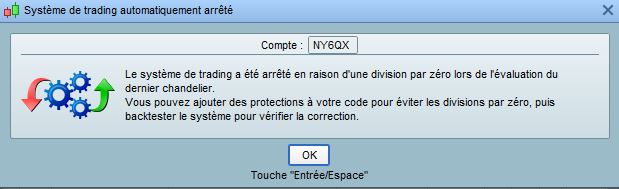

The test to go with Nikkei and version v5.5 Live is so just beaten after 1.5 hours ( Division Zero ) in the error display of PRT stands ” Add a protective device against division zero a “What can you do there??????

Hi Chrisinobi, NAS 1m Hull-SAR v.7.5 was built on PRT 10.3 with a very short backtest. After v11 came out I abandoned it and am now only running v5.5. I have no opinion on why v7.5 is getting errors as I can’t really recommend it at all.

As for making this work short, I spent some time on it and quickly decided that it wasn’t worth it. For me it works very nicely long-only – I have other programs that are better at short trades.

If you post your NIK v5.5 I can test it on 1m bars if you want.

Thank you that would be very nice. But I think v5.5 doesn’t work on Nikkei because of the bug, Division Zero. I looked at the chart and there are also miscarriages at 2min and I think that’s the problem and that’s why I tried higher time units with MTF to get no miscarriages, but that didn’t work either. I would like to buy some working Algos but unfortunately there is not the promised marketplace yet. Have just tested the v5.5 goes to other markets as well, let’s continue testing whether it runs live stable in other markets ? before investing time in any optimizations again. Must, of course, keep an eye on the spread and trading hours.

Missing candle, I said (-: if my translation program is mistranslated

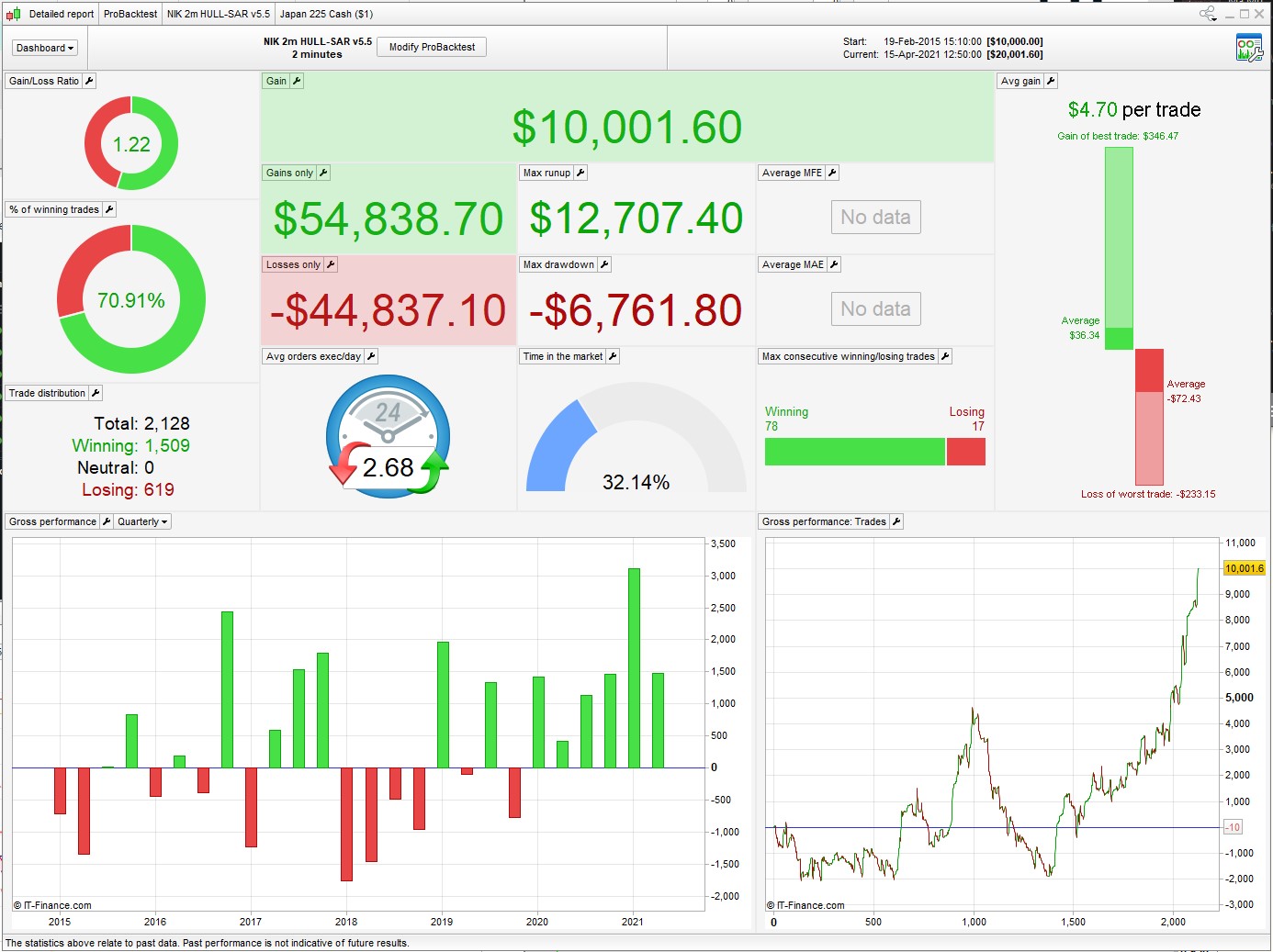

This is what it looks like over 6 years (positionsize=0.5 spread =7). One thing I noticed is that your Ctime settings cover a period when the Tokyo exchange is entirely closed, which is unusual.

You might get a better result optimizing for

Ctime = time >=020000 and time <080000//Euro time

My guess is this:

-One problem is with PRT when trying to auto insert values into the code. It gives the irrelevant error code of line 24 when the problem really is something else. PRT then adds decimal places by some reason. I have had the same thing happen on Another algo so I Think it´s a program problem with this new feature.

-The Hull-sar 5.3 algo problem with division by zero and not suffient preload bars might be Another thing since the algo seems to start when manually inserting fixed values in the code. Like i have mentioned i start with cumulate false and MM off. I can make it work for Long pos on some instruments and others not. When it comes to Short positions I can never make it work.

So Then maybe it has to do with the values I have chosen when optimizing for those markets!? Unfortunatly I´m not good enough at this to locate the problem where for example divizion by zero accours and there is no other option than to fail using this algo that for me looks promising on multiple markets…

Thanks anyway to nonetheless for providing this and many other interesting algos!

(Isn´t it strange that PRT can´t provide some tool to locate problems like divizion by zero since it seems to be a very common problem?)

I’ve made my own quick and dirty version of DJ v5.3 S and put it on Demo, I’ll let you know if it gets the same error. Might be awhile before the DJ goes sufficiently bearish…

That looks very good at first. I can’t go back that far. Thank you for your efforts! But unfortunately it doesn’t run live on Nikkei the v5.5. I have tried (Division Zero) My results were better when the Tokyo Stock Exchange is closed. but as already written, I don’t come back as far as you. Maybe someone in the forum will find the problem fixed so that you can test live whether it is profitable.

That looks very good at first

Everyone has their own attitude towards losses, but a full year is a very long time to wait for a strategy to come good. Bear in mind that if you were running this in 2018, you don’t have the benefit of knowing that in 2019 it gets better; all you see is losses month after month. I think you would ditch it and look for greener grass elsewhere (which is my honest advice – div by zero is not your biggest problem!)

Okay, I saw it, I agree with you. Sometimes I ask myself, can we win at all? I probably don’t think so. Last hope the marketplace !!!!! But hope dies last, thank you for your sacrifice.

Looks good for the first view. Maybe this have potenzial. The second version is TP optimized (points instead of %)

#161652 post

- DOW-SAR-2m-Test-2.itf

I used this code in autotrading it often stops because “stop loss is to close”. It’s very curious because SL is at 1.4%.

Anybody else has this problem ?

Thanks

Hello guys,

I finaly can launch the program in autotrading without probem. It doesn’t take postion yet but i don’t have error message.

With the advice i receive, i delete space line 2 and add endif around line 24. And i change preloadbars 10.000. Then, i can launch without problem. I will tell you if it works good.

I share you the itf file who run correctly.

It’s a short program who looks very good since 2018. i also join the 500k test in short only.

Thanks for all the work you did.

I speak too soon.

Now i have an error message of division by zero in last candle but only when i use optimization mode.

No error message when i use fixed position size.

Not done but we move on

Now i have an error message of division by zero in last candle but only when i use optimization mode. No error message when i use fixed position size. Not done but we move on

Got it. Just have to do becareful when you choose minipositionsize and startpositionsize. They have to be different.

Thats okay now. We got it.

God, new problem. I have an error after 1 hour running who say error calculation in the last candle. And the 2 modes stop : with and without optimisation