wp01

wp01Participant

Master

To trade the PF US500 in ProOrder you have to change line 51 to 5 and line 53/54/55 to 50. The minimum tradesize is 5 according to IG.

You get more or less the same outcome in the results as with the original sizes. Which is weird because if you take a look at the orderlist in the beginning of 2010

you see a couple of times orders with 2 positions only. The trades should have been rejected in live by the way.

And in this code the startrisk is 2. If you take less risk (<2) you probably have to change the minimumsize as well.

Regards,

Hello.

I’ve been following you here for a longer while. It’s very interesting and I can see how much work is already done in the Pathfinder trading systems.

Many thanks to all of you for this!

I would like to share my results with you in demo mode.

Here attached.

And I would like to ask you two three things too.

Is there anyone who runs the Pathfinder in the Dax live? If so, how long you do this and would you be willing to share the results?

What results have been obtained over the longest period of time tested with which system?

And last but not least.

Does anyone or can someone provide one of the Pathfinder systems as mt4. file? If not, do we want to pool money and hire a professional programming service?

until then

JohnScher

Translated with http://www.DeepL.com/Translator

Pathfinder Silver looks a lot better if you can backtest with 200.000 candles. So I am running it as well.

I am now live with 13 PF-4H algos. Wow, I hope they perform like in the last 2 weeks. Not a big hit, but all the small profits summed up to a nice chunk of cash.

I actually also hope they will not trigger all at once, this could severly crush my margin.

I will definitly reduce the algos when I hit 50%.

@wp01: Thanks for the tip with the Us 500. I changed it accordingly and updated the dropbox.

life/demo and backtest: backtest needs an additional candle before the data is synchronized again

From yesterday a position was opened on NIKKEI, but nothing on backtest. And there was more than 4h.

Is it normal?

Jan

JanParticipant

Veteran

Thanks a lot for sharing the code of the Pathfinder. Very organised and very well explained what it is doing in the code.

life/demo and backtest: backtest needs an additional candle before the data is synchronized again

From yesterday a position was opened on NIKKEI, but nothing on backtest. And there was more than 4h. Is it normal?

Guys, i checked the TS on Nikkei, and it should not have open a trade on 26 of febr, but it did. And i lost 1.200$ for it, could someone help me? @reiner @nicolas

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 50000 // start time of trading window in CET

ONCE endTime = 210000 // end time of trading window in CET

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5 // 5 is center of gravity, do not change

ONCE periodSecondMA = 10 // 10 is center of gravity, do not change

ONCE periodThirdMA = 3 // heartbeat of the instrument

// define filter parameter

ONCE periodLongMA = 250 // period lenght of the long moving average that works as filter

ONCE periodShortMA = 10 // period lenght of the short moving average that works as filter

// define money and position management parameter

// dynamic scaling of the chance/risk profile depending on account size

ONCE startRisk = 0.25 // start risk level e.g 0.25 - 25%, 0.5 - 50%, 0.75 - 75%, 1 - 100% and so on

ONCE maxRisk = 1 // max risk level e.g 1.5 - 150%

ONCE increaseRiskLevel = 300 // amount of profit from which the risk is to be increased

ONCE increaseRiskStep = 0.25 // step by which the risk should be increased

// size calculation: size = positionSize * trendMultiplier * saisonalPatternMultiplier * scaleFactor

ONCE positionSize = 1 // default start size

ONCE trendMultiplier = 3 // >1 with dynamic position sizing; 1 without

ONCE maxPositionSizePerTrade = 3 // maximum size per trade

ONCE maxPositionSizeLong = 6 // maximum size for long positions

ONCE maxPositionSizeShort = 1 // maximum size for short positions

ONCE stopLossLong = 5 // in % *changed from 4.75

ONCE stopLossShort = 1.5 // in % *changed from 3

ONCE takeProfitLong = 3.5 // in % *changed from 3.25

ONCE takeProfitShort = 1.75 // in %

ONCE trailingStartLong = 1.25 // in %

ONCE trailingStartShort = 0.5 // in %

ONCE trailingStepLong = 0.8 // in %

ONCE trailingStepShort = 0.3 // in %

ONCE maxCandlesLongWithProfit = 13 // take long profit latest after x candles *changed from 12

ONCE maxCandlesShortWithProfit = 10 // take short profit latest after x candles

ONCE maxCandlesLongWithoutProfit = 35 // limit long loss latest after x candles

ONCE maxCandlesShortWithoutProfit = 10 // limit short loss latest after x candles *changed from 25

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 1 //0 *changed from 0

ONCE January2 = 0 //0

ONCE February1 = 0 //0

ONCE February2 = 1.5 //2 *changed from 2

ONCE March1 = 0 //0

ONCE March2 = 0 //0

ONCE April1 = 1.5 //2 *changed from 2

ONCE April2 = 1.5 //2 *changed from 2

ONCE May1 = 0 //0

ONCE May2 = 1 //1

ONCE June1 = 0 //0

ONCE June2 = 1.5 //2 *changed from 2

ONCE July1 = 1.5 //2 *changed from 2

ONCE July2 = 0 //0

ONCE August1 = 0 //0

ONCE August2 = 0 //0

ONCE September1 = 2 //2

ONCE September2 = 0 //0

ONCE October1 = 1.5 //2 *changed from

ONCE October2 = 1.5 //1.5

ONCE November1 = 1.5 //2 *changed from 2

ONCE November2 = 1.5 //1.5

ONCE December1 = 1.5 //2 *changed from 2

ONCE December2 = 1.5 //2 *changed from 2

// calculate the scaling factor based on the parameter

scaleFactor = MIN(maxRisk, MAX(startRisk, ROUND(StrategyProfit / increaseRiskLevel) * increaseRiskStep))

// dynamic position sizing based on weekly performance

ONCE profitLastWeek = 0

IF DayOfWeek <> DayOfWeek[1] AND DayOfWeek = 1 THEN

IF StrategyProfit > profitLastWeek + 1 THEN

positionSize = MIN(trendMultiplier, positionSize + 1) // increase risk

ELSE

positionSize = MAX(1, positionSize - 1) // decrease risk

ENDIF

profitLastWeek = strategyProfit

ENDIF

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

previousDailyHigh = DHigh(2)

// calculate weekly high, weekly low is a poor signal

If DayOfWeek < DayOfWeek[1] AND lastweekbarindex = 0 THEN

lastWeekBarIndex = BarIndex

ELSE

IF DayOfWeek < DayOfWeek[1] THEN

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

ENDIF

// calculate monthly high/low

IF Month <> Month[1] AND lastMonthBarIndex=0 THEN

lastMonthBarIndex=barindex

ELSIF Month <> Month[1] THEN

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime THEN

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

ENDIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal multiplier

currentDayOfTheMonth = OpenDay

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

s3 = signalline CROSSES UNDER previousDailyHigh

// long entry with order cumulation

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize * saisonalPatternMultiplier) * scaleFactor)

IF (COUNTOFPOSITION + numberContracts) <= maxPositionSizeLong * scaleFactor THEN

IF SHORTONMARKET THEN

EXITSHORT AT MARKET

ENDIF

BUY numberContracts CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize) * scaleFactor)

IF (COUNTOFPOSITION + numberContracts) <= maxPositionSizeLong * scaleFactor THEN

IF SHORTONMARKET THEN

EXITSHORT AT MARKET

ENDIF

BUY numberContracts CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ( (s1 AND f3) OR (s2 AND f1) OR (s3 AND f3) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize * ABS(saisonalPatternMultiplier)) * scaleFactor)

IF (ABS(COUNTOFPOSITION) + numberContracts) <= maxPositionSizeShort * scaleFactor THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

SELLSHORT numberContracts CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize) * scaleFactor)

IF (ABS(COUNTOFPOSITION) + numberContracts) <= maxPositionSizeShort * scaleFactor THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

SELLSHORT numberContracts CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

stopLoss = stopLossLong * 0.1

takeProfit = takeProfitLong * 2

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

wp01Participant

Master

@Gianluca,

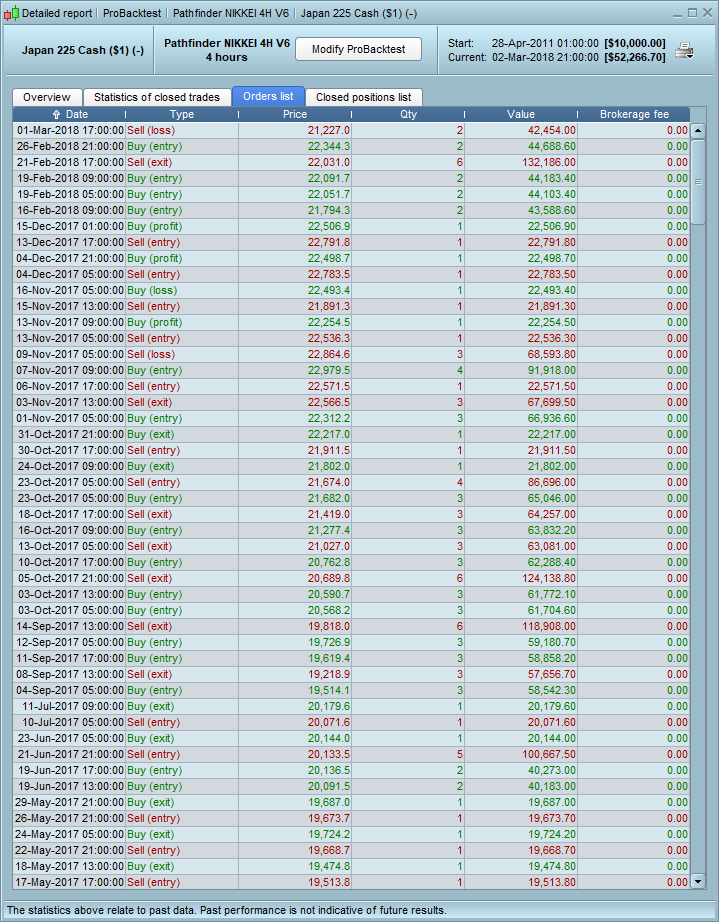

I loaded PF Nikkei V6 to check the latest positions and V6 also opened a position on the same date and time. I see in your tradelog that the opening was from PF V7, but

have you checked that you also activated the correct version in ProOrder or that maybe an old version is hanging there? I’m asking because your BT also show two versions.

Dajvop and Pfeiler are also running PF Nikkei V7. Maybe they can tell you if they had the same positions.

Kind regards,

Hello Wp thank you for your reply, the version on the screenshot are almost the same, i am running the code that i’ve posted, no trade on Backtest, trade in real :-/ Could you try to backtest it the same?

wp01Participant

Master

@Gianluca,

I already loaded your mac version and i get the same results as you have.

When did you activate it in ProOrder? There is a date on the right in ProOrder. I’m asking because i had some issues in the past when i activated a code in ProOrder while it is in position,

live and backtest were not always in sync. So if you activated it between 16-02-2018 09:00 hours and 26-02-2018 05:00 hours you were not have all the buys. I’m not sure if it goes well when the position

is closed. I can remember i had a few times a problem with that in the past. But this is easy to check for you. If it was before that date than this could not be the problem and i’m out of options.

Mmm i started the code on 20 of february…i need to try from that day, i will next week now i will be out for holiday.

@gianluca and @wp01

I activated the latest NIKKEI v7 on Feb 6. The first buy was on Feb 16 0900, the second on Feb 19 0500 and the third on Feb 19 0900. Now, the backtest and live trading differs.

BT buys on Feb 21 0900 and then exits on Feb 26 0500.

LT exits all positions on Feb 21 1700, then buys on Feb 26 2100 and exits with loss on Mar 1 1946.

wp01Participant

Master

Thanks dajvop. The latest trade is the same as Gianluca reported after he activated it on the 20th. of february.

Do you have an idea why it bought on the 26th. at 09.00 and why it didn’t show up in the BT?

My idea is that it bought a position because of the dynamic positionsize. The algo had a profit in the week before.

IF DayOfWeek <> DayOfWeek[1] AND DayOfWeek = 1 THEN

IF StrategyProfit > profitLastWeek + 1 THEN

positionSize = MIN(trendMultiplier, positionSize + 1) // increase risk

ELSE

positionSize = MAX(1, positionSize – 1) // decrease risk

ENDIF

profitLastWeek = strategyProfi

You also had the full profit because you activated it earlier instead of Gianluca. He activated it the 20th. According to your tradelog from above he didn’t had one of the buy orders.

I think the reason why the results differ from the LT is that when you start the algo, it also starts with 1 position, depending on the risk you take. But when you look at the BT for over

5 or more years it had already increased multi positions and risk because of the positive results. Looking at the dynamic positionsize it increases the positionsize looking at results and

seasonal multiplier. (see line 47 and 48). When activated in LT it basicly starts at zero.

@wp01

You are correct.

If I start the BT on Feb 6, then the result is identical to LT.

Buongiorno a tutti e un ringraziamento speciale a Reiner per la sua disponibilità, ha preso a disposizione il suo sistema pathfinder. Ho notato che quando uso pathfinder in modo reale le operazioni sono differenti da quelli eseguiti su backtest. Ho anche notato che, in modo reale, le operazioni dipendono dal momento in cui si avvia il sistema. La mia domanda è: qual è il momento giusto si deve lanciare il sistema? Qual è il momento giusto per le operazioni in modo reale coincidere con quelli in modo backtest? Grazie mille per l’eventuale risposta.

reb

rebParticipant

Master

Hello Ant.g

Il mio italiano non e sufficiente per una risposta

This post is in the english forum, so could you be kind to continue in this language ?

thks

Reb