I am referring to NAS-2m-HULL-SAR-v5.3L and NAS-2m-HULL-SAR-v5.3-L, it happened the same on both versions (at least in my account). Did you have the same problem?

No, I haven’t seen that. I’m running v5.5, it opened 2 positions, still open with the trail in place, behaving as it should.

What I have found is that the Target Profit doesn’t register, and maybe has to be entered after each buy instruction, but that won’t effect the Trail.

// Conditions to enter long positions

if tradetype=1 or tradetype=2 then

IF not longonmarket and CB and Flag THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

elsif Ctime and longonmarket and CB2 and COUNTOFLONGSHARES < MaxPos and Flag then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

Flag = 0

elsif longonmarket and CB2 and positionperf <0 and COUNTOFLONGSHARES < MaxPos2 and Flag1 then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

Flag1 = 0

elsif longonmarket and CB2 and positionperf <0 and COUNTOFLONGSHARES < MaxPos2 and Flag2 then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

Flag2 = 0

elsif longonmarket and CB2 and positionperf <0 and COUNTOFLONGSHARES < MaxPos2 and Flag3 then

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS sl

SET TARGET %PROFIT tp

Flag3 = 0

ENDIF

ENDIF

Is anyone running v5.3 SHORT (Tradetype = 3 to go Short) on a real account, in any market, without problems?

See #165505 for what i´m struggeling with.

I had a quick look at DJ 2m HULL-SAR v5.3S and I think there’s something wrong with the trail – try replacing it with this. Backtests ok but I haven’t tried running it.

The DJ looks like it might have some potential going short, I don’t think the NAS is worth the effort.

// %trailing stop function incl. cumulative positions

once trailingstoptype1= 1

if trailingstoptype1 then

//====================

trailingpercentlong = .28 // %

trailingpercentshort = TP02 // %

once acceleratorlong = .029 // [1] default; always > 0 (i.e. 0.5-3)

once acceleratorshort= ACC0022 // 1 = default; always > 0 (i.e. 0.5-3)

ts2sensitivity = 2 // 1 = close 2 = High/Low 3 = Low/High 4 = typicalprice (not use once)

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=typicalprice

ts2sensitivityshort=typicalprice

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

Thanks nonetheless!

For me the algo has stopped within a few seconds after start, so no positions then. But maybe still can be problems with the trail? I will try your code!

I have cumulative = false, but maybe that doesn´t matter with your code above?

I tried you code on DOW 5.3S but I get:

“The trading system was stopped because the historical data loaded was insufficient to calculate at least one indicator during the evaluation of the last candlestick.”

I got the same after changing to Preloadbars = 15000

in backtest or autotrading?

autotrading

Well, if you (or anyone else) gets 5.3 to work for shorts on any market I would be very interested to test it!

I will try DJ 2m HULL-SAR v5.3S and tell you back

Here is the backtest of Dow 2m Hull SAR v5.3S.

Looks good in 200k in short only

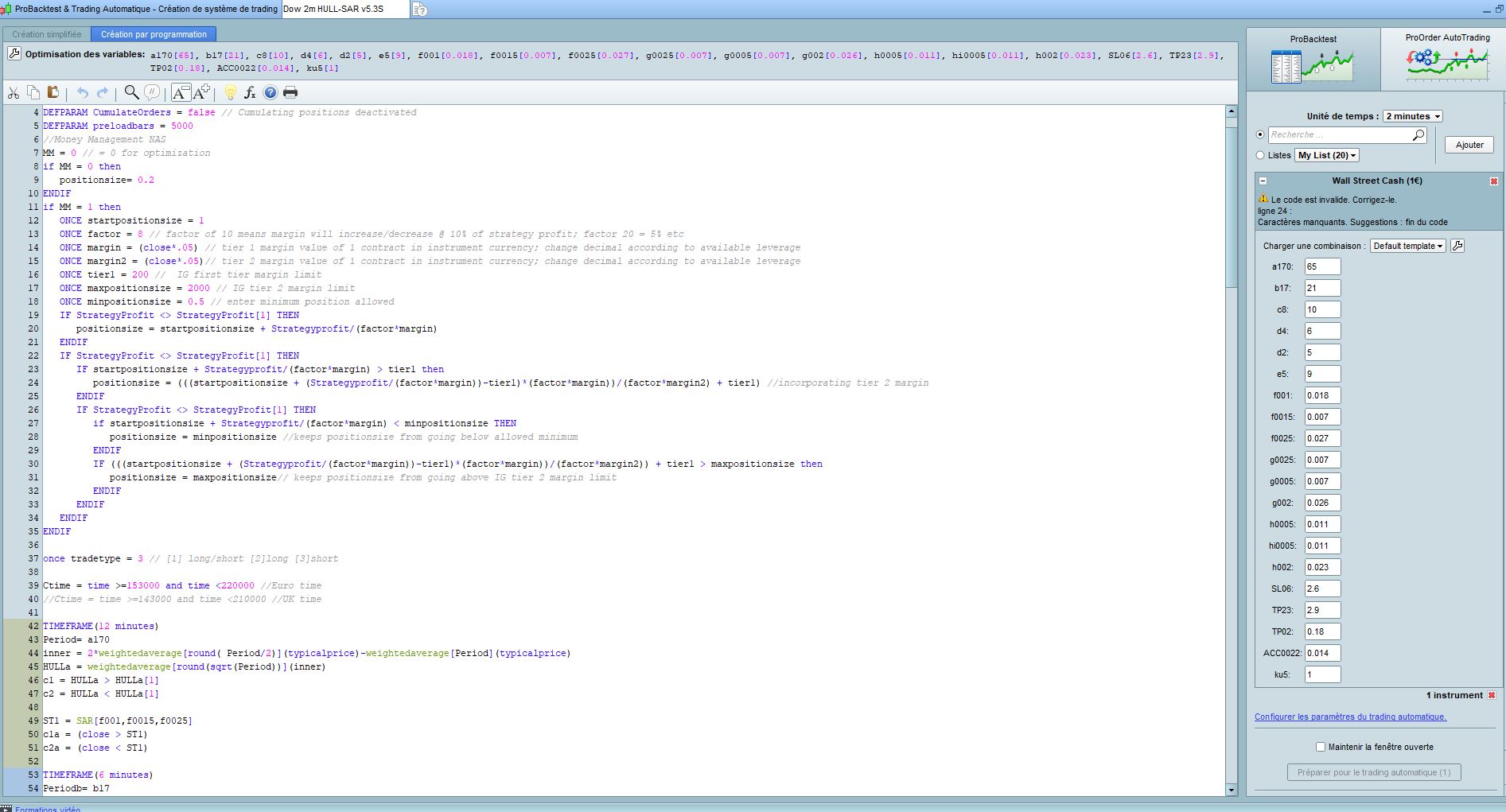

I curiously has trouble when i want launch in autotrading the Dow 2m Hull SAR v5.3S

Line 24. Message say end of code ?

I curiously has trouble when i want launch in autotrading the Dow 2m Hull SAR v5.3S

Line 24. Message say end of code ?

You can’t launch the system in autotrading because there are variables in the optimization boxes; you have first to define the values through the code, delete the optimization boxes and then you can run it.

Here is the backtest of Dow 2m Hull SAR v5.3S.

And looks good too in 1M barres

You can’t launch the system in autotrading because there are variables in the optimization boxes; you have first to define the values through the code, delete the optimization boxes and then you can run it.

I don’t think i have to do it with the last version of prorealtime V11.

The problem doesn’t come from it in my opinion

Line 24. Message say end of code ?

It may be that the code needs an extra Endif adding as the last line of the code?