Hello,

A work in progress strategy based on a simple mean reversion idea inspired by Kevin Davey that I have adapted from a daily to a 15 minute timeframe. It looks for low volume and low price over N bars, then goes long. Only two entry criteria and one initial filter, and works well but needs improving.

The focus at this stage is to work on reducing the Drawdown, and potentially the number of trades, by use of an entry filter. Thought I would share this early version in the hope that people might have some useful ideas for a suitable filter.

NASDAQ

15m

Spread 2

Thank you,

S

With screenshot that was dropped

Really impressive, thanks for sharing! 🙂

Wow. Impressing. No short entrys?

//================================================

// Code: TEST KD3 Mean Reverting v1

// Source: https://www.youtube.com/watch?v=D_P_XqB5nHs

// Entry Strategy #3 Mean REverting

// Author: Kevin Davey

// Version 1

// Index: NASDAQ

// TF: 15 min

// TZ: Europe

// Notes: v1.1 Long Olny

// Notes: v1.2 Entry Filter (optimised to 150 MA)

// Notes: v1.3 Day of week - do not trade Friday's

//

// Pending Test Short side

// Reduce Drawdown (Long Entry Filter)

//================================================

DEFPARAM CUMULATEORDERS = FALSE

//Risk Management

PositionSize=1

//=== Entry Filter ===

//Filter 1

indicator1=average[150,7]

F1 = close>indicator1

//Range Parameters

Nbars=15

Pbars=10

//Entry Criteria

indicator1 = Volume

c1 = (indicator1 < indicator1[Nbars])

// Conditions to enter long positions

If close > lowest[Pbars](low) and c1 and opendayofweek <> 5 and F1 then

Buy PositionSize CONTRACTS AT MARKET

ENDIF

// Conditions to enter short positions

//IF rrange>2*stdrange+avgrange and close<close[10] THEN

//SELLSHORT PositionSize CONTRACTS AT MARKET

//ENDIF

// Stops and targets

SET STOP LOSS 100 //50

SET TARGET PROFIT 175 //50

//FOR STOPLOSS MANNGEMENT

// Conditions to enter long positions

startBreakeven = 30

PointsToKeep = 12

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

//************************************************************************

IF longonmarket and barindex-tradeindex>1600 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>1800 and close>positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<30 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

//===================================

once openStrongLong = 0

once openStrongShort = 0

if (time <= 090000 or time >= 210000) then

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 30

once tradeMin = 2500

IF (time >= 090500) AND (time <= 090500 + tradeMin) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

once trendPeriod = 80

once trendPeriodResume = 10

once trendGap = 4

once trendResumeGap = 4

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//Started real wrong direction

once strongTrend = 60

once strongPeriod = 4

once strongTrendGap = 2

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod - strongTrendGap then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod - strongTrendGap then

sell at market

ENDIF

//SET STOP $LOSS stoploss

One thing you might want to look at is the section starting at line 73 above. In a 10 year backtest no trades have gone to 1600 bars so those values are doing nothing. This is also the case for the Breakout code you posted.

This is the snippet I use for that function, closes very long-running positions whether they’re winning or losing. You have to optimise for b1 and b2 (b3, b4 for short).

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF longonmarket and (barindex-tradeindex(1)>= b1 and positionperf>0) or (barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF shortonmarket and (barindex-tradeindex(1)>= b3 and positionperf>0) or (barindex-tradeindex(1)>= b4 and positionperf<0) then

exitshort at market

endif

endif

whats the different between B1 and B2 flr longmarket?

b1 if it’s winning, b2 if it’s losing.

but I should add that this isn’t always advantageous, you should also try switching it off, with some algos it’s better to just let them run.

B1 is for pp > 0 and B2 is for pp < 0.

I have successfully used above on several of my Algos from my early coding days, I will get back on it again, now I see you’re using it Nonetheless! 🙂

I also optimised using broad values for positionperf (in lieu of 0 as above).

but I should add that this isn’t always advantageous, you should also try switching it off, with some algos it’s better to just let them run.

Without this remark I already wanted to add :

I have attempted so many means of exiting because of too long “useless” trades. They always and always net lose. Otherwise this will be highly subject to curve fitting, IMO.

BUT

Only last week I applied a “strange” means for this : let shrink the SL per bar (or once in the so many, also OK). This seems counterproductive, but the contrary appears true. This starts with allowing for a higher SL (avoid peaks at entry) which is psychologically good. Next the losses because or running into the SL in practice are not that high at all. But moreover, this works out. For me it does …

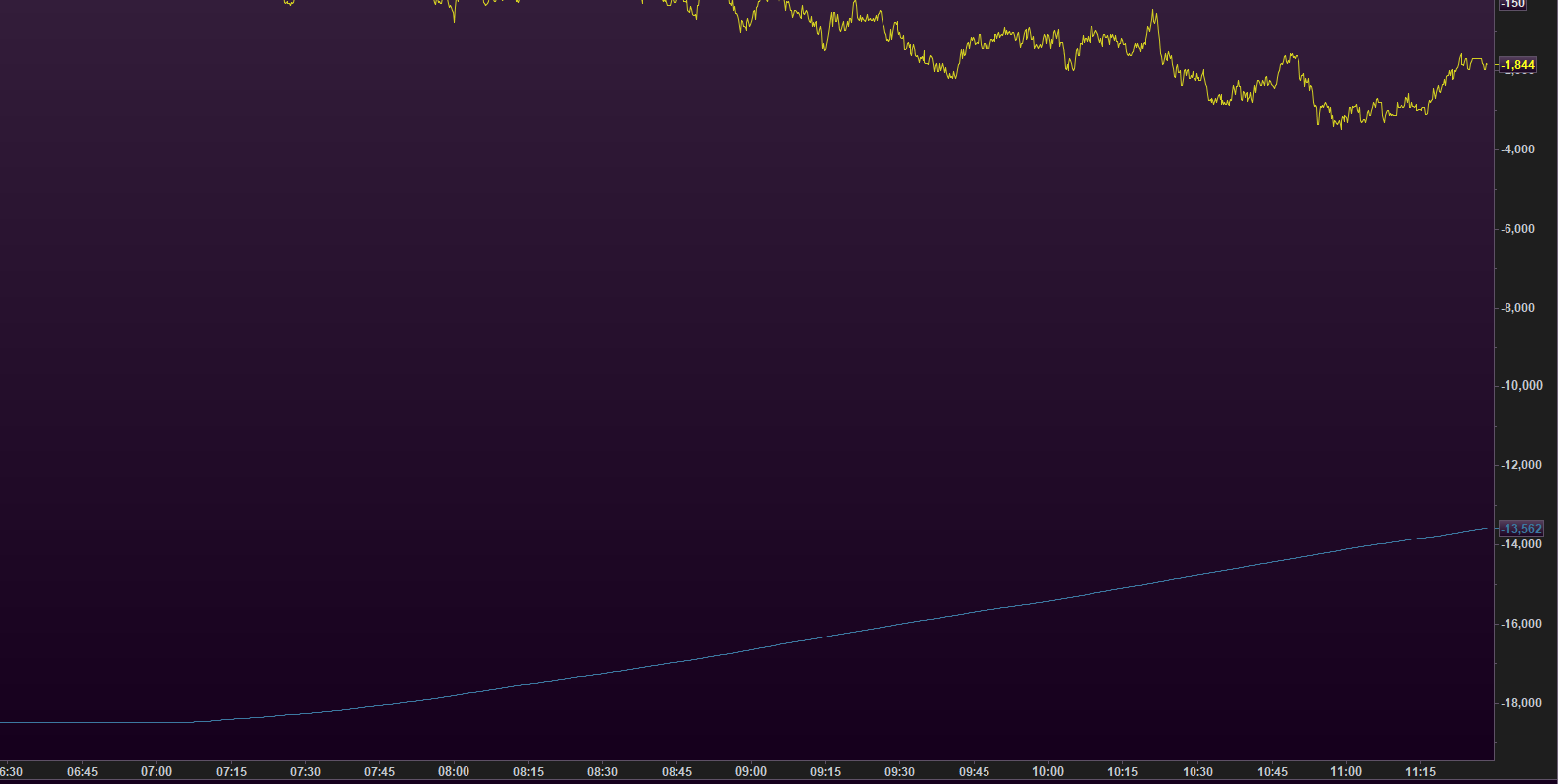

Warning : I am almost sure that we should not change the StopLoss per bar because the broker may not like that. Eh, *if* possible at all. So it needs to be your own exit (like the example code in the earlier post) and NOT changing the StopLoss each time.

Visualisation of what I was saying : when blue and yellow meet, it’s over.

thanked this post

One thing you might want to look at is the section starting at line 73 above. In a 10 year backtest no trades have gone to 1600 bars so those values are doing nothing. This is also the case for the Breakout code you posted.

This is the snippet I use for that function, closes very long-running positions whether they’re winning or losing. You have to optimise for b1 and b2 (b3, b4 for short).

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF longonmarket and (barindex-tradeindex(1)>= b1 and positionperf>0) or (barindex-tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF shortonmarket and (barindex-tradeindex(1)>= b3 and positionperf>0) or (barindex-tradeindex(1)>= b4 and positionperf<0) then

exitshort at market

endif

endif

//EXIT ZOMBIE TRADE

EZT = 1

if EZT then

IF longonmarket and (barindex–tradeindex(1)>= b1 and positionperf>0) or (barindex–tradeindex(1)>= b2 and positionperf<0) then

sell at market

endif

IF shortonmarket and (barindex–tradeindex(1)>= b3 and positionperf>0) or (barindex–tradeindex(1)>= b4 and positionperf<0) then

exitshort at market

endif

endif

Thank you very much, I shall add this in and retest. Much appreciated.

I also optimised using broad values for positionperf (in lieu of 0 as above).

Would u like to show an example

I played a bit with the strategy, on DAX 1€, 200K units, 5 min-TF (mtf), changing just TP & SL and slightly the Trailing Stop to use PointsToKeep as sort of a trailing step. Performance is nice and WF is around 25%. I also commented out exiting on RSI:

//================================================

//https://www.prorealcode.com/topic/nasdaq-mean-reversion/

//

// Code: TEST KD3 Mean Reverting v1.3

// Source: https://www.youtube.com/watch?v=D_P_XqB5nHs

// Entry Strategy #3 Mean REverting

// Author: Kevin Davey

// Version 1

// Index: DAX (ex NASDAQ)

// TF: 15 min

// TZ: Europe

// Notes: v1.1 Long Olny

// Notes: v1.2 Entry Filter (optimised to 150 MA)

// Notes: v1.3 Day of week - do not trade Friday's

//

// Pending Test Short side

// Reduce Drawdown (Long Entry Filter)

//================================================

DEFPARAM CUMULATEORDERS = FALSE

Timeframe(2h,UpdateOnClose) //1h

//Risk Management

nLots=1

//=== Entry Filter ===

//Filter 1

indicator1 = average[150,7] //150,7

F1 = close>indicator1

F2 = close<indicator1

//Range Parameters

Nbars = 15 //15

Pbars = 10 //10

//Entry Criteria

indicator1 = Volume

c1 = (indicator1 < indicator1[Nbars])

// Conditions to enter long positions

If close > lowest[Pbars](low) and c1 and opendayofweek <> 5 and F1 and Not OnMarket then

Buy nLots CONTRACTS AT MARKET

ENDIF

// Conditions to enter short positions

If close < highest[Pbars](high) and c1 and opendayofweek <> 5 and F2 and Not OnMarket then

//SELLSHORT nLots CONTRACTS AT MARKET

ENDIF

// Stops and targets

SET STOP pLOSS 50 //50

SET TARGET pPROFIT 70 //75

once openStrongLong = 0

once openStrongShort = 0

if (time <= 090000 or time >= 210000) then //090000 - 210000

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 30

once tradeMin = 2500

IF (time >= 090500) AND (time <= 090500 + tradeMin) AND ABS(close - open) > rangeOK THEN

IF close > open and close > open[1] THEN

openStrongLong = 1

openStrongShort = 0

ENDIF

IF close < open and close < open[1] THEN

openStrongLong = 0

openStrongShort = 1

ENDIF

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

once trendPeriod = 80

once trendPeriodResume = 10

once trendGap = 4

once trendResumeGap = 4

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//Started real wrong direction

once strongTrend = 60 //60

once strongPeriod = 4 //4

once strongTrendGap = 2 //2

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod - strongTrendGap then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod - strongTrendGap then

sell at market

ENDIF

//SET STOP $LOSS stoploss

Timeframe(default) //5 min

// Breakeven & Trailing Stop

startBreakeven = 25 //25

PointsToKeep = 5 //5

Distance = 6 //6

//

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

//

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=(startBreakeven*pipsize+PointsToKeep*pipsize) and breakevenlevel = 0 THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

IF LONGONMARKET AND close-breakevenlevel>=(startBreakeven*pipsize) and breakevenlevel > 0 THEN

breakevenLevel = breakevenlevel+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

IF close > (breakevenlevel + Distance) THEN

SELL AT breakevenLevel STOP

IF close < (breakevenlevel - Distance) THEN

SELL AT breakevenLevel LIMIT

ELSE

SELL AT Market

ENDIF

ENDIF

ENDIF

//************************************************************************

ONCE MaxBars = 305 //305

//

IF longonmarket and barindex-tradeindex>MaxBars then//and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>MaxBars then//and close>positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<30 and barindex-tradeindex>1 and longonmarket and close>positionprice then

//sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

//exitshort at market

endif

//===================================

@samsampop, what is the result about kevin’s initial strategy on daily timeframe ? thx

Hello MAKSIDE

I put the source for the original link at the top of the code, it’s pretty decent but I tend not to trade algos on a daily basis, only US OTC stocks.

Source: https://www.youtube.com/watch?v=D_P_XqB5nHs

Thanks