Hi,

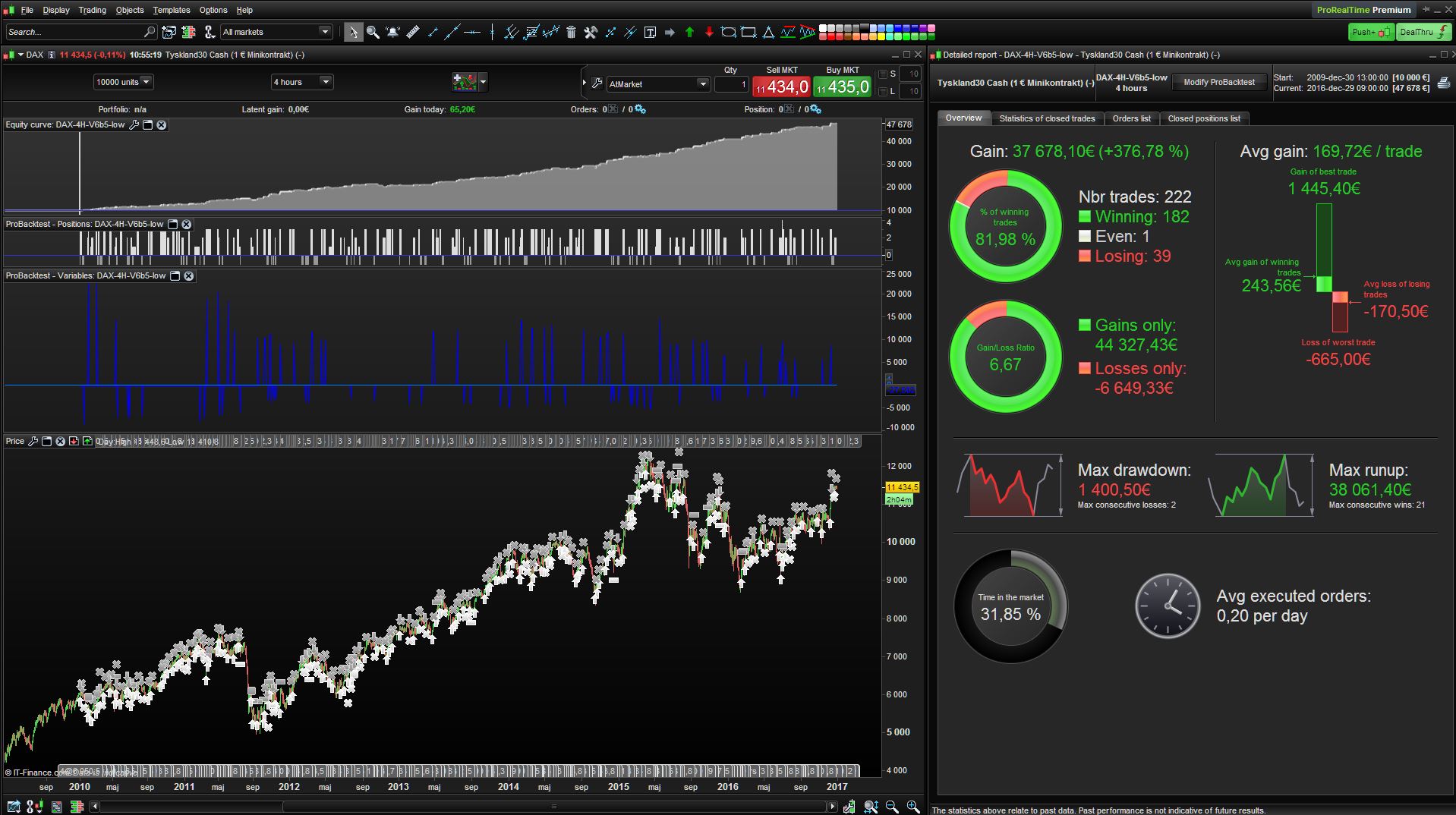

May be it is a stupid question but let me ask anyway. I have tested your code for DAX-1 euro contract and even for DAX-5 euro and DAX-25 euoro. Number of trades, winratio and performance (shape of equity curve) differs really. How it can be so for the same period? My first feeling was it had been a curve fitting just for DAX-1 euro but I might be wrong.

Regards,

/Hakan

Hi Reiner,

I have tested DOW daily V2 and it seems good but I would like to ask a question about performance criterias. Personally I do allways comparare the system with “buy&hold” outcome. In this case buy&hold should give allmost +1900% in DOW daily where the system generates +455% since 1977 (this comparison can be done for each and every year as well to see performance distribution instead of overall comparison but I did not study in deep for moment). According to the overall comparison system is not so good, am I right or what am I missing?

Regards,

/Hakan

@Hakan,

Considering the gains, in absolute, since 1979, is not very signifiactive, especially for the ancient years: you can see that in 1979 the Dow level was under 2000, instead of near 20 000 today: the variations were not the same as today, a variation of 1% has 10x more impact today; but the system is the same in the backtest, and that is why the equity curve has this hyperbolic form, but in fact the profit factor may be quite similar.

Hi Hakan76,

If I understand you right you expect the same backtest results when you are trading with the same account size (10k in your examples) a DAX 1 Euro-, 5 Euro- or 25 Euro contract.

I think your expectation is wrong. You have to synchronize at least account size and all position sizes with the contract value. I’m also not sure if all contract sizes have the same quotes.

Pathfinder DAX 4H is of course optimized for a 1 DAX mini contract but curve fitted – I hope not.

Best, Reiner

Hej Hakan,

I think Aloysius gave a good answer to your question. I mainly developed the Pathfinder daily versions for the purpose to find out the best saisonal adjustments. I think it’s more realistic to tweak the backtest for a slightly shorter history for instance the last 15-20 years. Maybe I can encourage you to improve the backtests.

Best, Reiner

Hi Reiner,

Read in the prevoius posts that Pathfinder also works on Bund Market, but i can’t find the corresponding code;

May I ask you to post the code ?

Thank you very much for the attention.

Best whishes for a wonderful 2017, Andrea

Hello,

let's suppose that I wanto to start autotrading and the TS is already in position.

Is there a way to syncronize "by hand" the portfolio?

Regards, Massimo

Alco

AlcoParticipant

Senior

Hi Guys,

I have heng seng running on demo. It opened a position (2) on dec 28. Today it opened another position (2). Already up for around 140 pips. Heng Seng profits are amazing but it has still a high drawdown. It would be great if we could optimize the settings to get a lower drawdown. Probably a great index to add in your portfolio.

My maximum drawdown with heng seng is around €4000. I’m not able to get a lower drawdown. Maybe its a good idea if we make a V6 version for Hang Seng.

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 5 Beta 3

// Instrument: Hang Seng mini 4H, 2:15-16:00 CET, 10 points spread, account size 100.000 HKD

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 22500

ONCE endTime = 170000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 8

// define filter parameter

ONCE periodLongMA = 380

ONCE periodShortMA = 25

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 3.25 // in %

ONCE stopLossShort = 2 // in %

ONCE takeProfitLong = 2.25 // in %

ONCE takeProfitShort = 2.25 // in %

maxPositionSizeLong = MAX(6, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(6, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.75 // in %

ONCE trailingStartShort = 1 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.2 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 20 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 25 // limit long loss latest after 25 candles

ONCE maxCandlesShortWithoutProfit = 6 // limit short loss latest after 6 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 1

ONCE February = 1

ONCE March = 1

ONCE April = 3

ONCE May = 1

ONCE June = 1

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 2

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

f4 = signalline < Average[periodshortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s4 = signalline CROSSES UNDER dailyHigh

s5 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ((s1 AND f3) OR (s5 AND f1) OR (f4 AND (s4 AND f2)) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

IF LONGONMARKET THEN

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

ELSIF SHORTONMARKET THEN

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

ENDIF

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Hi Reiner,

i get with the DOW 4H V6 a huge drawdown Jan/Feb 2016. It`s different to your backtest. Do you know why? I used the 24h chart of ig, too. Thanks for your help!!

Greets

Michael

Set PRELOADBARS to 1000 instead of 10000. May depends on which instrument you backtests.

Wallstreet cash (2 contract) have this problems. Wallstreet cash (1 EUR contract) dont’t.

Hallo

I tried to rebuild the SMI according to Reiners taste. More than 80% Profit and less than 25% Drawdown.

Milk the swiss cow.

All the best for 2017

MichiM

Hi guys,

With start 2017 I’m going to manage one of my ETF account with a bunch of Pathfinder daily swing robots and for this reason I have opened a new topic for the Pathfinder swing trading system idea here https://www.prorealcode.com/topic/pathfinder-swing-ts/

This topic remains for all general Pathfinder questions and especially for the “flagship” DAX 4H. All swing trade related questions please ask in the new topic.

Best, Reiner

wp01

wp01Participant

Master

@Reiner,

Beest wishes for 2017.

It seems that DAX4HV6 opened a short yesterday at 13:00 hours @ 11.578,30 (according to BT) but was not pushed as a real trade in IG.

This is actually the first time this happened with V6. Former trades went well.

I don’t think i am the only one with this issue. Do you have any idea what went wrong?

Thanks.

Best regards,

Patrick

Hi,

I am not sure if it possible but I feel that it is a litte hard to find different versions of Pathfinder in the forum, anyone have a recommendation about how can I find them easly and recognize old ones versus new?

Regards.

/Hakan