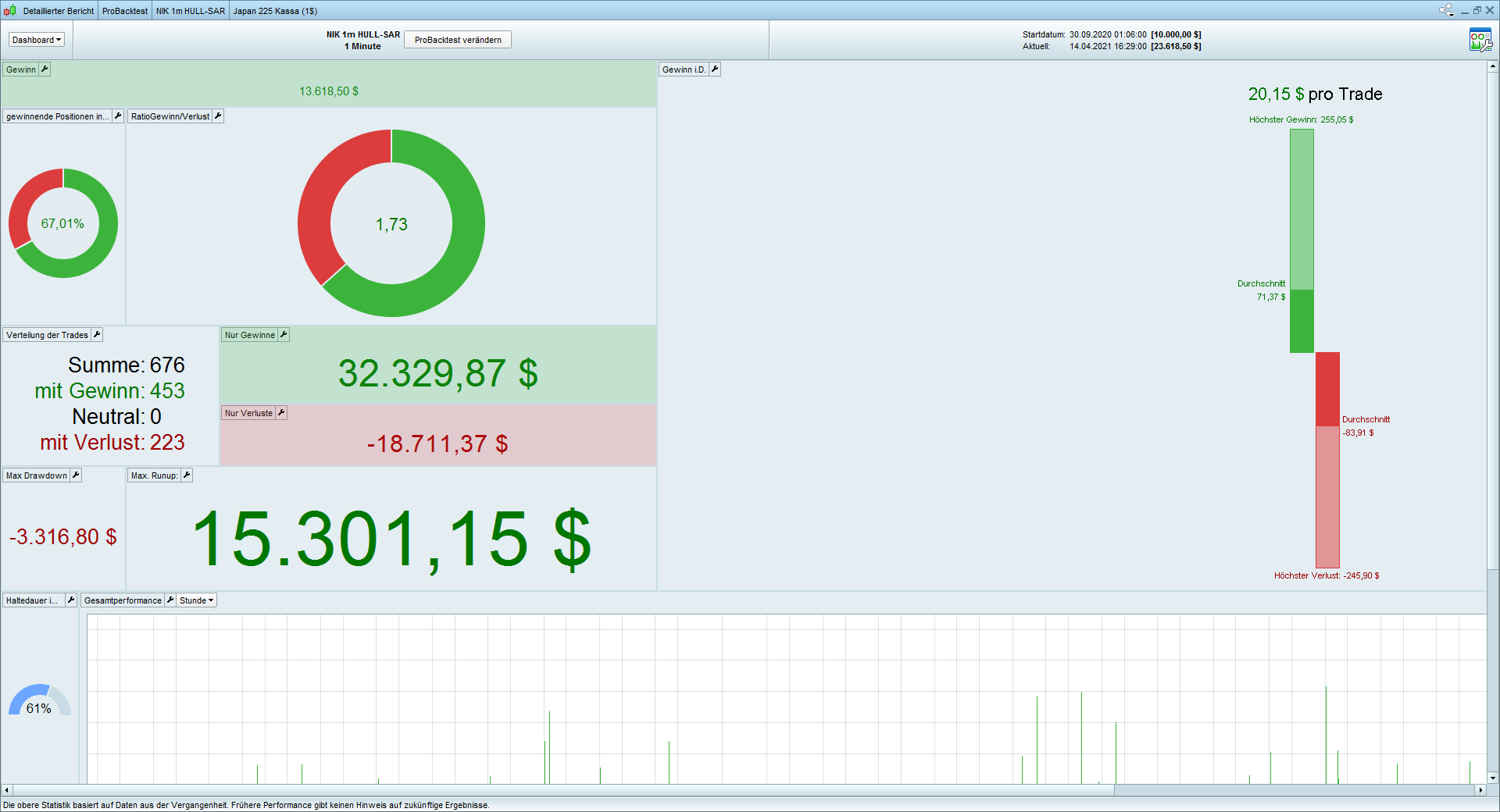

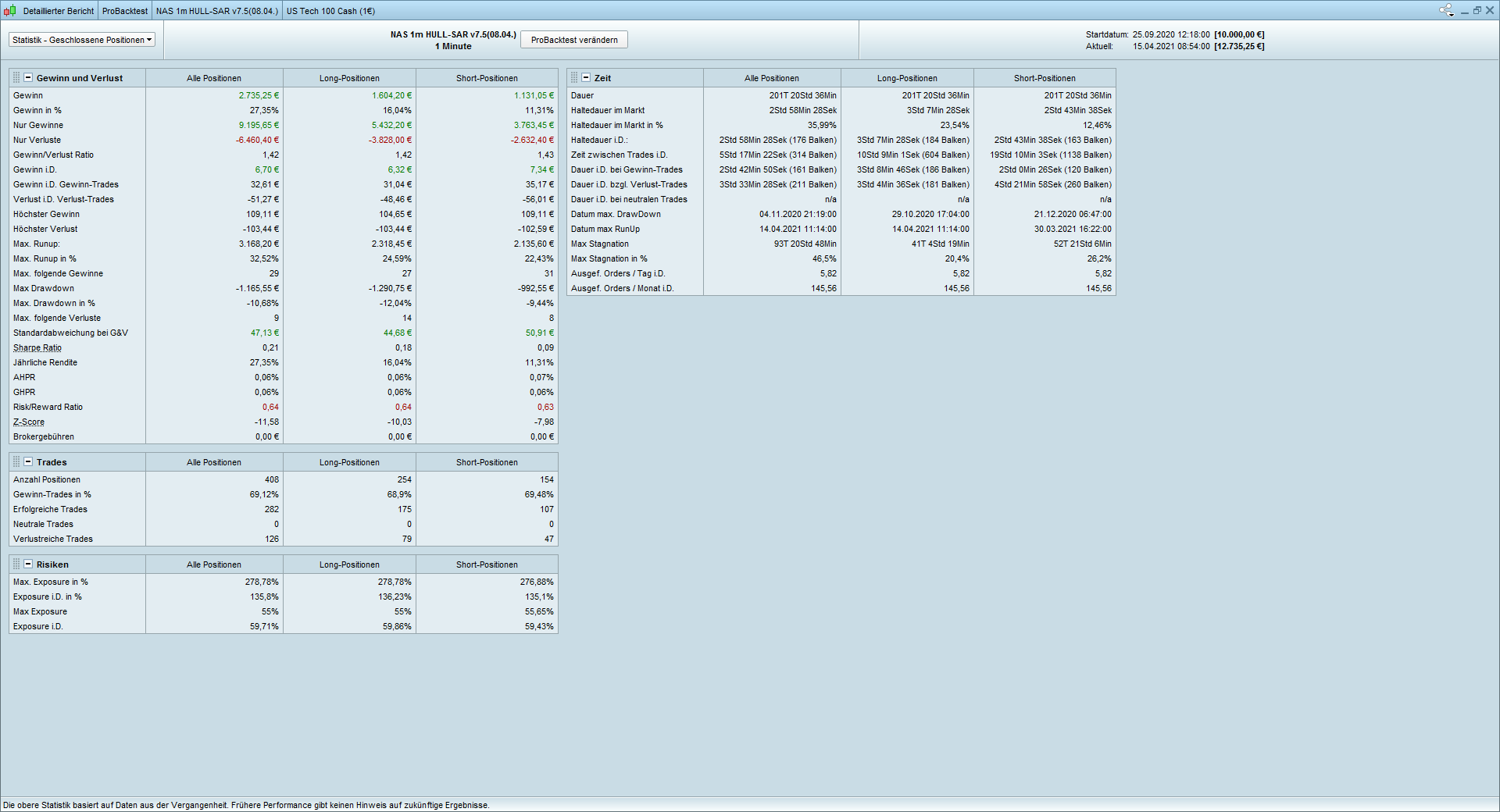

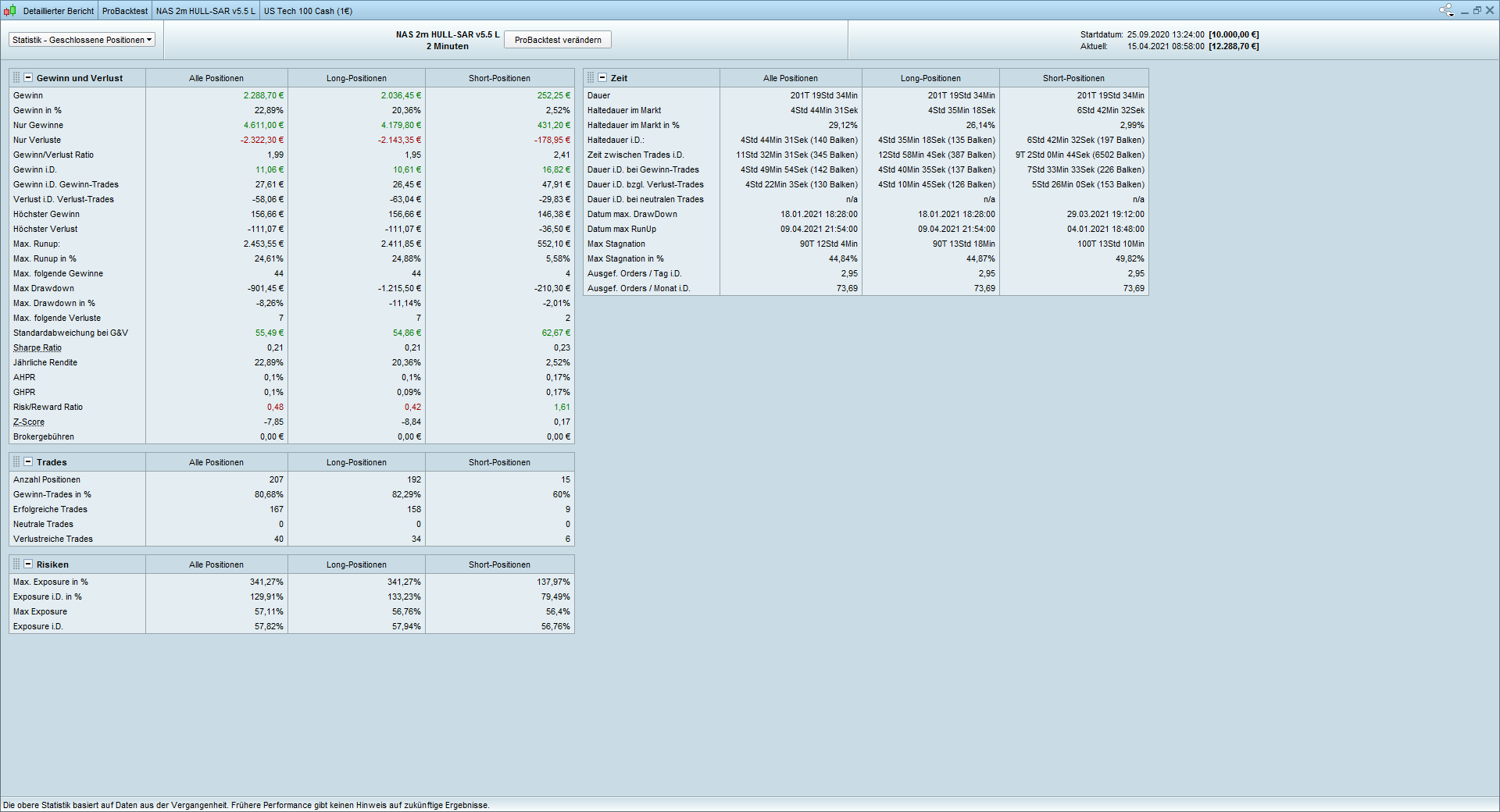

NIK 1m Hull-SAR

Hello everyone

Thank you very much for this good basic strategy. I ask for your indulgence and understanding, because I am still a beginner, do not speak English and work with a translator!

I do a test and optimization with Nikkei, with good results (see appendix). It doesn’t run live for very long and keeps getting error messages (see appendix). During the American trading hours it runs for 4 to 5 hours and a profit trade has already been achieved, but I need your help. How to get the algorithm stable, without error message and shutdown. On Nasdaq, things are going better but not perfect either, with 2 to 3 errors a week (always live).

– Error 1: Division by zero – what protections are there? That’s why I use MTF 5min over 7min to 22min total runs on 1min.

– Error 2: Historical data is not sufficient?

Ask for your help. I think the algorithm has potential. What is your opinion on this?

One more general question at the end. Can algorithms, after hundreds of hours of invested work, win in the long run? When will the marketplace come? ( I have at the moment 10 Algo live, of which 5 for rent )

Once again, pay tribute to your work!

Here are the .itf and pictures.

Thank you for your comment and help.

// Definition of code parameters

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

DEFPARAM preloadbars = 10000

//Money Management NAS

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=0.5

ENDIF

if MM = 1 then

ONCE startpositionsize = 0.5

ONCE factor = 6 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 200 // IG first tier margin limit

ONCE maxpositionsize = 2000 // IG tier 2 margin limit

ONCE minpositionsize = .5 // enter minimum position allowed

IF StrategyProfit <> StrategyProfit[1] THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF StrategyProfit <> StrategyProfit[1] THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

Ctime = time >=103000 and time <211400

TIMEFRAME(22 minutes)

Period= 80

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1] or HULLb > HULLa

c2 = HULLa < HULLa[1] or HULLb < HULLa

ST1 = SAR[0.02,0.015,0.025]

c1a = (close > ST1)

c2a = (close < ST1)

TIMEFRAME(7 minutes)

Periodb= 17

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c3 = HULLb > HULLb[1]

c4 = HULLb < HULLb[1]

c3b = HULLb > HULLb[1] and HULLb[1] < HULLb[2]

c4b = HULLb < HULLb[1] and HULLb[1] > HULLb[2]

ST2 = SAR[0.015,0.015,0.02]

c3a = (close > ST2)

c4a = (close < ST2)

//Stochastic RSI | indicator

lengthRSI = 3 //RSI period

lengthStoch = 3 //Stochastic period

smoothK = 6 //Smooth signal of stochastic RSI

smoothD = 4 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c3c = K>D

c4c = K<D

TIMEFRAME(5 minutes)

Periodc= 4

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c5 = HULLc > HULLc[1] and HULLc[1] < HULLc[2]

c6 = HULLc < HULLc[1] and HULLc[1] > HULLc[2]

c5b = HULLc > HULLc[1]

c6b = HULLc < HULLc[1]

ST3 = SAR[0.005,0.015,0.015]

c5a = (close > ST3)

c6a = (close < ST3)

TIMEFRAME(default)

Once MaxPositionsAllowed = 5*positionsize

// Conditions to enter long positions

IF not longonmarket and Ctime and c1 and c1a AND C3a and c3b and c3c AND C5a and c5b THEN

BUY positionsize CONTRACT AT MARKET

elsif longonmarket and Ctime and c1 and c1a and c3 and c3a and c5 and COUNTOFLONGSHARES < MaxPositionsAllowed then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.6

SET TARGET %PROFIT 1.4

ENDIF

// Conditions to enter short positions

IF not shortonmarket and Ctime and c2 and c2a AND C4a and c4b and c4c AND C6a and c6b THEN

sellshort positionsize CONTRACT AT MARKET

elsif shortonmarket and Ctime and c2 and c2a and c4 and c4a and c6 and COUNTOFSHORTSHARES < MaxPositionsAllowed then

sellshort positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.2

SET TARGET %PROFIT 1.7

ENDIF

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

once trailingpercentlong = 0.47 // %

once trailingpercentshort = 0.56 // %

once accelerator = 0.095 // 1 = default; always > 0 (i.e. 0.5-3)

once accelerator2 = 0.31 // 1 = default; always > 0 (i.e. 0.5-3)

once ts2sensitivity = 0 // [0]close;[1]high/low;[2]low;high

//====================

once steppercentlong = (trailingpercentlong/10)*accelerator

once steppercentshort = (trailingpercentshort/10)*accelerator2

if onmarket then

trailingstartlong = positionprice[1]*(trailingpercentlong/100)

trailingstartshort = positionprice[1]*(trailingpercentshort/100)

trailingsteplong = positionprice[1]*(steppercentlong/100)

trailingstepshort = positionprice[1]*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=2 then

ts2sensitivitylong=low

ts2sensitivityshort=high

else

ts2sensitivitylong=close

ts2sensitivityshort=close

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif