Hi Mark,

to make it even clearer, Pathfinder pyramiding the long position.

Pathfinder is cumulating the position for every long trigger.

- cross over dailyHigh – buy positionSize * saisonalPatternMultiplier < maxPositionSizeLong

- cross over weeklyHigh – buy positionSize * saisonalPatternMultiplier < maxPositionSizeLong

- cross over monthlyHigh – buy positionSize * saisonalPatternMultiplier < maxPositionSizeLong

For current month (November) the positionSize is 1*3 = 3 cfds for every long trade. Maximum position is 15 cfds. Please adjust the numbers to your account size. I recommend 10k and as reb mentioned i would increase the position size after 100% gain.

best, Reiner

Mark

MarkParticipant

Senior

Thanks guys, just getting my head around the system. I’m struggling to see what exactly the risk management calculation and starting balance exactly achieves? As when I cahsnge the account balance and risk % parameters it makes no change whatsoever to the outcome on back testing.

Or am I being stupid?

mark

Pere

PereParticipant

Veteran

Hi Pranik. Thanks for your work.

I also programmed a similar indicator, which works well. But I am presently trying to program an indicator which can show the distances of the signalline to those levels, which also can give some alerts when some of this distances is near the trigger level, only to see if the possibility to start is near or not. The distance levels should be programmable to set them on the desired level. The problem is that I only can study it some hours a month, and it still doesn’t work correctly. Perhaps you could improve it.

Regards

Hi Brage,

Pathfinder’s code control the signalline calculation and in my opinion that’s independent from the display settings. Sunday quoting is a good example, Pathfinder will use sunday quotes no matter it’s on or off because the code determine the behavior. On the other hand if you want to see the right Pathfinder’s level e.g with pranik indicator then you have to activate sunday quotes for the underlying instrument.

best, Reiner

Hi pranik,

Thanks for contribution.

Did you realize that with your indicator every level works fine without monthly low. Since 30.Sep. monthly low is wrong before that date it works well. I’m using more or less the same indicator and I have really no clue why. May be you have an explanation.

best, Reiner

Hi Mark,

I gues your comment is related to the following two lines of code:

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(15, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

Of course you are not stupid because I overruled the risc calculation. You have to set the value 15 to 1 to get the right results out of the formula.

best, Reiner

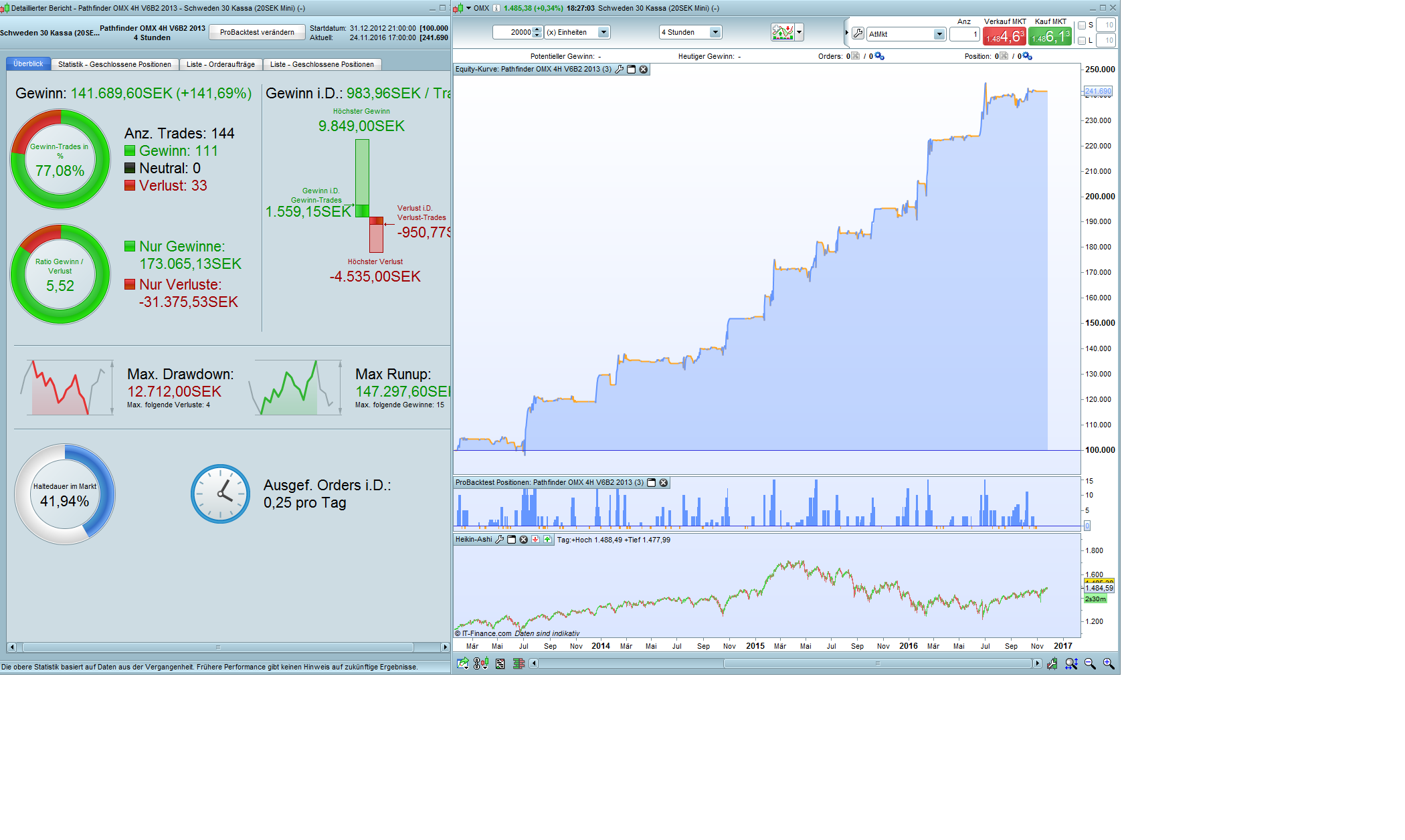

Hi Brage,

as promised please find attached an update of Pathfinder OMX 4H V6B2. I have compiled two versions, first backtest with the maximal available data since 2010 and the second was optimized for data from 2013.

best, Reiner

Thanks Reiner!

Much apreciated since your time is limited. Going live with this version tomorrow. And as always looking forward to news in this thread and further development of Pathfinder:)

MarkParticipant

Senior

Reiner,

Thank you for your reply, so with the values set at 15 the following bits of code are not necessary?

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

Mark

Hi Reiner,

I haven’t noticed that.

I think is related to Dlow/Dhigh functions returning value of previous day. The system considers the lower value of 30 sept as a lower value of 1 october.

Maybe we have to calculate current daily low/high without DLow/DHigh functions. Or Maybe we have to shift daily value of 1 day to include last month’s day value.

I’ll try.

Shifting 1 day seems to work. I’ve attached version 1.1. I think we can modify also the strategy to fix monthly values.

If Month[1] <> Month[2] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

Thanks pranik, your indicator works well now and all levels are synchron with the strategy. The values in the strategy were always correct.

Hi Mark,

The risk formula is widely used here in this forum and I have integrated this approach in Pathfinder to play around and observe the relationship beetween the variables. Backtests have shown that the system needs enough room for pyramiding to deliver this exeptional performance. The formula calculates the position size with the variables Capital and Risk and takes the maximal value of the result or the default value 15. You can reduce the default size and play around with your personal risk/capital values.

best, Reiner

PereParticipant

Veteran

Hi Reiner.

I am planning to test live Pathfinder with a small capital account, 4k€ to see how it works in real account. I will change, as you recommend, the maxPositionSizelong from 15 to 4, maxPositionSizeshort from 15 to 4 and saisonal position multiplier of November and December from 3 to 1 (or better to 2?).

But shall I also change the Capital from 10000 to 4000? Risk remains 5%? Any other change?

Thanks for your contribution!

Regards

Hi Petrus,

I would set December’s multiplier also to 1. With max 4 possible contracts the system has enough room for pyramiding. Backtest with 4 contracts was profitable. Capital and Risk variables can be remain unchanged.

best, Reiner