Hello community,

I open this topic to discuss and improve together Matriciel’s EURUSD HighLow strategy : https://www.prorealcode.com/prorealtime-trading-strategies/eurusd-15-minutes-timeframe-dhigh-dlow-strategy/

I think it has a great potential, and apparently we are struggling to communicate updates to each other through the comments.

This is the code :

DEFPARAM CumulateOrders = True

DEFPARAM PRELOADBARS = 10000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Horaire = time >= 000000 and time <= 200000

CloturePartielle = 1// 1 = ON, 0 = OFF

PositionsizeA = 1

PositionsizeV = 1

MAXSHARES = abs(COUNTOFPOSITION) <= 19

IF CloturePartielle THEN

PositionsizeA = 4

PositionsizeV = 3

ENDIF

MM = Average[56,3](totalprice)

Newhighest = max(DHigh(0),DHigh(1))

Newlowest = min(DLow(0),DLow(1))

Milieu = (Newhighest+Newlowest)/2

Surachat = average[10,4]((Newhighest+Milieu)/2)

Survente = average[10,4]((Newlowest+Milieu)/2)

CA = (MM > Surachat) and (close crosses over Milieu)

CV = (MM < Survente) and (close crosses under Milieu)

// Long Entries

IF Horaire AND CA AND MAXSHARES AND not daysForbiddenEntry AND NOT SHORTONMARKET THEN

BUY PositionsizeA CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF LONGONMARKET AND COUNTOFLONGSHARES <= 16 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 40*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 4 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 20*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 6 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 18*pointsize LIMIT

ENDIF

ENDIF

IF LONGONMARKET AND summation[35](close < close[6]) = 35 THEN

SELL AT MARKET

ENDIF

// Short Entries

IF Horaire AND CV AND MAXSHARES AND not daysForbiddenEntry AND NOT LONGONMARKET THEN

SELLSHORT PositionsizeV CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF SHORTONMARKET AND COUNTOFSHORTSHARES <= 20 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 78*pointsize LIMIT

ENDIF

IF SHORTONMARKET AND COUNTOFLONGSHARES <= 1 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 40*pointsize LIMIT

ENDIF

ENDIF

IF SHORTONMARKET AND summation[32](close > close[6]) = 32 THEN

EXITSHORT AT MARKET

ENDIF

//MFE

//trailing stop

trailingstop = 33

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//SET TARGET pPROFIT 46

SET STOP pLOSS 200

Don’t you just hate it when Nicolas does a refresh of the website between starting to write a message and posting it and then we end up not logged in and so the post is lost / not posted!?

Fortunately is was not a long post so I’ll do it again later.

Apologies for the moan @Nicolas , I know you have to do maintenance 🙂

I think I may copy posts to clipboard in future before posting?

This ‘moaning post’ is longer than the post I lost so I’d have been better keeping my mouth shut and re doing my original post! 🙂

This ‘moaning post’ is longer than the post I lost so I’d have been better keeping my mouth shut and re doing my original post! 🙂

We want the original post now ! 😛

I’ve had 2 trades only since 17 Oct 19 on Forward Test of this System … both in profit!

I didn’t Accumulate Orders (position size = 1) so only £58 profit, but 2 out of 2 in profit is a good start.

For whatever the reason, I am testing it on 10 min TF (eurusd)

Will Lines 41, 45, 61 and 64 (ish) work in real as they are partial exits?

I used, for example …

SELL AT TRADEPRICE + 20*pointsize LIMIT

Don’t you just hate it when Nicolas does a refresh of the website between starting to write a message and posting it and then we end up not logged in and so the post is lost / not posted!?

That wasn’t me, it happens sometimes automatically for security of your account, but not often!

Code works in backtest but how to overcome the partial close issue ?

how to overcome the partial close issue ?

Partial closure is only possible in back testing – not in live demo or live real trading unfortunately. There is no way round this except to ask IG when they plan to let us all partially close positions.

how to overcome the partial close issue ?

You mean you want to do partial closures or you want to eliminate partial closures?

If you want to eliminate then use …

SELL AT TRADEPRICE + 20*pointsize LIMIT

ExitShort AT TRADEPRICE + 20*pointsize LIMIT

@investment_account (GraHal)

Did you get my email yesterday?

Tku. I will try strategy without partial close.

J.

J.Participant

Average

I modified the code a little bit to add a compounding effect. In back testing I noticed it started of with a loss the first 6 months, if you calculate position size based on your current capital, it will make for better risk management in my opinion. I took $10k as starting capital for this example.

Below my code.

DEFPARAM CumulateOrders = True

DEFPARAM PRELOADBARS = 10000

//calculate position size based on capital

AMOUNT = (10000 + STRATEGYPROFIT) * 0.0001

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Horaire = time >= 000000 and time <= 200000

CloturePartielle = 1// 1 = ON, 0 = OFF

PositionsizeA = 1 * AMOUNT

PositionsizeV = 1 * AMOUNT

MAXSHARES = abs(COUNTOFPOSITION) <= 19 * AMOUNT

IF CloturePartielle THEN

PositionsizeA = 4 * AMOUNT

PositionsizeV = 3 * AMOUNT

ENDIF

MM = Average[56,3](totalprice)

Newhighest = max(DHigh(0),DHigh(1))

Newlowest = min(DLow(0),DLow(1))

Milieu = (Newhighest+Newlowest)/2

Surachat = average[10,4]((Newhighest+Milieu)/2)

Survente = average[10,4]((Newlowest+Milieu)/2)

CA = (MM > Surachat) and (close crosses over Milieu)

CV = (MM < Survente) and (close crosses under Milieu)

// Long Entries

IF Horaire AND CA AND MAXSHARES AND not daysForbiddenEntry AND NOT SHORTONMARKET THEN

BUY PositionsizeA CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF LONGONMARKET AND COUNTOFLONGSHARES <= 16 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 40*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 4 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 20*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 6 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 18*pointsize LIMIT

ENDIF

ENDIF

IF LONGONMARKET AND summation[35](close < close[6]) = 35 THEN

SELL AT MARKET

ENDIF

// Short Entries

IF Horaire AND CV AND MAXSHARES AND not daysForbiddenEntry AND NOT LONGONMARKET THEN

SELLSHORT PositionsizeV CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF SHORTONMARKET AND COUNTOFSHORTSHARES <= 20 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 78*pointsize LIMIT

ENDIF

IF SHORTONMARKET AND COUNTOFLONGSHARES <= 1 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 40*pointsize LIMIT

ENDIF

ENDIF

IF SHORTONMARKET AND summation[32](close > close[6]) = 32 THEN

EXITSHORT AT MARKET

ENDIF

//MFE

//trailing stop

trailingstop = 33

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//SET TARGET pPROFIT 46

SET STOP pLOSS 200

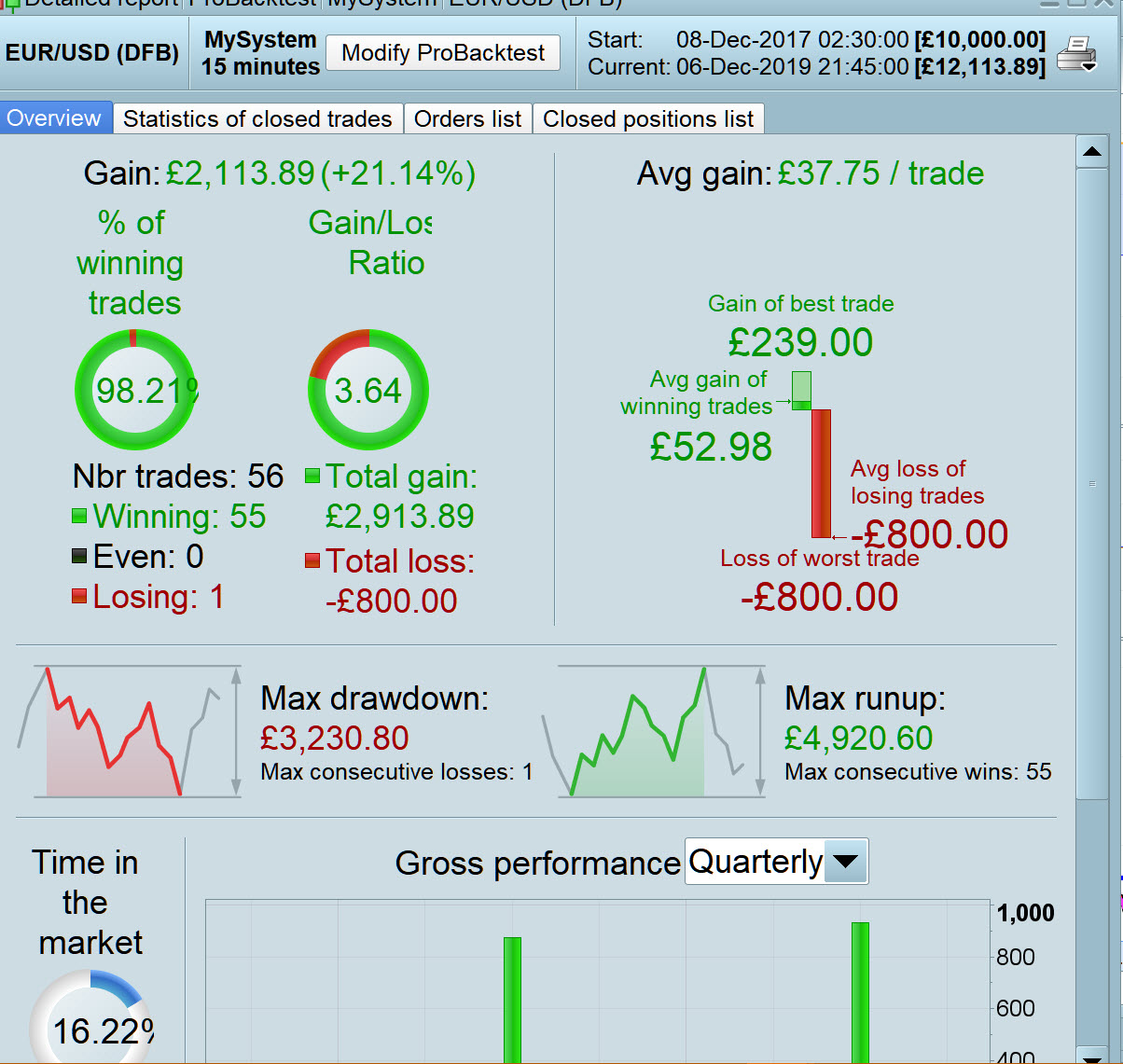

Do you get the results attached @J. Slowly?

I deducted 1 hour from your times (UTC +1) to get UTC +00 (UK time) and I used spread = 2.

Thanks for sharing. Works great in test indeed, ever greater with EURCAD isn’t it ? Does somenone has the code without partial closure wich indeed prevent form pushing it towards ProOrder ? Don’t have yet the time to clean it. Without partial closure, are the results still good ? Thanks !

Results are good but drawdown is huge