Brage,

as requested for play around please find attached itf-file for Pathfinder OMX 4H V5B2.

best, Reiner

Thanks again Reiner!

But when backtesting with the file you attached, I don’t get even close to the results you showed me before on OMX. What am I doing wrong?

Brage, I’m confused. I imported the itf file from above and with OMX mini 20 SEK the backtest shows the attached result.

Here is the used code:

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 2

// Instrument: OMX mini 4H, 8-22 CET, 1.5 points spread, account size 100.000 SEK

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 210

ONCE periodShortMA = 10

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 2 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 5 // in %

ONCE stopLossShort = 3.25 // in %

ONCE takeProfitLong = 3.25 // in %

ONCE takeProfitShort = 2 // in %

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(15, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 2.75 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.4 // in %

ONCE maxCandlesLongWithProfit = 21 // take long profit latest after 21 candles

ONCE maxCandlesShortWithProfit = 12 // take short profit latest after 12 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 3 // limit short loss latest after 3 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 3

ONCE February = 3

ONCE March = 1

ONCE April = 3

ONCE May = 1

ONCE June = 2

ONCE July = 3

ONCE August = -2

ONCE September = -2

ONCE October = 3

ONCE November = 1

ONCE December = 3

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

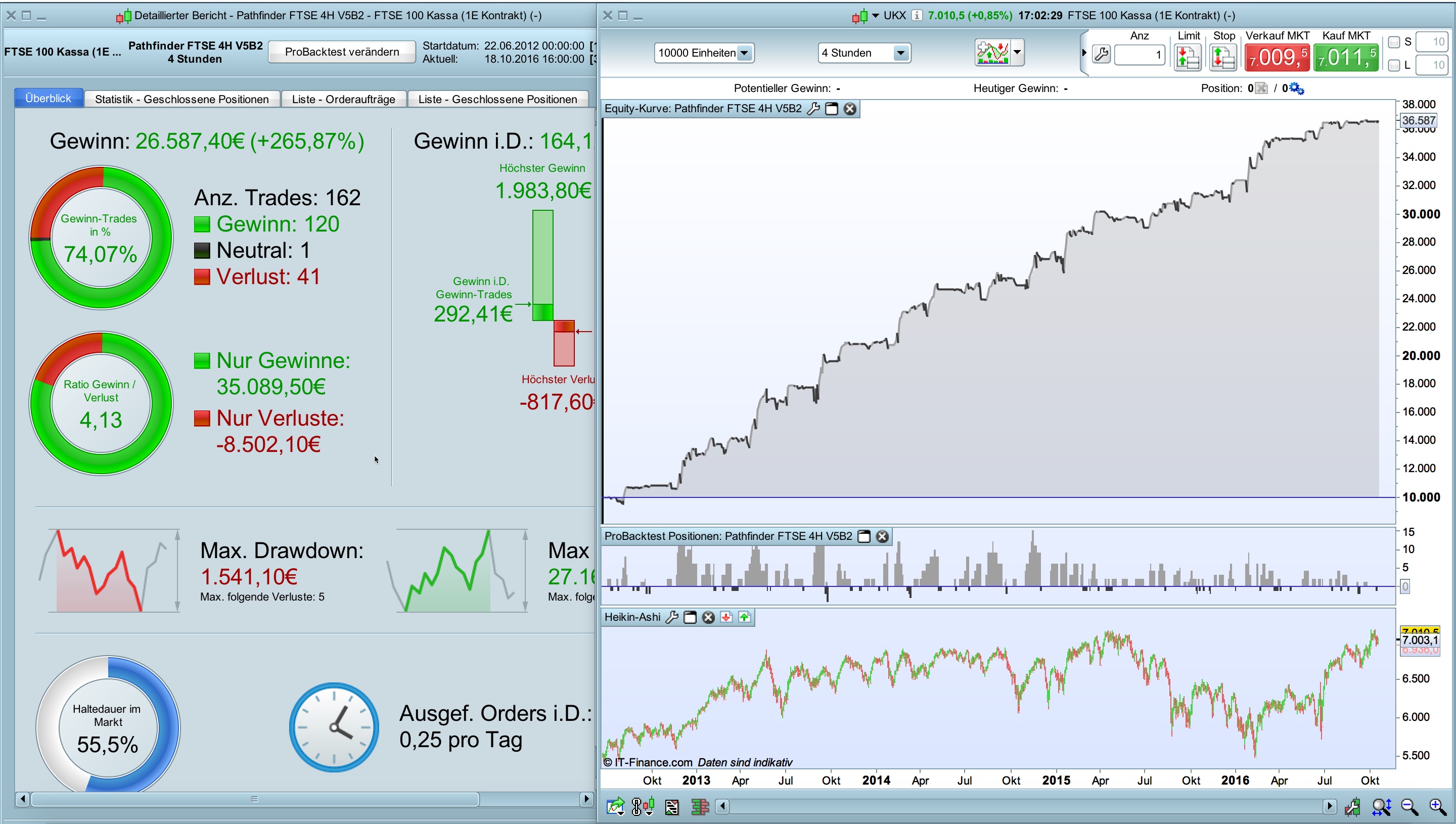

Oil also sees real good results. Reiner the FTSE 100 updated to v5 you have available?

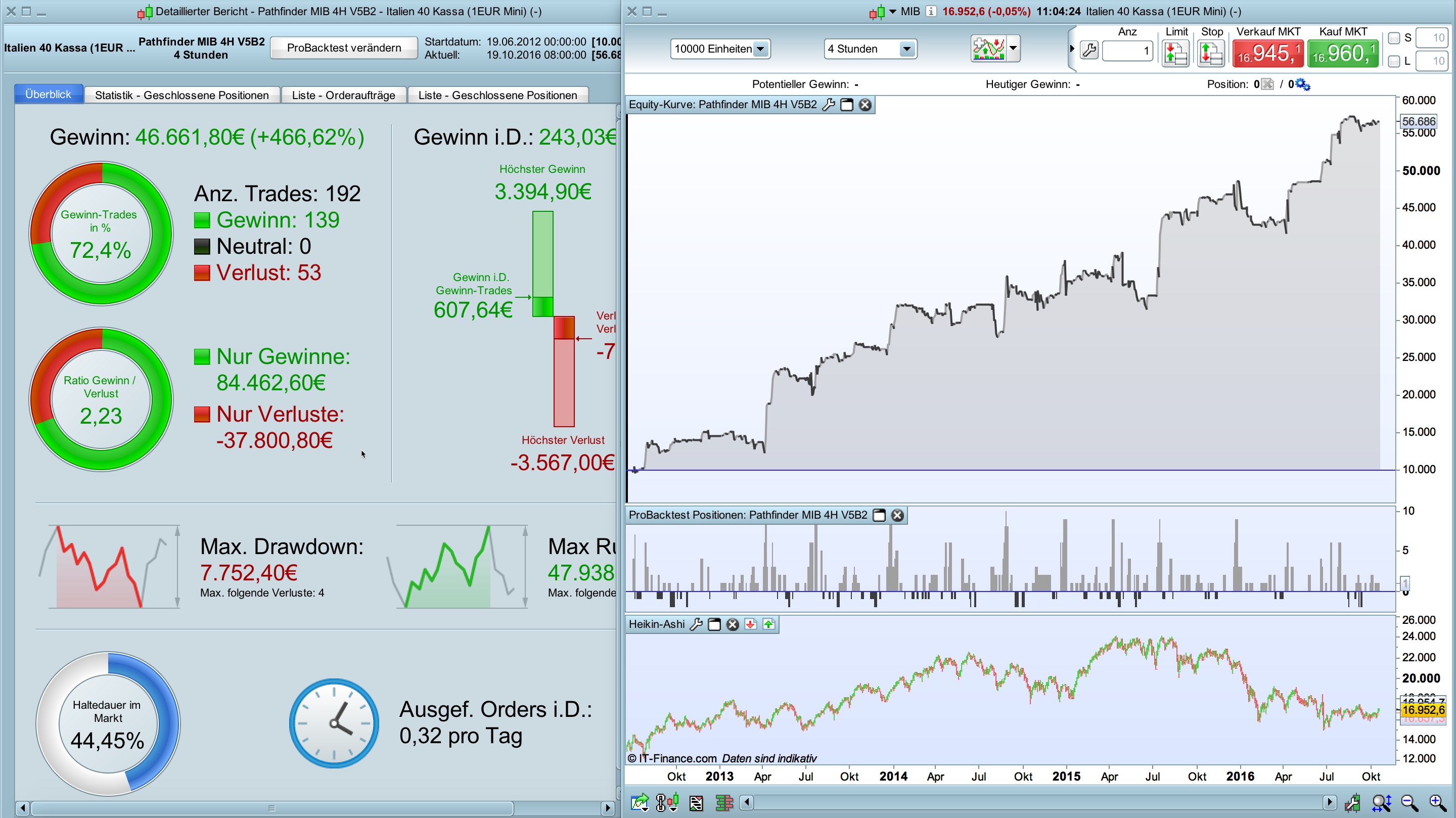

and the poor Italian index as it behaves?

Patrick, Miguel,

as requested here the current Pathfinder version V5B2 for the FTSE mini.

regards, Reiner

Hi Patrick,

Current Pathfinder’s algorithm requires 24H quoting for an underlying instrument (e.g. calculation of signalline, max holding candles, etc.). It won’t work for futures without adaptation. In IG’s world the future instruments have a very limited life time and unfortunately avoid backtesting over a longer time period. I have seen your test based on an instrument DAX30 Full1216 Future – were can I find this underlying in IG’s PRT?

best, Reiner

wp01

wp01Participant

Master

Hi Reiner,

Thank you for your reply. Unfortunately you can not find DAX30FULL1216 Future in PRT from IG. IG is a CFD provider and only has derivates of the original future or index.

With a CFD you never trade directly in the future or other product, but always in a derivate of the original product. This is also the discussion. You trade directly with CFD created software

in a CFD created environment which means that it looks like that you trade against IG, what they of course deny.

When you trade with futures from for example Interactive , you buy directly a future on the stock exchange in for example the DAX Bourse or Euronext. These bourses also closes at 20.00 hrs. or at

22.00 hrs. After these times until 08.00 hrs. there will not be a pricing and of course no candles. Now you have to take a look at the candles in the night at IG. You see sometimes very weird

results where all kind of stops are being triggered while there in the meantime no pricing is on the real stockexchange. Al these pricings in the night affect backtests of course.

If you want to adjust Pathfinder for the future market i suggest you open a free account at prorealtime.de. I thought you can get the first 2 weeks fully access including daytrading free of charge.

So if you want to you can try it free of charge and maybe you can with your experience easily adjust the Pathfinder for futuretrading. When it is working you can set your account to automatic trading

and than your trades will go through Interactive Brokers.

Best regards,

Patrick

Hi Reiner,

Fantastic work on the Pathfinder strategy! Do you know if this is also a good strategy for the CAC French index?

Thanks,

Mikael

Hi Miguel,

in general MIB is suitable for Pathfinder because of the high absolute value and the volatility. With IG MIB is unfortunately not tradable because of the very high spread outside of the core trading time (48 points).

Please find attached a MIB mini backtest, I didn’t find a smoothed equity curve because of the high spreads and the tough down trends. The return is really good but drawdown is also significant. The backtest is done with an unrealistic spread of 15 points and is very optimized.

I love Italian food and especially Italian women but not the MIB, stay with the DAX is still the best :-).

best, Reiner

hahahahahah great reiner .

Dax are many days that pathfinder not trade

Miguel,

look at the DAX over the last days and weeks. No trend, low volatility, no saisonal behavior and catched in a small range. Only scalping systems made some money in that scenario. Pathfinder is a swing trading system makes money mainly on the long side. In my opinion it’s an advantage of the system that it stay beside the line and wait for better trading chances instead of loosing money in sideway trends.

best, Reiner

reb

rebParticipant

Master

Hi Reiner, Hi all

The Reiner’s previous post shows the main reason why a lot of trading systems (swing trading) have some results problems.

One day you win, the day after you loose or vice and versa

At the end, you don’t earn anything but your broker does….

Reb

Hi Mikael,

Pathfinder works also well for CAC mini that’s not really surprising because the European Indices are more or less related. Please find attached the backtest and the code. Please be aware that this is an optimized view over the last 4 years. CAC had a longer sideway range (Feb 2015 – Feb 2016) and I suppose that a lot of traders loose the patience in that time. Overall the result is solid and drawdown is around 20% as mentioned before my favourite is still the DAX because of better performance and drawdown.

best, Reiner