Thanks @ProRealAlgos

I don’t know if you receive my Email but I do a trial, but all the PRA+ algos doesn’t work on my plateform ?

Does someone have the same problem ?

Thanks

Hi Zilliq,

Which issue are you having? Could you provide a screenshot of any error message or such?

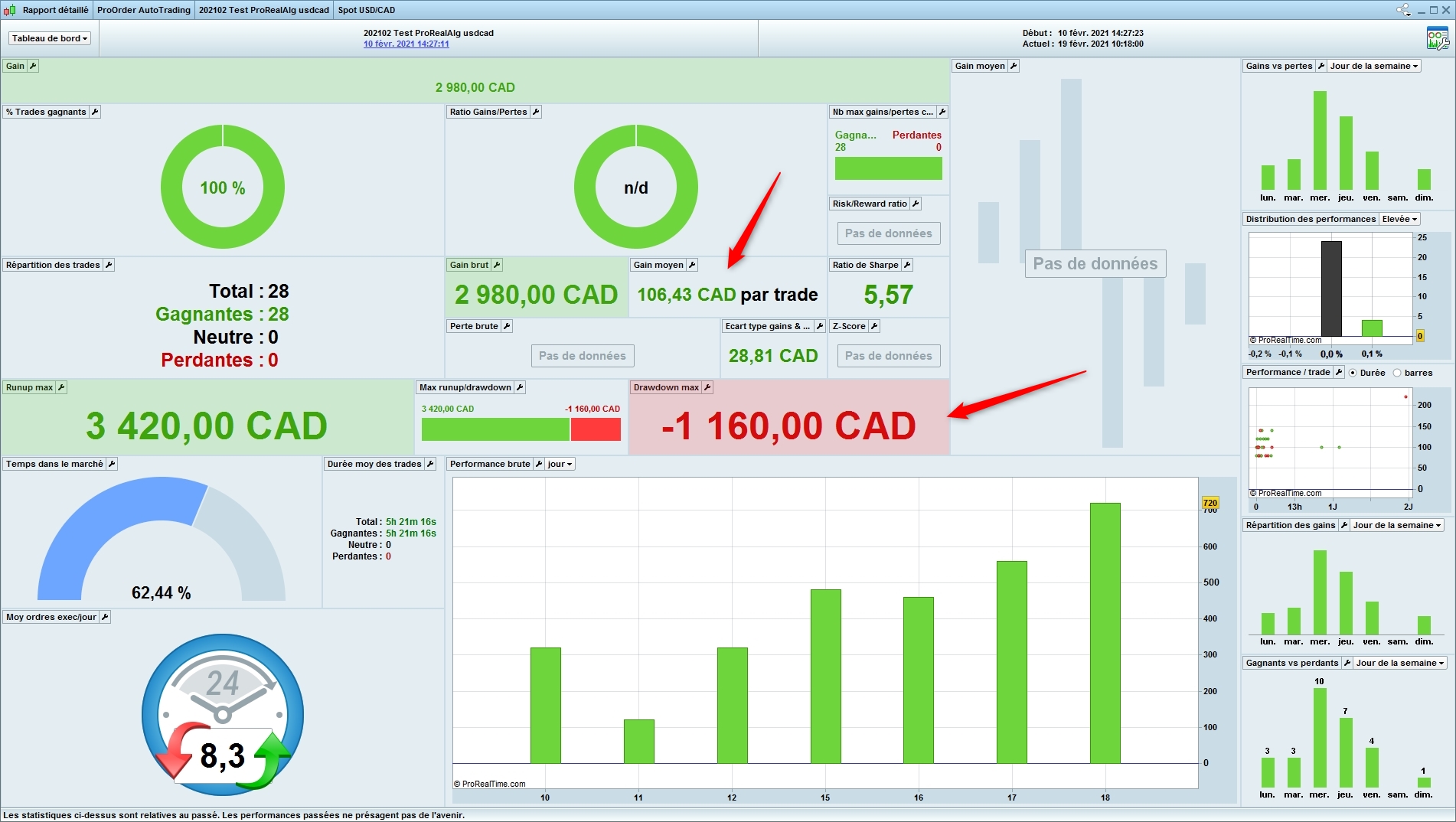

All my Trial PRA+ Algos traded … see attached.

Hi Grahal,

Thanks for sharing!

One could look at that image and think that the results for these 3 weeks were really bad. We don’t want to come across as being defensive , but I just want to clarify a few things so you don’t think that we forged the presented results.

- In the image I see that most algos were started in the end of the first week. Some of the big gains for this trial period came in the first 3-4 days of the first week of this trial.

- The 10 PRA+ algos had significant lesser gains than the 10 original algos that you haven’t started.

- I see that the position sizes differ from what we recommend. We recommend using factorized position sizes i.e. to set position size so that the risk is equally divided by the algos.

I will use the same example as I did earlier in the thread: Running 1 contract on DOW at ~30000 is a 15 times bigger position size than running 1 contract on OMX at ~2000

Please let us know if you have any questions.

So what has happened since the trial ended? These are the results from 2 weeks back.

Thanks @ProRealAlgos

Do you have the maxdrawdown/runup picture during this time ?

Thanks

@ProRealAlgos

Your algos seems to work well on Forex too. Good job !

The problem for me is the ratio between gain and max drawdown who is big

If the stop is reach, we need to have 10 win to compensate (for one loss)

Have a nice day

Zilliq

That means the win-rate has to be a minimum of 90% in order to have a profitable system right?

Is that the same for all their algos?

Yes we can say that

The problem is that with a backtest with a very good ratio win/loss as on this test we could think it works very well (And it could !)

But with a small ratio Win per trade / Max DD, that means that if you’re stop you need to win 10 times in a row to compensate this loss

Personnaly I think it’s dangerous but it’s only my opinion and thanks to share

A 50% win rate is fine if you win £51 with the winning bets and lose £50 with the losing bets – just as a 90% win rate strategy is fine if you win £91 with the winning bets and lose £90 with the losing bets.

The outcome is the same as long as your strategy has at least a £1 edge!

What will kill any strategy or group of strategies is a bank too small to cope with a run of losers no matter what the win rate is.

Perfect example

ONE lose, and it’s possible to lose all previous winning trades 🙁

Win/lose ratio is a good indicator but not the most important 😉

Bye and thanks

Perfect example

Not really as 8 trades is a terrible small sample size to base any decision as to whether a strategy has failed or not on.

Bye and thanks.

The small size is not really the point.

I was just to say that with one loss we can lose all and need 10 new wins to compensate, even with a good win/loss ratio

Have a nice week-end and thanks for your comment

A 50% win rate is fine if you win £51 with the winning bets and lose £50 with the losing bets – just as a 90% win rate strategy is fine if you win £91 with the winning bets and lose £90 with the losing bets.

The outcome is the same as long as your strategy has at least a £1 edge!

What will kill any strategy or group of strategies is a bank too small to cope with a run of losers no matter what the win rate is.

Yes, but I think the mental aspect of this should not be ignored. Imagine you spend a lot of money buying an algorithm with a higher win rate (like 90%). You start off with a loss, let´s say you lose €800. You then have to get 9 straight wins (€100 each) in order to be in a profit. It could also happen you get a 2nd loss early on. Then you might need 15 straight wins in order to get breakeven.

This could be a demanding task for the mind, especially if you in addition to be in minus also has spend money for the strategy.

with one loss we can lose all and need 10 new wins to compensate

So now that would be 18 trades with 17 winners and 1 loser and we haven’t lost any money. Doesn’t sound like too bad an outcome to me so far.

Mattias – A strategy with a high win rate with small wins and big losses is as stressful as a strategy with a low win rate and big wins and small losses. In one you get one or two big losses in a row that might make you panic and in the other you get ten or twenty small losses in a row that add up to a big loss that might make you panic. The important thing to keep your eye on is that in the long run the strategy makes more than it loses.

Put a stop loss close to the entry price and you will hit a lot of small losers but put a stop loss miles from an entry price and you will hardly see a loser but it will be a big one when you do see it. The risk and reward are directly correlated to the distance so our only challenge when trading is to beat the spread that puts us at a disadvantage as soon as we enter a trade.

Vonasi, yes, well said. But for me, I strive for the middle way, between those two you mention. Where the draw-down is slow and small, and the win-rate is not extreme in any way. This is of course subjective, but I think if you sell strategies, you should be very clear about these things to your customers, letting them know what kind of strategy it is, draw-downs, how it deals with e.g. with a Feb/March 2020-situation etc.

Perfect example

But are you using the strategy on the instrument and timeframe it was made for?