At the bottom of my code, I added this line

if longonmarket and close>positionprice and RSI[14](close)crosses under 70 and barindex-tradeindex>30 and opentime<130000 and close[1]-open[1]>20 then

sell at market

ENDIF

I modified the code for long entry and the difference between the two versions is high-high[1]>5

MM=average[30]

//and high-high[1]>5

cndLong= OPEN>MM and dopen(0)<close and high-close>1 and high-close<20 and low[1]<close

// Conditions to enter long positions

If close > lowest[Pbars](low) and c1 and opendayofweek <> 5 and F1 and cndLong then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

or this version

MM=average[30]

//

cndLong= OPEN>MM and dopen(0)<close and high-close>1 and high-close<20 and low[1]<close and high-high[1]>5 and not(open<low[1])

// Conditions to enter long positions

If close > lowest[Pbars](low) and c1 and opendayofweek <> 5 and F1 and cndLong then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

Hi Robert841 – Depending on the index, and whether it’s CFD or Spreadbet, it’s 0.2 or 0.5. Once you’ve run it in demo for a bit and are happy then you can try it on a small size.

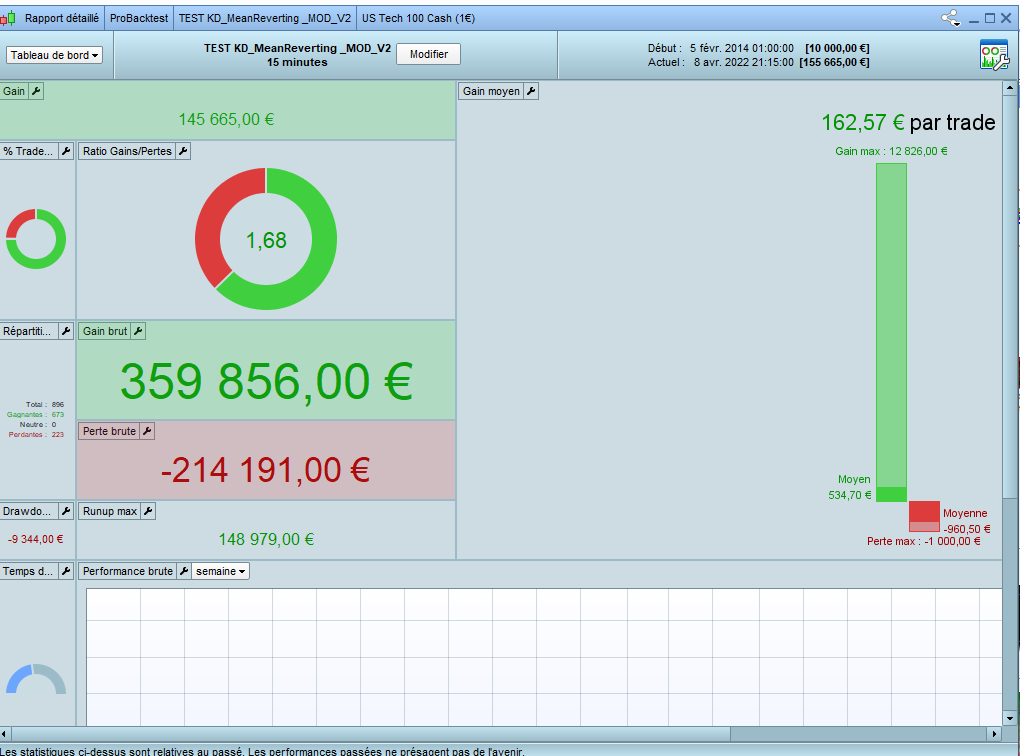

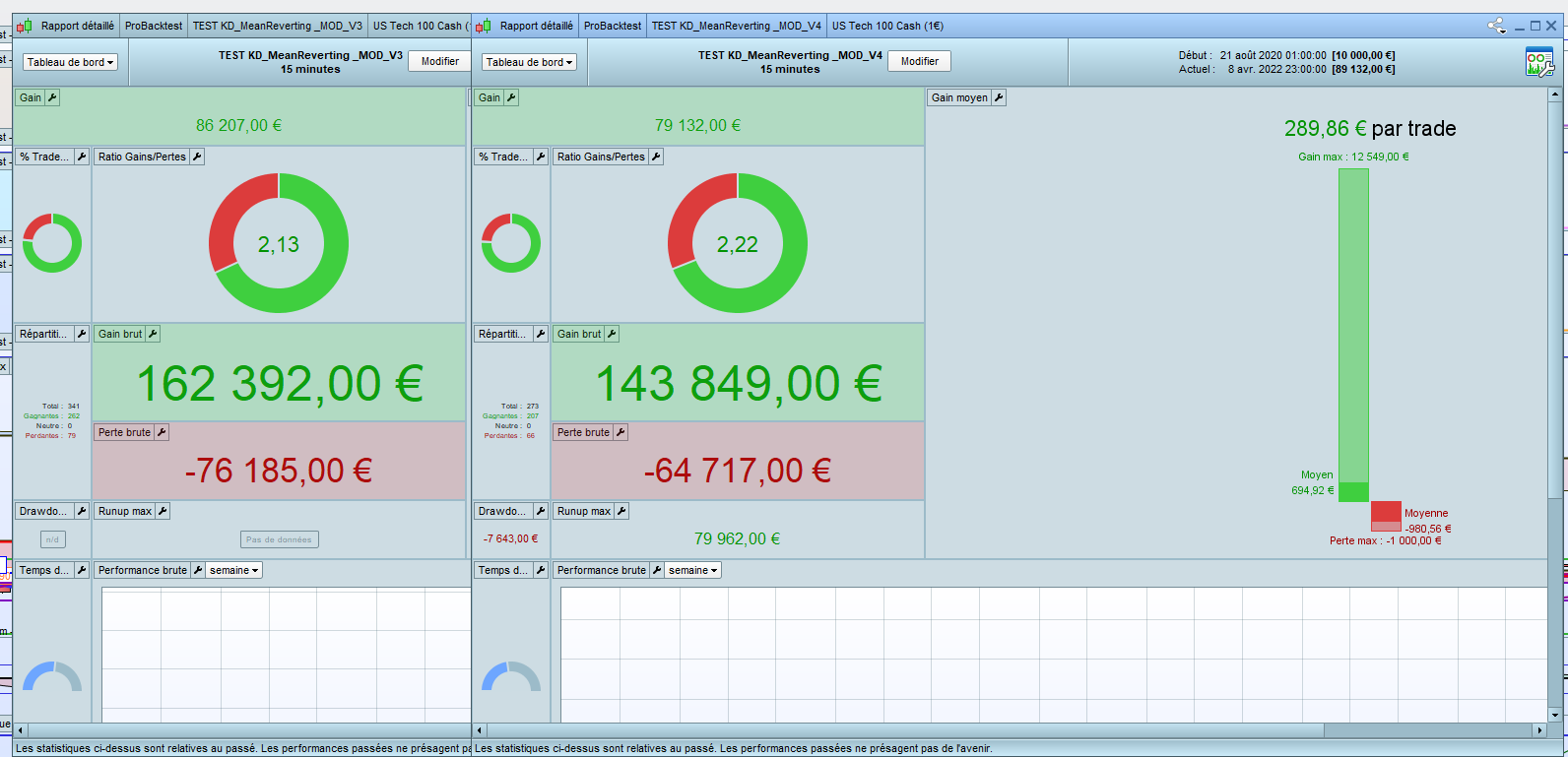

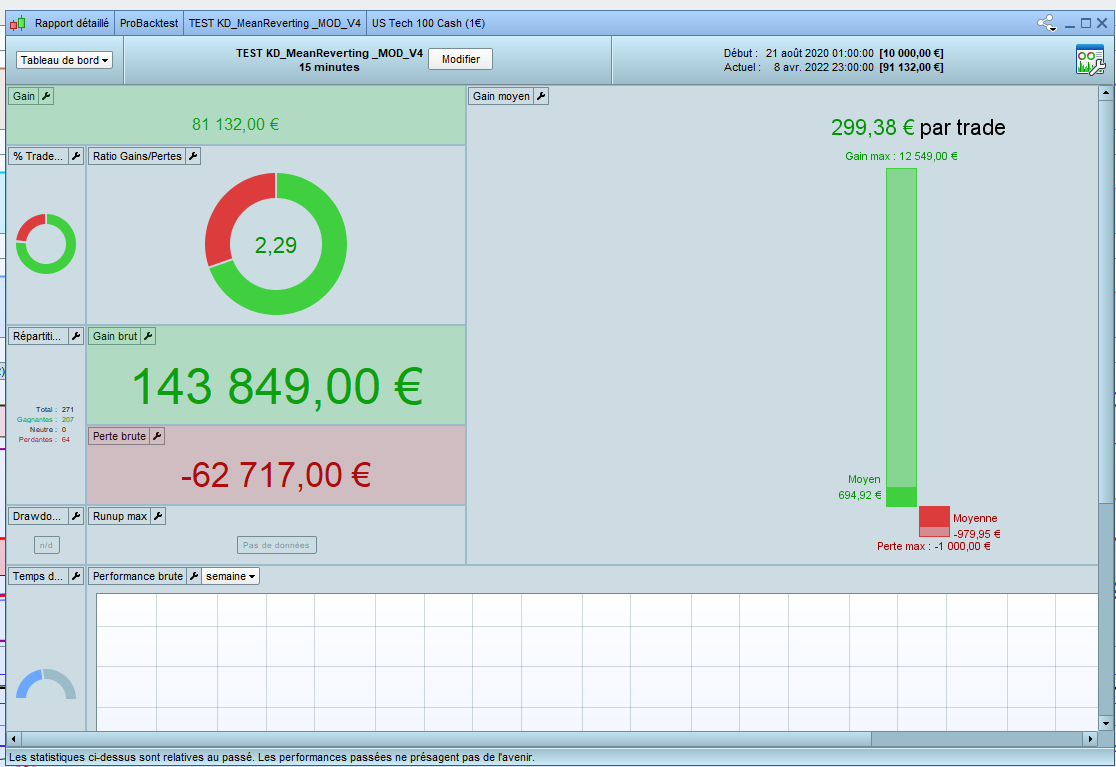

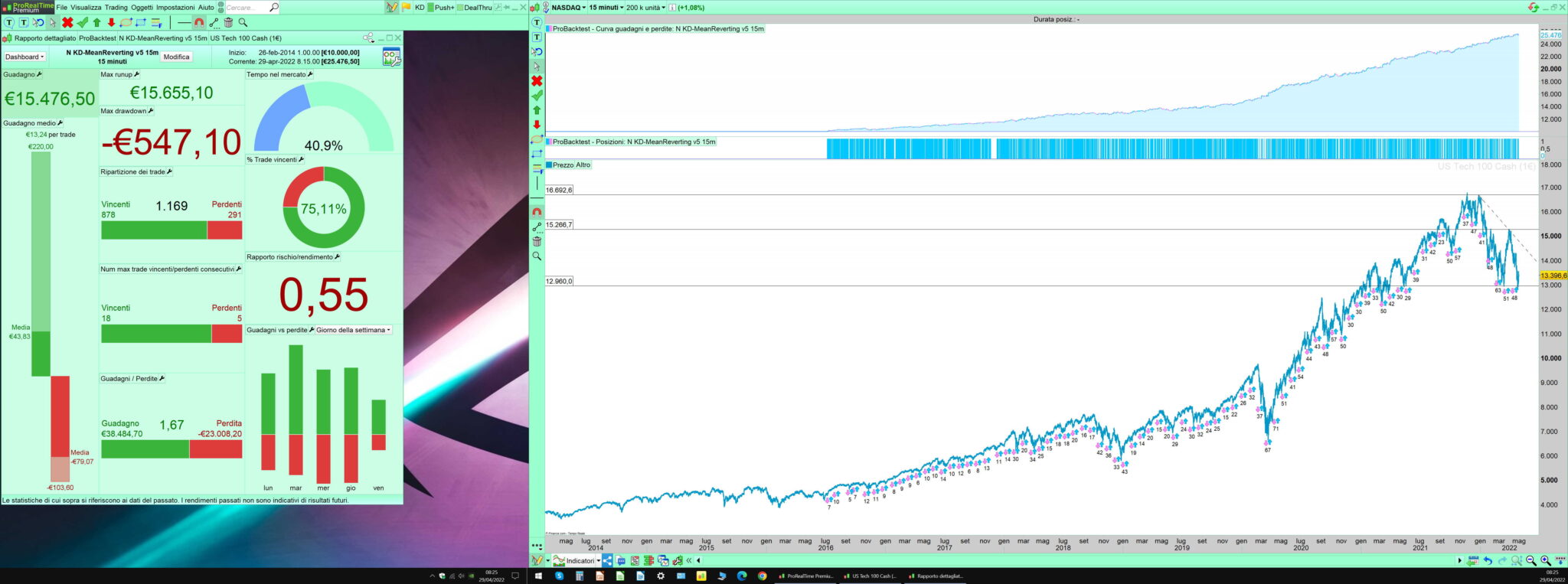

Hi, this is one of my revised and simplified versions (v5) with the addition of Fifi improvement.

//TS KD Mean Reverting v5 - Nasdaq 15 min

// spread 2 points

DEFPARAM CUMULATEORDERS = FALSE

positionSize = 1

//--------------------------------------------------------

avgHull = average[150,7]

nBarsVolume = 15

average30 = average[30](close)

//--------------------------------------------------------

c1L = close > avgHull

c2L = volume < volume[nBarsVolume]

c3L = open > average30 and dOpen(0)< close and high - close > 1 and high - close < 20 and low[1] < close // [Fifi improvement "cndLong": rif. 191539]

//--------------------------------------------------------

If c1L and c2L and c3L and nLoss < nLossMax and openDayOfWeek <> 5 then

buy positionSize contracts at market

endif

//-------------------------------------------------------------------------------------

set target pProfit 220

set stop pLoss 100

//-------------------------------------------------------------------------------

once nLoss = 0

nLossMax = 2 //max N daily losses

if intradayBarIndex = 0 then

nLoss=0

endif

if strategyProfit < strategyProfit[1] then

nLoss=nLoss +1

endif

//------------------------------------------------------------------------

EZT = 1 //EZT (exit zombie trades - Nonetheless)

if EZT then

if longOnMarket and (barIndex-tradeIndex(1)>= 1600 and positionPerf<0) then

sell at market

endif

endif

//-----------------------------------------------------

EWT = 1 //(exit winning trades - MauroPro)

nCandles = 8

percentTP = 1.8

endTime = 080000

if EWT then

if longOnMarket and (barIndex-tradeIndex(1)>nCandles and positionPerf*100 > percentTP) and (time>000000 and time<endTime) then

sell at market

endif

endif

//------------------------------------------------------------------

myRsi = rsi[14](close) //RSI exit

if myRsi < 30 and longOnMarket and close > positionPrice then

sell at market

endif

//----

if longOnMarket and close>positionPrice and RSI[14](close)>70 and close-open>100 then //added by Fifi

sell at market

ENDIF

//-------------------------------------------------------------------------------------------

pointToReachLong = 38*pointSize // 30

pointToKeepLong = 12*pointSize

If not onMarket then

newSL = 0

endif

If longOnMarket then

If newSL = 0 and high-tradePrice(1)>pointToReachLong then

newSL = tradePrice(1)+ pointToKeepLong

endif

If newSL > 0 and close-newSL>pointToReachLong then

newSL = newSL+pointToKeepLong

endif

endif

If newSL > 0 then

sell at newSL STOP

endif

//-----------------------------------------------------------------------------------------------------

once bollPeriod = 20 // bollPercent Exit

once multiplier = 2

avgBoll = average[bollperiod,1](close)

stDevBoll = std[bollperiod]

bollUp = avgBoll + multiplier * stDevBoll

bollDown = avgBoll - multiplier * stDevBoll

bollPercent = 100 * (close - bollDown) / (bollUp - bollDown)

//-----------------------------------------------------------------------------

once rangeOk = 40

once timeOk = 0

if time <= 090000 or time >= 210000 and (high - low) > rangeOk then

timeOk = 0

endif

IF time >= 080000 and time <= 200000 and (high - low) > rangeOk then

timeOk = 1

endif

period = 4 // exit with 2 of the last 4 bars below the threshold of 40 bollPerCent

levelPercent = 40

candleNum = 2

if timeOk = 1 and (barIndex - tradeIndex) < 12 and summation[period](bollPercent < levelPercent) = candleNum then

sell at market

endif

//------------------------------------------------------------------------------------------------------------