Price distance can be set at 2 points with SP500 with a clear conscience.

There are different versions of Roberto’s Trp. I used the version on page 4 (rif: 165976): https://www.prorealcode.com/topic/breakeeven-trailing-profit/page/4/

Roberto, is there a better one for this TS?

Is there a reason why you define TP and SL outside of the if block? Is this better from the encoding or just a coding style?

looks interesting, thanks for sharing.

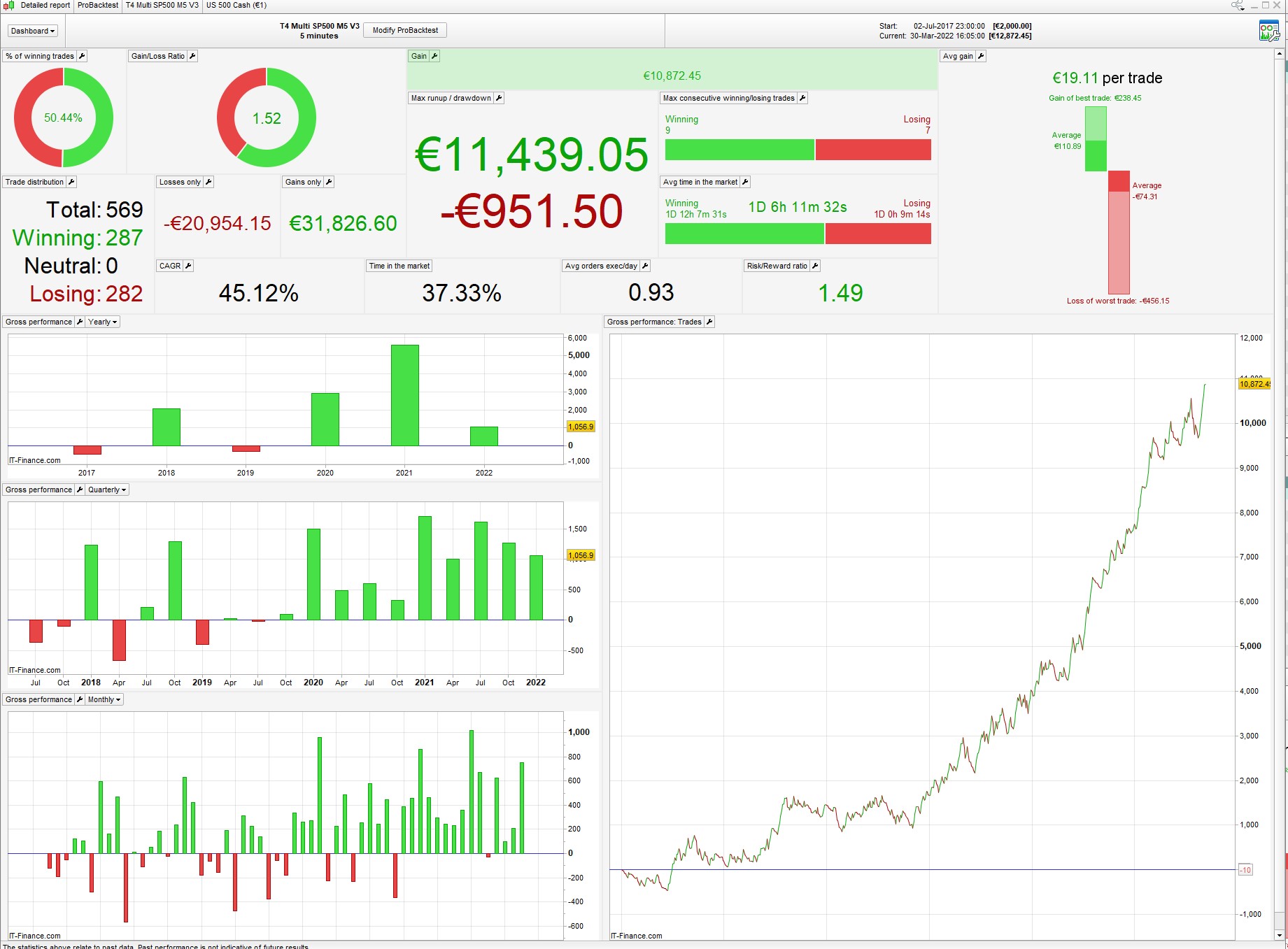

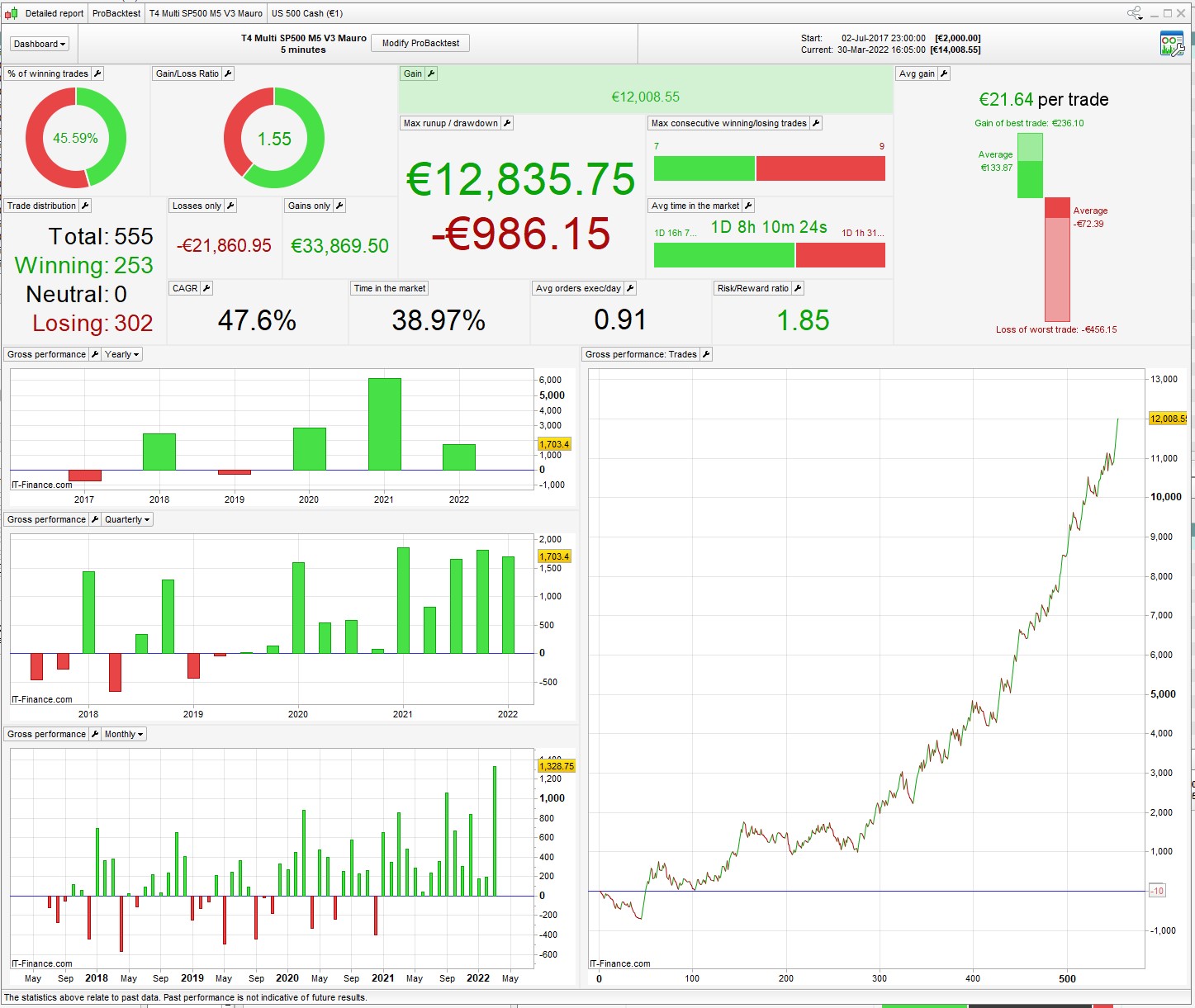

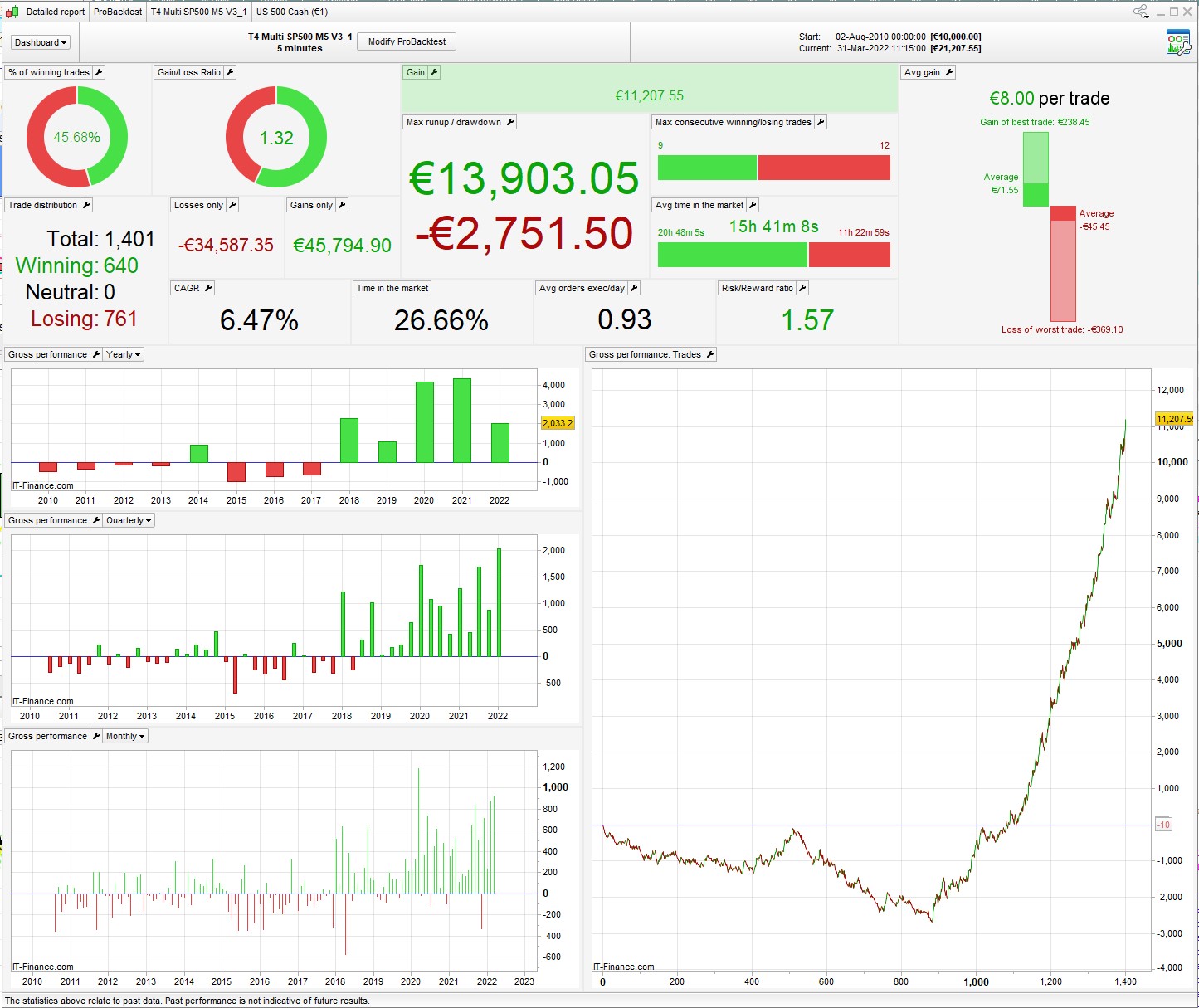

I tried reworking it on 1m bars but it’s fairly dead before 2018, so here’s a quick treatment on a 5 year backtest. Attached are results for yours and Mauro’s for that same period and you can see that they’re curve-fit to 200k

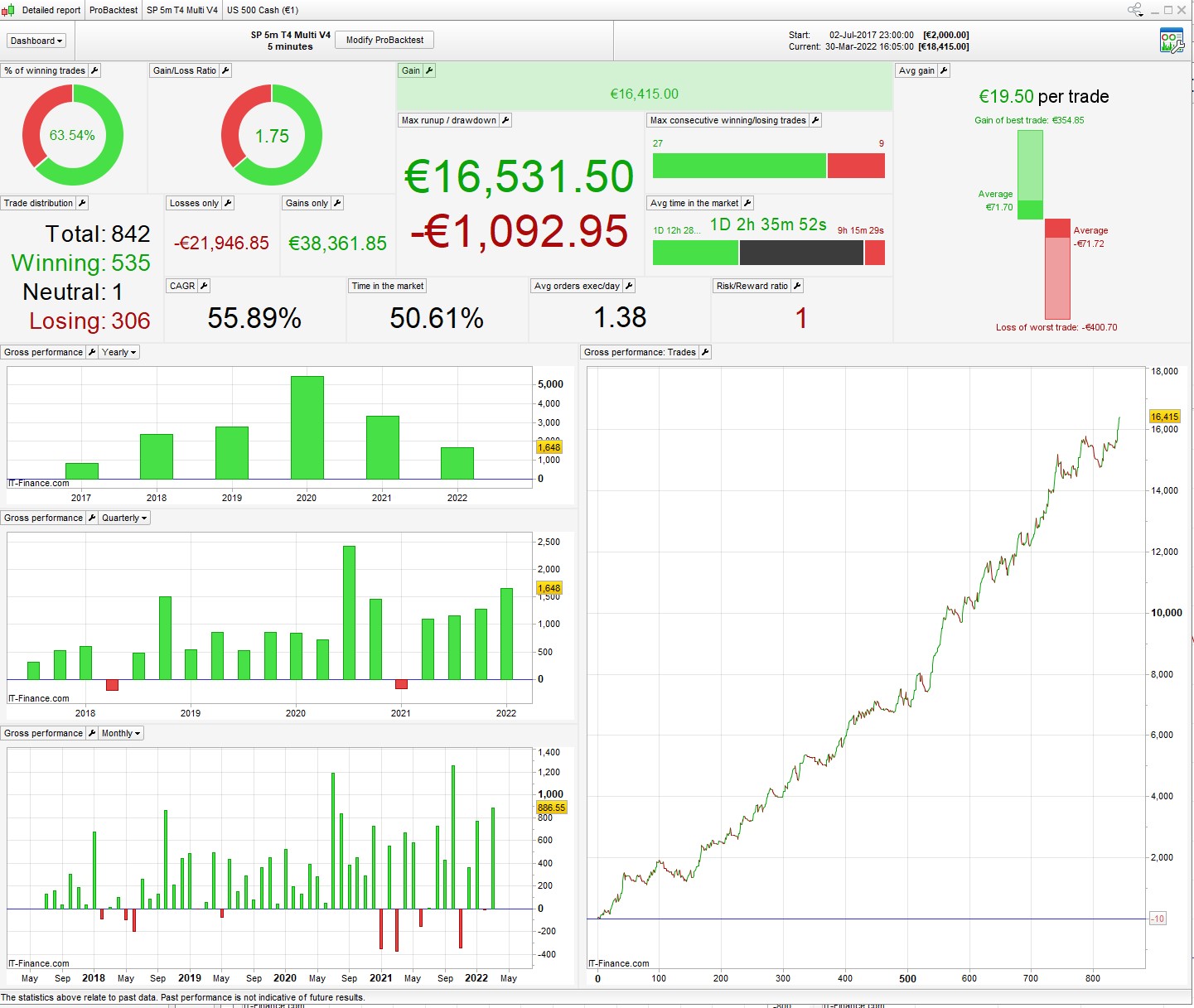

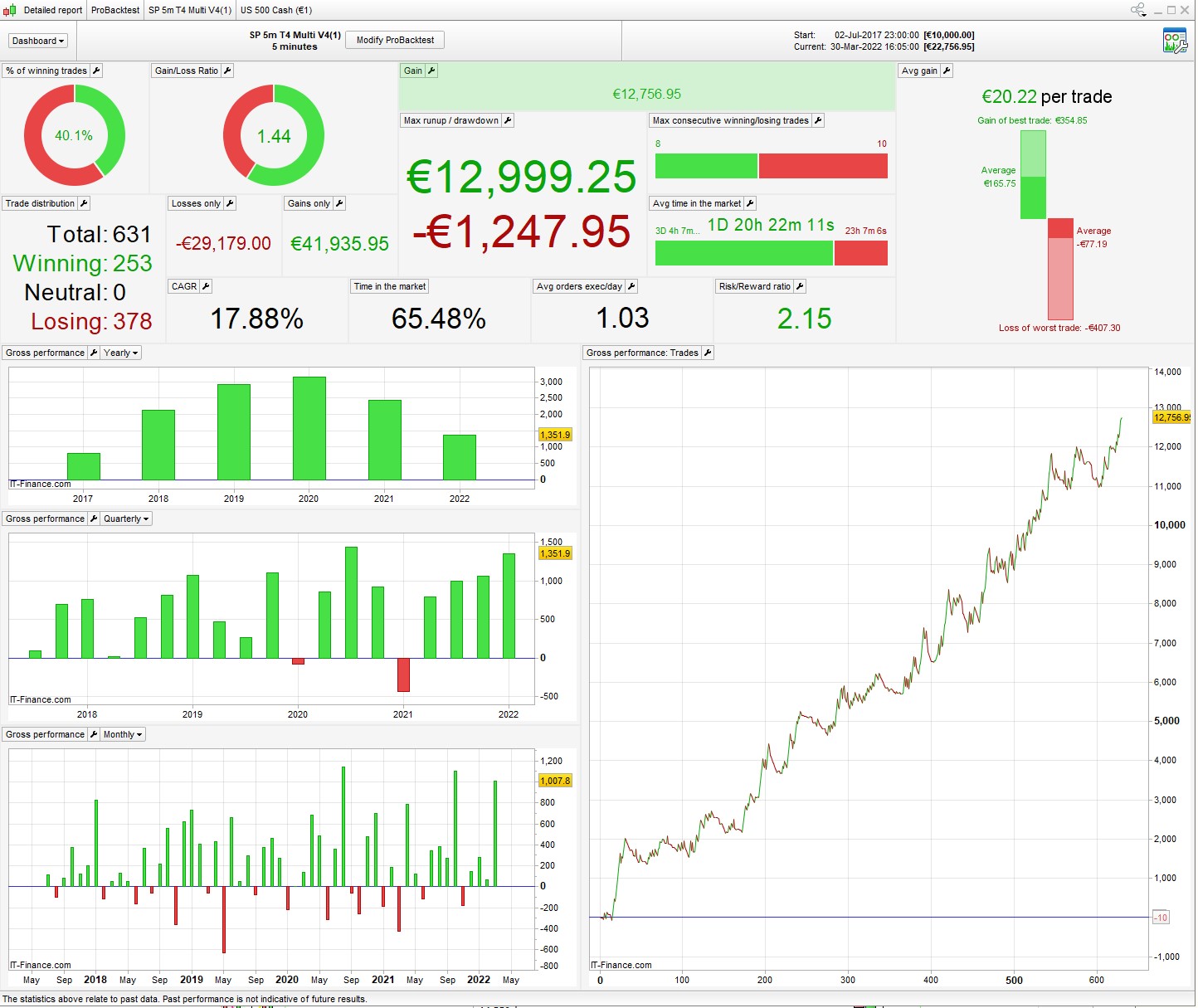

SP 5m T4 Multi v4.1 is with Roberto’s trail, but I didn’t change any of the values from Mauro’s version, so that could be worth playing with.

More room for improvement, I’m sure

It’s just a coding style, I think the code remains cleaner.

here’s the code for mine, so you can see the changes

//30.03.2022 200000k

//US500 M5 Spread 0.6

//UK Time

defparam preloadbars = 10000

defparam CUMULATEORDERS = false

possize = 5

//Tradetime

//UK time

h1 = 143000

h2 = 220000

//Euro time

//h1 = 153000

//h2 = 230000

//adjustment for American Daylight Savings time

ADLS =1

if ADLS then

DLS =(Date >= 20100314 and date <=20100328) or (Date >= 20101031 and date <=20101107) or (Date >= 20110313 and date <=20110327) or (Date >= 20111030 and date <=20111106) or (Date >= 20120311 and date <=20120325) or (Date >= 20121028 and date <=20121104) or (Date >= 20130310 and date <=20130331) or (Date >= 20131027 and date <=20131103) or (Date >= 20140309 and date <=20140330) or (Date >= 20141026 and date <=20141102) or (Date >= 20150308 and date <=20150329) or (Date >= 20151025 and date <=20151101) or (Date >= 20160313 and date <=20160327) or (Date >= 20161030 and date <=20161106) or (Date >= 20170312 and date <=20170326) or (Date >= 20171030 and date <=20171105) or (Date >= 20180311 and date <=20180325) or (Date >= 20181028 and date <=20181104) or (Date >= 20190310 and date <=20190331) or (Date >= 20191027 and date <=20191103) or (Date >= 20200308 and date <=20200329) or (Date >= 20201025 and date <=20201101) or (Date >= 20210314 and date <=20210328) or (Date >= 20211031 and date <=20211107) or (Date >= 20220313 and date <=20220327) or (Date >= 20221030 and date <=20221106) or (Date >= 20230312 and date <=20230326) or (Date >= 20231029 and date <=20231105) or (Date >= 20240310 and date <=20240331) or (Date >= 20241027 and date <=20241103)

If DLS then

Tradetime = time >=h1-10000 and time <h2-10000

elsif not DLS then

Tradetime = time >=h1 and time <h2

endif

endif

if not ADLS then

Tradetime = time >=h1 and time <h2

endif

timeframe(8 hour)

ma = average[a1,t1](typicalprice)

cb1 = ma > ma[1]

mb = average[a2,t2](typicalprice)

cs1 = mb < mb[1]

timeframe(15 minutes)

MA1 = average[x1,t3](typicalprice)

MA2 = average[x2,t3](typicalprice)

MA4 = average[x5,t5](typicalprice)

MA5 = average[x6,t5](typicalprice)

cb2 = MA1 > MA2 //and MA2 > MA3 //and MA2 > MA2[1]

cs2 = MA4 < MA5 //and MA5 < MA5[1]

timeframe(default)//M5

MAL1 = average[a7,t7](typicalprice)

MAL2 = average[a8,t7](typicalprice) //15

cb3 = MAL1 crosses over MAL2

cs3 = MAL1 crosses under MAL2

long = cb1 and cb2 and cb3 //and RangelongD20

short = cs1 and cs2 and cs3 //and RangeshortD20

// position management

IF Tradetime THEN

If long then //not onmarket and

BUY possize CONTRACT AT market

SET STOP %LOSS hl

SET TARGET %PROFIT gl

EndIf

If short then

sellshort possize CONTRACT AT market

SET STOP %LOSS hs

SET TARGET %PROFIT gs

EndIf

endif

If longonmarket and cs1 then

sell at market

endif

If shortonmarket and cb1 then

exitshort at market

endif

////////////////////////////////////////

Thank you for your work. I’ll compare in peace. But it is interesting to see that a suitable system is created with simple indicators without much magic. I think the “problem” with the Roberto Trail is that it uses points instead of percent. I suspect. And that before 2018 the S&P500 was worth half what it is today. Of course, the fluctuations were much smaller than today.

the Roberto Trail is that it uses points instead of percent

this version has a % option:

//RGTS2

ONCE RGTS2 = 1

if RGTS2 then

ONCE UseCLOSE = 0 //1=use CLOSE, 0=use High/Low

srcH = close //defaults to CLOSE

srcL = close //defaults to CLOSE

IF UseCLOSE = 0 THEN

srcH = high

srcL = low

ENDIF

ONCE UsePerCentage = 1 //0=use Pips (default), 1=use Percentages

ONCE UseEquity = 0 //0=use price (default), 1=use current Equity (initial Capital + StrategyProfit, as defined by variable MyEquity)

MyEquity = 0

DirectionSwitch = (LongOnMarket AND ShortOnMarket[1]) OR (LongOnMarket[1] AND ShortOnMarket) //True when there's been a change in the direction (likely to be due to a Stop & Reverse)

//

IF Not OnMarket OR DirectionSwitch THEN

//

// when NOT OnMarket or thare's been a change in direction, reset values to their default settings

//

StartPerCent = pc //0.25 = 0.25% to start triggering Trailing Stop (when UsePerCentage=1)

StartPerCentShort = pcs

StepPerCent = spc //50 = 50% (of the 0.25% above) as a Trailing Step (when UsePerCentage=1) (set to 100 to make StepSize=TrailStart, set to 200 to make it twice TrailStart)

//

TrailStart = 30 //30 Start trailing profits from this point (when UsePerCentage=0)

MinStart = 10 //10 Minimum value for TrailStart (when UseEquity=1, to prevent TrailStart from dropping below ZERO when Equity turns negative)

IF UsePerCentage THEN

TrailStart = (close / PipSize) * StartPerCent / 100 //use current price (CLOSE) for calculations

TrailStartShort = (close / PipSize) * StartPerCentShort / 100

IF UseEquity THEN //alternative calculations using EQUITY

TrailStart = Max(MinStart,(MyEquity / PipValue) * StartPerCent / 100) //MyEquity is the variable (feel free to use a different name) retaining your current equity

ENDIF

ENDIF

//

BasePerCent = bpc //0.08 - 0.2 Profit percentage to keep when setting BerakEven

//

StepSize = ss //5 - 15 Pip chunks to increase Percentage

IF UsePerCentage THEN

StepSize = TrailStart * StepPerCent / 100

ENDIF

//

PerCentInc = pci //0.06 - 0.14 PerCent increment after each StepSize chunk

RoundTO = rnd //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = IG * pipsize //IG minimum distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

//PositionCount = 0

SellPrice = 0

SellPriceX = 0

ExitPrice = 9999999

ExitPriceX = 9999999

ELSE

//------------------------------------------------------

// --- Update Stop Loss after accumulating new positions

//------------------------------------------------------

//PositionCount = max(PositionCount,abs(CountOfPosition))

//

// update Stop Loss only when PositionPrice has changed (actually when increased, we don't move it if there's been some positions exited)

//

//IF PositionCount <> PositionCount[1] AND (ExitPrice + SellPrice)<>9999999 THEN //go on only if Trailing Stop had already started trailing

IF PositionPrice <> PositionPrice[1] AND (ExitPrice + SellPrice) <> 9999999 THEN //go on only if Trailing Stop had already started trailing

IF LongOnMarket THEN

q1 = PositionPrice + ((srcH - PositionPrice) * ProfitPerCent) //calculate new SL

SellPriceX = max(max(SellPriceX,SellPrice),q1)

SellPrice = max(max(SellPriceX,SellPrice),PositionPrice + (y1 * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ELSIF ShortOnMarket THEN

r1 = PositionPrice - ((PositionPrice - srcL) * ProfitPerCent) //calculate new SL

ExitPriceX = min(min(ExitPriceX,ExitPrice),r1)

ExitPrice = min(min(ExitPriceX,ExitPrice),PositionPrice - (y2 * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ENDIF

ENDIF

// --- Update END

ENDIF

//

IF LongOnMarket AND srcH > (PositionPrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (srcH - PositionPrice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND srcL < (PositionPrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (PositionPrice - srcL) / pipsize //convert price to pips

IF x2 >= TrailStartShort THEN // go ahead only if N+ pips

Diff2 = abs(TrailStartShort - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

//------------------------------------------------------------------------------

// manage actual Exit, if needed

//------------------------------------------------------------------------------

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = max(SellPrice,PositionPrice + (y1 * pipsize)) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = min(ExitPrice,PositionPrice - (y2 * pipsize)) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

ENDIF

Which do you prefer? This one (Robertos) or your own, which I also use? Both of which are by Roberto in terms of construction.

I mostly use this one (above) – has a few more options and usually gives better results. I added a separate TrailStartShort as it often helps to have different values there.

I have found that separate trailing for long and short is important. But the steps must also be separate. Short trades usually have to be secured faster than long trades.

Thanks for sharing nonetheless

Agree with you that % is better than fixed. Given the change in index value over the last 2 years I tend to optimise over a more recent data set to have something more relevant going forwards.

I once again looked at my original version and installed lightweight filter …

In the H4 time frame I installed a new noTrade-filter that should prevent the strategy enters a covered or oversold market. In addition, I added an entrance timer who should find out if there is a better price after the Ma-Cross.

All small changes, but … more Profit, Smaller Drawdown.

//31.03.2022 200000k

//US500 M5 Spread 0.6

//German Time

defparam preloadbars = 10000

defparam CUMULATEORDERS = false

possize = 5

timeframe(4hour, updateonclose)

myRSI = RSI[rs](close)

noTradeL = myRSI > rso

noTradeS = myRSI < rsu

timeframe(15minute, updateonclose)

RangeMAD5 = average[480,0](close) //Wochentrend Daily MA5

RangelongD5 = close > RangeMAD5

RangeshortD5 = close < RangeMAD5

RangeMAD20 = average[1920,0](close) //"Monatstrend" Daily MA20

RangelongD20 = RangeMAD5 > RangeMAD20

RangeshortD20 = RangeMAD5 < RangeMAD20

MA1 = average[x1,0](close)

MA2 = average[x2,0](close)

//MA3 = average[x3,0](close)

MA4 = average[x5,1](close)

MA5 = average[x6,1](close)

longA = MA1 > MA2 //and MA2 > MA3 //and MA2 > MA2[1]

shortA = MA4 < MA5 //and MA5 < MA5[1]

MAL1 = average[5,0](close)

MAL2 = average[15,0](close) //15

longB = MAL1 crosses over MAL2

shortB = MAL1 crosses under MAL2

timeframe(default)//M5

long = RangelongD5 and longB[t1] and longA and not noTradeL //and RangelongD20

short = RangeshortD5 and shortB[t2] and shortA and not noTradeS //and RangeshortD20

Exit1 = RangeshortD5

Exit2 = RangelongD5

// trading window

ONCE BuyTime = 110000

ONCE SellTime = 213000

ONCE BuyTime2 = 150000

ONCE SellTime2 = 213000

// position management

IF Time >= buyTime AND Time <= SellTime THEN

If long then //not onmarket and

BUY possize CONTRACT AT market

SET STOP %LOSS hl

SET TARGET %PROFIT gl

EndIf

endif

IF Time >= buyTime2 AND Time <= SellTime2 THEN

If short then

sellshort possize CONTRACT AT market

SET STOP %LOSS hs

SET TARGET %PROFIT gs

EndIf

endif

If longonmarket and Exit1 then

sell at market

endif

If shortonmarket and Exit2 then

exitshort at market

endif

if time = 223000 then //223000

//sell at market

exitshort at market

endif

if time = 225500 and dayofweek=5 then //225500

sell at market

exitshort at market

endif

////////////////////////////////////////

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

trailingpercentlong = startl // %

trailingpercentshort = start // %

once acceleratorlong = stepl // typically tst*0.1

once acceleratorshort= step // typically tss*0.1

ts2sensitivity = 2 // [1] close [2] high/low [3] low/high [4] typicalprice

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=(typicalprice)

ts2sensitivityshort=(typicalprice)

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong then

newsl = positionprice+trailingsteplong + 0.2

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort then

newsl = positionprice-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

if (shortonmarket and newsl > 0) or (longonmarket and newsl>0) then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

if shortonmarket then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

//////////////////////////////////////////////////////////////

thanked this post

I expect you’ve decided that you don’t really care what happened before your test period, but just in case you’re curious: