Hi guys

I have the same problem, I think others have it too.

There is someone more experienced who can help us

Thank you

God, new problem.

I have tried all mentioned above and with combination with the trail from #165967, no luck…

I think the problem is with your Stoch-RSI values, esp the first one (lengthRSI = 1)

This is the lookback period for the RSI so a value of 1 doesn’t make sense – default value is 14

This is possibly giving you a div/zero problem in line 8 of the indicator: StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

In my own test version (that I knocked up v quickly and is not optimized), I put in a value of 4 and it hasn’t been rejected.

Unfortunately though, it seems that lengthRSI = 1 is also skewing the results.

Running a 1m bar optimization with a range of 4 – 14 in steps of 2 returns a value of 12 (leaving all other other values as they are) – see attached.

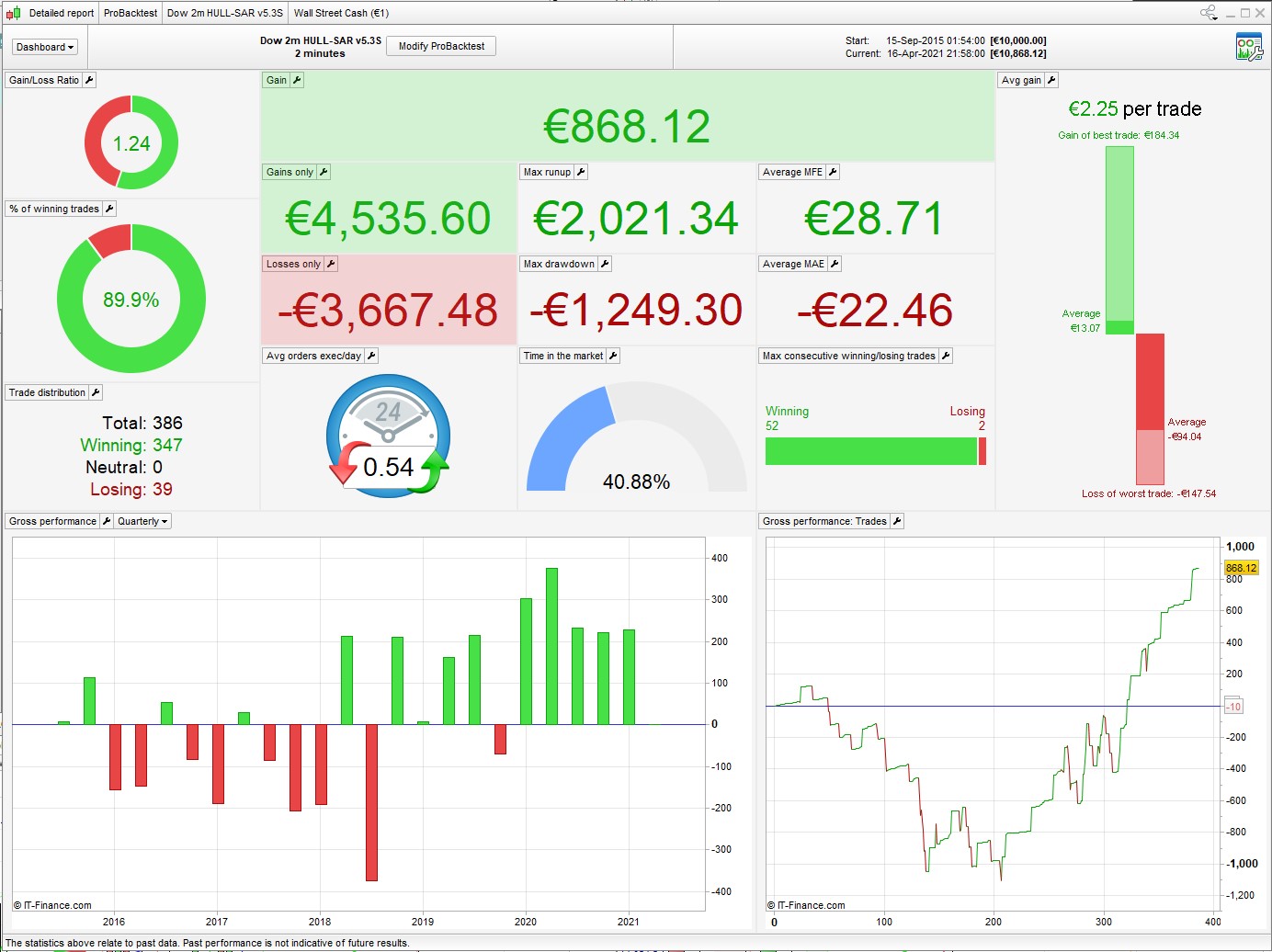

Here’s the itf

Hi Nonetheless,

I worked a bit the NAS 2m HULL-SAR v5.5L you share. I tested it a 18min timeframe in place of 12min (same as the V3b.3). I optimised q, w and e from this timeframe and the results are quit good in 200k and 1M. I share you the screenshot.

Thanks for that Laurent, could be worth exploring. Not a big change over 6 years, but distinctly better for the recent curve, esp the lower drawdown.

I know that when I was looking into a DJ version it def needed a higher TF on top, 20 mins – I should take another look at it.

I tested it a 18min timeframe

You likely will find that due to non-standard TF (18min does not divide into 1 hour) that the Live performance is very different from backtested performance.

I hope it isn’t … let us know please.

You likely will find that due to non-standard TF (18min does not divide into 1 hour) that the Live performance is very different from backtested performance. I hope it isn’t … let us know please.

Hi Grahal, can you explain me why it should be different in backtested and and Live (because not divide into 1 hour). I don’t know and understand the problem.

I had this idea because i’m using in Live the V3b.3 version and it’s working quite good.

Please let me know if i have to worry.

I have launch the v5.5L with 12min and also 18min TF. I will share you the results

Hello Laurent

is it possible to share your v5.5l versions ?

Thank you in advance

regards

can you explain me why

There was a member on here who persisted on running on 28 seconds (non-standard TF) and a few of us had big discussions and tests and in the end he gave up on the 28 sec TF. If you can find the Topic all the reasons why are discussed.

In essence it is because a non-standard TF runs out of sync with standard and even with itself relative to, for example, 1 hour, so on 18 min TF … 18 min past the hour, 36, 54, 12 min past the hour, 30, 48, 6 min past the hour etc etc.

Maybe the out-of-sync in your strategy works well?

I’m all for trying any maverick ideas, so let us know if the performance in Live is acceptable compared to your optimised backtest performance?

EDIT

You mentioned 12 min TF, this may perform better (?) as every hour it is back in sync with the 1 hour and itself … 12 past the hour, 24, 36, 48, 60 so next is 12 past the hour again.

There was a member on here who persisted on running on 28 seconds (non-standard TF) and a few of us had big discussions and tests and in the end he gave up on the 28 sec TF. If you can find the Topic all the reasons why are discussed. In essence it is because a non-standard TF runs out of sync with standard and even with itself relative to, for example, 1 hour, so on 18 min TF … 18 min past the hour, 36, 54, 12 min past the hour, 30, 48, 6 min past the hour etc etc. Maybe the out-of-sync in your strategy works well? I’m all for trying any maverick ideas, so let us know if the performance in Live is acceptable compared to your optimised backtest performance? EDIT You mentioned 12 min TF, this may perform better (?) as every hour it is back in sync with the 1 hour and itself … 12 past the hour, 24, 36, 48, 60 so next is 12 past the hour again.

Thanks for your explain. The only fed back i have is a good results between Live and backtest with the NAS-2m-HULL-SAR-v3b-3 who works with this sort of 18 min time frame.

As i said, i launch in live the v5.5L in 18 min too. I will tell you back the experience.

is it possible to share your v5.5l versions ?

You can find all pieces joint in top of this page with ” View all attachments”.

ok

I see attachment 95 is v5.5l, but it seems you are using other versions, you have modified few parameters ?

You mentioned 12 min TF, this may perform better

The 12m works fine, fairly consistent results between backtest and live. I think an 18m TF might be problematic if it were the entry level (assuming that big institutional traders are more likely to be working on 1h). But in this case the entry is at the 6m level – also non-standard but at least it hits the hour mark. The 18m is just a general trend filter, so should matter less ???

I see attachment 95 is v5.5l, but it seems you are using other versions, you have modified few parameters ?

This version is very good. It’s basis on this one i did some test with other time frame and it’s what we are talking about (12min / 18min TF)

The 12m works fine, fairly consistent results between backtest and live. I think an 18m TF might be problematic if it were the entry level (assuming that big institutional traders are more likely to be working on 1h). But in this case the entry is at the 6m level – also non-standard but at least it hits the hour mark. The 18m is just a general trend filter, so should matter less ???

Thanks for the answer. I launch the 2 versions in same time so i will compare them in live wih same basis.

They moved same for the trade of yesterday. It’s a good begining