point

BasePerCent = base // 0.200 20.0% Profit percentage to keep when setting BerakEven

StepSize = ss //10 Pip chunks to increase Percentage

PerCentInc = pci // 0.100 10.0% PerCent increment after each StepSize chunk

BarNumber = bn //10 Add further % so that trades don't keep running too long

BarPerCent = bpc // 0.100 10% Add this additional percentage every BarNumber bars

RoundTO = 0 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 4 * pipsize //IG minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN

//LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN

//SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

//----------------------------------------------------------------------------

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF (longonmarket and barindex-tradeindex(1)>= b1 and positionperf>0) or (longonmarket and barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf>0) or (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf<0) then

exitshort at market

endif

endif

//----------------------------------------------------------------------------

RSIexit = 1 // in profit

if RSIexit then

myrsi2=rsi[r](close)

if myrsi2<rl and barindex-tradeindex>1 and longonmarket and positionperf>0 then

sell at market

endif

if myrsi2>70 and barindex-tradeindex>1 and shortonmarket and positionperf>0 then

exitshort at market

endif

endif

//----------------------------------------------------------------------------

DSD = 1

if DSD then

once openStrongLong = 0

once openStrongShort = 0

if (time <= 120000 or time >= 170000) then // 070000, 100000

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = rok // 30

once tradeMin = tm // 1000

IF (time >= 120500) AND (time <= 120500 + tradeMin) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

once bollperiod = bp // 20

once bollMAType = 1

once s = 2

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

once trendPeriod = trp //80

once trendPeriodResume = tpr // 10

once trendGap = 4

once trendResumeGap = 4

if not onmarket then

fullySupported = 0

fullyResisted = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisted = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisted = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisted = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//Started real wrong direction

once strongTrend = st // 60

once strongPeriod = sp // 4

once strongTrendGap = stg // 2

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod - strongTrendGap then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod - strongTrendGap then

sell at market

ENDIF

endif

In my opinion, it´s sensless to do a backtest without spread, the results are falsified.

I agree with you, it’s just to help to find what’s wrong with my backtest wich is 55% less good than Nonetheless Backtest :’D

I though that, but surely the spread is in the code somehow / somewhere??

I just glanced over the code, but spread didn’t jump out at me.

Attached are the results with a constant exposure value of €10k, gives a better visual on the histogram and the curve.

I am comparing my backtest with the backtest of this “constant exposure” that i don’t know what it is. Thanks

JS

JSParticipant

Veteran

Line 223 STDDEV = STD[bollperiod]

STDDEV = STD[bollperiod] (price)

Missing the (price) ?

comparing my backtest with the backtest of this “constant exposure”

this means positionsize = 10000/close

shows performance if you had risked a constant value (€10k) rather than a constant size per point

this would definitely explain the difference you are seeing!

Thank you very much @nonetheless, I understand now the difference !

@nonetheless

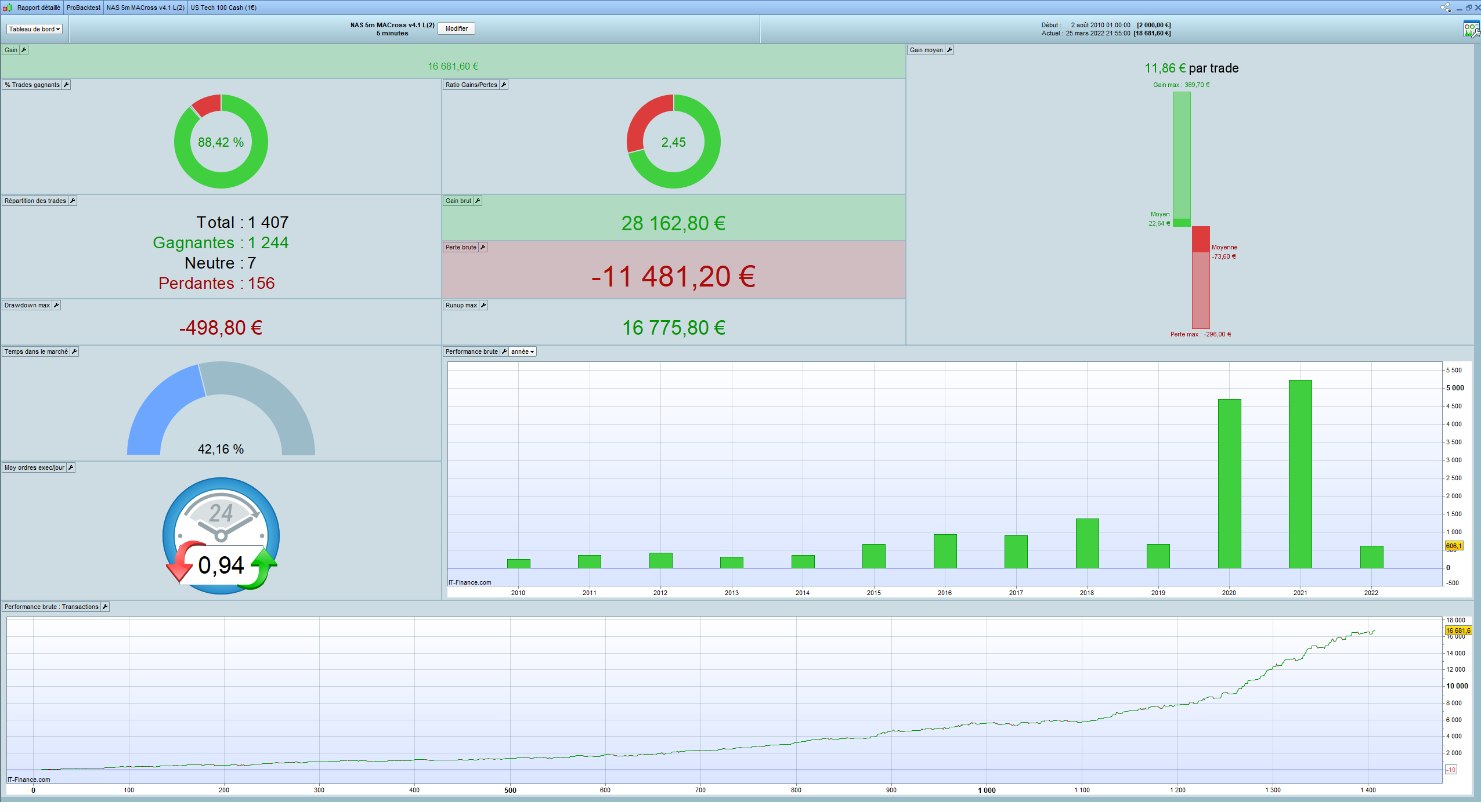

What are your experiences with this type of optimization? I see a lot of small wins and a big SL. In the report, the average gains are also much smaller than the average losses. In my experience, with such values, the strategy usually collapses in sideways phases, so it is not robust. I optimize as much as possible in such a way that the average wins are always greater than the average losses. So you still have the chance to come out plus/minus 0 in sideways phases. Hit rate is then of course lower, between 40-60%.

how do you see it?

I have some systems with only 55% win rate, but very high risk/reward, others with over 90% wins but risk/reward around .3 or so. Then I have one with the best of both worlds … but very few trades, maybe one per month. There’s always going to be a trade-off between these factors and I think the difference is largely psychological. Either can turn a profit in the long term, it depends on what you’re comfortable with.

A broker I had years ago liked to say, “No one ever went bankrupt by booking small gains” … and I guess that message stuck as I tend towards high win rate, even if the wins are small. This often means a low breakeven level and high SL that others may find makes them anxious. Personally it doesn’t bother me to carry a trade the wrong way for 1.6 or 1.8% knowing that 90% of the time it will turn around and close for a profit.

Attached is the first few weeks OOS for v4.1L, positionsize = 1

(nicely demonstrates one good thing about long-only systems: what you lose on the way down you will probably get back on the way up)

thanked this post

@nonetheless

Thanks for the information. I’ll just try it on one of my systems to achieve a high hit rate. Then I’ll try running it next to the original and compare.

Here is my humble contribution to an MA Cross system. I use SP500 here because most of my systems are based on it (many systems, little margin, little spread, portfolio building).

I solved it completely conventionally, with simple SMAs. The all-important trend seems to be the weekly trend. M15/SMA480 = D1/SMA5

Here is the system, long/short combined. Maybe there is still room for improvement?

@nonetheless

You always have a golden touch. Maybe you can take a look?

//30.03.2022 200000k

//US500 M5 Spread 0.6

//German Time

defparam preloadbars = 10000

defparam CUMULATEORDERS = false

possize = 5

timeframe(15minute, updateonclose)

RangeMAD5 = average[480,0](close) //Wochentrend Daily MA5

RangelongD5 = close > RangeMAD5

RangeshortD5 = close < RangeMAD5

RangeMAD20 = average[1920,0](close) //"Monatstrend" Daily MA20

RangelongD20 = RangeMAD5 > RangeMAD20

RangeshortD20 = RangeMAD5 < RangeMAD20

MA1 = average[x1,0](close)

MA2 = average[x2,0](close)

//MA3 = average[x3,0](close)

MA4 = average[x5,1](close)

MA5 = average[x6,1](close)

longA = MA1 > MA2 //and MA2 > MA3 //and MA2 > MA2[1]

shortA = MA4 < MA5 //and MA5 < MA5[1]

MAL1 = average[5,0](close)

MAL2 = average[15,0](close) //15

longB = MAL1 crosses over MAL2

shortB = MAL1 crosses under MAL2

timeframe(default)//M5

long = RangelongD5 and longB and longA //and RangelongD20

short = RangeshortD5 and shortB and shortA //and RangeshortD20

Exit1 = RangeshortD5

Exit2 = RangelongD5

// trading window

ONCE BuyTime = 110000

ONCE SellTime = 213000

ONCE BuyTime2 = 150000

ONCE SellTime2 = 213000

// position management

IF Time >= buyTime AND Time <= SellTime THEN

If long then //not onmarket and

BUY possize CONTRACT AT market

SET STOP %LOSS hl

SET TARGET %PROFIT gl

EndIf

endif

IF Time >= buyTime2 AND Time <= SellTime2 THEN

If short then

sellshort possize CONTRACT AT market

SET STOP %LOSS hs

SET TARGET %PROFIT gs

EndIf

endif

If longonmarket and Exit1 then

sell at market

endif

If shortonmarket and Exit2 then

exitshort at market

endif

if time = 223000 then //223000

//sell at market

exitshort at market

endif

if time = 225500 and dayofweek=5 then //225500

sell at market

exitshort at market

endif

////////////////////////////////////////

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

trailingpercentlong = startl // %

trailingpercentshort = start // %

once acceleratorlong = stepl // typically tst*0.1

once acceleratorshort= step // typically tss*0.1

ts2sensitivity = 2 // [1] close [2] high/low [3] low/high [4] typicalprice

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=(typicalprice)

ts2sensitivityshort=(typicalprice)

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong then

newsl = positionprice+trailingsteplong + 0.2

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort then

newsl = positionprice-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

if (shortonmarket and newsl > 0) or (longonmarket and newsl>0) then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

if shortonmarket then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

//////////////////////////////////////////////////////////////

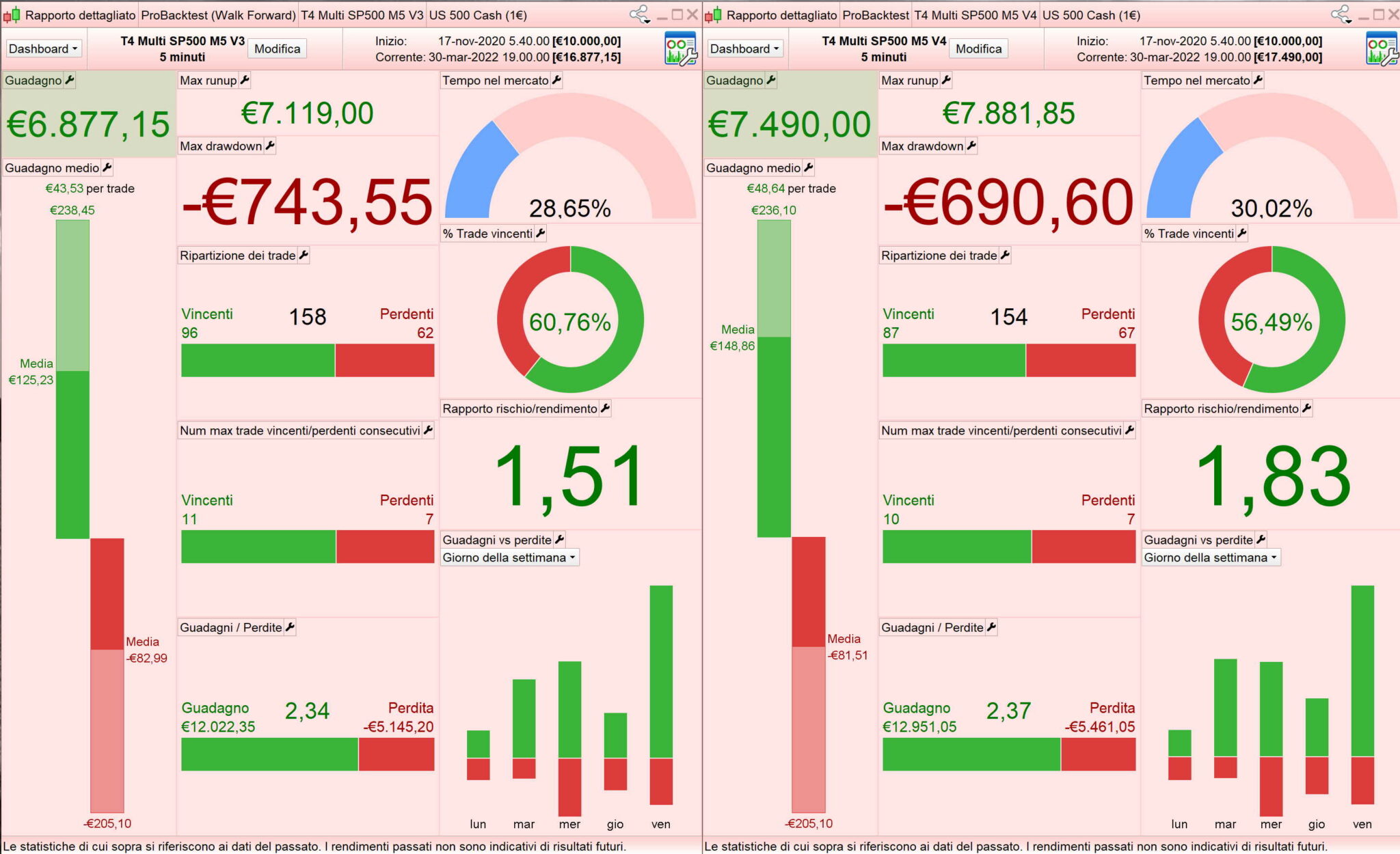

This is the same version (rewritten)of Phoentzs [ T4 -Multi -SP500 -M5-V3] , with Roberto’trailing. The performance up to 200k is slighthly better, up to 100k is better (see image).

//TS MULTI SP500 v4 - CFD 1 euro - Spread 0.6

defparam CUMULATEORDERS = false

positionSize = 5

//---------------------------------------------------------------------------------------

timeFrame(15 minute, updateOnClose) //15 minutes

avgWeekly = average[480,0](close) //weekTrend Daily

c1L = close > avgWeekly

c1S = close < avgWeekly

avg1 = average[15,0](close)

avg2 = average[55,0](close)

avg3 = average[14,1](close)

avg4 = average[20,1](close)

c2L = avg1 > avg2 //trend

c2S = avg3 < avg4

avg5 = average[5,0](close)

avg6 = average[15,0](close)

c3L = avg5 crosses over avg6 //trigger

c3S = avg5 crosses under avg6

//---------------------------------------------------------------------------------------

timeFrame(default) //5 minutes = DEFAULT

cLong = c1L and c2L and c3L

cShort = c1S and c2S and c3S

cLongExit = c1S

cShortExit = c1L

//--------------------------------------------------------------------------------------

ONCE buyTime = 110000

ONCE sellTime = 213000

ONCE buyTimeShort = 150000

ONCE sellTimeShort = 213000

//--------------------------------------------------------------------------------------

if time >= buyTime and time <= sellTime then //LONG

if cLong then

buy positionSize contract at market

endif

endif

if longOnMarket and cLongExit then

sell at market

endif

//----------------------------

if time >= buyTimeShort and time <= sellTimeShort then //SHORT

if cShort then

sellshort positionSize contract at market

endif

endif

if shortOnMarket and cShortExit then

exitShort at market

endif

//----------------------------------------------------------------------------------------

if longOnMarket then //SL & TP

set stop %loss 1.7

elsif shortOnMarket then

set stop %loss 0.5

endif

if longOnMarket then

set target %profit 1

elsif shortOnMarket then

set target %profit 1

endif

//------------------------------------------------------------------------------------

if time = 223000 then //time Exit

//sell at market

exitshort at market

endif

if time = 225500 and dayofweek=5 then

sell at market

exitshort at market

endif

//--------------------------------------------------------------------------------------------

DirectionSwitch = (LongOnMarket AND ShortOnMarket[1]) OR (LongOnMarket[1] AND ShortOnMarket) //TrP

IF Not OnMarket OR DirectionSwitch THEN

TrailStart = 40 // Start trailing profits

PointToKeep = 0.2 // 20% Profit percentage to keep when setting BreakEven

StepSize = 5 // Point to increase Percentage

PerCentInc = 0.2 // 20% PerCent increment after each StepSize Chunk

RoundTO = -0.6 //-0.5 rounds always to Lower integer, 0 defaults PRT behaviour

PriceDistance = 6* pipsize //minimun distance from current price

maxProfitL = 0

maxProfitS = 0

ProfitPerCent = PointToKeep //reset to desired default value

SellPriceX = 0

SellPrice = 0

ExitPriceX = 9999999

ExitPrice = 9999999

ELSE

IF PositionPrice <> PositionPrice[1] AND (ExitPrice + SellPrice) <> 9999999 THEN //go on only if Trailing Stop had already started trailing

IF LongOnMarket THEN

newSlL = PositionPrice + ((close - PositionPrice) * ProfitPerCent) //calculate new SL

SellPriceX = max(max(SellPriceX,SellPrice),newSlL)

SellPrice = max(max(SellPriceX,SellPrice),PositionPrice + (maxProfitL * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ELSIF ShortOnMarket THEN

newSlS = PositionPrice - ((PositionPrice - close) * ProfitPerCent)

ExitPriceX = min(min(ExitPriceX,ExitPrice),newSlS)

ExitPrice = min(min(ExitPriceX,ExitPrice),PositionPrice - (maxProfitS * pipsize))

ENDIF

ENDIF

ENDIF

//---------------------------------------------------------------------------------------------------------------------------------------------------

IF LongOnMarket AND close > (PositionPrice + (maxProfitL * pipsize)) THEN //LONG positions

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

profitL = (close - PositionPrice) / pipsize //convert price to pips

IF profitL >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - profitL) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = PointToKeep + (PointToKeep * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

maxProfitL = max(profitL * ProfitPerCent, maxProfitL)

ENDIF

ELSIF ShortOnMarket AND close < (PositionPrice - (maxProfitS * pipsize)) THEN //SHORT positions

profitS = (PositionPrice - close) / pipsize

IF profitS >= TrailStart THEN

Diff2 = abs(TrailStart - profitS)

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO))

ProfitPerCent = PointToKeep + (PointToKeep * (Chunks2 * PerCentInc))

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent))

maxProfitS = max(profitS * ProfitPerCent, maxProfitL)

ENDIF

ENDIF

//--------------------------------------------------------------------------------------------------------------------------------------------------------------

IF maxProfitL THEN //LONG positions - Place pending STOP order when maxProftiL > 0 (LONG positions)

SellPrice = max(SellPrice,PositionPrice + (maxProfitL * pipsize)) //convert pips to price

IF abs(close - SellPrice) > PriceDistance THEN

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

SELL AT Market

ENDIF

ENDIF

IF maxProfitS THEN

ExitPrice = min(ExitPrice,PositionPrice - (maxProfitS * pipsize)) //SHORT positions

IF abs(close - ExitPrice) > PriceDistance THEN

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

EXITSHORT AT Market

ENDIF

ENDIF

//------------------------------------------------------------------------------------------------------------------------

Thank you Mauro, did you really just take another trailing stop? Didn’t think it would make such a big difference.