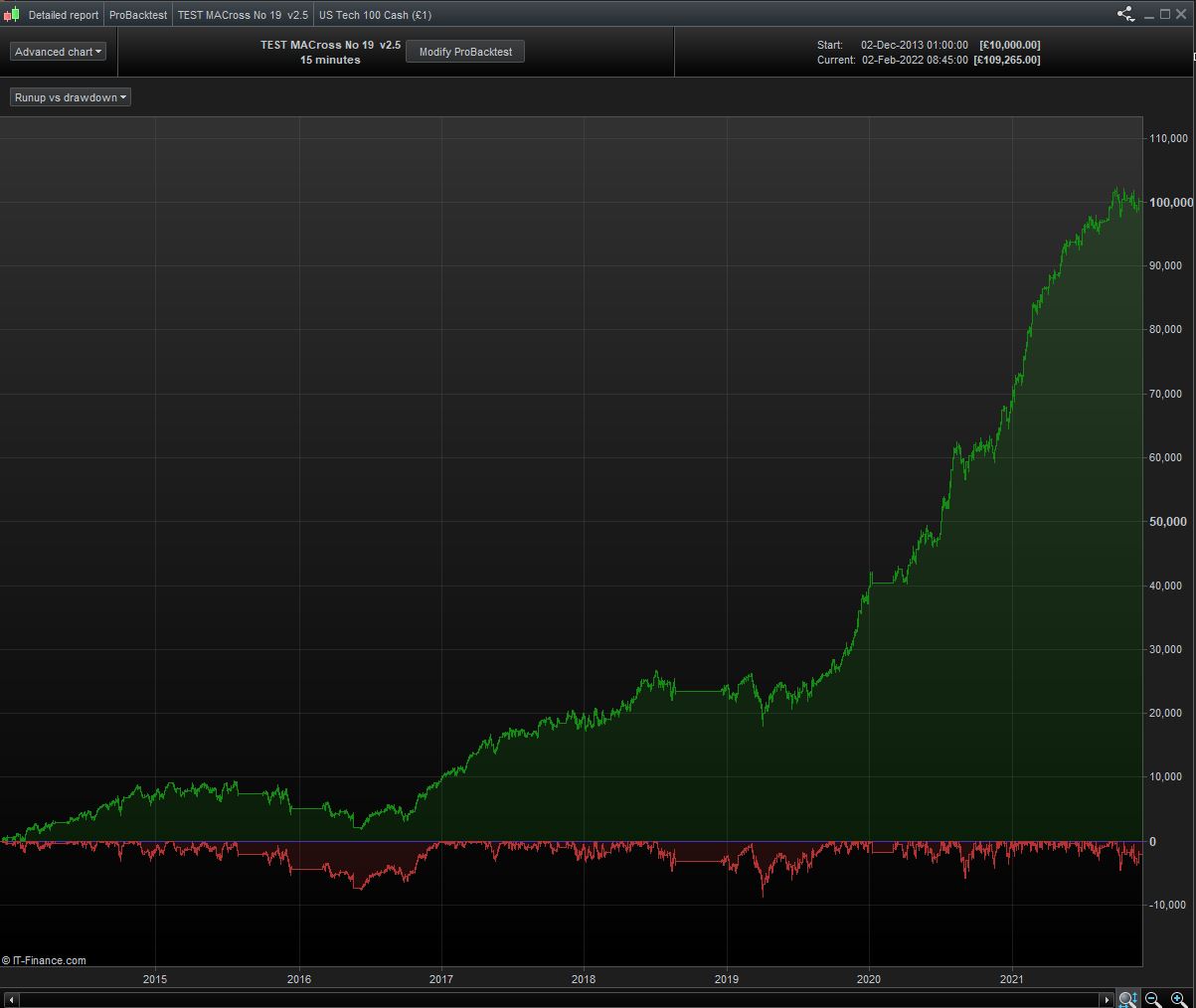

Have added a volatility filter to the original 15 min version, which was optimized over the last 50k bars. Reduces draw down and increases performance so net happy with this minor addition. Will rerun the Walk Forward process but expect little change.

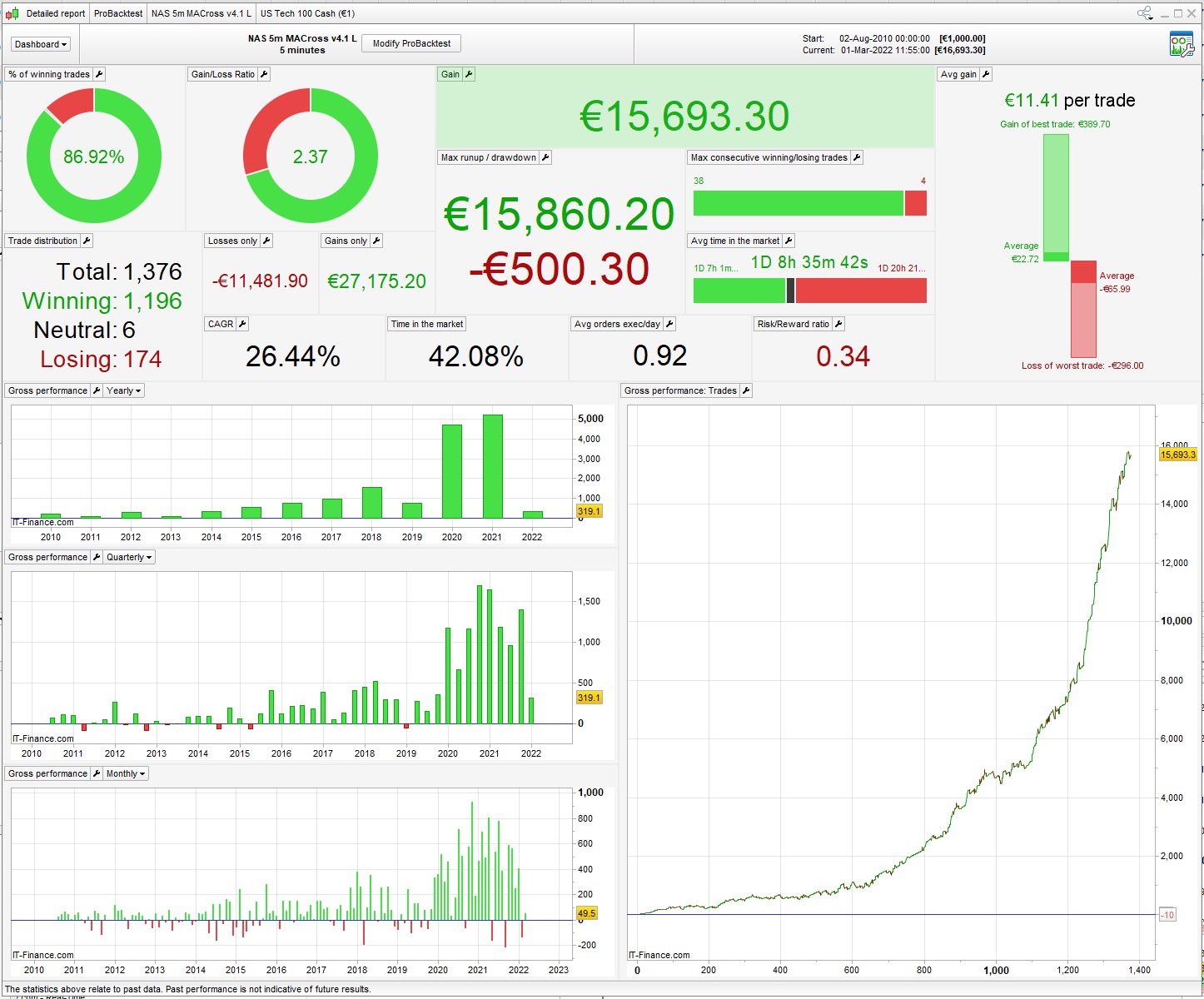

Am also testing the 5 min version which nonetheless kindly posted as this too looks very promising.

I advice you don’t surprise yourself with backtest, or maybe to be sure of the robustness of your code, test Long on some sample down trends and see how it reacts or maybe try with Walk Forward strategy, and I totally agree with you the simpler the better

this answer is for phoentzs, sorry

on the Backtest you only buy half a point ?

I do backtests at the minimum position size, in this case 0.5 pp

This is partly because the M0ney Management is based on the max drawdown @ min position size (line 26)

As for your further comments, my basic attitude is that no matter how good a backtest might look, I assume that it’s completely wrong and totally unreliable, will probably crash and burn.

Run it for months in demo, study the entries and exits – see if it behave the way you expected.

This one got off to a good start yesterday, 4 winning trades, ~400 pts.

maybe you can try to optimise with the Walk Forward method, it’s maybe will help you, I will study if in the future deeply maybe, now I’m not at this level

@samsampop

I haven’t a chance to run your new version but one thing you should change is line 69, should be:

PriceDistance = 4 * pipsize

this is the IG minimum stop distance, so it will change from one instrument to the next.

thanked this post

Quick update – strategy has stayed out of the market since Jan 20th and good job too for a long only strategy.

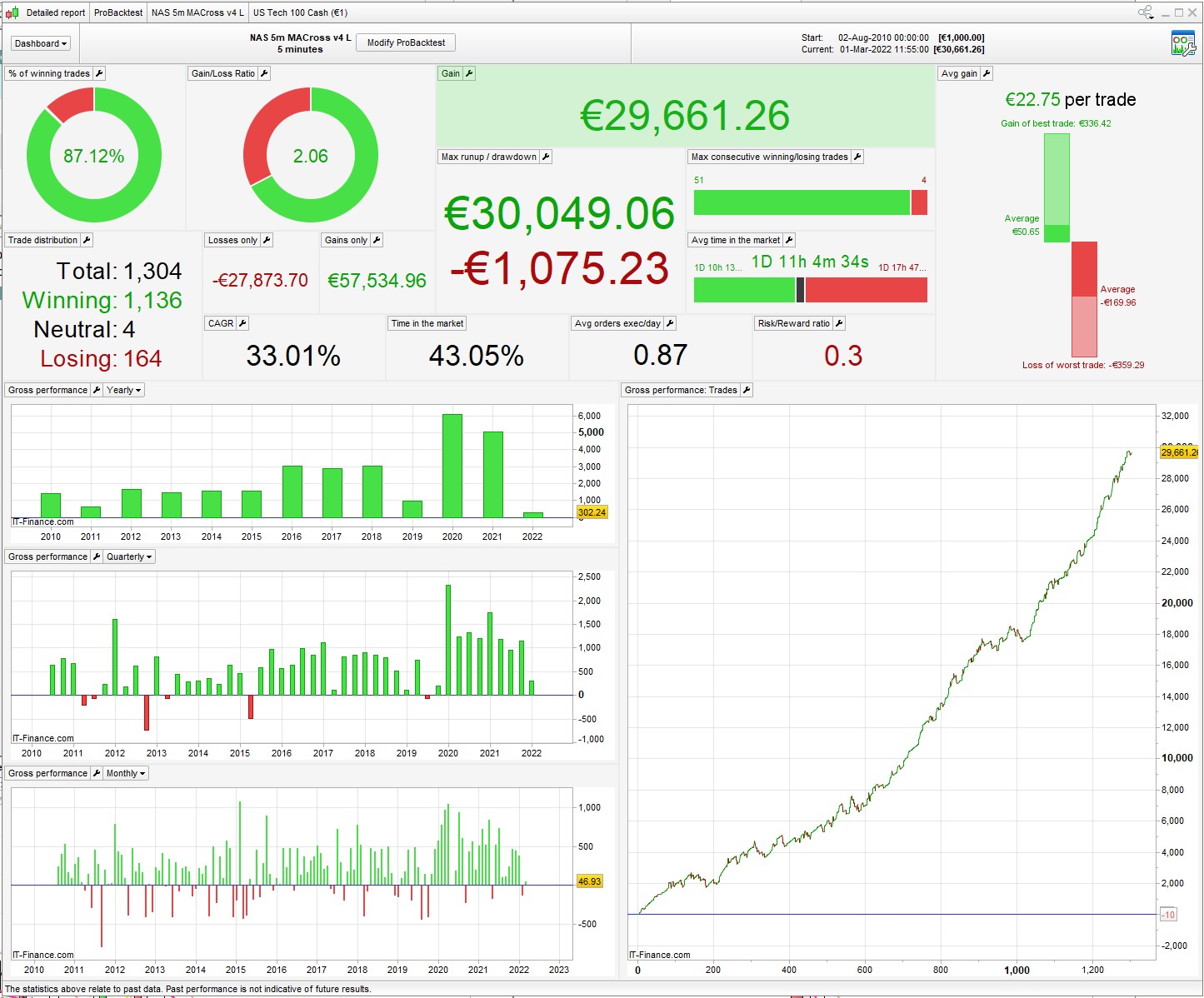

here’s a revised 5m version – better long term performance with lower drawdown, positionsize = 1

altered the 4h filter and added StochasticRSI

took one loss in Feb, but otherwise managed the Ukraine mess fairly well (so far)

Hi nonetheless

Quick question if I may – how often would you re-optimize the variables for this latest strategy that you have kindly posted?

Thanks very much

I don’t have a fixed policy on that. I rework things as and when I have an idea that might improve some aspect. Obviously, if you’re optimizing on max data on a 12 year backtest you’d hope that those numbers would be worth keeping. Someone else might keep the basic structure of the algo but optimize for maybe 6 years where most of the profit has been made – I guess then you’d want to refresh it more often. Who knows … 🤔

thanked this post

thank you very much for your contribution nonetheless. I quickly looked at the code and tested to remove all code after trailing. was basically the same result.

the 3 functions after the trail are standard bits of code that i add to most algos, the effect varies from one to the next. In this case they collectively add about 3%

If you’d rather not have an extra 3% then I suggest you switch them off immediately 😁

Attached are the results with a constant exposure value of €10k, gives a better visual on the histogram and the curve.

Hello @nonetheless, than you for your work. I am really confused, i’am not having same backtest as you, I am using V4.1 L, and i have add 1h at h1 and h2 because i’m in France. Can you share with us the last itf you have. Thank you very much.

I haven’t done any other work on that one, so v4.1L is the only itf I have. How much discrepancy are you seeing?

@nonetheless Here is my backtest for the same period and Position size 1 MM off so you can see the huge difference :’D . I added also the parametres. Thanks for you help.

the only thing i can think of is the time settings in the DSD section. Try it like this, allowing for the Euro time difference

DSD = 1

if DSD then

once openStrongLong = 0

once openStrongShort = 0

if (time <= 120000 or time >= 170000) then // 070000, 100000

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = rok // 30

once tradeMin = tm // 1000

IF (time >= 120500) AND (time <= 120500 + tradeMin) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

Thank you, it ads a bit of amelioration but still not that great performance that you have.

This is my code, no spread for this backtest, no MM, parametres are the same.

I’m ready to change the time zone for PRT if it will improve my results.

If you can’t see any solution. I will not be a problem. I am already grateful for your contribution.

Thanks

// opt: 01/03/2022

//=======================================================================

DEFPARAM CUMULATEORDERS = FALSE

DEFPARAM preloadbars = 10000

positionsize = 1

//Tradetime

//adjustment for American Daylight Savings time

ADLS =1

if ADLS then

DLS =(Date >= 20100314 and date <=20100328) or (Date >= 20101031 and date <=20101107) or (Date >= 20110313 and date <=20110327) or (Date >= 20111030 and date <=20111106) or (Date >= 20120311 and date <=20120325) or (Date >= 20121028 and date <=20121104) or (Date >= 20130310 and date <=20130331) or (Date >= 20131027 and date <=20131103) or (Date >= 20140309 and date <=20140330) or (Date >= 20141026 and date <=20141102) or (Date >= 20150308 and date <=20150329) or (Date >= 20151025 and date <=20151101) or (Date >= 20160313 and date <=20160327) or (Date >= 20161030 and date <=20161106) or (Date >= 20170312 and date <=20170326) or (Date >= 20171030 and date <=20171105) or (Date >= 20180311 and date <=20180325) or (Date >= 20181028 and date <=20181104) or (Date >= 20190310 and date <=20190331) or (Date >= 20191027 and date <=20191103) or (Date >= 20200308 and date <=20200329) or (Date >= 20201025 and date <=20201101) or (Date >= 20210314 and date <=20210328) or (Date >= 20211031 and date <=20211107) or (Date >= 20220313 and date <=20220327) or (Date >= 20221030 and date <=20221106) or (Date >= 20230312 and date <=20230326) or (Date >= 20231029 and date <=20231105) or (Date >= 20240310 and date <=20240331) or (Date >= 20241027 and date <=20241103)

If DLS then

Tradetime = time >=h1-10000 and time <h2-10000

elsif not DLS then

Tradetime = time >=h1 and time <h2

endif

endif

if not ADLS then

Tradetime = time >=h1 and time <h2

endif

//Long Entry Filter

Timeframe(4 hours)

FMA1 = average[p,t](typicalprice)

//FMA2 = average[p1,t](typicalprice)

cb1 = FMA1 > FMA1[1]

//cs1 = FMA1 < FMA2

Timeframe(15 minutes)

M15 = average[p2,t2](typicalprice)

cb2 = (close>m15)

//cs2 = close<average[p2,t2](typicalprice)

Timeframe(Default)

//Long Entry Criteria

MA1=average[p3,t3](typicalprice)

MA2=average[p4,t3](typicalprice)

cb3 = MA1 crosses over MA2

//cs3 = MA1 crosses under MA2

//Stochastic RSI | indicator

lengthRSI = lr //RSI period

lengthStoch = ls //Stochastic period

smoothK = sk //Smooth signal of stochastic RSI

smoothD = sd //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

cb4 = K>D

// Conditions to enter long positions

If Tradetime and cb1 and cb2 and cb3 and cb4 Then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

SET STOP %LOSS sl

SET TARGET %PROFIT tp

// Break even and trailing stop RTS

IF Not OnMarket THEN

// when NOT OnMarket reset values to default values

ts = (tradeprice*pc)/100 // % trailing start

TrailStart = ts //30 Start trailing profits from this point

BasePerCent = base // 0.200 20.0% Profit percentage to keep when setting BerakEven

StepSize = ss //10 Pip chunks to increase Percentage

PerCentInc = pci // 0.100 10.0% PerCent increment after each StepSize chunk

BarNumber = bn //10 Add further % so that trades don't keep running too long

BarPerCent = bpc // 0.100 10% Add this additional percentage every BarNumber bars

RoundTO = 0 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 4 * pipsize //IG minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN

//LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN

//SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

//----------------------------------------------------------------------------

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF (longonmarket and barindex-tradeindex(1)>= b1 and positionperf>0) or (longonmarket and barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf>0) or (shortonmarket and barindex-tradeindex(1)>= 4000 and positionperf<0) then

exitshort at market

endif

endif

//----------------------------------------------------------------------------

RSIexit = 1 // in profit

if RSIexit then

myrsi2=rsi[r](close)

if myrsi2<rl and barindex-tradeindex>1 and longonmarket and positionperf>0 then

sell at market

endif

if myrsi2>70 and barindex-tradeindex>1 and shortonmarket and positionperf>0 then

exitshort at market

endif

endif

//----------------------------------------------------------------------------

DSD = 1

if DSD then

once openStrongLong = 0

once openStrongShort = 0

if (time <= 120000 or time >= 170000) then // 070000, 100000

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = rok // 30

once tradeMin = tm // 1000

IF (time >= 120500) AND (time <= 120500 + tradeMin) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

ENDIF