Anyone still runs something of all this?

Léo

LéoParticipant

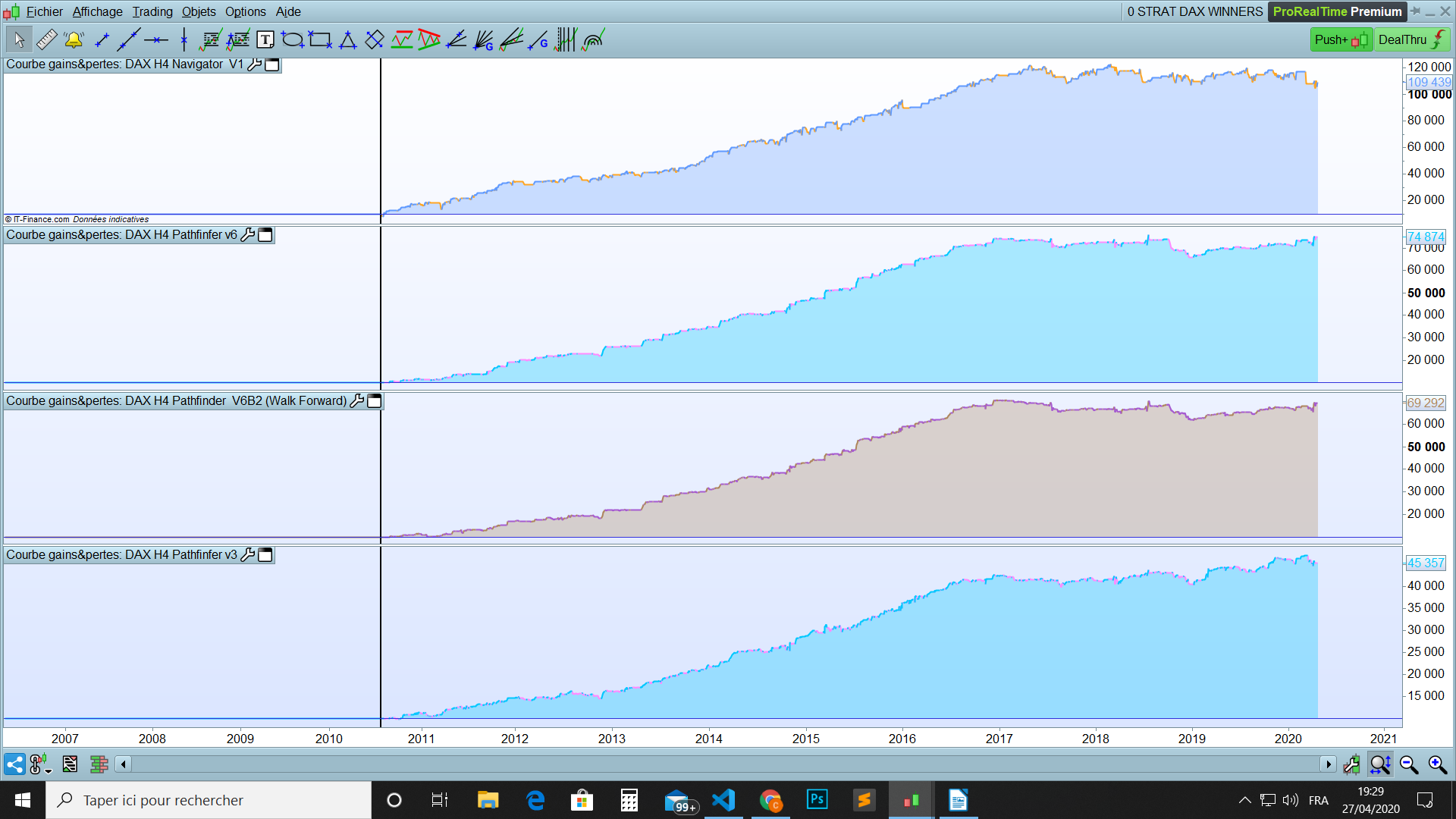

Average

Dear Gianluca,

thank you for this list.

I wanted to backtest these strategies (knowing that you use them live) but could not find the related itf files (at least not with the exact same name). Would you mind copying them here or confirm where I can find them on this website ?

Also you indicated that you close the Italy strategy manually – is the TP too ambitious ? Do you also close other strategies manually ?

Thank you in advance for your help.

Alex.

Ciao Léo, i just stopped time to time because my account size dosn’t fit the DrawDown of the sistem, but since 2018 is 100% winning rate the Italy Swing, you can find it scrolling back the page!

ok, i think there is some misunderstanding, that sistem that i use on ITA is the swing, so you can find in the swing sistem post

LéoParticipant

Average

Hi Gianluca,

Thank you for the (very fast) reply 🙂

I have been testing the file Path-Swing-Italy-Cash.itf and I am also planning the file FTSEMIB-SWING.itf . I find both files scrolling back the page (and in a post from you from 2018).

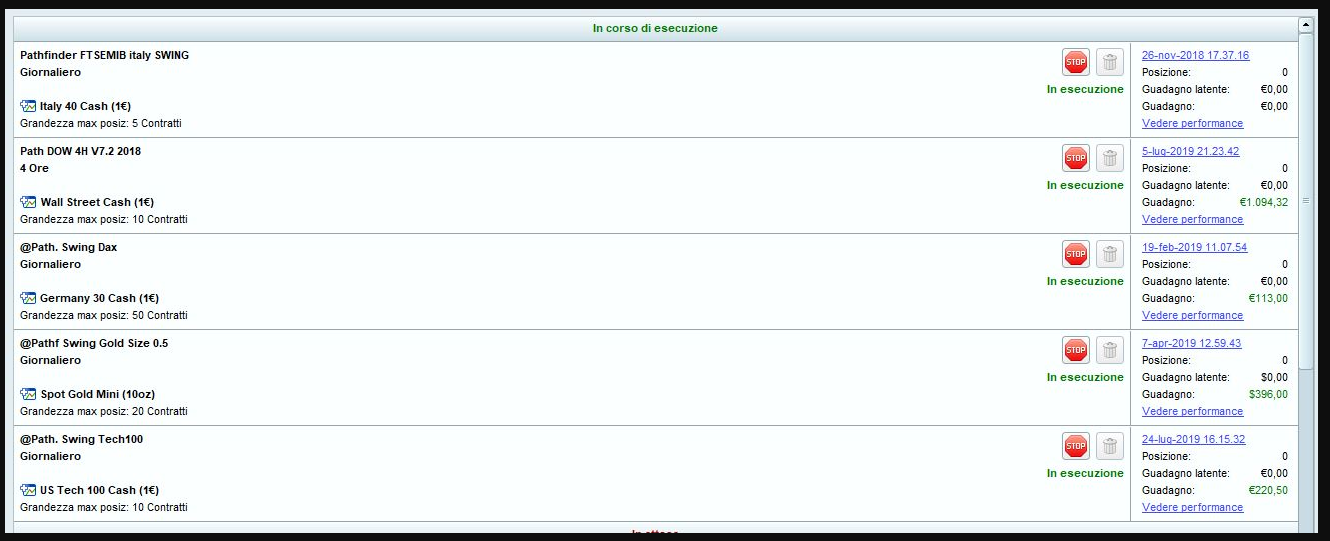

I just realized looking at your printscreen (attached) that the one you are using live has a different name (Pathfinder FTSEMIB italy SWING) – I was just wondering if these were different versions.

Also I would like to test the other strategies you recommended (Path Dow 4H V7.2 2018 / Path Swing Dax / Path Swing Gold Size 0.5 / Path Swing Tech100) but could not find the ITF files in the attachments list in this page.

Can you confirm where I can find those ?

Thank you again !

I use the Vanilla Nasdaq 4h system and its working very well

Nice, can you share this code please ?

one of the reason could be

a completely changed behaviour of the biggest investors after Draghis whatever it takes

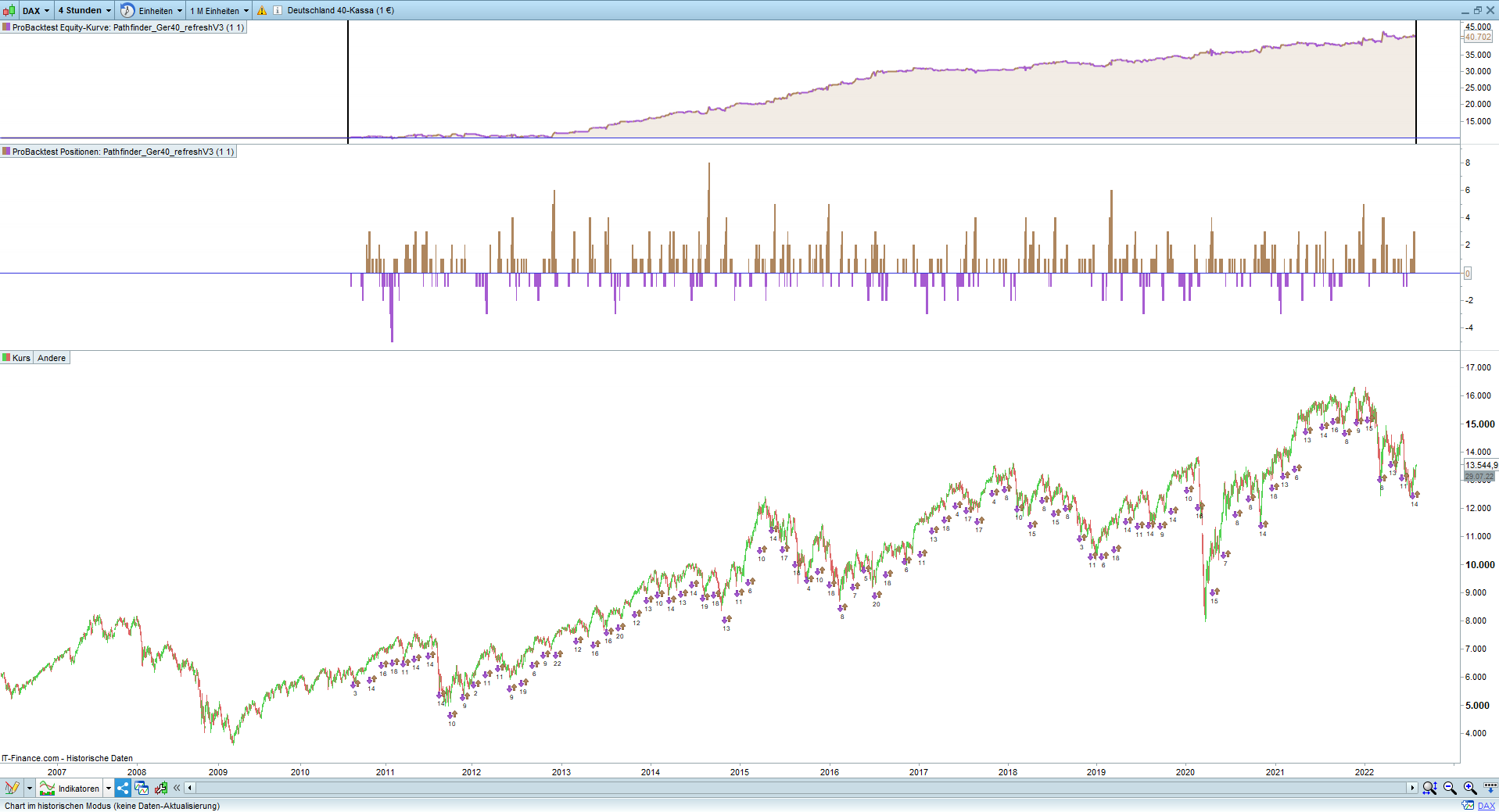

// pathfinder system @ ger40 version 3

// timezone europetime berlin

// timeframe 4H

// 2 points spread

// Dax breakout system triggered by previous daily, weekly and monthly high/low crossings

// Original by Reiner , refresh by JohnScher @ 07/31/2022

// proOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// smoothed average parameter (signalline)

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// filter parameter

ONCE periodLongMA = 250

ONCE periodShortMA = 50

// trading paramter

ONCE PositionSize = 1

// money and position management parameter

ONCE stoppLoss = 5 // in %

ONCE takeProfitLong = 5 // in %

ONCE takeProfitShort = 2 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 18 candles

ONCE maxCandlesShortWithProfit = 17 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 30 // limit short loss latest after 25 candles

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// filter criteria because not every breakout is profitable

c1 = close > Average[periodLongMA](close)

c2 = close < Average[periodLongMA](close)

c3 = close > Average[periodShortMA](close)

c4 = close < Average[periodShortMA](close)

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// long timebased conditions

tmLong = openmonth <> 1 and openmonth <> 9

tdLong = opendayofweek >= 1 and opendayofweek <= 4 //sik!

ttLong = time >= 090000 and time <= 210000

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER monthlyLow

s3 = signalline CROSSES UNDER dailyLow

// short timebased conditions

tmShort = openmonth <> 3 and openmonth <> 5 and openmonth <> 10 and openmonth <> 11

tdShort = opendayofweek >= 1 and opendayofweek <= 5

ttShort = time >= 090000 and time <= 210000

// long entry

IF tmLong and tdLong and ttLong then

IF ( l1 OR l4 OR l2 OR (l3 AND c2) ) THEN // cumulate orders for long trades

BUY PositionSize CONTRACT AT MARKET

takeProfit = takeProfitLong

ENDIF

Endif

// short entry

IF tmShort and tdShort and ttShort THEN

IF ( (s1 AND c3) OR (s2 AND c4) OR (s3 AND c1) ) THEN // no cumulation for short trades

SELLSHORT positionSize CONTRACT AT MARKET

takeProfit = takeProfitShort

ENDIF

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stoppLoss

SET TARGET %PROFIT takeProfit

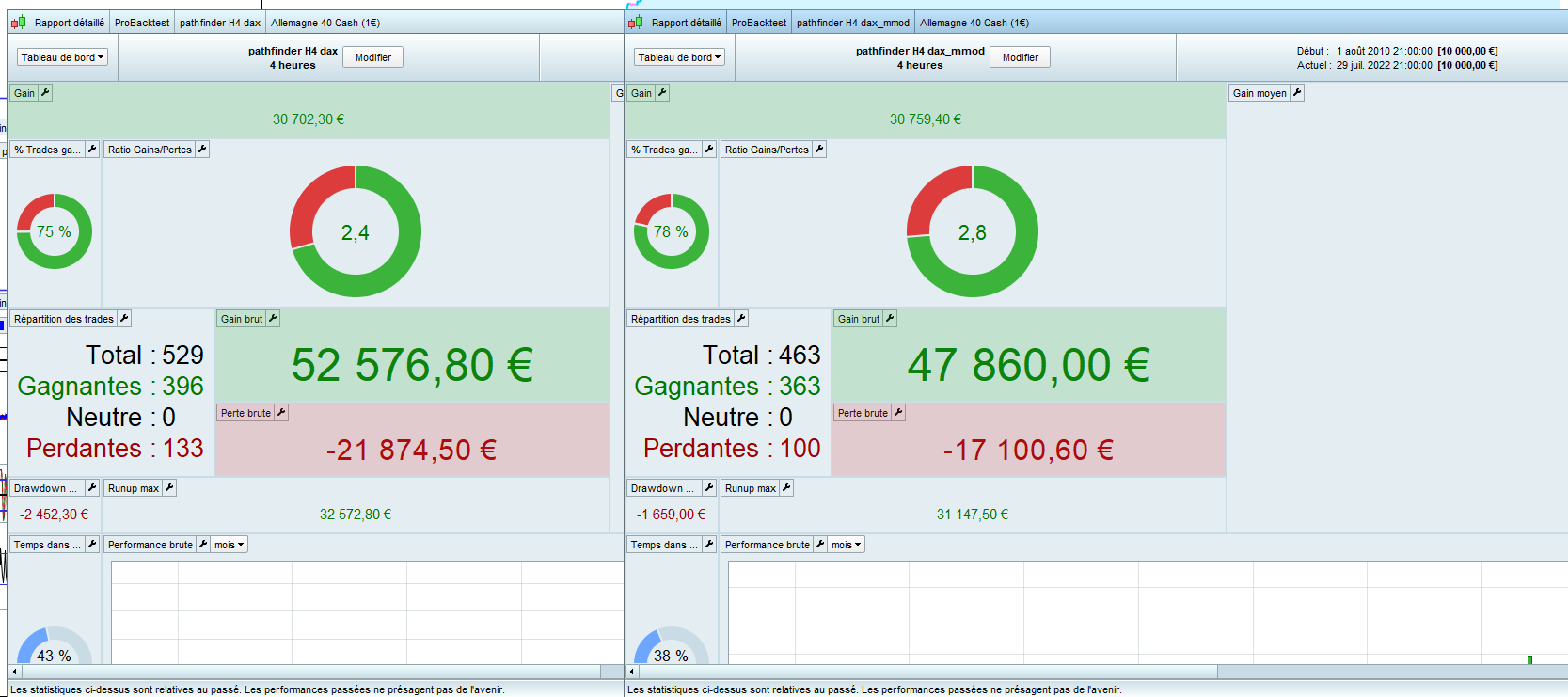

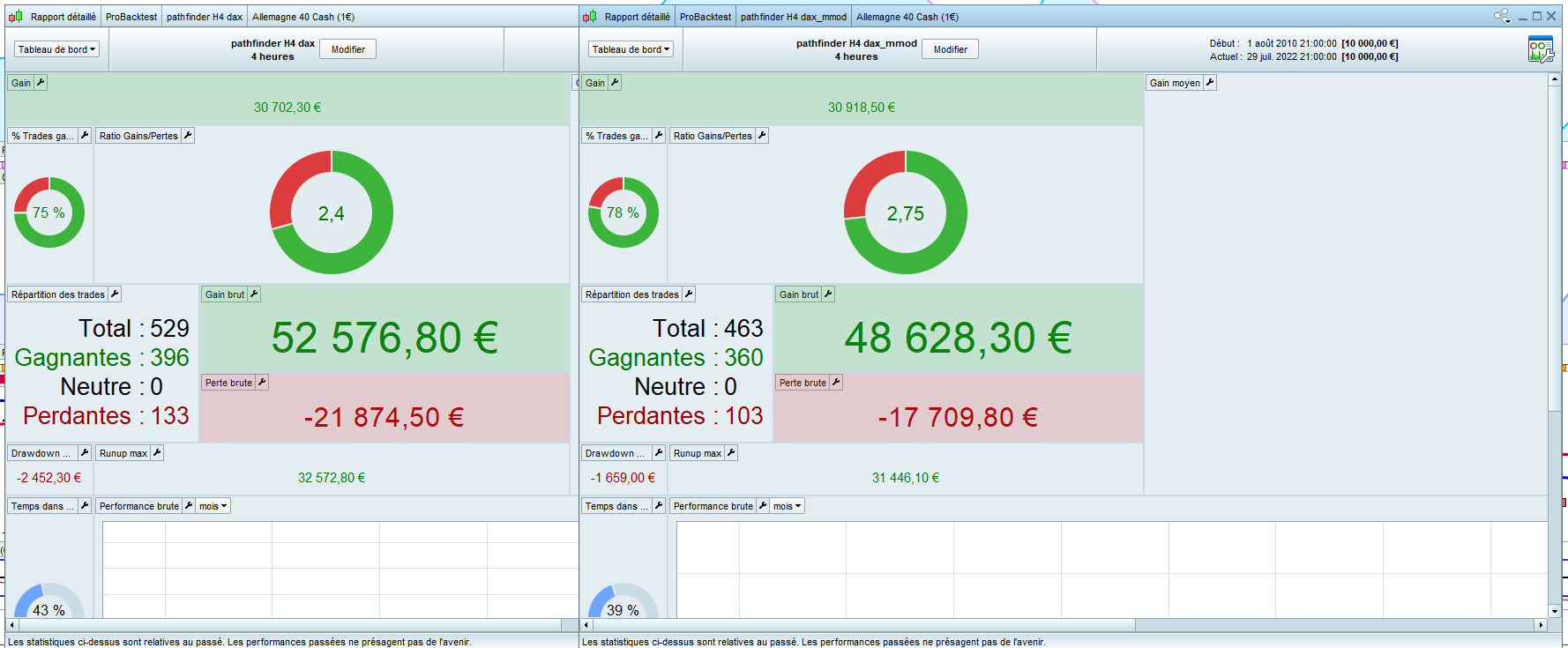

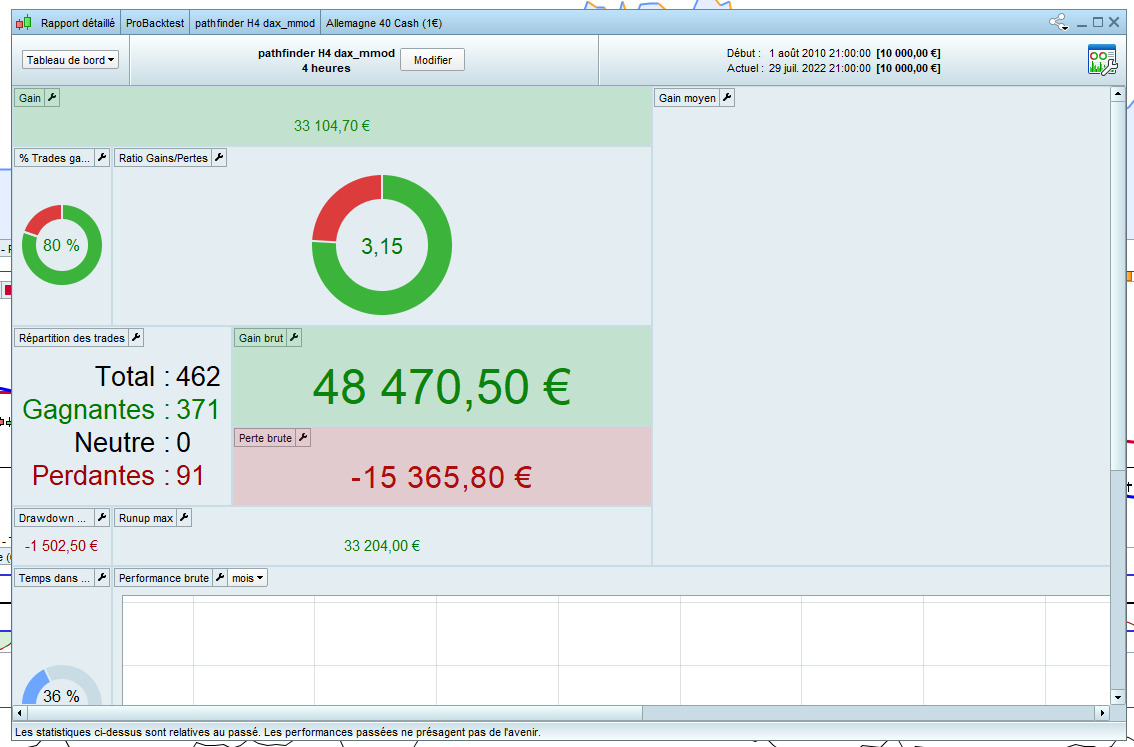

Good morning,

on the left your version and on the right the version modified just now

I modified the TP short =5

Yes, thank you, it has been a long day.

“Pathfinder refresh” opened a first position yesterday 21.00. Long at 13,692 on my live account.

Let’s see how the system performs for half a year