Oh great, thanks for the feedback.

please, can someone try to explain why this happens, i really dont get it !

When i backtest the strategy it goes SHORT but automatic trading took a LONG today….

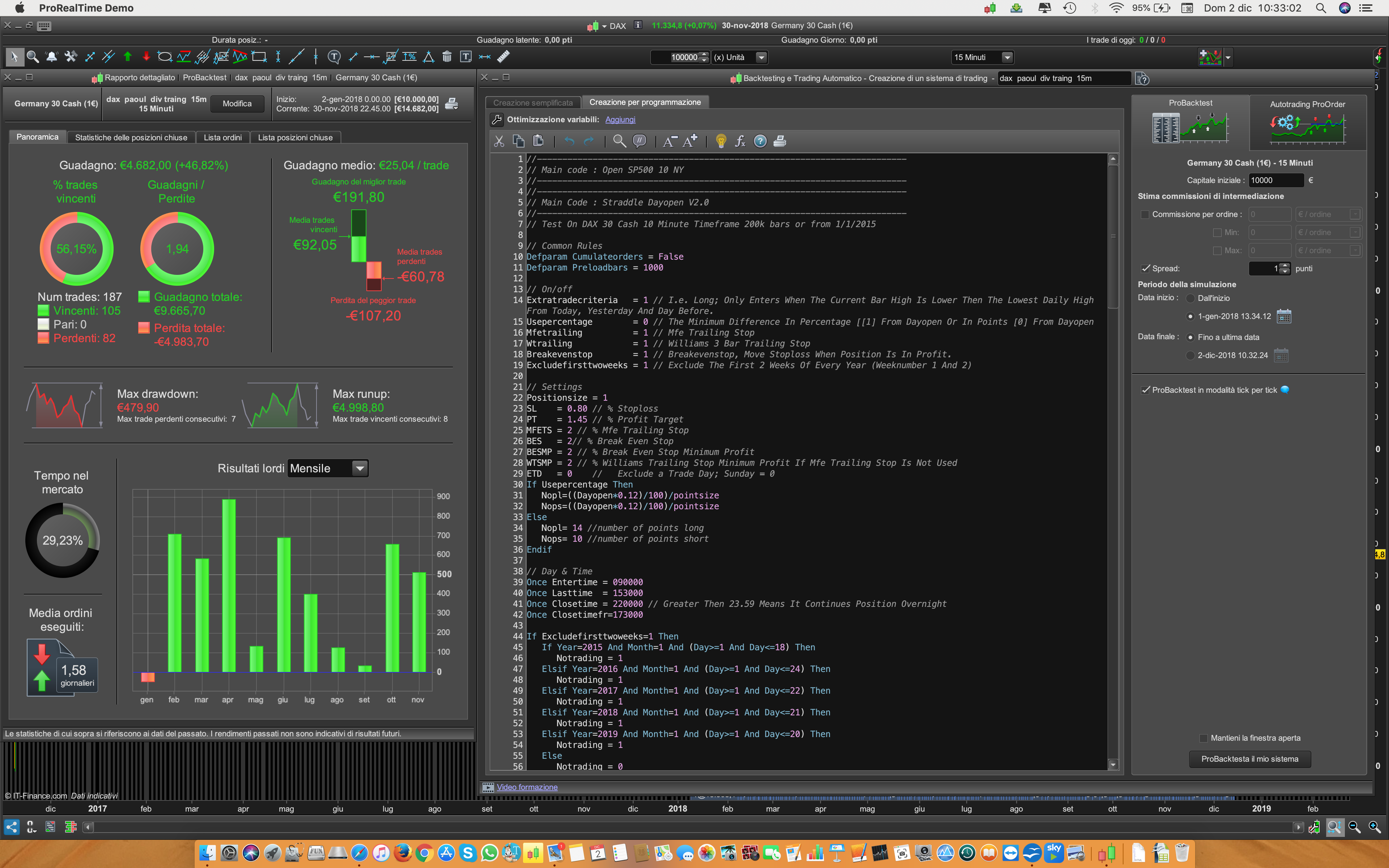

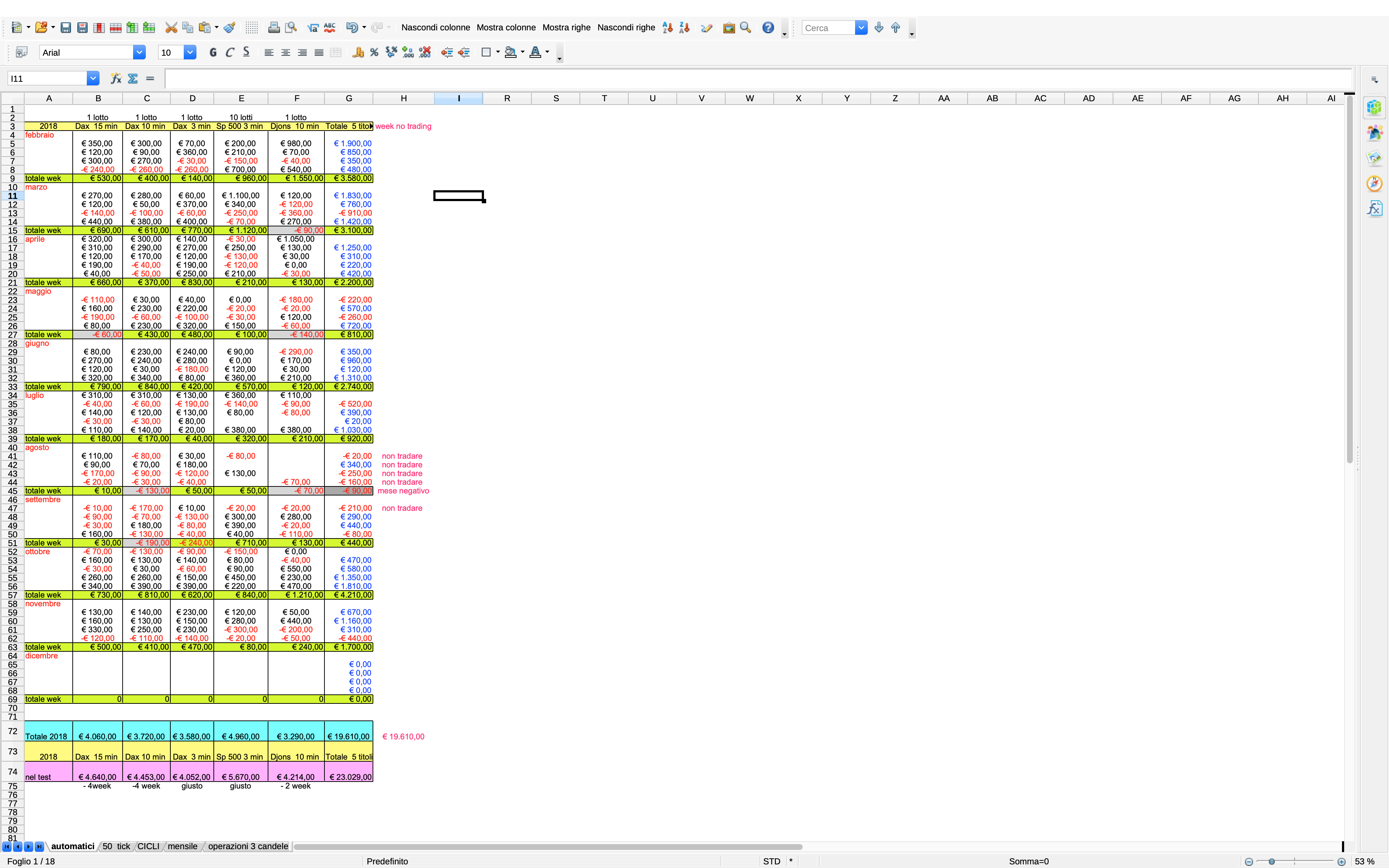

buongiorno paolo volevo mostrarti alcune modifiche sul tuo lavoro , io sono neofita ho appena iniziato a capirci qualcosa ,

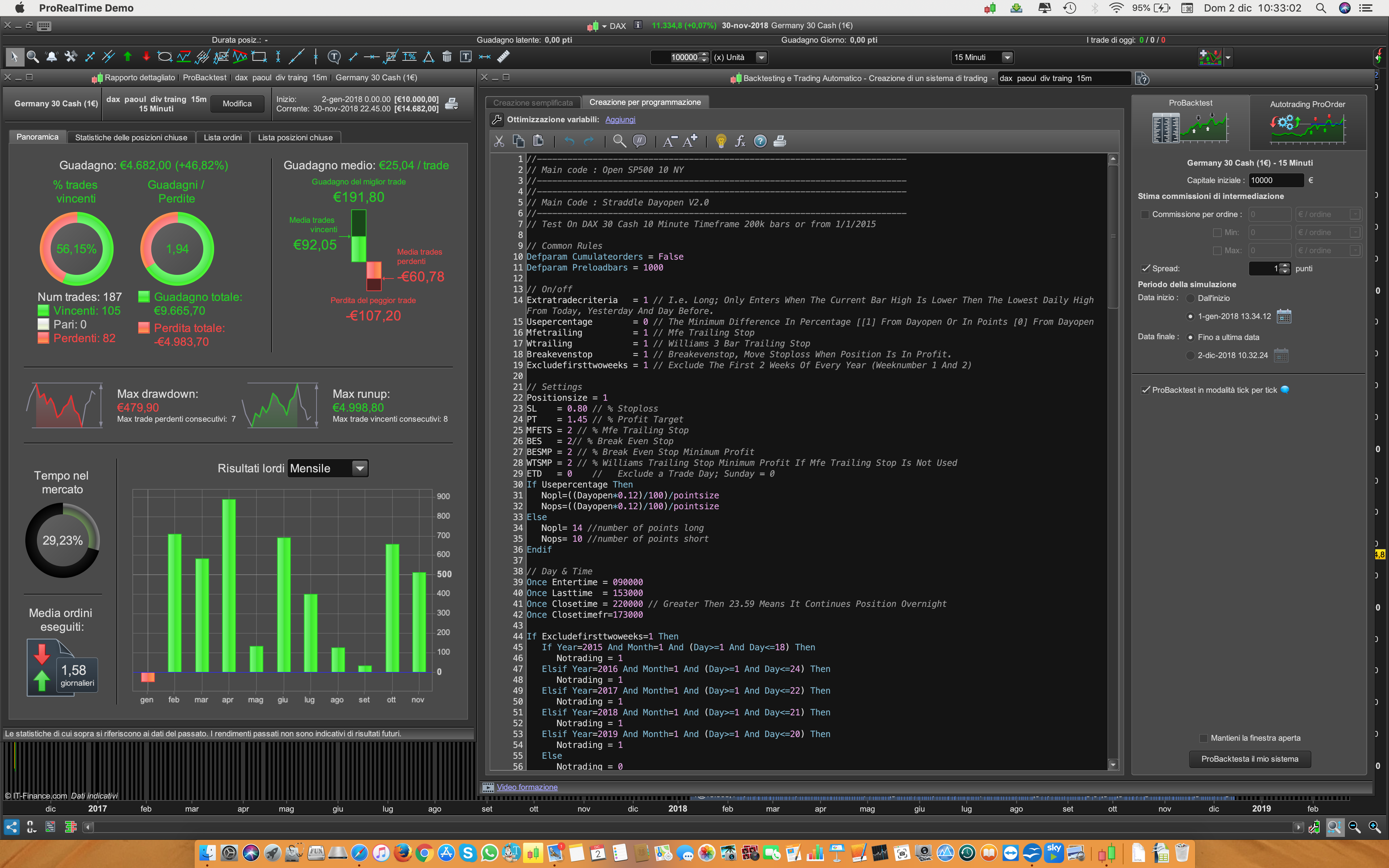

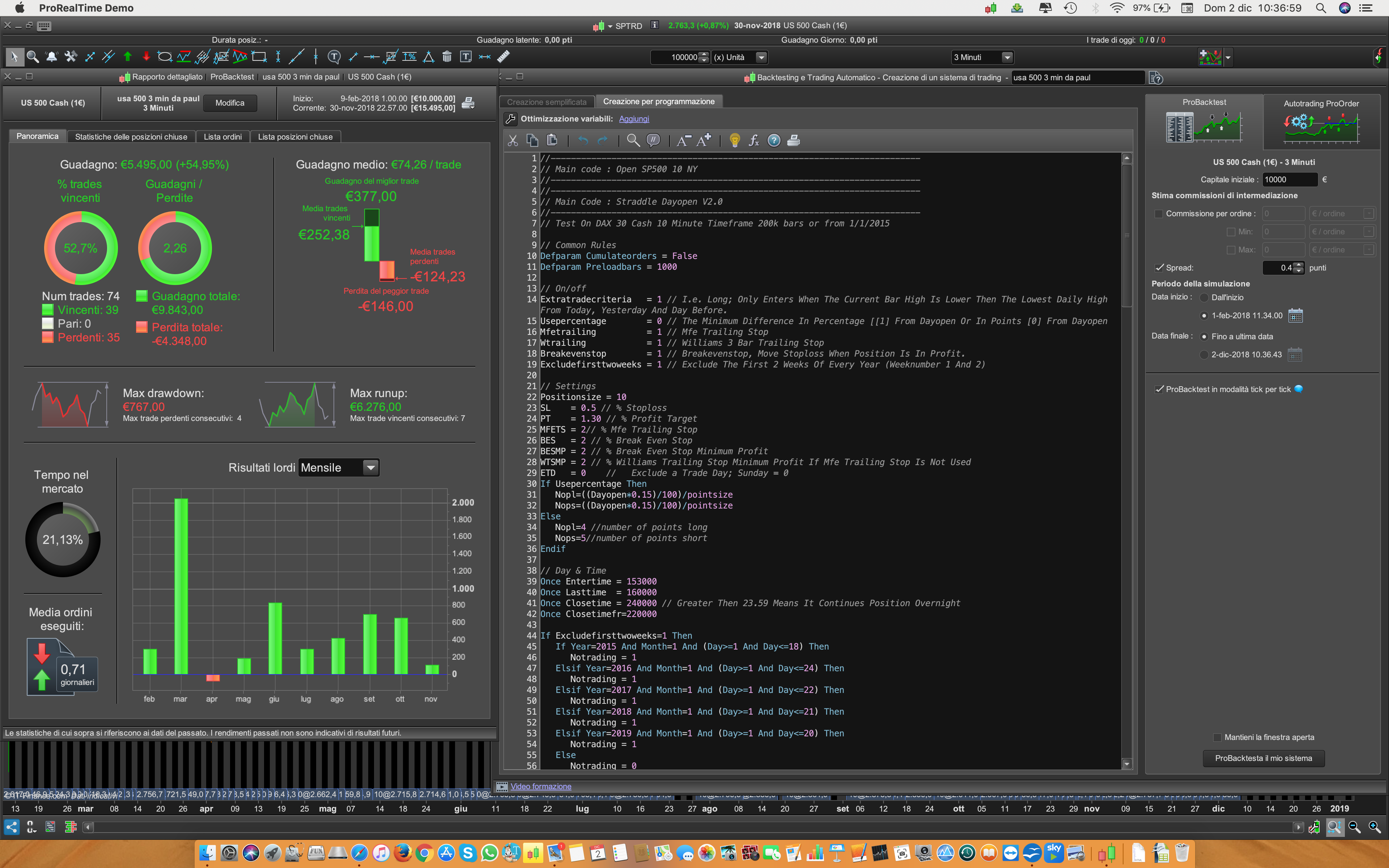

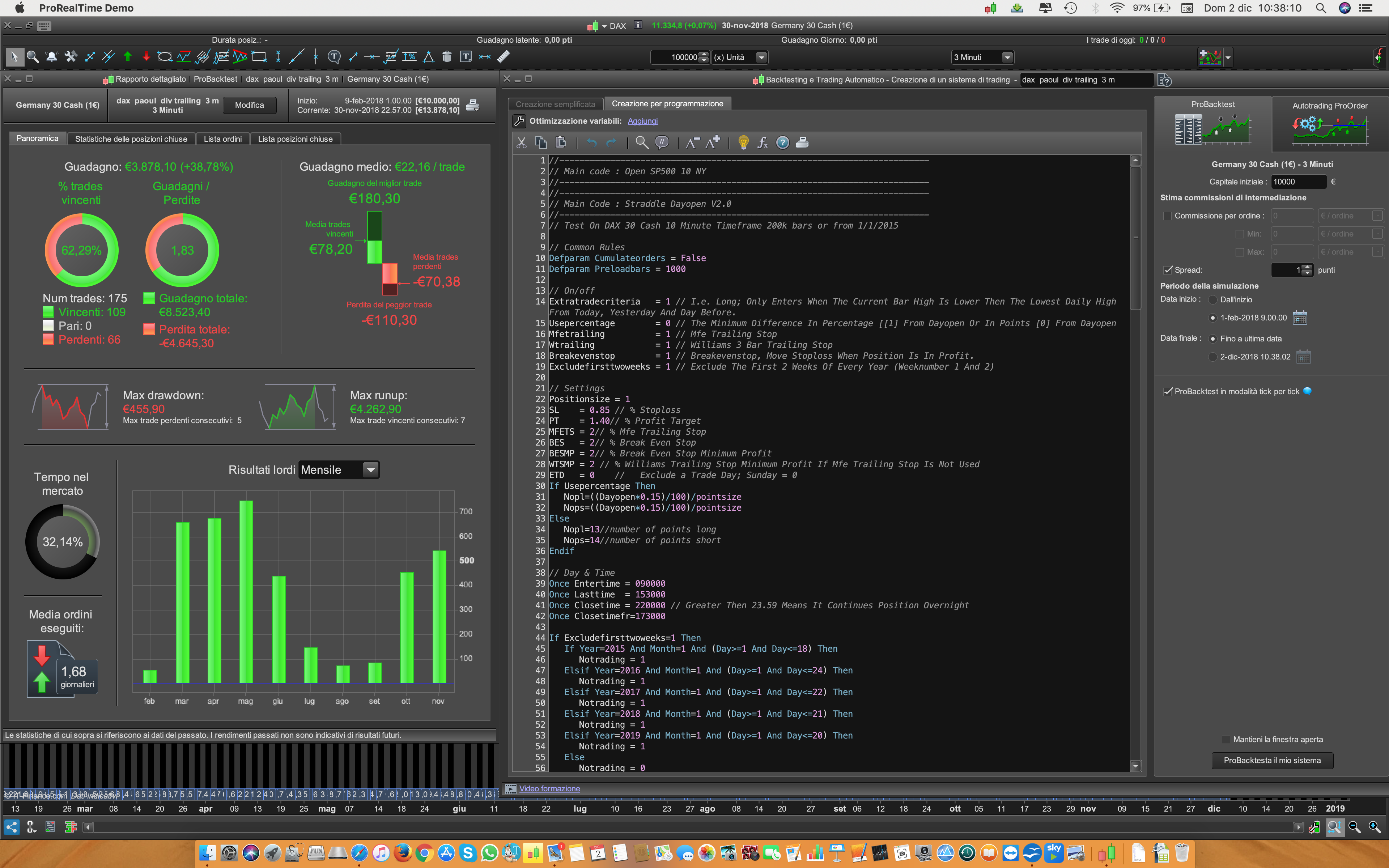

quindi mi scuserai se mostro cavolate , ho fatto anche il djons a 10 minuti e funziona bene , i dati che ti mostro sono non più di un anno ma li ho testi anche sui 2 anni e funzionano bene .

ho escluso il Trailing stop da tutti perché funziona meglio e da risultati migliori .

domani inizio a metterli sul reale con piccola size , cosa ne pensi ?

grazie ancora x il lavoro che hai svolto

eugenio

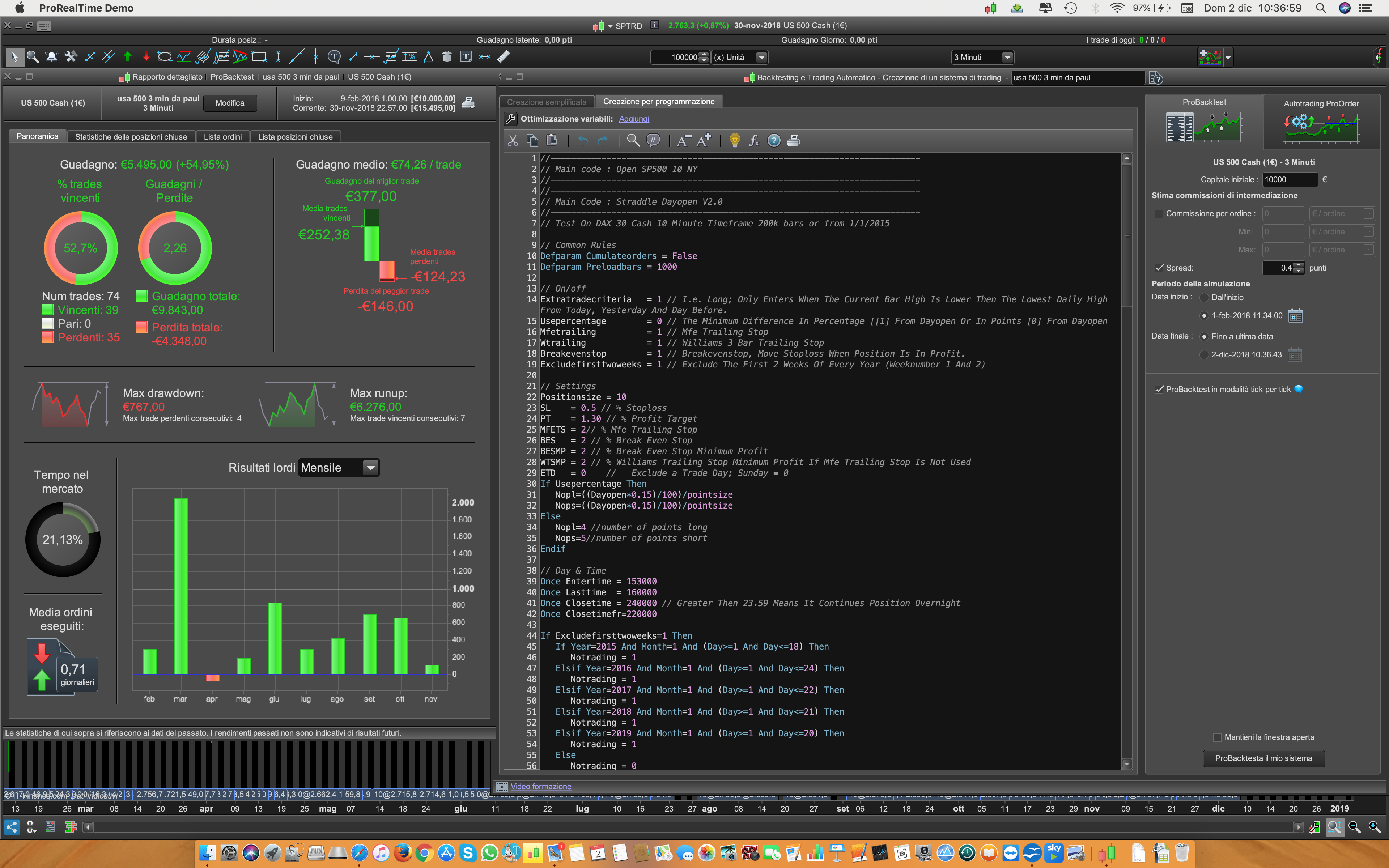

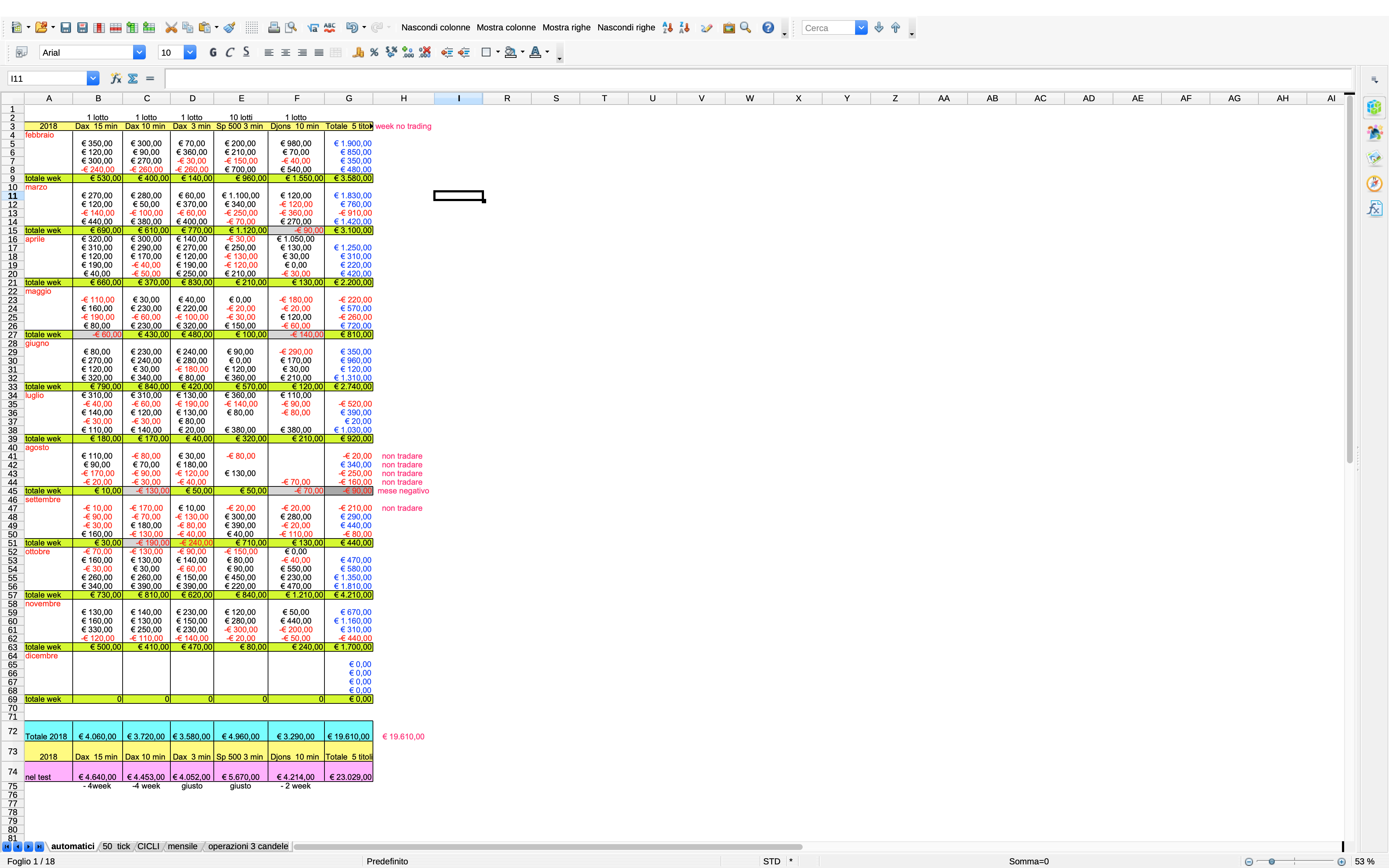

scusa dimenticavo ho fatto tutti i conti e la resa dei mesi del 2018 e ho notato che il mese di agosto non è da tradare ,

ho escluso gennaio che non rende

guarda i risultati e dimmi cosa ne pensi

grazie

eugenio

chiaramente mi piacerebbe un opinione anche da tutti ,

sempre ne valga la pena

grazie

eugenio

@eugenio

sul forum inglese scrivi in inglese. Grazie.

I apologize again in English

hello paolo I wanted to show you some changes on your work, I’m neophyte I just started to understand something,

so you will excuse me if I show stupid things, I have also done the djons 10 minutes and it works well, the data I show you are not more than a year but I have them even on 2 years and they work well.

I have excluded the Trailing stop from everyone because it works better and results better.

Tomorrow I start to put them on the real with a small size, what do you think?

I made all the accounts and the yield of the months of 2018 and I noticed that the month of August is not to be traded,

I excluded January that does not make

thanks again for the work you have done

clearly I would like an opinion from everyone,

eugenio

Hi,

can you share the strategy version for SP500 ?

@eugenio: It could be a solution, but I preferred to do an optimization to keep high percentage of positive trade minimizing the DD. So I kept the trailing.

thanks

//-------------------------------------------------------------------------

// Main code : Open SP500 3 minuti NY

//------------------------------------------------------------------------

// Common Rules

Defparam Cumulateorders = False

Defparam Preloadbars = 1000

// On/off

Extratradecriteria = 1 // I.e. Long; Only Enters When The Current Bar High Is Lower Then The Lowest Daily High From Today, Yesterday And Day Before.

Usepercentage = 0 // The Minimum Difference In Percentage [[1] From Dayopen Or In Points [0] From Dayopen

Mfetrailing = 1 // Mfe Trailing Stop

Wtrailing = 1 // Williams 3 Bar Trailing Stop

Breakevenstop = 1 // Breakevenstop, Move Stoploss When Position Is In Profit.

Excludefirsttwoweeks = 1 // Exclude The First 2 Weeks Of Every Year (Weeknumber 1 And 2)

// Settings

Positionsize = 10

SL = 0.5 // % Stoploss

PT = 1.30 // % Profit Target

MFETS = 2// % Mfe Trailing Stop

BES = 2 // % Break Even Stop

BESMP = 2 // % Break Even Stop Minimum Profit

WTSMP = 2 // % Williams Trailing Stop Minimum Profit If Mfe Trailing Stop Is Not Used

ETD = 0 // Exclude a Trade Day; Sunday = 0

If Usepercentage Then

Nopl=((Dayopen*0.15)/100)/pointsize

Nops=((Dayopen*0.15)/100)/pointsize

Else

Nopl=4 //number of points long

Nops=5//number of points short

Endif

// Day & Time

Once Entertime = 153000

Once Lasttime = 160000

Once Closetime = 240000 // Greater Then 23.59 Means It Continues Position Overnight

Once Closetimefr=220000

If Excludefirsttwoweeks=1 Then

If Year=2015 And Month=1 And (Day>=1 And Day<=18) Then

Notrading = 1

Elsif Year=2016 And Month=1 And (Day>=1 And Day<=24) Then

Notrading = 1

Elsif Year=2017 And Month=1 And (Day>=1 And Day<=22) Then

Notrading = 1

Elsif Year=2018 And Month=1 And (Day>=1 And Day<=21) Then

Notrading = 1

Elsif Year=2019 And Month=1 And (Day>=1 And Day<=20) Then

Notrading = 1

Else

Notrading = 0

Endif

Endif

Tt1 = Time >= Entertime

Tt2 = Time <= Lasttime

Tradetime = Tt1 And Tt2 and Notrading = 0 And Dayofweek <> ETD

// Reset At Start

If Intradaybarindex = 0 Then

Longtradecounter = 0

Shorttradecounter = 0

Tradecounter = 0

Mclong = 0

Mcshort = 0

Endif

// [pc] Position Criteria

Pclong = Countoflongshares < 1 And Longtradecounter < 1 And Tradecounter < 1

Pcshort = Countofshortshares < 1 And Shorttradecounter < 1 And Tradecounter < 1

// [mc] Main Criteria

If Time = Entertime Then

Dayopen=open

Endif

If High > Dayopen+nopl Then

Mclong=1

Else

Mclong=0

Endif

If Low < Dayopen-nops Then

Mcshort=1

Else

Mcshort=0

Endif

// [ec] Extra Criteria

If Extratradecriteria Then

Min1 = Min(Dhigh(0),dhigh(1))

Min2 = Min(Dhigh(1),dhigh(2))

Max1 = Max(Dlow(0),dlow(1))

Max2 = Max(Dlow(1),dlow(2))

Eclong = High < Min(Min1,min2)

Ecshort = Low > Max(Max1,max2)

else

Eclong=1

Ecshort=1

Endif

// Long & Short Entry

If Tradetime Then

If Pclong and Mclong And Eclong Then

Buy Positionsize Contract At Market

Longtradecounter=longtradecounter + 1

Tradecounter=tradecounter+1

Endif

If Pcshort and Mcshort And Ecshort Then

Sellshort Positionsize Contract At Market

Shorttradecounter=shorttradecounter + 1

Tradecounter=tradecounter+1

Endif

Endif

// Break Even Stop

If Breakevenstop Then

If Not Onmarket Then

Newsl=0

Endif

If Longonmarket And close-tradeprice(1)>=((Tradeprice/100)*BES)*pipsize Then

Newsl = Tradeprice(1)+((Tradeprice/100)*BESMP)*pipsize

Endif

If Shortonmarket And Tradeprice(1)-close>=((Tradeprice/100)*BES)*pipsize Then

Newsl = Tradeprice(1)-((Tradeprice/100)*BESMP)*pipsize

Endif

If Newsl>0 Then

Sell At Newsl Stop

Exitshort At Newsl Stop

Endif

Endif

// Exit Mfe Trailing Stop

If Mfetrailing Then

Trailingstop = (Tradeprice/100)*MFETS

If Not Onmarket Then

Maxprice = 0

Minprice = Close

Priceexit = 0

Endif

If Longonmarket Then

Maxprice = Max(Maxprice,close)

If Maxprice-tradeprice(1)>=trailingstop*pipsize Then

Priceexit = Maxprice-trailingstop*pipsize

Endif

Endif

If Shortonmarket Then

Minprice = Min(Minprice,close)

If Tradeprice(1)-minprice>=trailingstop*pipsize Then

Priceexit = Minprice+trailingstop*pipsize

Endif

Endif

If Onmarket And Wtrailing=0 And Priceexit>0 Then

Sell At Market

Exitshort At Market

Endif

Endif

// Exit Williams Trailing Stop

If Wtrailing Then

Count=1

I=0

J=i+1

Tot=0

While Count<4 Do

Tot=tot+1

If (Low[j]>=low[i]) And (High[j]<=high[i]) Then

J=j+1

Else

Count=count+1

I=i+1

J=i+1

Endif

Wend

Basso=lowest[tot](Low)

Alto=highest[tot](High)

If Close>alto[1] Then

Ref=basso

Endif

If Close<basso[1] Then

Ref=alto

Endif

If Onmarket And Mfetrailing=0 And Positionperf>WTSMP Then

If Low[1]>ref And High<ref Then

Sell At Market

Endif

If High[1]<ref And Low>ref Then

Exitshort At Market

Endif

Endif

If Onmarket And Mfetrailing=1 And Priceexit>0 Then

If High<ref Then

Sell At Market

Endif

If Low>ref Then

Exitshort At Market

Endif

Endif

Endif

// Exit At Closetime

If Onmarket Then

If Time >= Closetime Then

Sell At Market

Exitshort At Market

Endif

Endif

// Exit At Closetime Friday

If Onmarket Then

If (Currentdayofweek=5 And Time>=closetimefr) Then

Sell At Market

Exitshort At Market

Endif

Endif

// Build-in Exit

Set Stop %loss SL

Set Target %profit PT

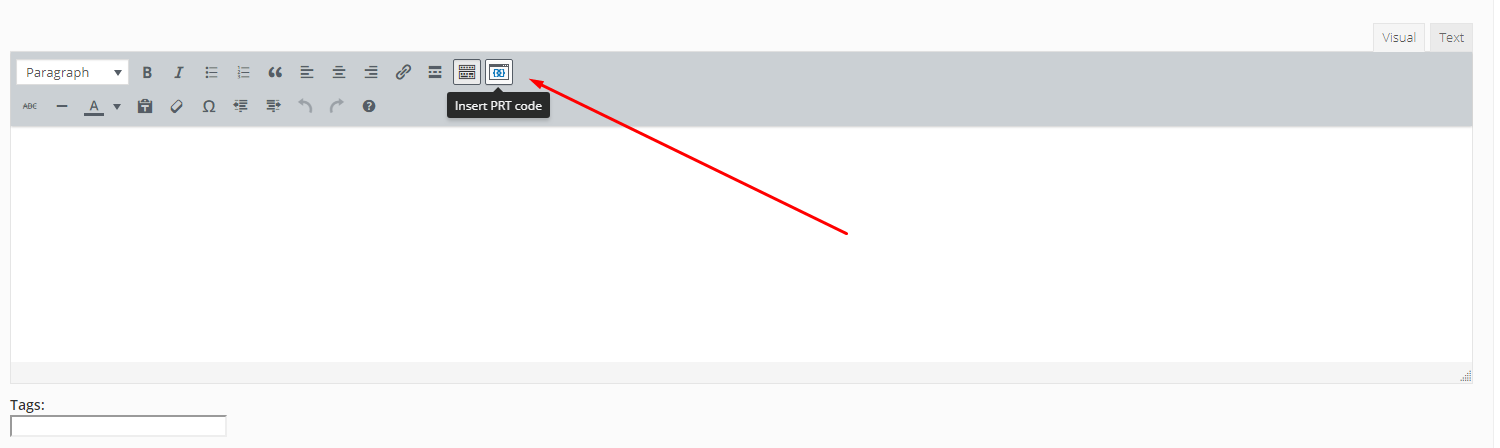

eugenio – Please use the ‘Insert PRT Code’ button when putting code in your posts as it makes it far easier for others to read. I have tidied up your post for you. 🙂

Attaching an exported ITF file can also be a useful alternative when the code is quite large.

good morning ,

I did not know, you tell me where I find ‘Insert PRT Code’ button?

thanks for the instruction, unfortunately I’m new on this forum

eugenio

Paul

PaulParticipant

Master

@eugenio

Thanks for posting!

I like to keep the mfe trailing stop and the breakeven.

It may look that the total results are better with trailing stop disabled, but are you ready to see a gain nearing a profit target go back to your stoploss level?

A SL too small may get you out quickly.

a correction in the code

// Long & Short Entry

If not onmarket and Tradetime Then

true what you say Paul, but the results speak clearly, the trailing too many times affect the overall gain, if I know, as from the test that the total and greater gain I prefer lose,

clearly this consideration is very personal, so I fully share your expression, you did well to put the trailing stop, then it’s up to everyone to do what they think.

however, the fact remains that your work is fantastic.

Have you already used it in real?

I start tomorrow

Thanks again

eugenio

eugenio – This is where you find the ‘Insert PRT Code’ button.

[attachment file=86202]

PaulParticipant

Master

Yes, i’am running it live and the results are similar to the backtest!

A trailing stop, especially the small one, can get you out quickly.

If you prefer to disable the trailing stop, you can still use the breakeven.

i.e. when a position is in profit for 0.35% it moves the breakeven stop from -1.00 to -.0.50%

At a quick glance, it improves the results.

edit; tested the sp500 3min