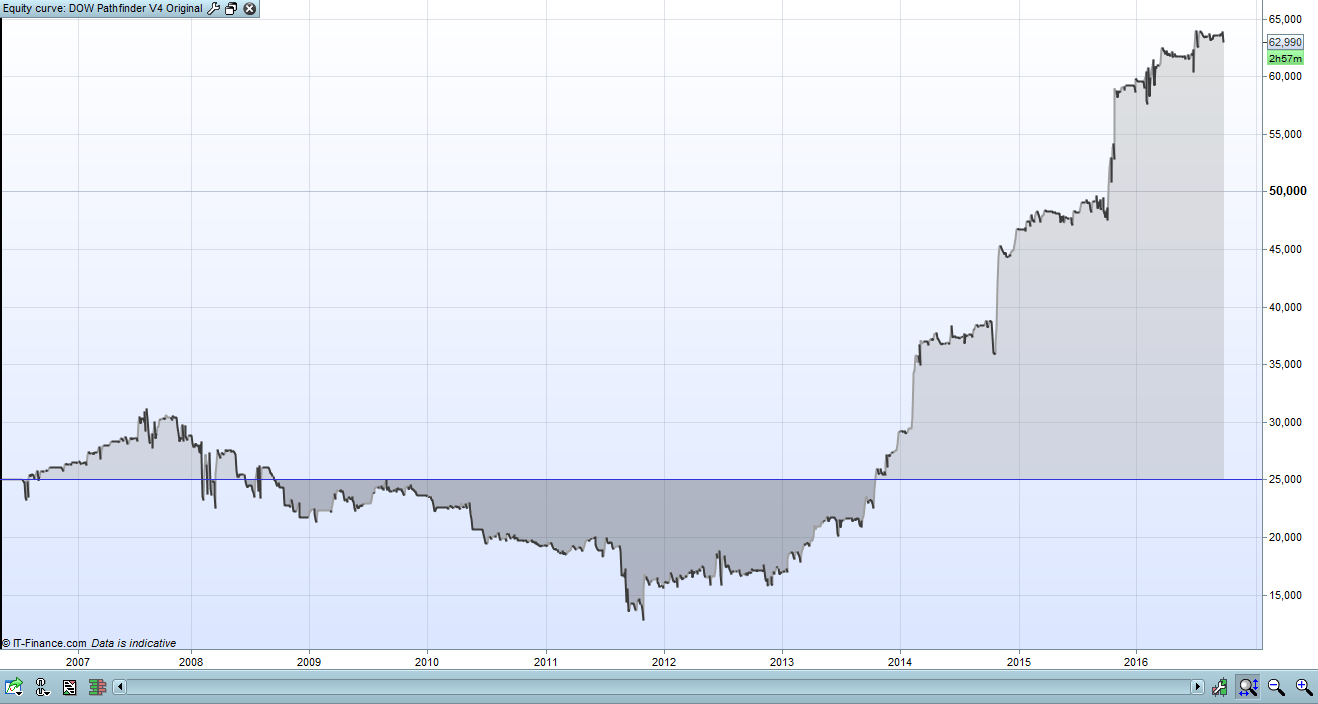

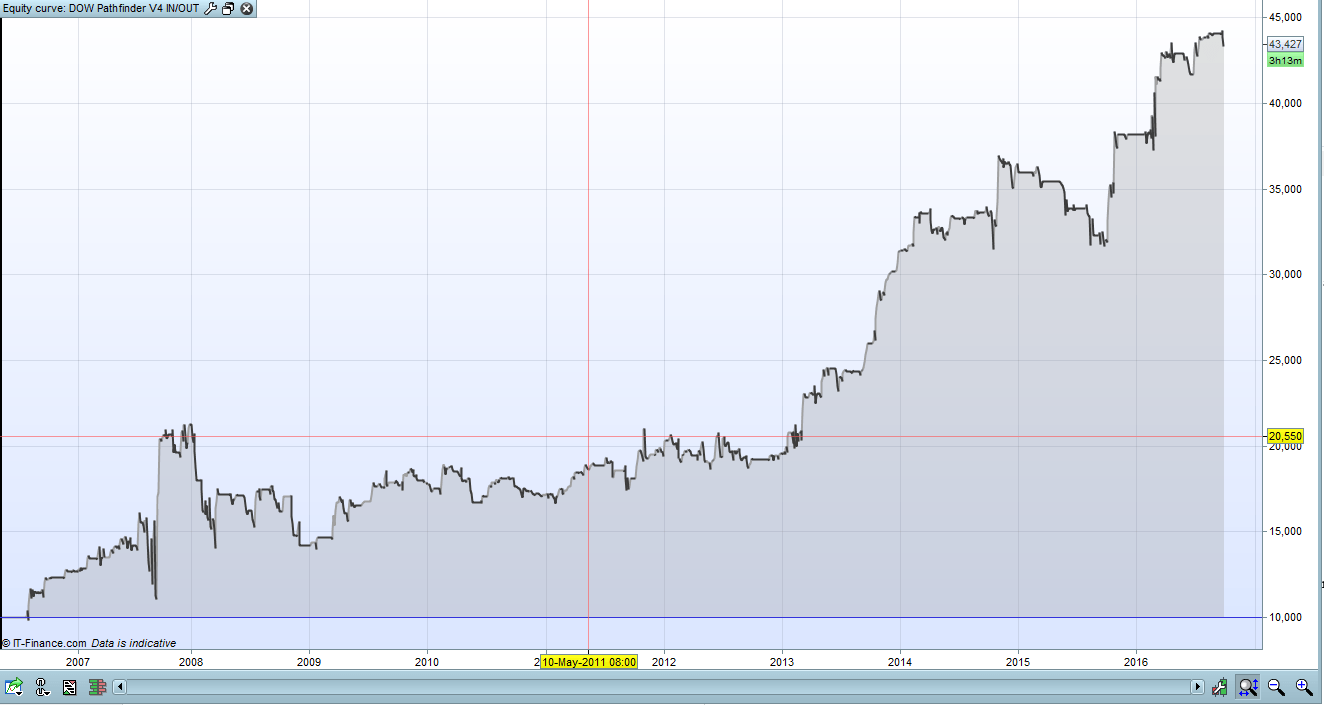

The DOW result is impressive but there are also a couple of higher losses.

Pathfinder DOW V4

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 4

// Instrument: DOW mini 4H, 8-22 CET, 2.8 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 7

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 10

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 3

ONCE maxPositionSizeShort = 3

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 1.75 // in %

ONCE takeProfitLong = 2.75 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE maxCandlesLongWithProfit = 17 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 40 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short

ONCE January = 2

ONCE February = 3

ONCE March = 2

ONCE April = 2

ONCE May = 2

ONCE June = 2 // 3

ONCE July = 2

ONCE August = 2

ONCE September = -2

ONCE October = 3

ONCE November = 2

ONCE December = 2

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) THEN // cumulate orders for long trades

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) THEN // no cumulation for short trades

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

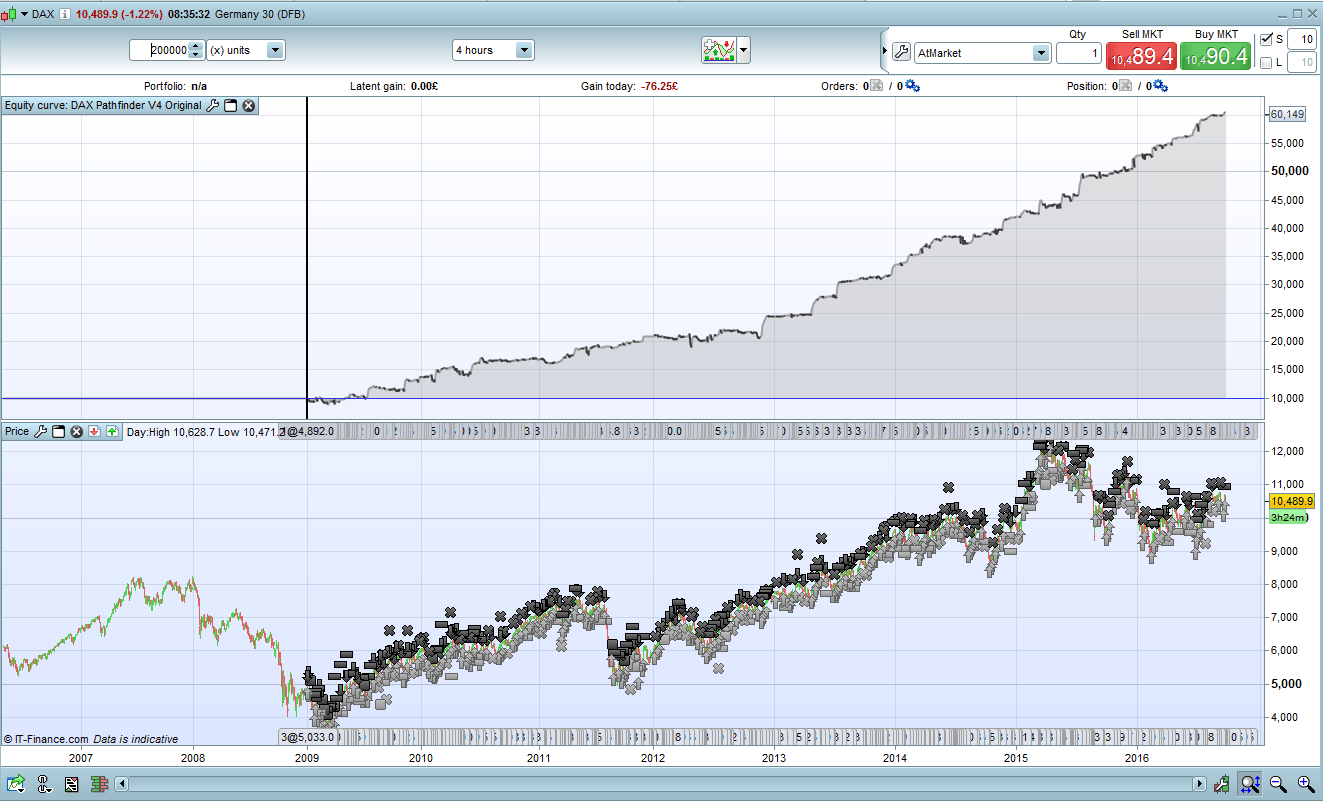

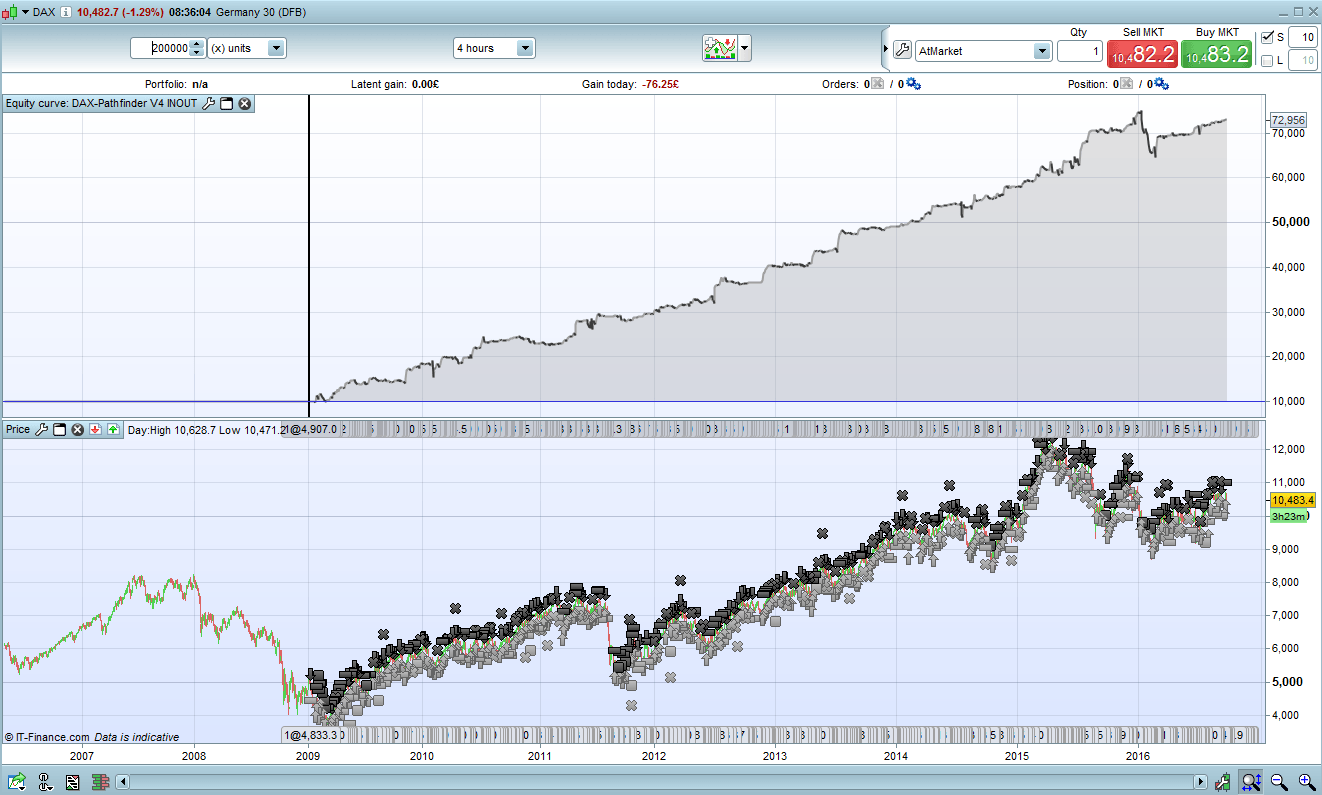

So a little play with V4 IN/OUT sample. Jan 2009 – March 2014.

Actually picks out first and third MA as 2…

Bit choppier than your version with MUCH more drawdown, overall result slightly better but prefer your version. I think it proves that your version is solid…?

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 2 //5

ONCE periodSecondMA = 12 //10

ONCE periodThirdMA = 2 //3

// define filter parameter

ONCE periodLongMA = 280 //300

ONCE periodShortMA = 45 //50

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stopLossLong = 6.5 // in % 5.5

ONCE stopLossShort = 2.75 // in % 3.5

ONCE takeProfitLong = 3.25 // in % 2.75

ONCE takeProfitShort = 1.5 // in % 1.75

ONCE maxCandlesLongWithProfit = 18 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 10 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 32 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 27 // limit short loss latest after 25 candles

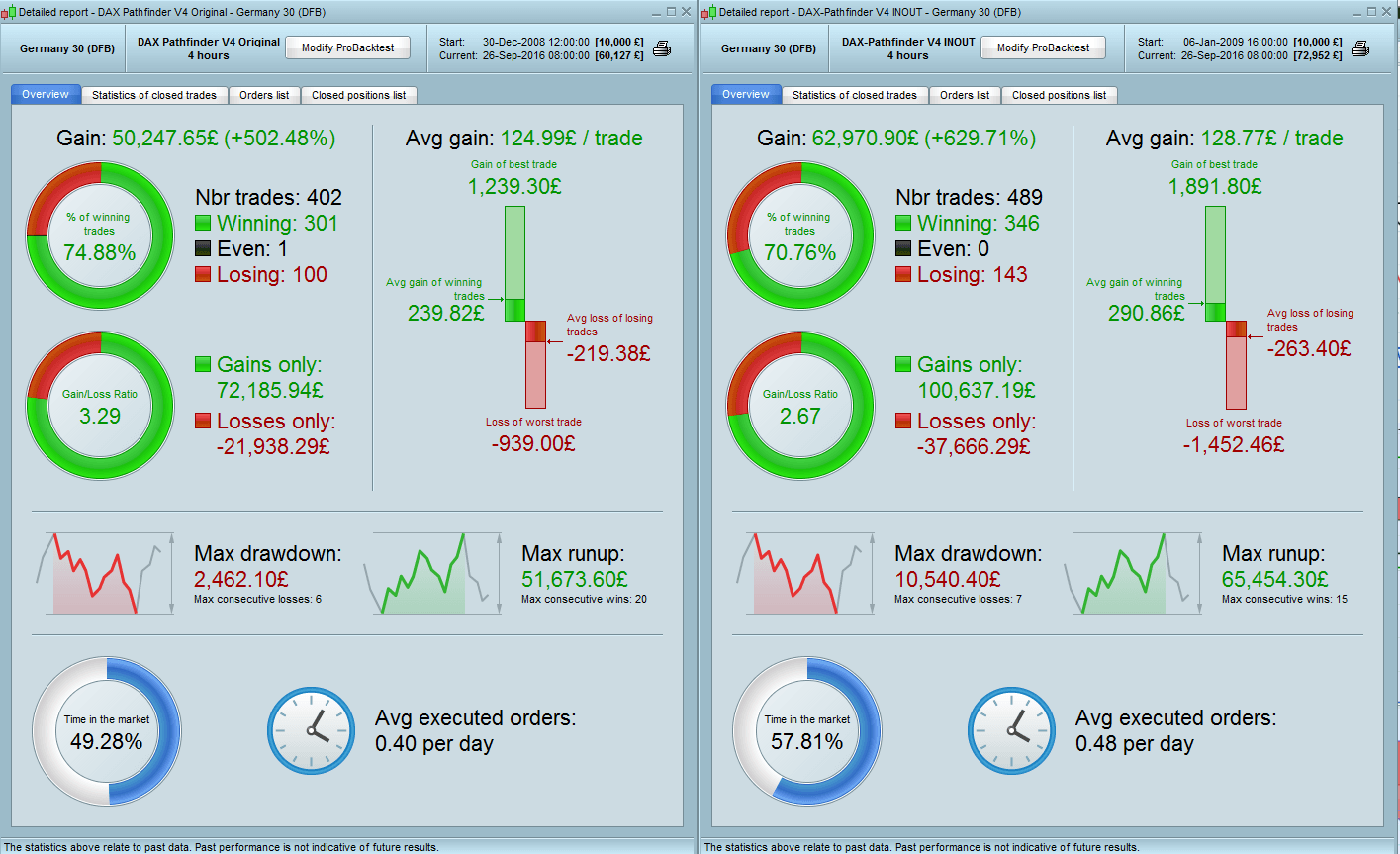

in backtest the version 4 seems better results for the DAX and the FTSE 100 while Wallstreet looks no better. I noticed that putting as 8-23 transaction time is improved a little.

Cosmic1, Thanks for your confirmation. It’s good to know that DAX V4 works reliable and without big drawdowns before 2013.

Miguel, You are right. In Pathfinder DOW V4 the new variables maxPositionSizeLong and maxPositionSizeShort have the wrong values (3) and limit the result. Please change the values to 15 and you will see a comparable V3 result. I have attached a comparison of V3 and V4. Sorry for the confusion.

Hi Reiner, DOW not looking so pretty before 2012.

If you want to ping me a message on email travel141 at gmail dot com I can give you skype details if you want to throw any code like this at the extended data I have if that would help?

Hi Reiner,

Great work!

I have been running v3 live since Sept 19 and it opened a long position on Sept 26 17 pm, but the backtest did not, unless I limit the starting date and time to Sept 19. Is there anything I should think about before starting v4?

Regards,

David

Hi Reiner,

Disregard my post above. I had forgot to set the correct no. of units to show in the backtest, so now both show the same.

Regards,

David

Perfetto. Tutto ok Reiner.

Hi Reiner,

I’ve been following your progress over the last few months and its been really impressive. I only put it on a live demo account in the last few weeks. How have things matched up in relation to the backtest and live testing/trading since you started.

I know you have talked about this in a previous post but I think this is the topic everyone is keen to find out about. Many of my simple strategies produce fine results on PRT but when it is a complex piece of coding it concerns me that the live results and backtest may be quite different.

Thanks for all your effort,

James

Cosmic1, Thanks for DOW backtest and your offer. I appreciate your support for this project and will come back to you.

No worries.

IN/OUT optimise with 10 years of data. 2.8 Spread.

ONCE periodFirstMA = 7 //5

ONCE periodSecondMA = 10 //10

ONCE periodThirdMA = 6 //7

// define filter parameter

ONCE periodLongMA = 315 //300

ONCE periodShortMA = 3 //10

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 15

ONCE stopLossLong = 6.25 // in 5.5%

ONCE stopLossShort = 2 // in 1.75%

ONCE takeProfitLong = 3.25 // in 2.75%

ONCE takeProfitShort = 1.75 // in 1.75%

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 17 candles

ONCE maxCandlesShortWithProfit = 11 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 41 // limit long loss latest after 40 candles

ONCE maxCandlesShortWithoutProfit = 21 // limit short loss latest after 25 candles

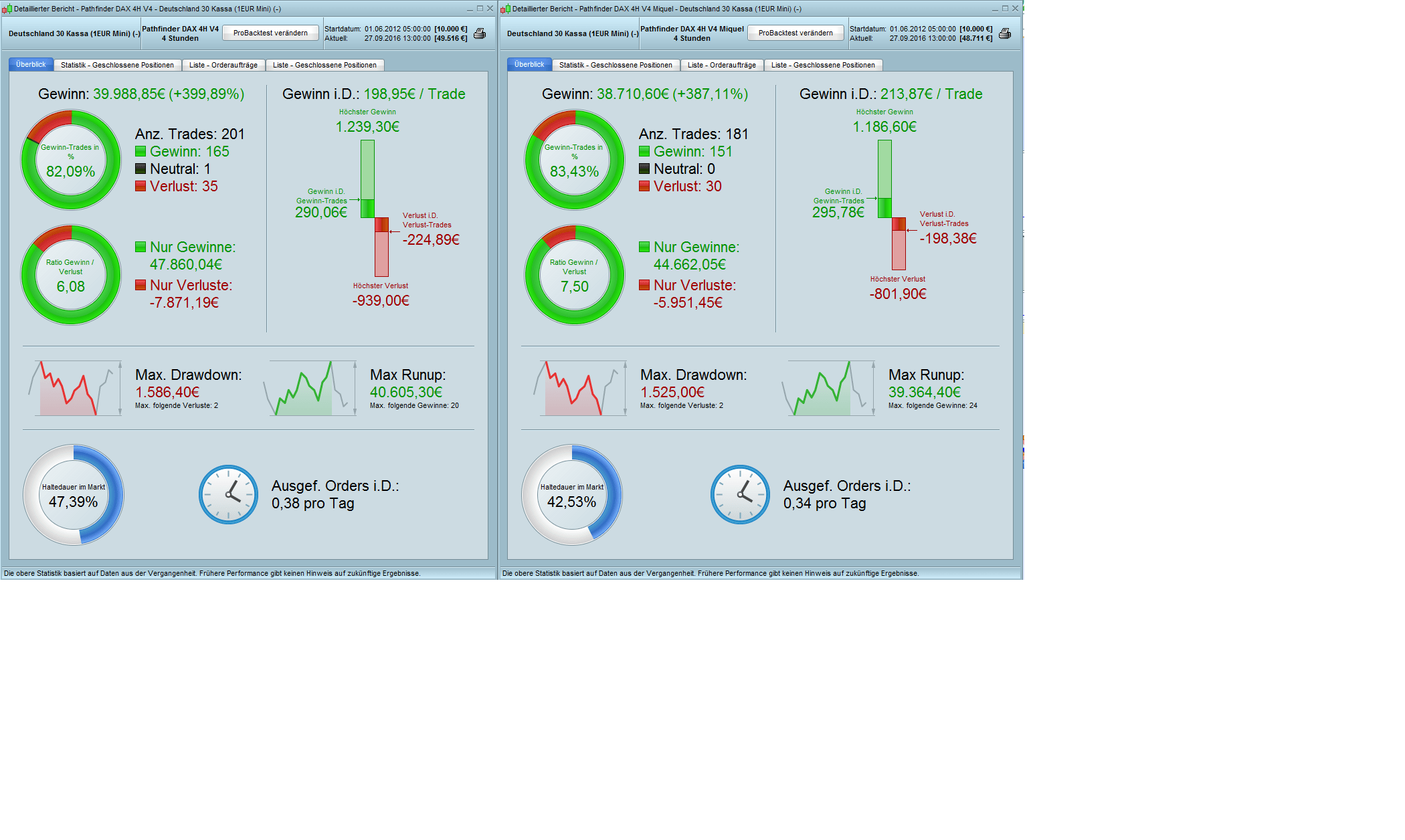

Miguel, I have tested your idea that Pathfinder avoid intraday reopen a position in the same direction. Please find attached the comparison of both backtests with DAX mini. Your idea is valueable!

Here is the code, changes are tagged with #Miguel:

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 4 - avoid reopen of intraday positions in same direction (from Miguel)

// Instrument: DAX mini 4H, 8-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.5 // in %

ONCE takeProfitLong = 2.75 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE maxCandlesLongWithProfit = 15 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open #Miguel

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// reduced position? #Miguel

reduceLongInTradingWindow = COUNTOFLONGSHARES < startPositionLong

reduceShortInTradingWindow = COUNTOFSHORTSHARES < startPositionShort

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND not reduceLongInTradingWindow ) THEN // cumulate orders for long trades #Miguel

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND not reduceShortInTradingWindow THEN // no cumulation for short trades #Miguel

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Hi James,

Pathfinder is a completely transparent project from the first idea up to the current state every step is documented here in the forum. The backtest with the DAX seems to be realible over the last years but to be honest I have no idea whether such a system realy works under real condition. From mid of July until now I traded several versions V2, V3 and now V4 but not continously and the return is more or less zero. An automatic trading system needs volatility and a trend to make money and over the last month DAX was a “lame duck”. It requires hundreds of trades to realy judge a system and requires a lot of patience. In a 4H timeframe it will take a time (months).

I’m not a professional trader and I’m far away to be a professional trading system developer so every idea, reniew and improvement from the real pros are welcome.

best Regards,

Reiner

Perfetto Reiner.

if you enter definendo intra dal trading window 8-23. …. Incredibile more

miguel.