GOOD MORNING, I’M A NEOFITE AND I’M STARTING TO STUDY THIS TYPE OF TRADING.

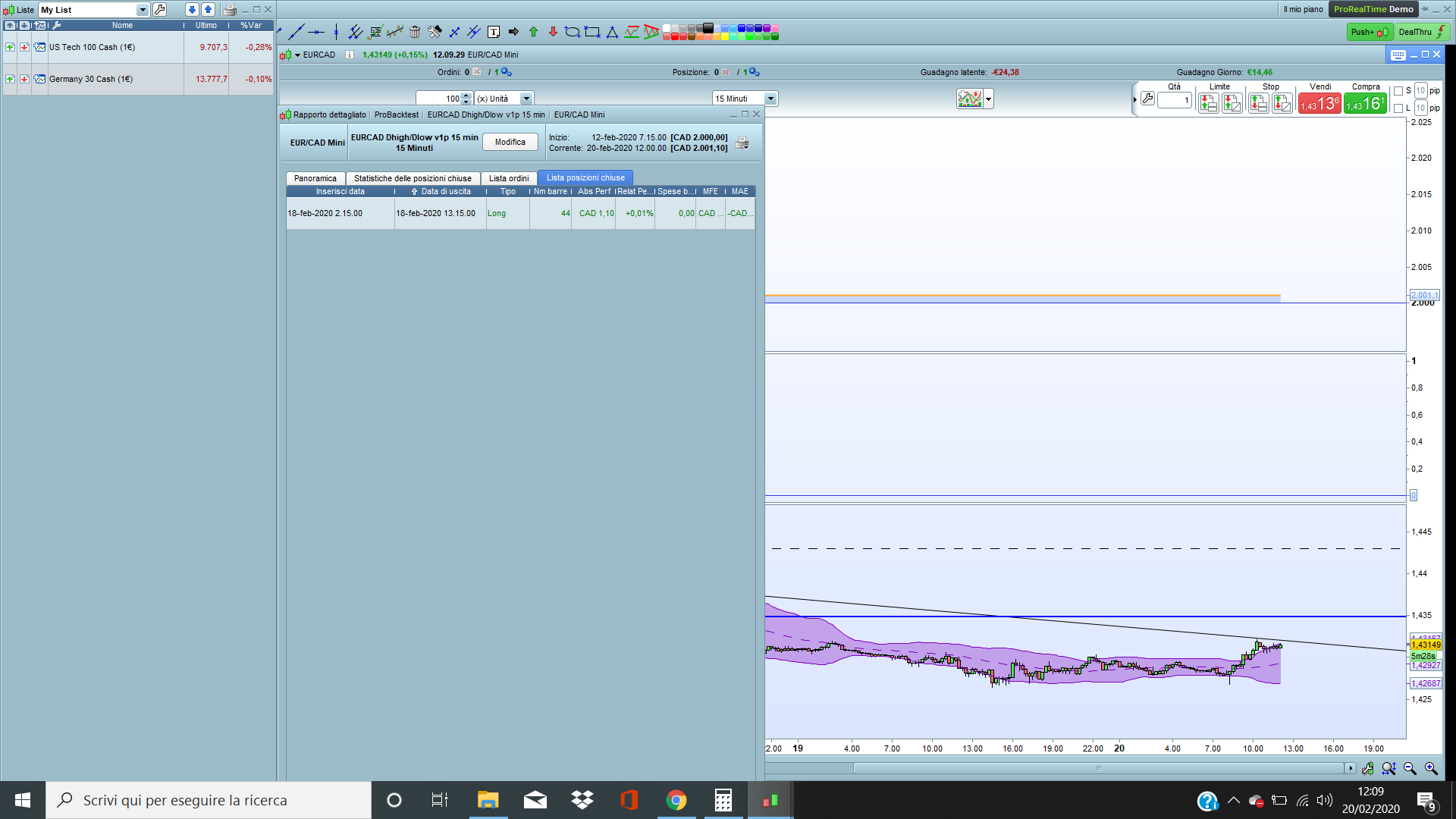

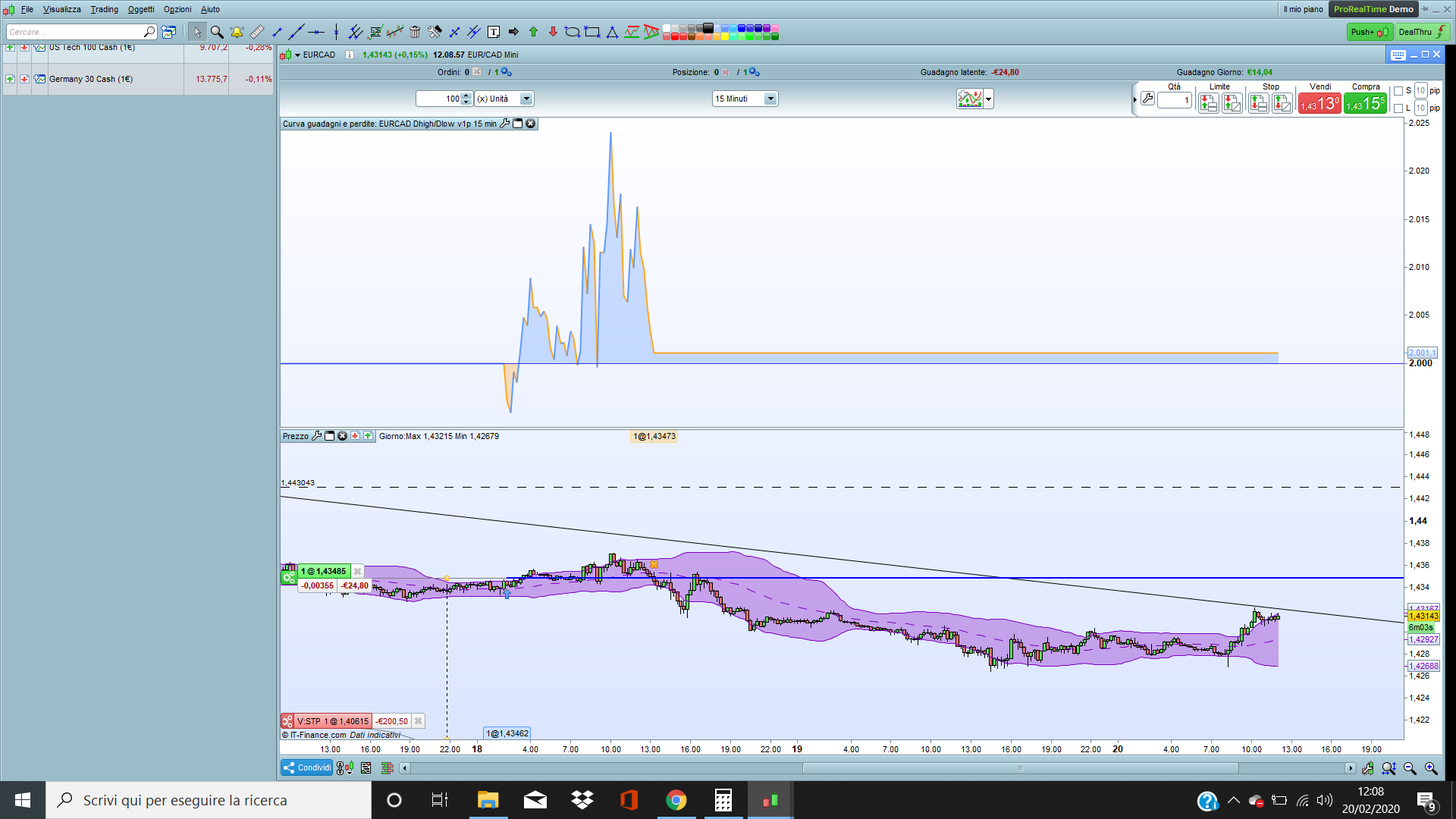

I TESTED THE STRATEGY IN THE ANNEX BUT IN REAL THE SYSTEM DID NOT CLOSE THE POSITION. WHAT COULD IT BE DUE TO? THANK YOU

valflare – Please don’t type in all capital letters. The use of capitals is considered as shouting in forums. In these forums you will find that code words will sometimes be typed in capital letters to highlight that they are different from normal text but otherwise we try to keep the shouting to a minimum! 🙂

Hello gentlemen,

I also made some modifications to this highly interesting EUR/CAD 15m strategy. Changes:

- Changed spread to 2.5 since that is what IG uses on EUR/CAD.

- Added a re-invest code found on this forum. It’s highly flexible, choose your own risk by adjusting the last line (I set 25 to default. 100 = 1 contract). Thank you creator of that code!

- Lower stop loss (didn’t have effect on backtesting, just the illusion of lower risk and keep IG happy when go live).

- Removed graphonprice to allow it to run on automatic trading in demo.

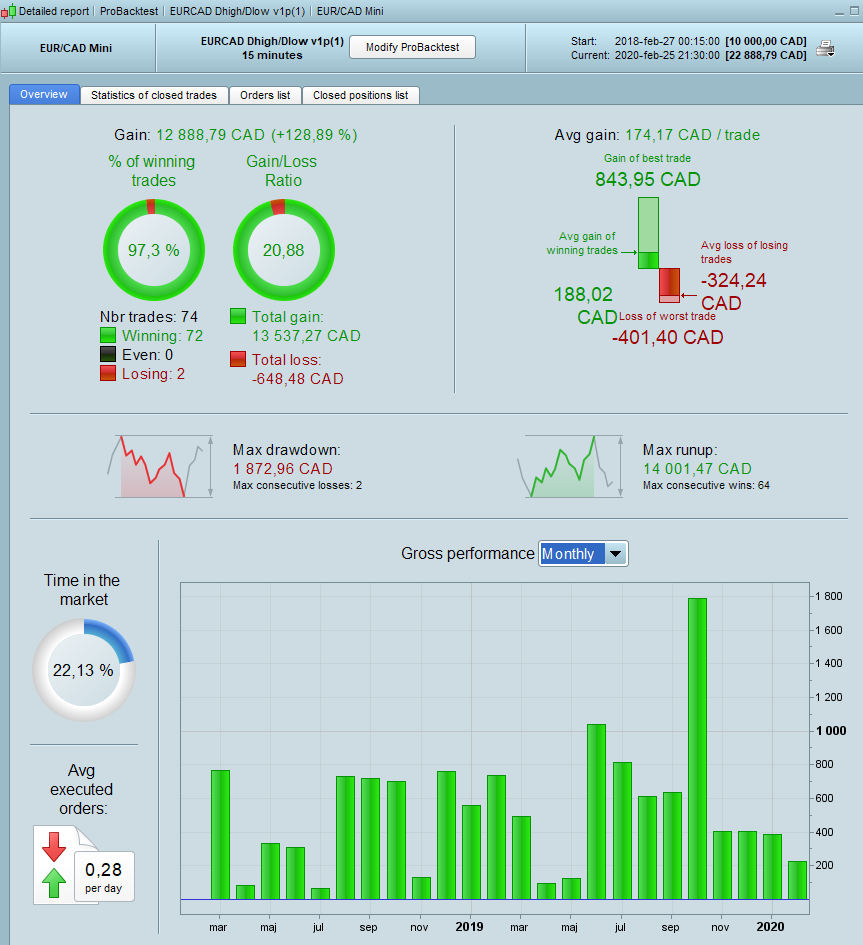

As mentioned by the original creator Matriciel the time-in-market is i bit high which will add interest cost. But the % winning trades and gain/loss ratio is fabulous. It would be nice to not have a large MAE in almost every trade but I don’t know how to fix that 🙂

// EURCAD Dhigh/Dlow v2 15m

// spread 2.5

defparam cumulateorders = false

defparam preloadbars = 10000

//

once enablets = 1

once select=2 // optimized for period1,2,3

once tds =1 // added on optimized results

// code re-invest

Capital = 10000

Equity = Capital + StrategyProfit

Position = Max(1, Equity * (1/Capital))

Position = Round(Position*100)

Position = Position/25

if select=1 then // TF 15 MIN

tr1=45

tr2=25

period1=78

period2=12

period3=4

elsif select=2 then // TF 15 MIN

tr1=45

tr2=20

period1=84

period2=6

period3=8

endif

// trend detection

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(Average[tr1](close)>Average[tr1](close)[1])

trenddown=(Average[tr2](close)<Average[tr2](close)[1])

else

if tds=2 then

endif

endif

endif

// strategy

//ctime = time >= 000000 and time <= 220000

mm = average[period1,3](totalprice)

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

avghl = (Newhighest+Newlowest)/2

c1 = average[period2,period3]((Newhighest+avghl)/2)

c2 = average[period2,period3]((Newlowest+avghl)/2)

condbuy = mm > c1

condbuy = condbuy and close crosses over avghl

condbuy = condbuy and trendup

condsell = mm < c2

condsell = condsell and close crosses under avghl

condsell = condsell and trenddown

//

//if ctime then

if condbuy then

buy position contract at market

endif

if condsell then

sellshort position contract at market

endif

//endif

// trailing stop atr

if enablets then

//

once steps=0 // set to 0 to ignore steps

once minatrdist=16

once atrtrailingperiod = 14 // atr parameter value

once minstop = 0 // minimum trailing stop distance

if barindex=tradeindex then

trailingstoplong = 16 // trailing stop atr relative distance

trailingstopshort = 16 // trailing stop atr relative distance

else

if longonmarket then

if prezzouscita>0 then

if trailingstoplong>minatrdist then

if prezzouscita>prezzouscita[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-steps

endif

else

trailingstoplong=minatrdist

endif

endif

endif

if shortonmarket then

if prezzouscita>0 then

if trailingstopshort>minatrdist then

if prezzouscita<prezzouscita[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-steps

endif

else

trailingstopshort=minatrdist

endif

endif

endif

endif

//

atrtrail=averagetruerange[atrtrailingperiod]((close/1)*pipsize)

trailingstartl=round(atrtrail*trailingstoplong)

trailingstarts=round(atrtrail*trailingstopshort)

tgl=trailingstartl

tgs=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice=0

minprice=close

prezzouscita=0

endif

//

if longonmarket then

maxprice=max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

prezzouscita=maxprice-tgl*pointsize

else

prezzouscita=maxprice-minstop*pointsize

endif

endif

endif

//

if shortonmarket then

minprice=min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

prezzouscita=minprice+tgs*pointsize

else

prezzouscita=minprice+minstop*pointsize

endif

endif

endif

//

if longonmarket then

if prezzouscita>0 then

sell at prezzouscita stop

endif

endif

if shortonmarket then

if prezzouscita>0 then

exitshort at prezzouscita stop

endif

endif

endif

set stop %loss 1.7

200k is not the best.

But it’s a very good starting point, needs to be watched better. Good job!

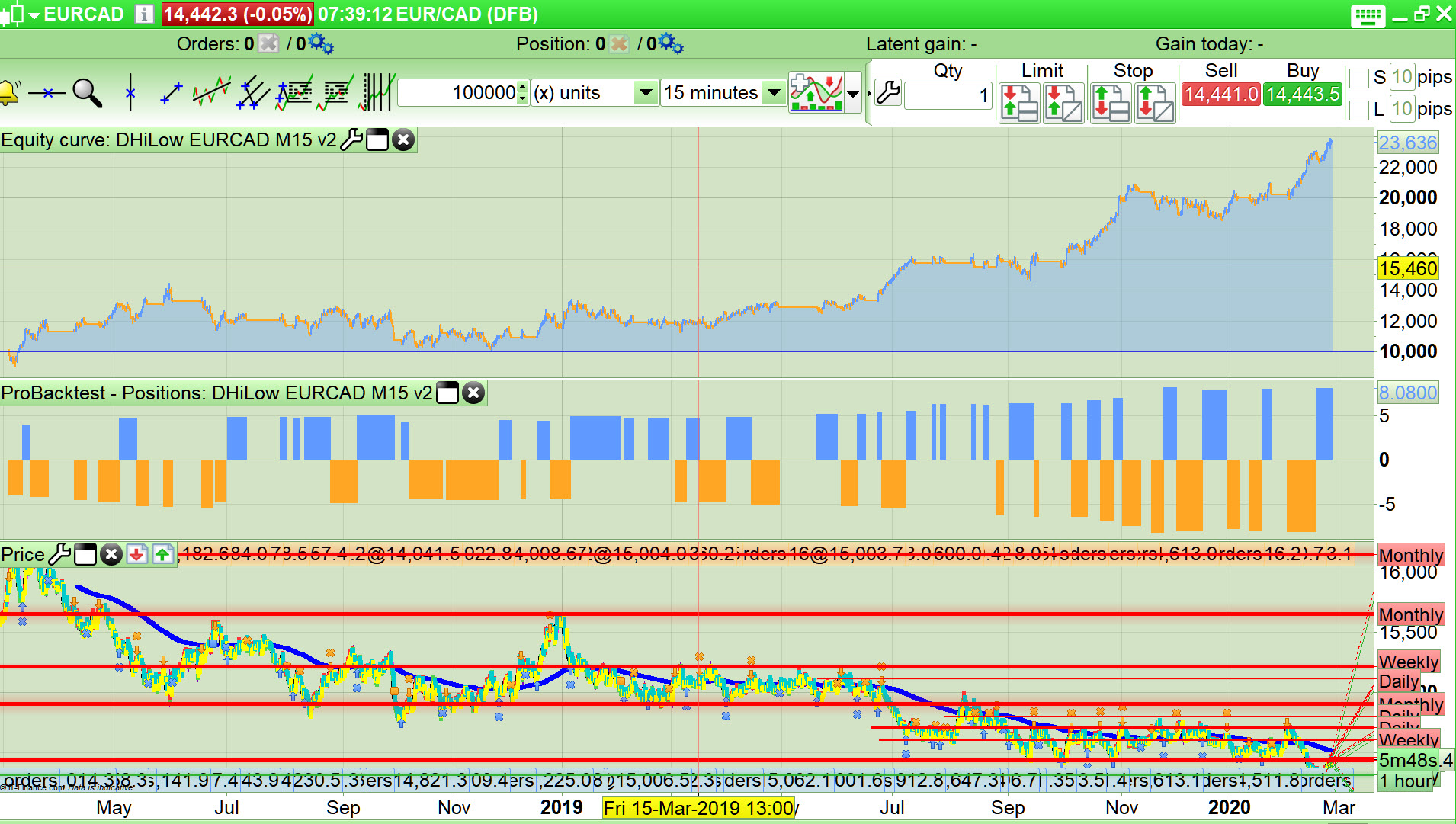

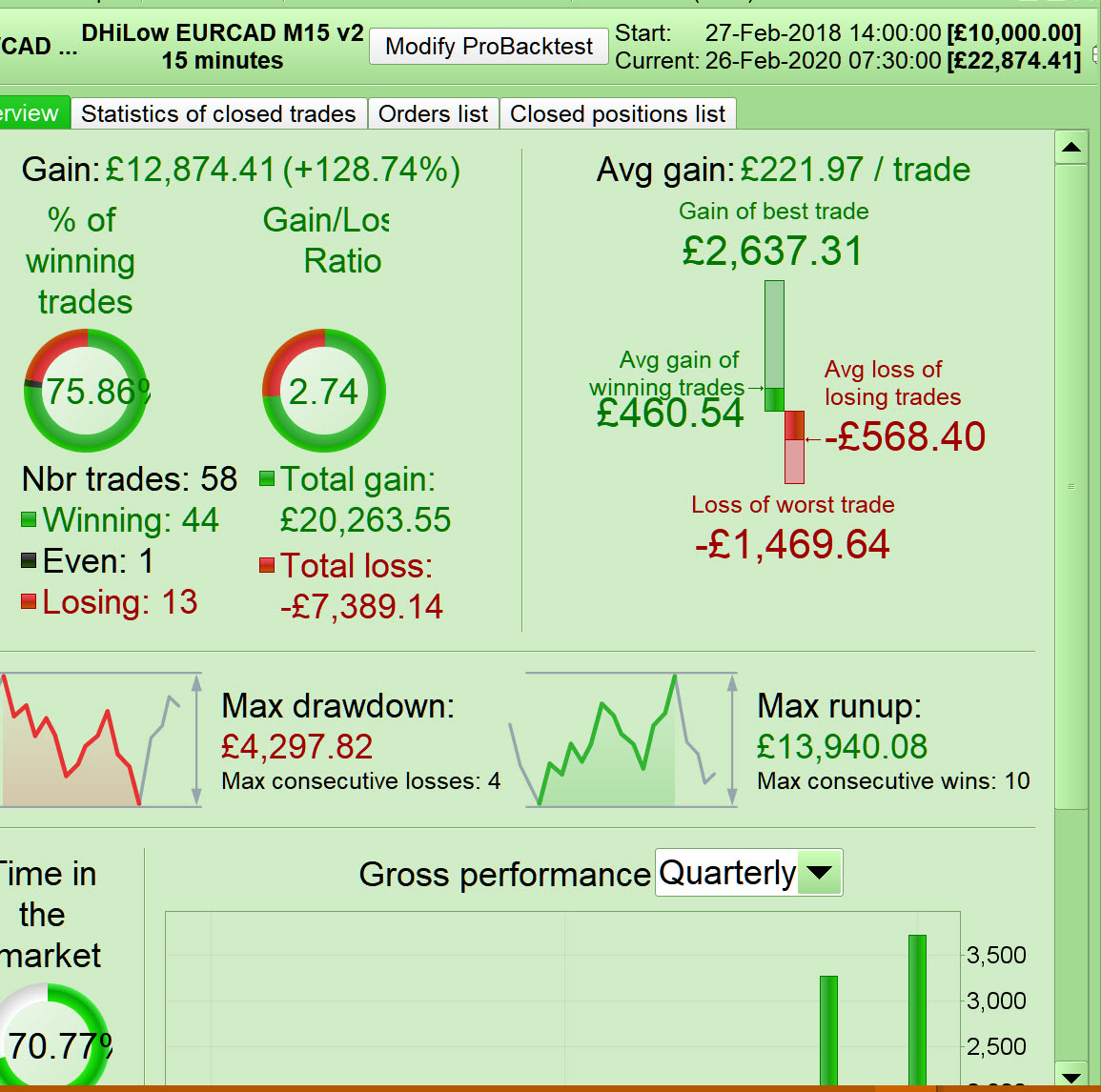

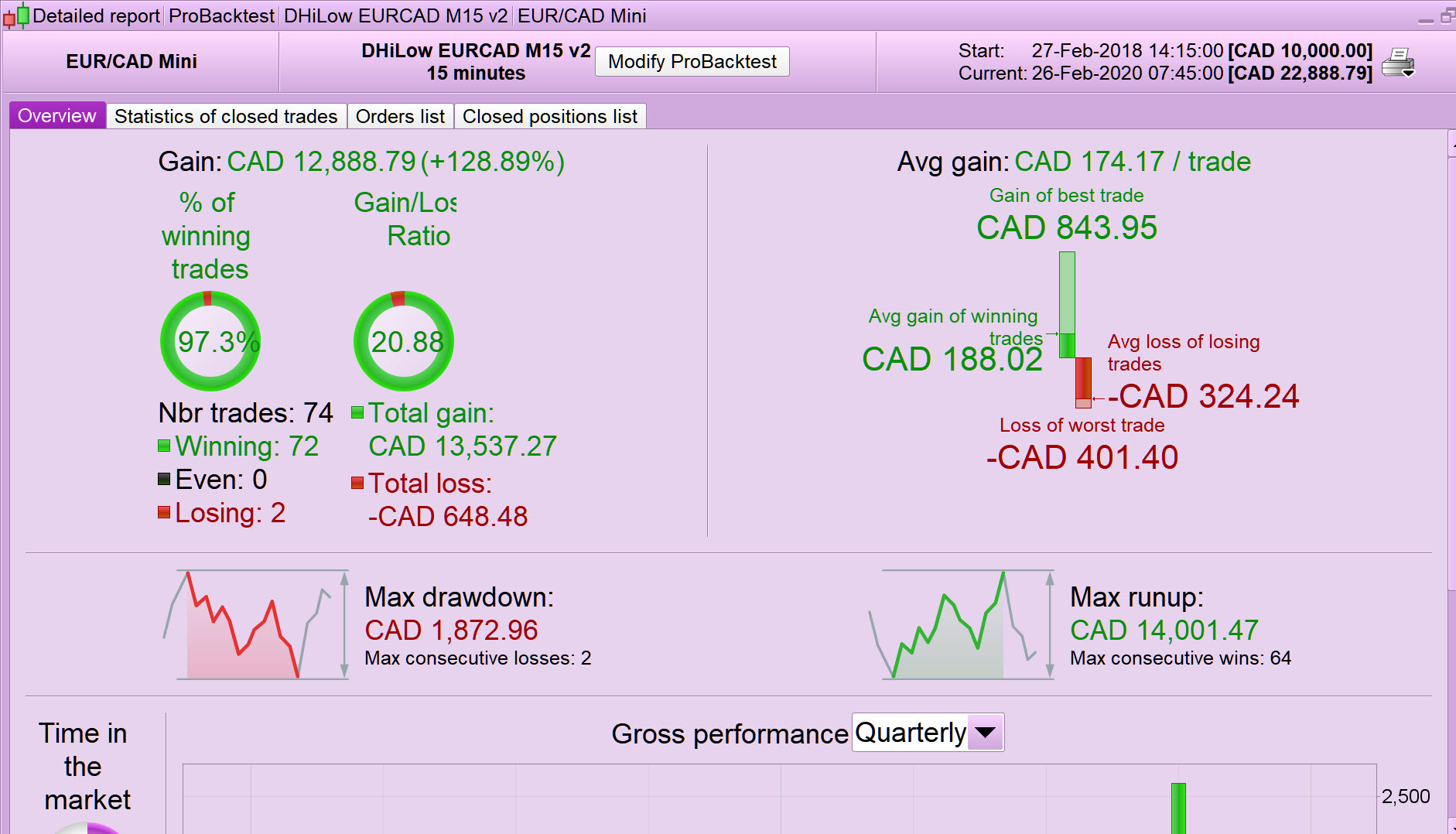

Weird … I don’t get the same curve or stats as you and there is no Time that I need to align with UK time, so I can’t think why we should be different.

I’m on SB and you are on CFD but I would expect that to only show a minor difference in performance stats?

Any thoughts anyone or what do you get??

I’ll try it on my CFD Platform.

EDIT / PS

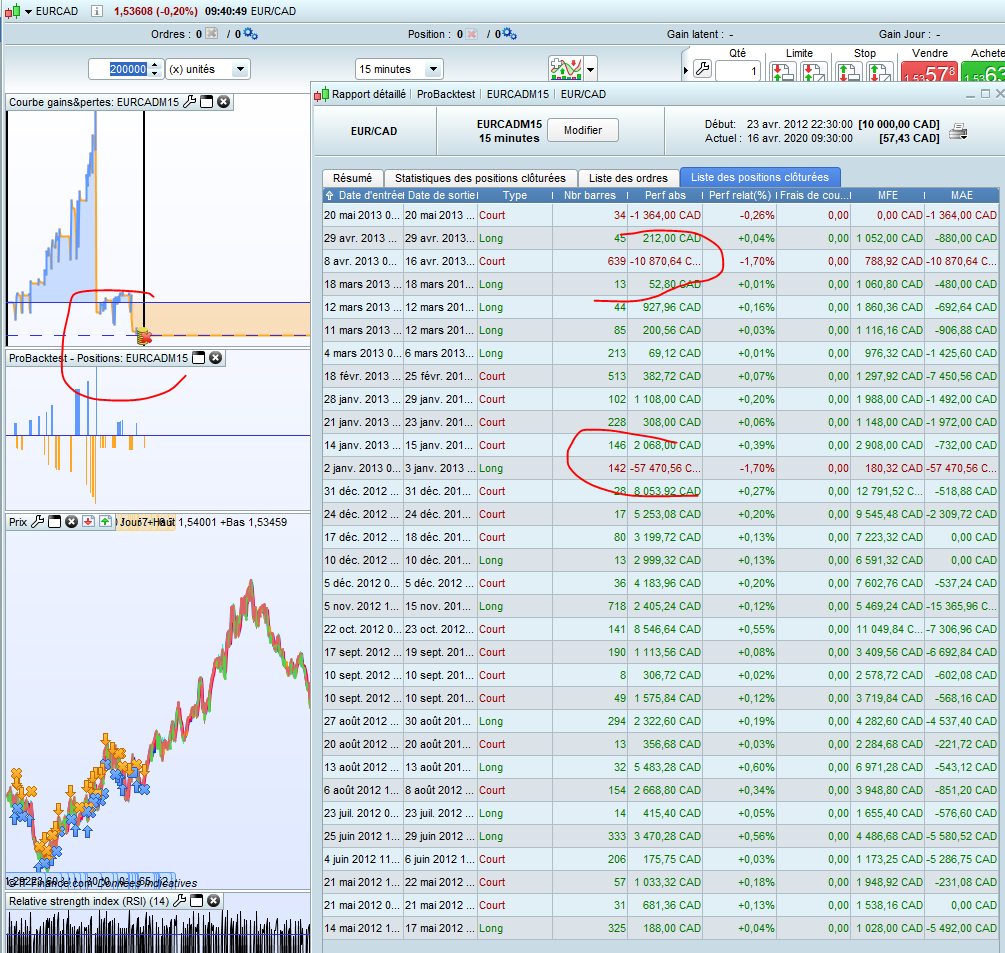

Yep …. on CFD same as you now @swedshare … see 3rd image … how unsettling is that??

Can only be that IG are playing around with the SB data to our disadvantage??

Price and spread (2.5) are the same currently on SB and CFD, but they can’t always be else performance stats would be same on SB as CFD … or has my coffee not worked through yet?? 🙂

3rd image attached (missed off from above post).

I get 74 trades on CFD (same as you) but I only get 58 trades on SB … and both charts are running over the same time period of 100k bars.

Very worrying anomaly for us British .. is Brexit hurting us already!!?? 🙂 🙂

Thanks Swedshare! Its awesome!

I am the beginninger in this.

May I know the time 000000 to 200000, if my time zone is GMT+8. The code any update? thanks.

Alfred, you don’t really need to care about the time. It can run 24/7. The important part to notice is the relatively high risk. When/if a trade reaches its stoploss you will get a big loss.

Another factor to consider is why the strategy only seems to work well on EUR/CAD and not the other currency pairs. That should rise a red flag 🙂

Hello to you all,

I have a good feedback on the EUR code USD H1. May I am still blocking about partial fences, impossible to run in prorder. Can one of you help me?

May I am still blocking about partial fences

Above does not make sense.

But if you mean partial closures? ProOrder does not allow partial closures.

Change Sell and Exitshort to below

Sell at Market

ExitShort at Market

Thanks Swedshare

I have run this strategy one month ago, the result is ok

Hello Grahall, thank you for your reply. Indeed my first message was incorrectly translated by my English translation software. But you get it.

Despite your trick, I can’t get the code to work.

If I send it to you, can you make the changes? I am a poor coder yet… To read you, thank you, cordially.

Hi all, I backtested the EurUsd 15min and the EurCad 15min v2 and… 97% win. I actually tried to activate autotrading on my demo account of both with max 1 contract (100.000) and I’ll see. I just had to “//” the graph function on EurUSd otherwise the system won’t let me use it.

Is there some parameter for auto trading you suggest me to set up?

Thanks a lot

@swedshare

Are you sure about your strategy ?

if tp not reached, > sl. 200k test/spread 2.5

Hi @MAKSIDE

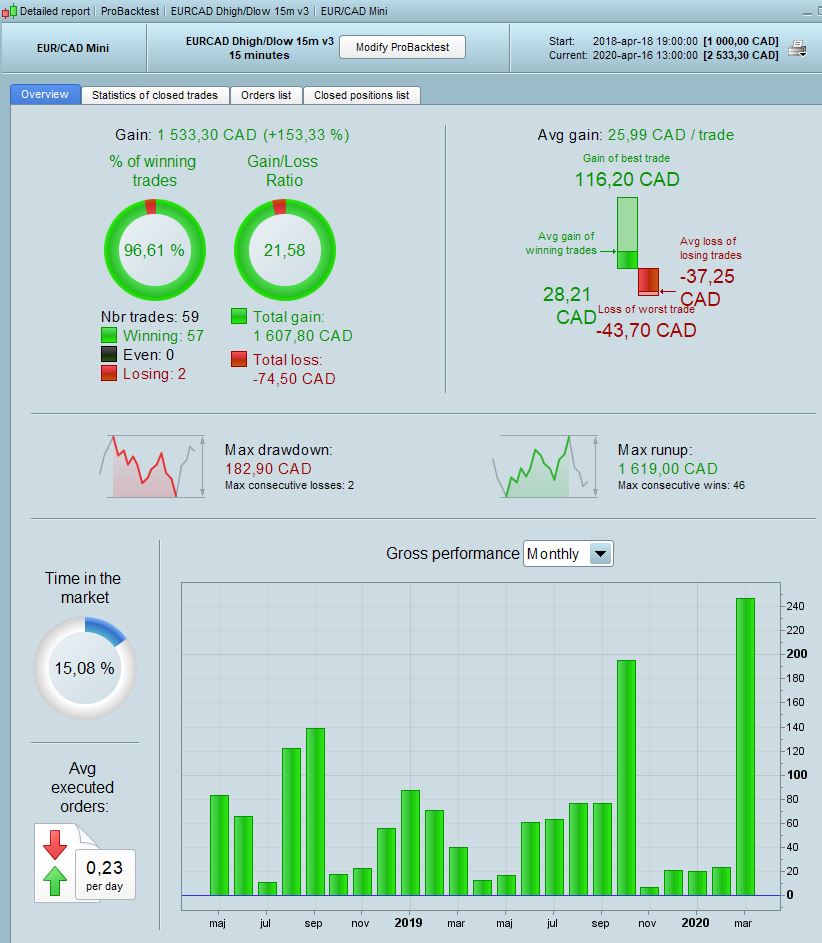

I definately have doubts about the long term robustness of the strategy. I made some minor changes since the v2. See attached for current version. I have disabled the re-invest and only buy 1 contract each time. Also don’t hold position over weekend. If you would like to check how the equity curve developes in 200k it would be appreciated. Spread is now set to 6 to reflect what IG offers. Initial capital 1000 CAD.

// Created by Matriciel. Added MM, riskM and calender by swedshare

// EURCAD Dhigh/Dlow v3 15m

// spread = 6 (actual spread on IG CFD)

defparam cumulateorders = false

defparam preloadbars = 5000

//code re-invest

Capital = 1000 // initial capital

Equity = Capital + StrategyProfit

Position = Max(1, Equity * (1/Capital))

Position = Round(Position*100)

Position = Position/100 // not activated. Change "1" to "position" in the buy conditions to use re-invest.

//********************

set stop %loss 1.30

//code quit strategy

maxequity = max(equity,maxequity)

DrawdownNeededToQuit = 40 // percent drawdown from max equity to stop strategy

if equity < maxequity * (1 - (DrawdownNeededToQuit/100)) then

quit

endif

//*****************

// Force close of positions at Friday 21:30:00 (UTC+2 Europe/Berlin)

if dayofweek = 5 and time = 213000 then

IF longonmarket THEN

SELL AT MARKET

endif

if shortonmarket then

EXITSHORT AT MARKET

ENDIF

ENDIF

//*************

// Don't take position after friday 20:00:00 (UTC+2 Europe/Berlin)

BadTime = dayofweek = 5 AND OpenTime > 200000

//*************

once enablets = 1

once select=1 // optimized for period1,2,3

once tds =1 // added on optimized results

if select=1 then // TF 15 MIN

tr1=45

tr2=25

period1=78

period2=12

period3=4

elsif select=2 then // TF 15 MIN

tr1=45

tr2=20

period1=84

period2=6

period3=8

endif

// trend detection

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(Average[tr1](close)>Average[tr1](close)[1])

trenddown=(Average[tr2](close)<Average[tr2](close)[1])

else

if tds=2 then

endif

endif

endif

mm = average[period1,3](totalprice)

Newhighest=max(DHigh(0), DHigh(1))

Newlowest=min(DLow(0), DLow(1))

avghl = (Newhighest+Newlowest)/2

c1 = average[period2,period3]((Newhighest+avghl)/2)

c2 = average[period2,period3]((Newlowest+avghl)/2)

condbuy = mm > c1

condbuy = condbuy and close crosses over avghl

condbuy = condbuy and trendup

condsell = mm < c2

condsell = condsell and close crosses under avghl

condsell = condsell and trenddown

if condbuy and not BadTime then

buy 1 contract at market

endif

if condsell and not BadTime then

sellshort 1 contract at market

endif

//endif

// trailing stop atr

if enablets then

//

once steps=0 // set to 0 to ignore steps

once minatrdist=16

once atrtrailingperiod = 14 // atr parameter value

once minstop = 0 // minimum trailing stop distance

if barindex=tradeindex then

trailingstoplong = 16 // trailing stop atr relative distance

trailingstopshort = 16 // trailing stop atr relative distance

else

if longonmarket then

if prezzouscita>0 then

if trailingstoplong>minatrdist then

if prezzouscita>prezzouscita[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-steps

endif

else

trailingstoplong=minatrdist

endif

endif

endif

if shortonmarket then

if prezzouscita>0 then

if trailingstopshort>minatrdist then

if prezzouscita<prezzouscita[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-steps

endif

else

trailingstopshort=minatrdist

endif

endif

endif

endif

//

atrtrail=averagetruerange[atrtrailingperiod]((close/1)*pipsize)

trailingstartl=round(atrtrail*trailingstoplong)

trailingstarts=round(atrtrail*trailingstopshort)

tgl=trailingstartl

tgs=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice=0

minprice=close

prezzouscita=0

endif

//

if longonmarket then

maxprice=max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

prezzouscita=maxprice-tgl*pointsize

else

prezzouscita=maxprice-minstop*pointsize

endif

endif

endif

//

if shortonmarket then

minprice=min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

prezzouscita=minprice+tgs*pointsize

else

prezzouscita=minprice+minstop*pointsize

endif

endif

endif

//

if longonmarket then

if prezzouscita>0 then

sell at prezzouscita stop

endif

endif

if shortonmarket then

if prezzouscita>0 then

exitshort at prezzouscita stop

endif

endif

endif