Yes I guess if you think about it logically one candle on a daily time frame gives us a whole 24 hour survey of market sentiment whereas a 1 hour candle is a very small market sample for the same survey. It will tell us 1/24th of what the daily candle can tell us. With a better survey we are more likely to be right – we just have to have enough patience to wait for the survey to be finished and the budget to pay to hold positions overnight while we wait to be proved right.

Hi guys, i’ve put a pyramid into the ts

//EURUSD(-) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK - 200.000 bars

// SPREAD 0.6 PIP

// ALE

DEFPARAM CumulateOrders = TRUE

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

CP=108

if close[cp] >= highest[2*cp+1](close) then

LH = 1

else

LH=0

endif

if close[cp] <= lowest[2*cp+1](close) then

LL= -1

else

LL=0

endif

if LH=1 then

HIL = close[cp]

endif

if LL = -1 then

LOL=close[cp]

endif

// RETURN, HIL COLOURED(0,200,0) AS "BREAKOUT LEVEL LONG",HIL COLOURED(200,0,0) AS "BREAKOUT LEVEL SHORT"

//////////////////////////

ONCE POSITIONSIZE = 1

ONCE ExitIndex = -1

//LONG and SHORT CONDITIONS

O=COUNTOFLONGSHARES<2

P=COUNTOFSHORTSHARES<2

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

A1= (CLOSE-CLOSE[1])>30*POINTSIZE

B1= (CLOSE-CLOSE[1])<-30*POINTSIZE

IF C1 and not shortonmarket AND NOT LONGONMARKET THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

IF C1 and not shortonmarket AND A1 AND O THEN

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and not longonmarket AND NOT SHORTONMARKET THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

IF D1 and not longonmarket AND B1 AND P THEN

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL =9

TGS=10

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ExitIndex = BarIndex

ENDIF

// DONCHIAN STOP

DC=20

e= Highest[DC](high)

f=Lowest[DC](low)

if longonmarket then

laststop = f[1]

endif

if shortonmarket then

laststop = e[1]

endif

if onmarket then

sell at laststop stop

exitshort at laststop stop

ExitIndex = BarIndex

endif

if (time >=100000 and time < 170000) THEN

TP=30

ELSE

TP=20

ENDIF

IF COUNTOFLONGSHARES>2 THEN

TP=5

ENDIF

set target pprofit TP

///PIRAMIDE////

IF Barindex = ExitIndex + 1 THEN

ExitIndex = 0

IF PositionPerf(1) < 0 THEN

POSITIONSIZE = POSITIONSIZE + 1

REM Double POSITIONSIZE if the last position was a losing position.

ELSIF PositionPerf(1) > 0 THEN

POSITIONSIZE = POSITIONSIZE + 0

REM Reset position size to 1 if the last trade was a winning trade.

ENDIF

ENDIF

ALE ps hai telegram?

ALE

ALEModerator

Master

Hello Altares,

in theory it is very beautiful, but the data of the probacktest are always different from the reality, above all on smaller timeframe of the daily, therefore I recommend you do not to apply it to real market

ALE u running this live still? It looks almost to good to be true 🙂 amazing backtest-results

I’ve played with different forex pairs and it seems like u can definitly optimize this for different pairs..

If ur running it live, on what pairs so far?

Live results close to backtest so far?

how long have u been running it live?

ALEModerator

Master

Hello Jebus

I’m testing it on the real one of the first versions, to understand better the differences with the probacktest, along time we have observed quite a lot differences, probably caused by closings not happened for a simple tick, in real as in the probacktest.

The weakness of this strategy also consists in too little points of gain for every trade.

The concept it’s good, but it’s not so simple to automatize it.

Thanks for you attention!

hello,

after 5 years, we have a size lot of 100.

it’s a lot.

the strategy need a reset to restart sometimes to 1? no?

thanks

don’t take attention to my last comment 🙂

ALEModerator

Master

Hi Vonasi, has reread your questions and I has acknowledged you not to have answered. In that days had not understood your questions, Excuse me!

Hi Vonasi, has reread your questions and I has acknowledged you not to have answered. In that days had not understood your questions, Excuse me!

You are excused! Although I do not fully understand what you have written in your post. My last post on this thread was over three months ago and my memory does not go back that far with much clarity!

CN

CNParticipant

Senior

Has anyone tried the 30M v2 on 1h eur/usd and seen what happens?

Crazy results, cant understand why… Anyone care to explain?

ALEModerator

Master

Hello Cn

could you explain better?

tks

Ale

CNParticipant

Senior

Of course,

I tried out the 30min v2 strategy, that u have on the first post, on the 1H TF, eur/usd mini.

The results are above from that backtest, not alot of trades, but It looks too good to be true. 95% win rate.

Anyone can try a 200k backtest and/or a WF?

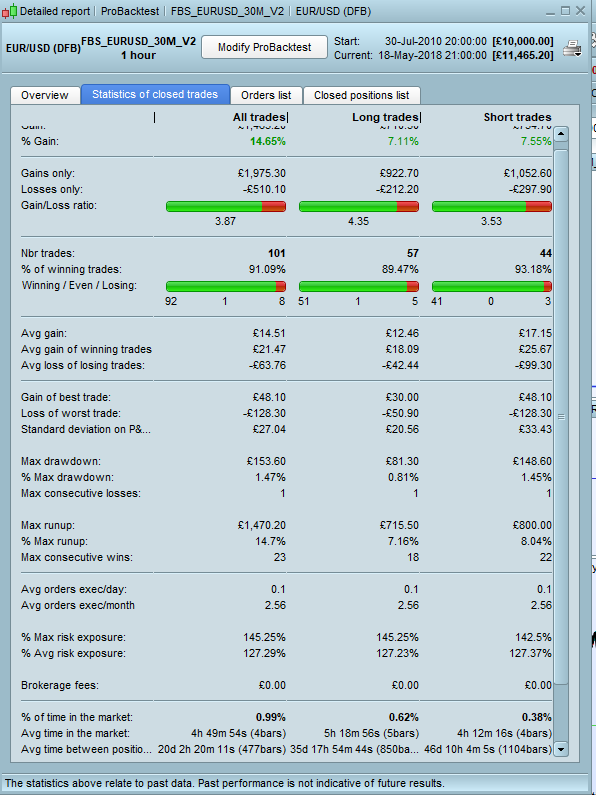

200K backtest with 30min v2 strategy on 1 hour chart.

Good results but very low returns per trade and it also appears that in recent times performance has been dropping off.

[attachment file=70837]

[attachment file=70838]

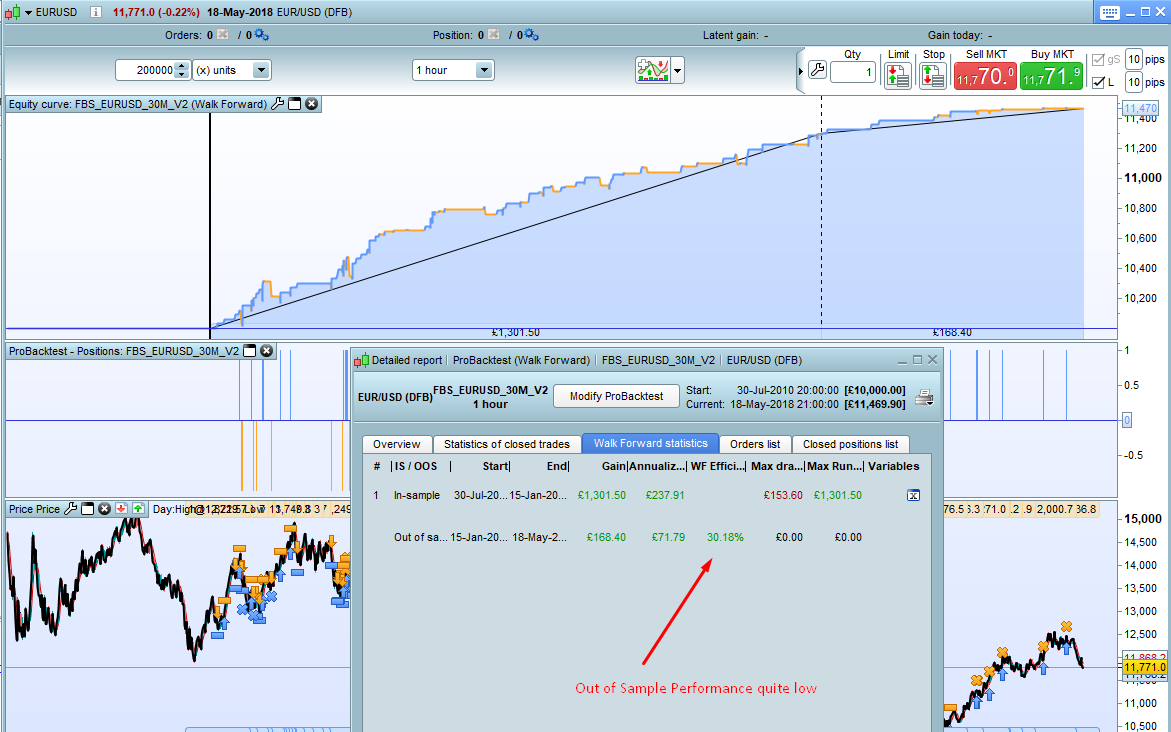

WF with 5 and 1 repetitions.

[attachment file=70851]

[attachment file=70852]

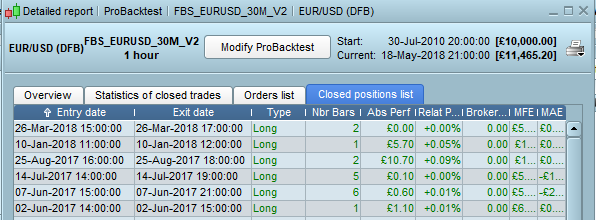

ALE released the code to us on 16-4- 2017 so (although he never intended it to be run on the 1 hour chart so it was not optimized for this at all) any trades since this date are true OOS trades. Not many to go on and not very exciting even if there is a small profit.

[attachment file=70858]