Below the text I wrote in response to your first post in this topic, Roberto. But I did not post it because the explanation would be too complicated. In other words, I could not finish that text.

Point is : although the situation is challenged because putting an order at the wrong side of the price, what happens as result is no reason to just say “you should not do it”. As you will read below in brief – I do it all the time. But in controlled fashion.

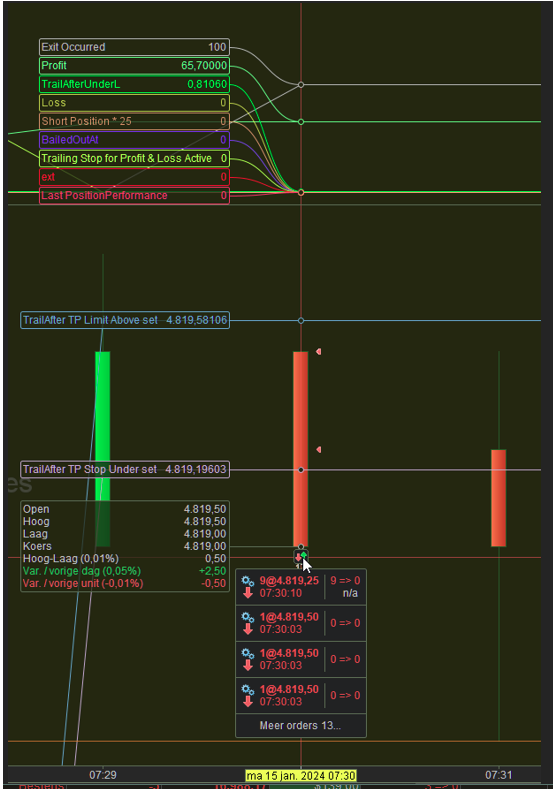

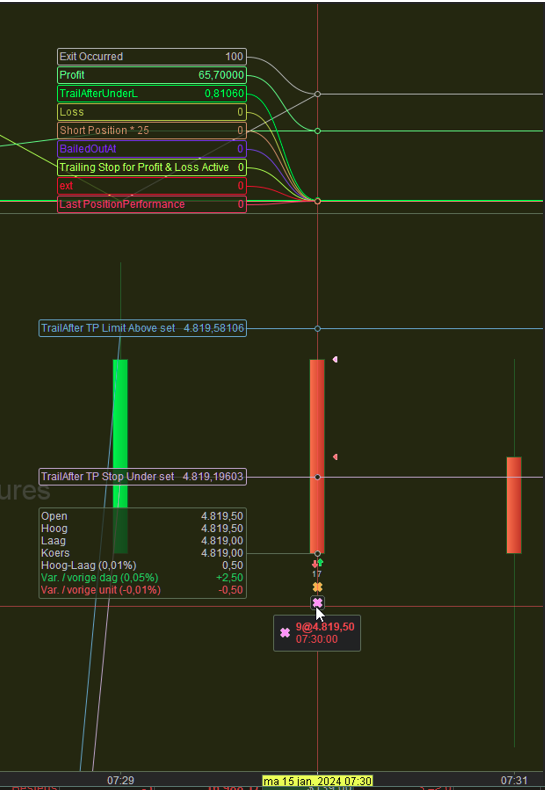

My text from yesterday summarized (in attempt), we can reason that the broker and PRT in combination enter an impossible situation, of which I could show longer essays of me and ProRealTime reasoning this out, BUT, this is about Live situations – not Backtest. The Live situations are about orders being filled partially, what PRT won’t anticipate – nothing does. But it is challenged for with two orders in the same bar (candle).

In my situation, which is related to Eurex and an extra layer of “Exchange” I can mimic the situation easily and it causes the system to go short while the strategy as such does not even Sell Short anywhere. It is about left overs of the order of a previous bar which could not complete, but which completes later. Even several bars later.

It is NOT the situation of nevtek, but think of the simple example of your Market order not filled (or partially filled), while your code simply says Sell at Market. It only requires a redundant registration of the system having done such, and the misery is there. There is no solution to this, other than an If Not OnMarket, in combination with resets I applied all over, because a few lines back I simply *know* I am out of position (while it appears I am not at all).

Again, this is not nevtek’s situation, but it is illustrative for what is challenged with the means of ordering you, nevtek, apply (which is odd to say the least, but which would be allowed anyway AND WHICH WOULD NOT BVE POSSIBLE WITH MANUAL TRADING – please think of this … your position would be gone because the (first) limit order at the wrong side of the price, would eliminate the position ride away).

The reason why I could not finish my initial response is because this cannot happen in Backtesting. Or at least not that I experienced. In Live, Yes (Demo, probably also not).

The problem – thus in the same realm – is more challenged for with IB than IG, because IB is more capable of not filling orders than IG. With IB it can therefore be so that pending order should be eliminated, but it is not because another pending order already was given to IB while the former is not cancelled (this is about the principle of pending orders in the first place). Thus mind you, the cancellation is an explicit activity, and nothing knows it should be done twice (it is an unexpected situation). It is is also about the informal OCO principle (one Cancels the Other) which is not formally present within AutoTrading, bit which works out 99 of 100 times as should anyway because you don’t pose a strange act to PRT and/or the broker. Anyway just envision :

You Exit a Long position at 08:10 and at 08:25 you suddenly have a Short position and you won’t know the heck where it came from. But it comes from the still pending Exit (which is a virtual Short against a Long and which is perfectly allowed as Exit means), while something else caused the position to Exit long gone, and the other Exit still pending because it was never cancelled. It is now only a matter of waiting until the price is touched (could be a year later, you never seeing the order, always pending).

All you can do against it is a. knowing about it and b. not challenge the situation. And b. is what is happening here, although I can’t see how precisely – and especially not with backtesting. But envisioning the Manual situation is sufficient – you won’t be able to have both orders in because the one at the wrong side of the price will exit the position. What’s left is the other Limit order and now thing how that one will or at least can unwind …

Peter

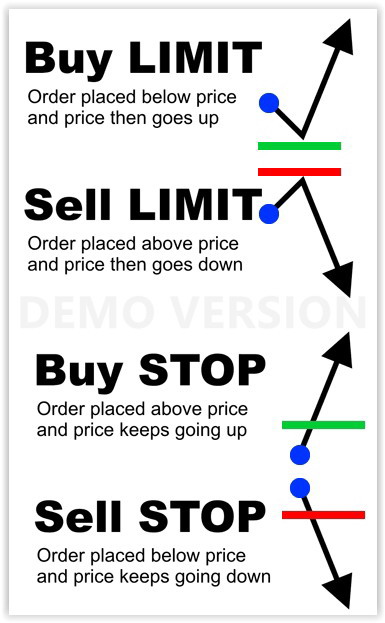

Nothing prevents from putting a limit at the wrong side of the price, so Roberto, if you think that causes the culprit within PRT, please elaborate ?

I am using Stops and Limits at the wrong side of the price all of the time, though it would be coincidental (I can’t always know where the price is going). Nothing goes wrong with that.

I have been staring at this too, and all I can come up with is that something goes wrong because of the usage of two the same type of pending orders at the same time. Point is, manually this is allowed, but, nobody will do that manually at the wrong side of the price (or else you lose your position right away because it becomes a Market order).

With the context of Roberto being correct but without him further explaining, I come to this reasoning (and could show examples from Live Autotrading if necessary) :

When two Limit (or two Stop) orders are given to the broker, there is no way for PRT to know that the one has been filled while the other is still not. Theoretically this can obviously be known, but it is an unexpected situation. Thus, when the one order is filled, the other is still pending and that can be filled too, later. Especially in the realm of one hour, this can easily happen. But when I buy 10 and 10 go out as well […]