but its stopping sometimes and I dont know why

What stop message is IG showing you?

Usually the Renko’s stop due to Stop Loss being less than minimum stop allowed by IG?

Well I havent checked I though prorealtime did that.

Paul

PaulParticipant

Master

I got that problem too. Posted in an existing (old) topic this problem. No info at the rejected/canceled tab. Annoying, since it makes the results unstable.

Im running 1s on both demo and live they are doing so many different trades. Sometimes live doesnt take the trade demo does and vice versa. Thats wierd.

PaulParticipant

Master

This is what i’am testing. It provided some nice profits before, now it doesn’t look good in a backtest.

Goal is more to have consistent opening-trades from the backtest & live.

I removed a few lines which defined renkomax/min and didn’t expect it would work but it did.

//-------------------------------------------------------------------------

// Hoofd code : Renko dji 5s A3.1

//-------------------------------------------------------------------------

defparam cumulateorders = false

defparam preloadbars = 1000

defparam flatbefore = 080000

defparam flatafter = 173000

once tradetype = 1 // [1]long&short;[2]long;[3]short

boxsizeL=40

boxsizeS=30

// strategy

ctime= time>=080000 and time<150000

if close > renkomax + boxsizeL and not (close < renkomin - boxsizeS) then

renkomax = renkomax + boxsizeL

renkomin = renkomin + boxsizeL

endif

if close < renkomin - boxsizeS and not (close > renkomax + boxsizeL) then

renkomax = renkomax - boxsizeS

renkomin = renkomin - boxsizeS

endif

// conditions

condbuy=high > (renkomax + boxsizeL)

condbuy=condbuy and open<>close and low<>close and open<>high

condsell=low < (renkomin - boxsizeS)

condsell=condsell and open<>close and high<>close and open<>low

// entry

if ctime then

If (tradetype=1 or tradetype=2) then

if condbuy and not longonmarket then

buy 1 contract at market

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and not shortonmarket then

sellshort 1 contract at market

endif

endif

endif

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once steps = 0.1 // set to 0 to ignore steps

once minatrdist= 1.0

once atrtrailingperiod = 14 // atr parameter

once minstop = 10 // minimum trailing stop distance

once sensitivityts = 0 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 3 // trailing stop atr distance

trailingstopshort = 3 // trailing stop atr distance

else

if longonmarket then

if newsl>0 then

if trailingstoplong>minatrdist then

if newsl>newsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-steps

endif

else

trailingstoplong=minatrdist

endif

endif

endif

if shortonmarket then

if newsl>0 then

if trailingstopshort>minatrdist then

if newsl<newsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-steps

endif

else

trailingstopshort=minatrdist

endif

endif

endif

endif

//

atrtrail=averagetruerange[atrtrailingperiod]((close/10)*pipsize)/1000

tgl=round(atrtrail*trailingstoplong)

tgs=round(atrtrail*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice=0

minprice=close

newsl=0

endif

//

if sensitivityts then

sensitivitytslong=high

sensitivitytsshort=low

else

sensitivitytslong=close

sensitivitytsshort=close

endif

//

if longonmarket then

maxprice=max(maxprice,sensitivitytslong)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

newsl=maxprice-tgl*pointsize

else

newsl=maxprice-minstop*pointsize

endif

endif

endif

//

if shortonmarket then

minprice=min(minprice,sensitivitytsshort)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

newsl=minprice+tgs*pointsize

else

newsl=minprice+minstop*pointsize

endif

endif

endif

//

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market //when stop is rejected

endif

endif

endif

//

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market //when stop is rejected

endif

endif

endif

endif

set stop %loss .4

Goal is more to have consistent opening-trades from the backtest & live.

Do you start the System on both Backyest and Live at same time?

If No … might differences between Backtest and Live be due to brick size being counted / measured from different starting points??

PaulParticipant

Master

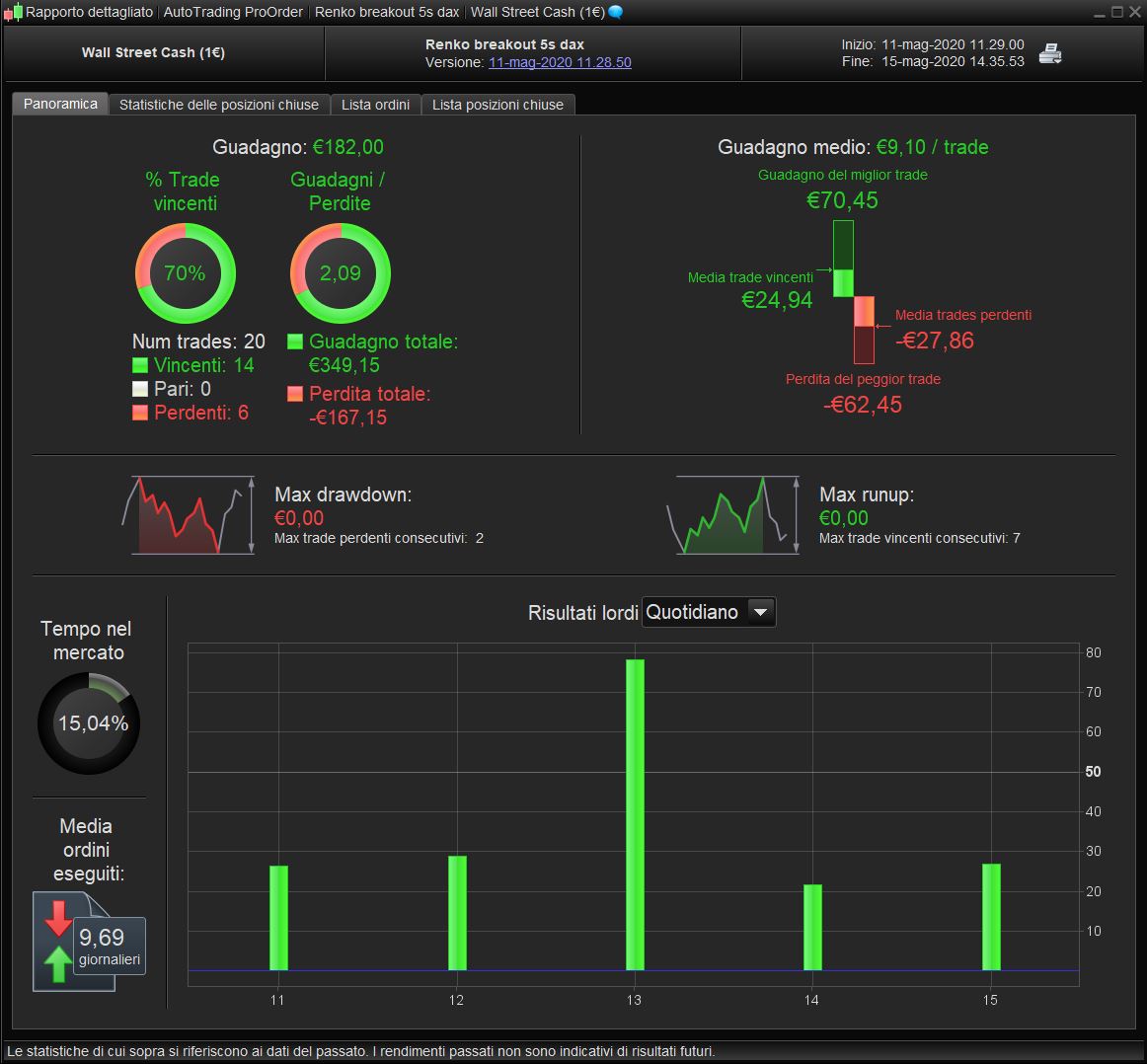

yeah understand what y’re saying and you are right. This version is a bit different and give me somewhat hope 🙂 Here’s today so far.

What I see now in the screenshot, left it’s defined as exit at 9.06.55 and on the right as entry. Why is that? There was no market position before that.

@Paul why did u decided to operate between that time frame? Higher volatility or what?

Are there someone who is running anyone of thoose renko strategys and getting good results?

PaulParticipant

Master

@Francesco biggest reason is different market behaviour as to when the market opens. When it opens its seems harder to get good results, maybe indeed one cause is volatility.

@Paul You still getting good results out there in the jungle? 😀

PaulParticipant

Master

Hi

It’s tough. Yesterday I did, today not so much!

With removing some parts defining “once” the renkoboxes, It seems to have stable results for the entry live compared to the backtest (when the system wasn’t stopped). That was the goal.

It’s running from 26 april and still +/-500 profit. While it doesn’t show in the backtest, for the moment it didn’t break down completely, which is often the case on fast timeframes.

But it’s not good enough. New idea’s are welcome!

thanked this post

PaulParticipant

Master

profits are gone. A really bad day!

Still every entry is the same as the entry in the backtest. So maybe there’s a basis for ML.

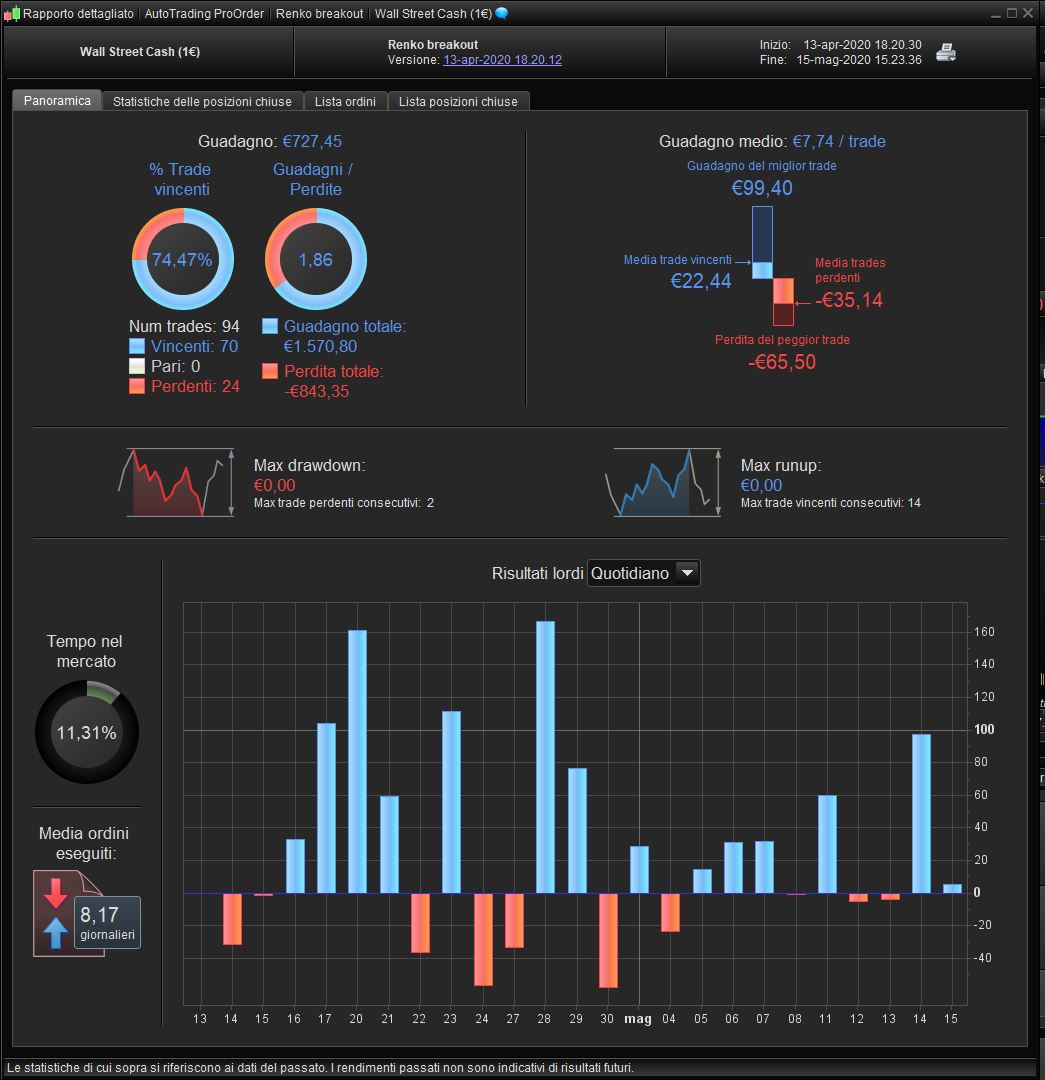

I wanna share my own version of an automated renko system: it’s a breakout system based on a Nicolas’ code and using ATR trailing stop seen here.

These are the result in live demo and in the first week of real account, on Dow 5s…

PaulParticipant

Master

There doesn’t seem much interest in a fast timeframe anymore.

One part in your code I didn’t like and that’s using the average renkobox. Somehow it slows down backtesting a lot or is doesn’t load. I removed that part.

I inserted a breakeven do lower the maximum losses and the more recent atr trailingstop. Maybe somehow pivots can be used here. Thanks for posting your version!