The backtests seem fine to me but could be an issue with positionsize. Minimum for demo is 1, minimum live is .5

But didn’t obtain same variables as you

Probably because mine is optimized with 200k of data. But also, I don’t necessarily choose variables for max profit, sometimes I think it’s better to go for a higher %win esp if it gives higher number of trades. Sometimes it’s based on VRT results.

As for adapting to other instruments, you really just have to go through all the variables for each timeframe top to bottom. You’ll have to do this 2 or 3 times as one change effects another. I have tried versions for DAX, CAC, SP500, FTSE, ASX – cant remember what else. Some of them are still limping along in demo but the DJ and NAS are the only ones I have faith in. If anything else might work, I would start with the DAX and try to bang that into shape, using DJ v5 as a template.

@nonetheless It is the same time as in Spain that comes in “NAS 5m MoD v4S” On November 1 the time changes in the US and then it will be necessary to put if not onmarket or (time <= 153000 – USDLS and time> = 220000 – USDLS) and it keeps giving me the same failure with the MM activated and I have 1 lotti in demo. Doesn’t it give you an error?

once longStep = 0

once openStrongShort = 0

if not onmarket or (time <= 143000 - USDLS and time >= 210000 - USDLS) then

longStep = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 50

once tradeMin = 500

IF (time >= 144000 - USDLS) AND (time <= 144000 + tradeMin - USDLS) THEN

openStrongShort = close < open AND open - close > rangeOK

ENDIF

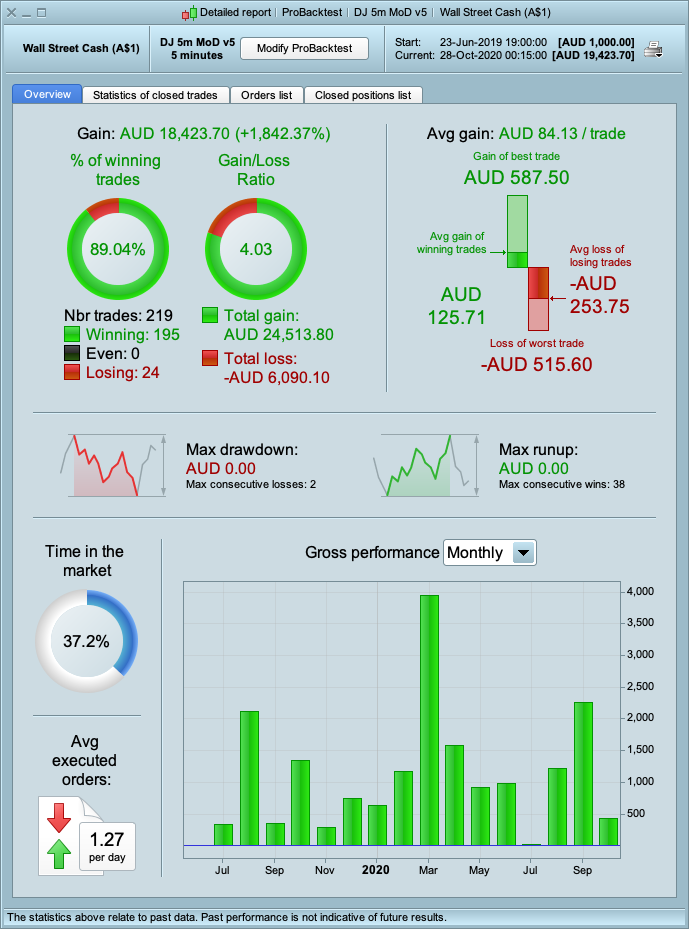

It tests fine for me, both with or without MM. If the problem only occurs with MM you could try using a higher factor, like 5 0r 10, or try it with volpiemanuele’s MM

You are right, putting a factor of 5 does not give an error. Could you put what result gives you in 200k of candles with factor 3, please? thanks

I really wouldn’t worry about it, any factor below 10 will give a result in the millions – it’s only something to dream about. But if factor 3 blows up over the past 100k then that can also happen over the coming 100k. I will change mine to 5; if the algo succeeds then positionsize will increase dramatically enough.

@volpiemanuele @nonetheless (ps. still searching for you)

Can you think of any reason why MM v5 and V.5a would be giving me these blank results. I am literally using the code that you both posted.

DJI MOD v5 works perfectly (see attached). It’s really strange.

This is DJI v5a + MM

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DOW

MM = 1 // = 0 for optimization

if mm = 1 then

prof = 0

ddpp = 212// max dd per point

ddm = 2 // multiples of max drawdowns to factor into positionsize

capital = 350 //starting bank

dpct = 5 //% margin for deposit

deposit = (open/100)*dpct //margin per point

pri = 1 // percent to reinvest as a decimal

positionsize = (capital +((strategyprofit + prof)*pri))/((ddm*ddpp)+deposit)

if positionsize < 0.25 then

positionsize = 0.2

endif

else

once positionsize = 0.2

endif

TIMEFRAME(2 hours,updateonclose)

Period= 495

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[8,4]

c3 = (close > indicator1)

c4 = (close < indicator1)

ma = average[60,3](close)

c11 = ma > ma[1]

c12 = ma < ma[1]

//Stochastic RSI | indicator

lengthRSI = 15 //RSI period

lengthStoch = 9 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 5 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

c14 = K<D

TIMEFRAME(30 minutes,updateonclose)

indicator5 = Average[2](typicalPrice)

indicator6 = Average[7](typicalPrice)

c15 = (indicator5 > indicator6)

c16 = (indicator5 < indicator6)

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[4](typicalPrice)

indicator3 = Average[8](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= 22

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(10 minutes)

indicator4 = SuperTrend[2,6]

indicator4a = SAR[0.025,0.025,0.1]

c19 = (close > indicator4) or (close > indicator4a)

c20 = (close < indicator4) or (close < indicator4a)

TIMEFRAME(5 minutes)

//Stochastic RSI | indicator

lengthRSIa = 3 //RSI period

lengthStocha = 6 //Stochastic period

smoothKa = 9 //Smooth signal of stochastic RSI

smoothDa = 3 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[15,3](typicalPrice)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= 15

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF dhigh(0)-high<300 and c1 AND C3 AND C5 and c7 and c9 and c11 and c13 and c15 and c19 and c21 and c23 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

ENDIF

// Conditions to enter short positions

IF low-dlow(0)<600 and c2 AND C4 AND C6 and c8 and c10 and c12 and c14 and c16 and c20 and c22 and c24 THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 2

SET TARGET %PROFIT 2.2

ENDIF

//================== exit in profit

if longonmarket and C6 and c8 and close>positionprice then

sell at market

endif

If shortonmarket and C5 and c7 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND c2 and c6 and close<positionprice then

sell at market

endif

If shortonmarket and c1 and c5 and close>positionprice then

exitshort at market

endif

//%trailing stop function

once trailingpercentlong = 0.21 // %

once trailingpercentshort = 0.24 // %

once accelerator = 0.05 // 1 = default; always > 0 (i.e. 0.5-3)

once accelerator2 = 0.01 // 1 = default; always > 0 (i.e. 0.5-3)

once ts2sensitivity = 2 // [0]close;[1]high/low;[2]low;high

//====================

once steppercentlong = (trailingpercentlong/10)*accelerator

once steppercentshort = (trailingpercentshort/10)*accelerator2

if onmarket then

trailingstartlong = tradeprice(1)*(trailingpercentlong/100)

trailingstartshort = tradeprice(1)*(trailingpercentshort/100)

trailingsteplong = tradeprice(1)*(steppercentlong/100)

trailingstepshort = tradeprice(1)*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl=0

endif

if ts2sensitivity=1 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=2 then

ts2sensitivitylong=low

ts2sensitivityshort=high

else

ts2sensitivitylong=close

ts2sensitivityshort=close

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-tradeprice(1)>=trailingstartlong then

newsl = tradeprice(1)+trailingsteplong

endif

if newsl>0 and ts2sensitivitylong-newsl>trailingsteplong then

newsl = newsl+trailingsteplong

endif

endif

if shortonmarket then

if newsl=0 and tradeprice(1)-ts2sensitivityshort>=trailingstartshort then

newsl = tradeprice(1)-trailingstepshort

endif

if newsl>0 and newsl-ts2sensitivityshort>trailingstepshort then

newsl = newsl-trailingstepshort

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

//************************************************************************

IF longonmarket and barindex-tradeindex>1900 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>580 and close>positionprice then

exitshort at market

endif

//=============================================

if longonmarket and abs(open-close)<1 and high[1]>high and close>positionprice and high-close>13 then

sell at market

endif

if shortonmarket and abs(open-close)<1 and low[1]>low and close-low>9 and close<positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<20 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

once shortStep = 0

once longStep = 0

once openStrongLong = 0

once openStrongShort = 0

if not onmarket or (time <= 143000 - USDLS and time >= 210000 - USDLS) then

shortStep = 0

longStep = 0

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 45

once tradeMin = 500

IF (time >= 144000 - USDLS) AND (time <= 144000 + tradeMin - USDLS) THEN

openStrongLong = close > open AND close - open > rangeOK

openStrongShort = close < open AND open - close > rangeOK

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

once BollLevel = 90

once BollSR = 50

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

//Market spike up

IF shortonmarket AND shortStep = 0 AND bollPercent > BollLevel THEN

shortStep = 1

ENDIF

//Market slowly come down

IF shortonmarket AND shortStep = 1 AND bollPercent < 100 - BollLevel THEN

shortStep = 2

ENDIF

//Market still go back to bullish and supported after strong bull open, exit

IF shortonmarket AND shortStep = 2 AND bollPercent > BollSR AND openStrongLong THEN

exitshort at market

ENDIF

//Market shoot down

IF longonmarket AND longStep = 0 AND bollPercent < 100 - BollLevel THEN

longStep = 1

ENDIF

//Market slowly go back up

IF longonmarket AND longStep = 1 AND bollPercent > BollLevel THEN

longStep = 2

ENDIF

//Market still go back to bearish and resisted after strong bear open, exit

IF longonmarket AND longStep = 2 AND bollPercent < 100 - BollSR AND openStrongShort THEN

sell at market

ENDIF

once trendPeriod = 70

once trendPeriodResume = 30

once trendGap = 3

once trendResumeGap = 6

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//Started real wrong direction

once strongTrend = 70

once strongPeriod = 6

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod then

sell at market

ENDIF

This is DJI MOD v5a code that I am using:

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DOW

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=15

ENDIF

if MM = 1 then

ONCE startpositionsize = .4

ONCE factor = 5 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

TIMEFRAME(2 hours,updateonclose)

Period= 495

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULLa = weightedaverage[round(sqrt(Period))](inner)

c1 = HULLa > HULLa[1]

c2 = HULLa < HULLa[1]

indicator1 = SuperTrend[8,4]

c3 = (close > indicator1)

c4 = (close < indicator1)

ma = average[60,3](close)

c11 = ma > ma[1]

c12 = ma < ma[1]

//Stochastic RSI | indicator

lengthRSI = 15 //RSI period

lengthStoch = 9 //Stochastic period

smoothK = 10 //Smooth signal of stochastic RSI

smoothD = 5 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

c14 = K<D

TIMEFRAME(30 minutes,updateonclose)

indicator5 = Average[2](typicalPrice)

indicator6 = Average[7](typicalPrice)

c15 = (indicator5 > indicator6)

c16 = (indicator5 < indicator6)

TIMEFRAME(15 minutes,updateonclose)

indicator2 = Average[4](typicalPrice)

indicator3 = Average[8](typicalPrice)

c7 = (indicator2 > indicator3)

c8 = (indicator2 < indicator3)

Periodc= 22

innerc = 2*weightedaverage[round( Periodc/2)](typicalprice)-weightedaverage[Periodc](typicalprice)

HULLc = weightedaverage[round(sqrt(Periodc))](innerc)

c9 = HULLc > HULLc[1]

c10 = HULLc < HULLc[1]

TIMEFRAME(10 minutes)

indicator4 = SuperTrend[2,6]

indicator4a = SAR[0.025,0.025,0.1]

c19 = (close > indicator4) or (close > indicator4a)

c20 = (close < indicator4) or (close < indicator4a)

TIMEFRAME(5 minutes)

//Stochastic RSI | indicator

lengthRSIa = 3 //RSI period

lengthStocha = 6 //Stochastic period

smoothKa = 9 //Smooth signal of stochastic RSI

smoothDa = 3 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

Ka = average[smoothKa](stochrsia)*100

Da = average[smoothDa](Ka)

c23 = Ka>Da

c24 = Ka<Da

ma3 = average[15,3](typicalPrice)

c21 = ma3 > ma3[1]

c22 = ma3 < ma3[1]

Periodb= 15

innerb = 2*weightedaverage[round( Periodb/2)](typicalprice)-weightedaverage[Periodb](typicalprice)

HULLb = weightedaverage[round(sqrt(Periodb))](innerb)

c5 = HULLb > HULLb[1]and HULLb[1]<HULLb[2]

c6 = HULLb < HULLb[1]and HULLb[1]>HULLb[2]

// Conditions to enter long positions

IF dhigh(0)-high<300 and c1 AND C3 AND C5 and c7 and c9 and c11 and c13 and c15 and c19 and c21 and c23 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP %LOSS 1.5

SET TARGET %PROFIT 2.5

ENDIF

// Conditions to enter short positions

IF low-dlow(0)<600 and c2 AND C4 AND C6 and c8 and c10 and c12 and c14 and c16 and c20 and c22 and c24 THEN

SELLSHORT positionsize CONTRACT AT MARKET

SET STOP %LOSS 2

SET TARGET %PROFIT 2.2

ENDIF

//================== exit in profit

if longonmarket and C6 and c8 and close>positionprice then

sell at market

endif

If shortonmarket and C5 and c7 and close<positionprice then

exitshort at market

endif

//==============exit at loss

if longonmarket AND c2 and c6 and close<positionprice then

sell at market

endif

If shortonmarket and c1 and c5 and close>positionprice then

exitshort at market

endif

//%trailing stop function

trailingpercentlong = 0.21 // %

trailingpercentshort = 0.24 // %

once acceleratorlong = 0.05 // [1] default; always > 0 (i.e. 0.5-3)

once acceleratorshort= 0.01 // 1 = default; always > 0 (i.e. 0.5-3)

ts2sensitivity = 3 // [1] default [2] hl [3] lh (not use once)

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

//************************************************************************

IF longonmarket and barindex-tradeindex>1900 and close<positionprice then

sell at market

endif

IF shortonmarket and barindex-tradeindex>580 and close>positionprice then

exitshort at market

endif

//=============================================

if longonmarket and abs(open-close)<1 and high[1]>high and close>positionprice and high-close>13 then

sell at market

endif

if shortonmarket and abs(open-close)<1 and low[1]>low and close-low>9 and close<positionprice then

exitshort at market

endif

//===================================

myrsiM5=rsi[14](close)

//

if myrsiM5<20 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsiM5>70 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

once shortStep = 0

once longStep = 0

once openStrongLong = 0

once openStrongShort = 0

if not onmarket or (time <= 143000 - USDLS and time >= 210000 - USDLS) then

shortStep = 0

longStep = 0

openStrongLong = 0

openStrongShort = 0

endif

//detect strong direction for market open

once rangeOK = 45

once tradeMin = 500

IF (time >= 144000 - USDLS) AND (time <= 144000 + tradeMin - USDLS) THEN

openStrongLong = close > open AND close - open > rangeOK

openStrongShort = close < open AND open - close > rangeOK

ENDIF

once bollperiod = 20

once bollMAType = 1

once s = 2

once BollLevel = 90

once BollSR = 50

bollMA = average[bollperiod, bollMAType](close)

STDDEV = STD[bollperiod]

bollUP = bollMA + s * STDDEV

bollDOWN = bollMA - s * STDDEV

IF bollUP = bollDOWN THEN

bollPercent = 50

ELSE

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

ENDIF

//Market spike up

IF shortonmarket AND shortStep = 0 AND bollPercent > BollLevel THEN

shortStep = 1

ENDIF

//Market slowly come down

IF shortonmarket AND shortStep = 1 AND bollPercent < 100 - BollLevel THEN

shortStep = 2

ENDIF

//Market still go back to bullish and supported after strong bull open, exit

IF shortonmarket AND shortStep = 2 AND bollPercent > BollSR AND openStrongLong THEN

exitshort at market

ENDIF

//Market shoot down

IF longonmarket AND longStep = 0 AND bollPercent < 100 - BollLevel THEN

longStep = 1

ENDIF

//Market slowly go back up

IF longonmarket AND longStep = 1 AND bollPercent > BollLevel THEN

longStep = 2

ENDIF

//Market still go back to bearish and resisted after strong bear open, exit

IF longonmarket AND longStep = 2 AND bollPercent < 100 - BollSR AND openStrongShort THEN

sell at market

ENDIF

once trendPeriod = 70

once trendPeriodResume = 30

once trendGap = 3

once trendResumeGap = 6

if not onmarket then

fullySupported = 0

fullyResisteded = 0

endif

//Market supported in the wrong direction

IF shortonmarket AND fullySupported = 0 AND summation[trendPeriod](bollPercent > 50) >= trendPeriod - trendGap THEN

fullySupported = 1

ENDIF

//Market pull back but continue to be supported

IF shortonmarket AND fullySupported = 1 AND bollPercent[trendPeriodResume + 1] < 0 AND summation[trendPeriodResume](bollPercent > 50) >= trendPeriodResume - trendResumeGap THEN

exitshort at market

ENDIF

//Market resisted in wrong direction

IF longonmarket AND fullyResisteded = 0 AND summation[trendPeriod](bollPercent < 50) >= trendPeriod - trendGap THEN

fullyResisteded = 1

ENDIF

//Market pull back but continue to be resisted

IF longonmarket AND fullyResisteded = 1 AND bollPercent[trendPeriodResume + 1] > 100 AND summation[trendPeriodResume](bollPercent < 50) >= trendPeriodResume - trendResumeGap THEN

sell at market

ENDIF

//Started real wrong direction

once strongTrend = 70

once strongPeriod = 6

IF shortonmarket and openStrongLong and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent > strongTrend) = strongPeriod then

exitshort at market

ENDIF

IF longonmarket and openStrongShort and barindex - tradeindex < 12 and summation[strongPeriod](bollPercent < 100 - strongTrend) = strongPeriod then

sell at market

ENDIF

@nonetheless – I just realized that in v5a you have MM switched on for some reason?

That’s what seems to be breaking it for me. Is there any variables in MM that would be tied to the instrument or currency?

As soon as I switch MM off it works again, which would also explain why the MM version is not working.

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

DEFPARAM preloadbars = 5000

//Money Management DOW

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .4

ONCE factor = 5 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

MM = 0 // = 0 for optimization

if mm = 1 then

prof = 0

ddpp = 212// max dd per point

ddm = 2 // multiples of max drawdowns to factor into positionsize

capital = 350 //starting bank

dpct = 5 //% margin for deposit

deposit = (open/100)*dpct //margin per point

pri = 1 // percent to reinvest as a decimal

positionsize = (capital +((strategyprofit + prof)*pri))/((ddm*ddpp)+deposit)

if positionsize < 0.25 then

positionsize = 0.2

endif

endif

if mm = 0 then

positionsize = 0.2

endif

@StingeRe My code run ok in my PRT (demo or live version). Try to change MM inserting this code. If MM = 0 you have fixed position and if MM = 1 you have the MM. I see that your currency is AUD. You can insert the correct value in AUD in this variable “ddpp” and “capital”. My currency is EURO. Thanks

@SitngeRe…first change the value in AUD….for me the problem is this….the code is correct….

I just realized that in v5a you have MM switched on for some reason?

MM is entirely optional, for me it tests correctly both with or without. If yours wont run with MM=1 you can try altering the positionsize, the factor or both.

@nonetheless, I have some issues with the TS, it just adjusts to BE but does not follow the price forward to cover the open positions. Do you have any idea why? Thanks in advance!

Yeah, I just noticed that as well, I’ll look into it.

Hopefully this fixes the TS problem. NAS to follow…

Thanks @nonetheless, I noticed this last night as well when I was forward testing 4.xx vs 5.

Interesting they both ended up taking similar profits in the end though.

Thanks kindly for the fix.