where did you try? have not seen a reply to my comment?

I think Paul may mean that he looked at his code and tried to reverse engineer it into plain english for you to understand? Some guys (and gals! 🙂 ) think straight into code and not in plain english first. There are also language differences making it even more difficult.

Jonas … have you tried to choose what you think is a trade trigger and GRAPH it against the results equity curve? This is one way to better understand what is triggering a trade. Then repeat for all the triggers as you see them.

https://www.prorealcode.com/documentation/graph/

If you cannot see / understand a single trigger then say so and maybe we (you, me, others) can take it one small bite at a time?

I don’t understand code easily either, but above is how I would do it if I wanted to convert back from a coded System into Manual trading?

Hope above idea helps you move forward?

where did you try? have not seen a reply to my comment?

I think Paul may mean that he looked at his code and tried to reverse engineer it into plain english for you to understand? Some guys (and gals! ) think straight into code and not in plain english first. There are also language differences making it even more difficult.

Jonas … have you tried to choose what you think is a trade trigger and GRAPH it against the results equity curve? This is one way to better understand what is triggering a trade. Then repeat for all the triggers as you see them.

https://www.prorealcode.com/documentation/graph/

If you cannot see / understand a single trigger then say so and maybe we (you, me, others) can take it one small bite at a time?

I don’t understand code easily either, but above is how I would do it if I wanted to convert back from a coded System into Manual trading?

Hope above idea helps you move forward?

but since he built the strategy he must know what his entry signal is?

all i understand is if high of 10 min today bar is lower than highest high of last 2 daily bars, its a long. Buy when x points over open?

Paul

PaulParticipant

Master

Hi Jonas, please read the first post in this thread and the second post of page 2 which explains the reasoning of the extra criteria.

you wrote

all i understand is

if high of 10 min today bar is lower than highest high of last 2 daily bars, its a long. Buy when x points over open?

that should be

if high of 10 min today bar is lower than lowest high of last 2 daily bars (and from current day) and the index raises over i.e. 24 points from the openings-value of the bar at 9.00 AM, then it’s a long. If this doesn’t happen in the first hour, you don’t trade long.

Hope this helps.

wp01

wp01Participant

Master

Hi Paul,

Thank you for sharing your strategy. If i try it with 200k units on the 10m and 3min timeframe with 2 points spread i get much worse results than shown on your picture on the last page.

I would like to ask you if you changed maybe other settings in the code for the 10m. and the 3 min. Or did you used the exact same as you posted for both timeframes?

Thanks in advance for your reply.

PaulParticipant

Master

@wp01 Thanks for you feedback.

I use the same code posted above with maybe other settings. The spread needs mentioning.

It is possible an exit is not triggered during 9-17.30 which means in workdays the position is kept overnight. At Friday the position is always closed at 17.30

After 17.30, or before 09u trades can trigger an exit and then you talk about a higher spread.

In the code there’s also an exit-time. If you want to be sure you trade in a timeframe 9u-17.30 without a position overnight, just change closetime 240000 to 173000 or a smaller value.

a quick test i.e. 10 min timeframe 1 year

133 trades = 266 transactions of which are 13 with a spread of 2

133 trades = 266 transactions of which are 6 with a spread of 7

So generally speaking there is between a 5-10% chance you get a higher spread then used in the backtest.

But a test with spread 2 while the spread is 1 for the other 90-95% is not correct.

When trading the 3 minute timeframe, because of the smaller NOP value, there is a lower chance you trade in the more expensive times. But then there are more transactions.

It a choice. Want to be sure, then change the close-time. Results are still ok.

wp01Participant

Master

Thank you Paul for your reply.

I think i do not get it completely. I understand the part with the spreads, but when i change the time to 173000 for a year i get aound 100 trades.

When i change it back to 240000 it actualy does not change a thing.

wp01Participant

Master

Paul,

I adjested the settings which gives me more or less the same result of the backtests you posted.

Thanks.

PaulParticipant

Master

good! in the detailed rapport sort the trade by the number of bars. If you change to 17.30.00 then the maximum number of bars a trade is held in 10min timeframe is 51.

Thanks, Paul for the suppport. Are there any adjustment based on the vola needed ?

dont understand why it enters on that bar in my pic, why not earlier?

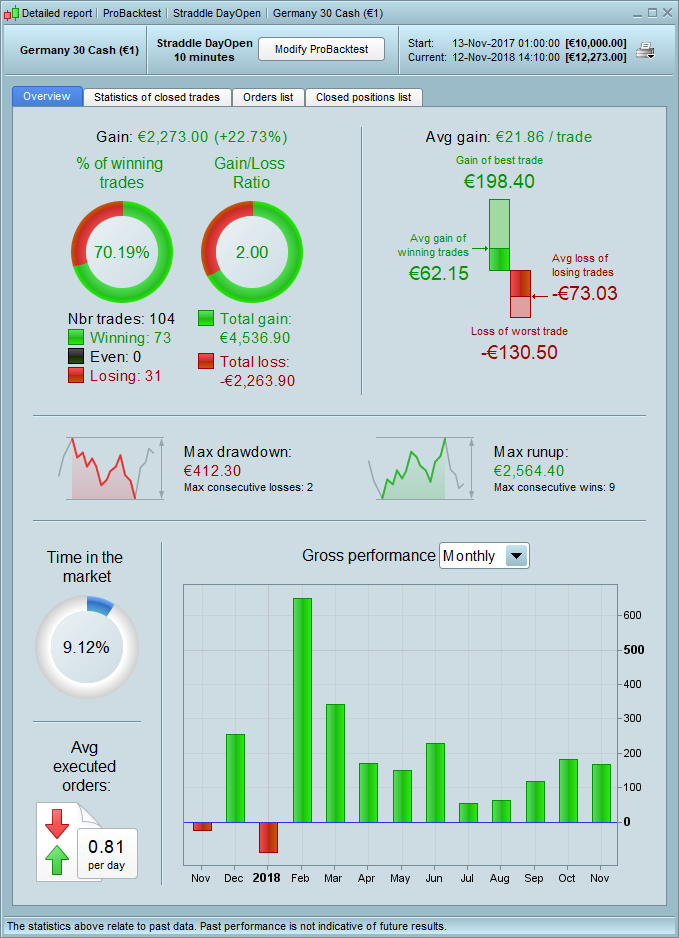

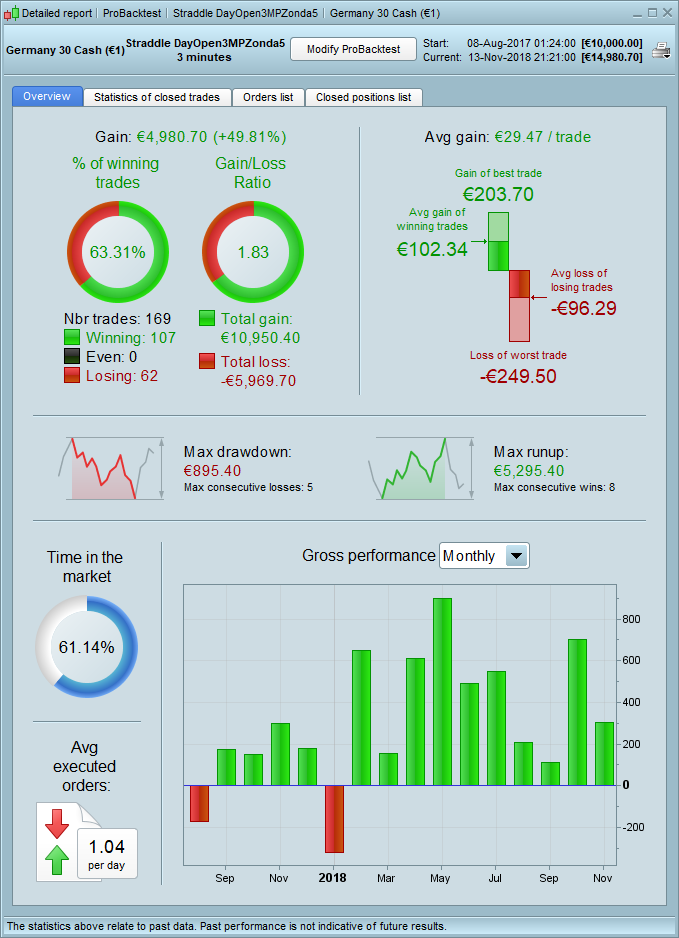

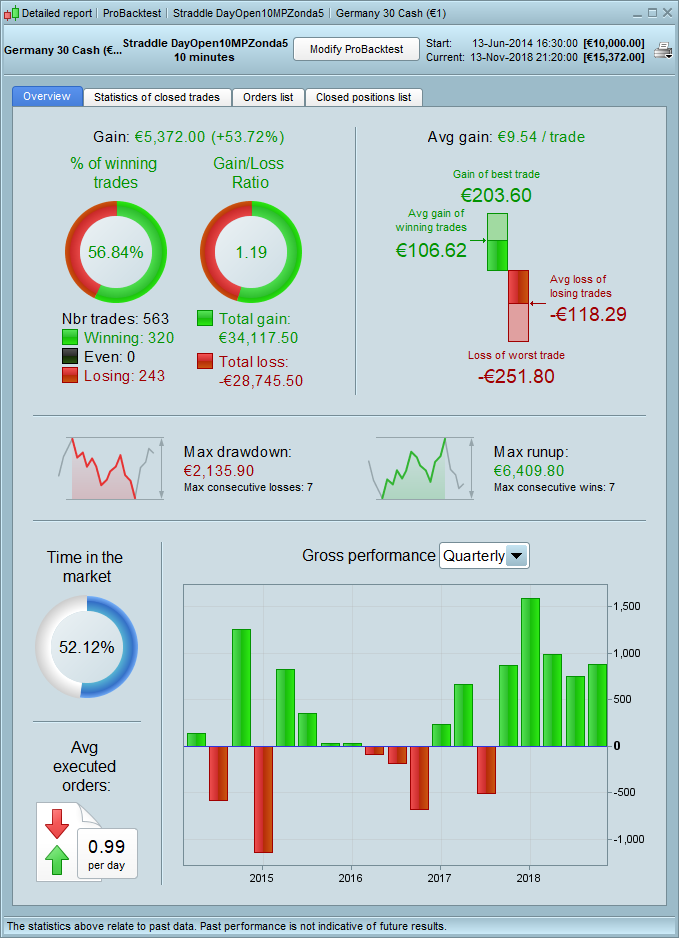

After fiddling around with all the different parameters, I found that the following settings gave the best results (Tested with 100k units & Spread = 1 on PRT platform via IG Markets):

3 Min: NOP (Long and Short) = 15 / Stop Loss = 1.90 / Every On/Off parameter set to zero except for Extratradecriteria

10 Min: NOP (Long and Short) = 15 / Stop Loss = 1.90 / Every On/Off parameter set to zero except for Extratradecriteria

15 Min: NOP (Long and Short) = 26 / Stop Loss = 1.45 / Every On/Off parameter set to zero except for Extratradecriteria

Since I only play with the NOP and Stop Loss settings, you get a strategy where the only reason why a running trade gets sold is because 1) it hits its Stop Loss level / 2) its friday 17:30 / 3) a trade in the opposite direction is triggerd.

Or said differently: you let your Long trade run until it’s time for a Short trade (and vice versa)

When I turn on the other parameters I don’t seem to be able get close to the results that you can find in the attachments.

I’m curious to see what the results are on a 200K unit timeframe, but I’m only able to test it with 100K units (guess this is a limitation of IG).

I’m curious to see what the results are on a 200K unit timeframe,

Thank you PZonda5 for your findings.

If you post the .itf files with the settings (you state above) already set up / included then I’m sure somebody might be kind enough (if we make it easy for them) to import the .itf files and press backtest so we can see the 200k equity curve and performance stats.

Who knows (through above) we may even get another recruit to Paul’s excellent strategy? 🙂

I can’t do 200k bars either, sorry.

wp01Participant

Master

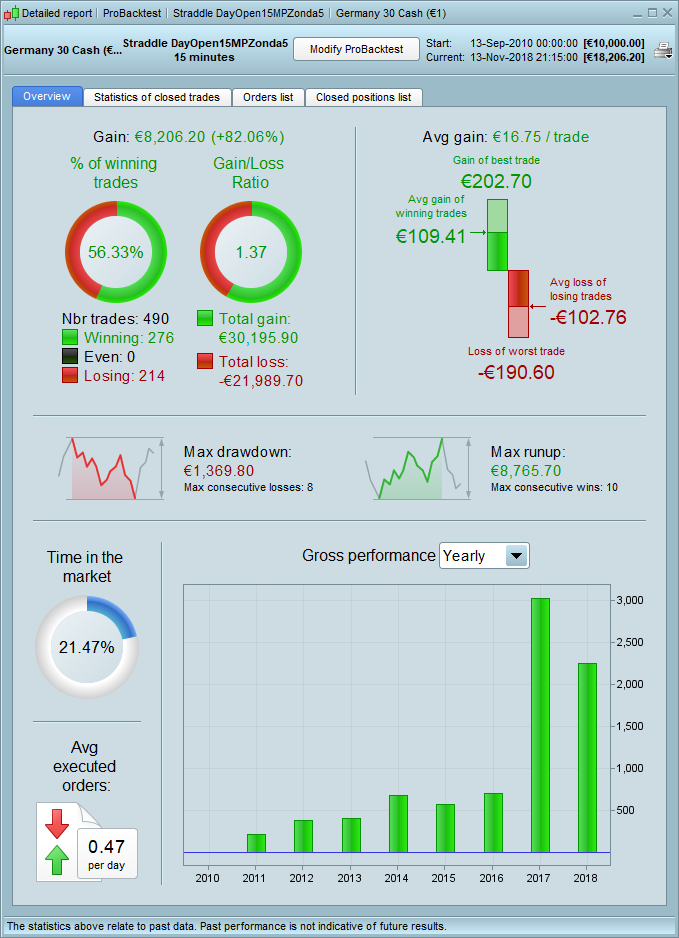

As attached with the settings from PZonda5 with 200K bars.

@wp01: I noticed your results are not quite the same as mine. For example: The profit for ‘february 2018 – 3 Min’ on my printscreen crosses the 1200 level, while on your printscreen it only crosses the 600 level. I guess this difference arises from the fact that I forgot to mention in my previous post that I had also turned off the Take Profit command.

I have added my ITF files to avoid any confusion about what I exactly did to get my results.

Could you run the 200K test again based on these files?(Thanks)

Hopefully this will result in monthly profit bars that look the same for you and me (and also shows a more profitable backtest)

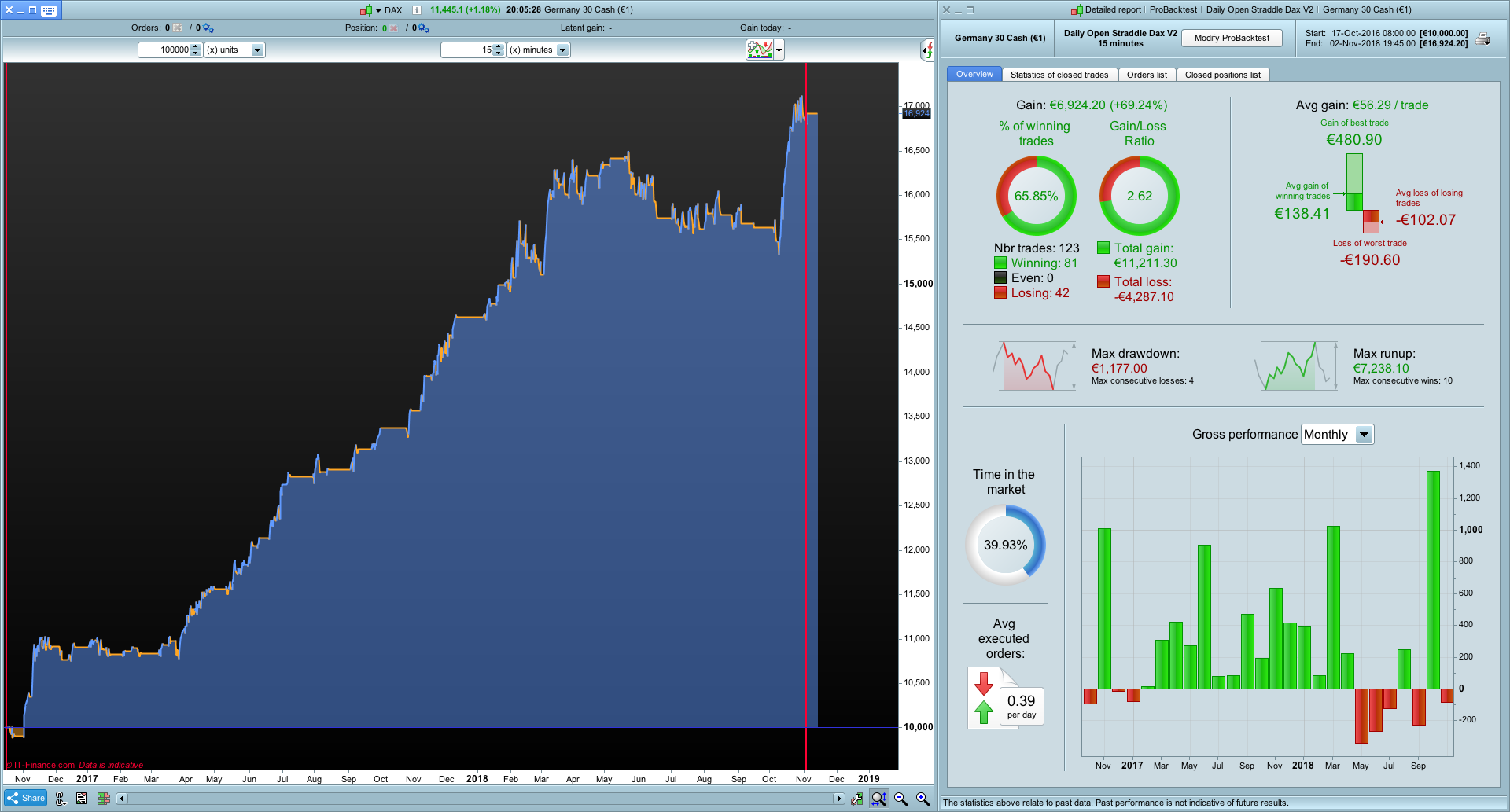

I have altered the 10 min. strategy a little bit to squeeze out some more profit.