Yes, phoentzs is right, you should use a Trailing Stop code snippet,you can search this forum or the Snippet Library.

Hi, murre87 I thought I would write you a tweaked BOT, modified around stop and entry to improve with a little 5 min direction to help!

Anyone feel free to use or improve, I am going to post this to the library

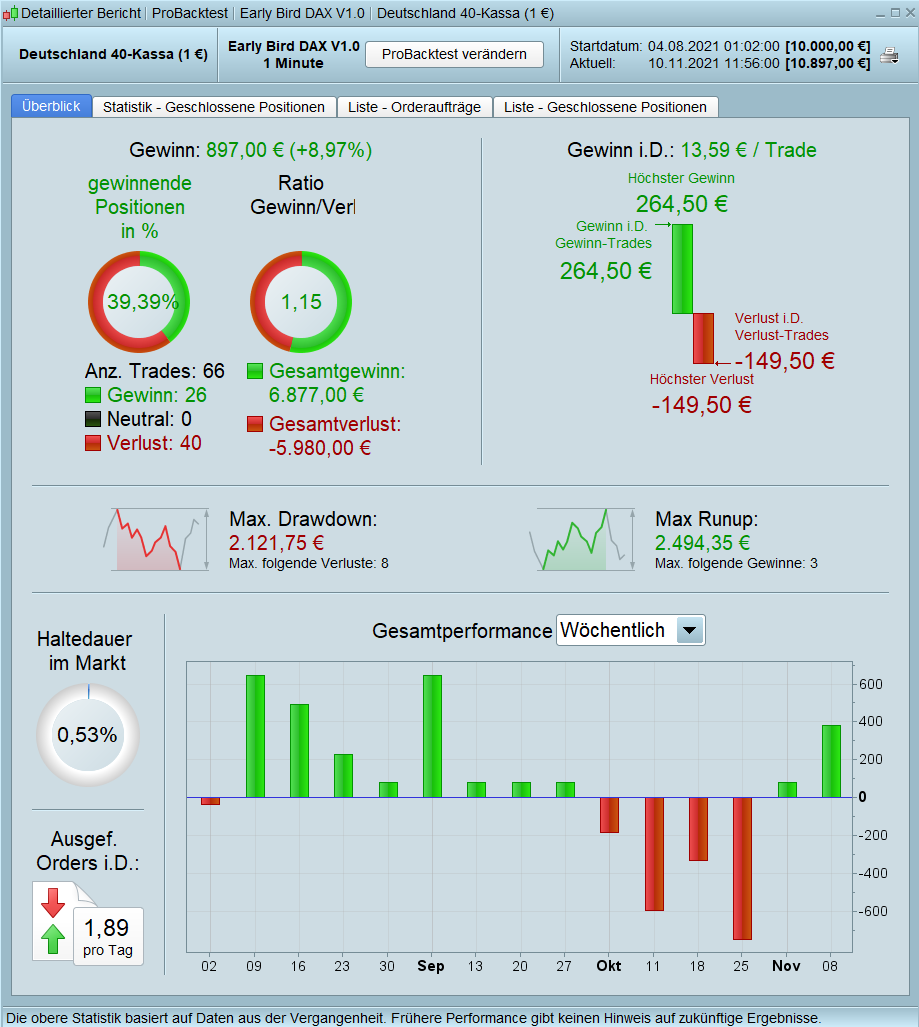

My results are a little bit diffrent. The spread in that program is wrong. Spread is 1.2 (for german user). But also with 1p spread, the results are diffrent.

smp

smpParticipant

Average

Thanks for the feedback, guys. I reviewed and adjusted the code to include a 1.2 spread (Thanks, VinzentVega for the reminder), so don’t add more spread when testing!

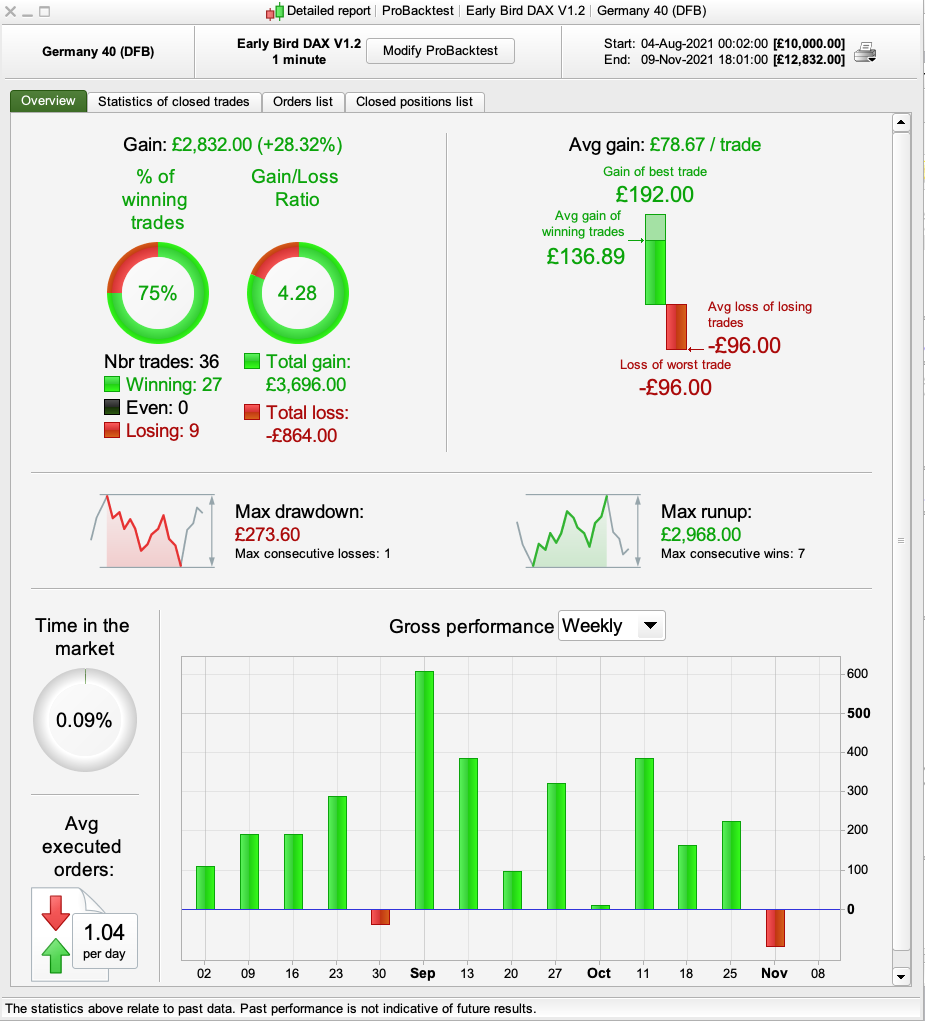

I have reduced the losses, improved the risk management.

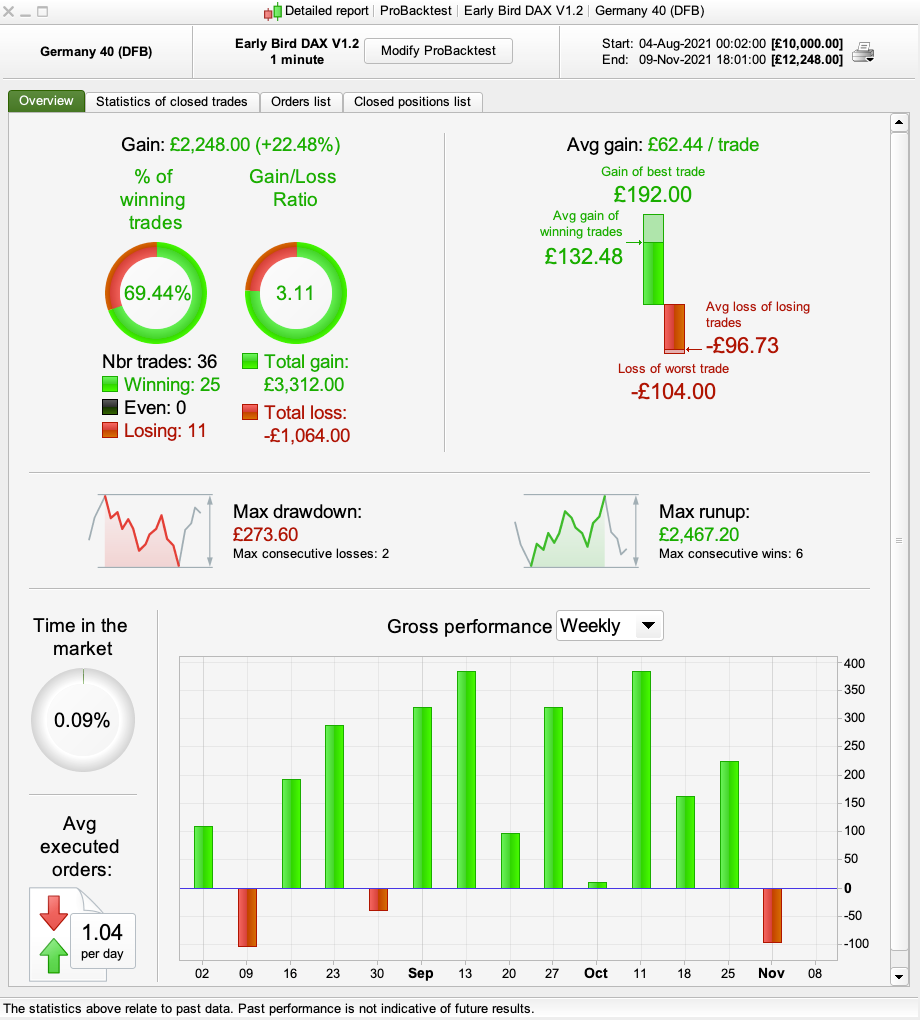

Again tested on V10.3 using 100,000 units

Test pic of tick by tick on and off

//Early Bird Breakout Strategy v1.0, updated with active risk code v1.2

//November 10th 2021

//www.harkoltd.com

//==========================================================

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Cancel all pending orders and close all positions at the "FLATAFTER" time

DEFPARAM FLATAFTER = 120000

// Prevents the system from placing new orders to enter the market or increase position size after the specified time

noEntryAfterTime = 110000

timeEnterAfter = time < noEntryAfterTime

//==========================================================

// Prevents the system from placing new orders on specified days of the week

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

//==========================================================

//Stake limited to 1.0% bank risk and topping at 1.7% return using active risk management code. Bank Risk Stop =1% and Target >2% (based on £10k account)

Stake=16

Spread=1.2

maxstop=6

Takeprofit=15

//==========================================================

//Limit to one trade

Trade = Barindex - TradeIndex(1) > IntradayBarIndex

//==========================================================

//Trading spread, entry of half spread

If Spread = 1.2 THEN

SpreadEntry = 0.6

ELSE

SpreadEntry = Spread

ENDIF

//==========================================================

//Active Risk management rules (To help the longs, shorts when wrong go straigh stop)

BreakevenAt =6

takeprofit =12

startBreakeven = takeprofit *(BreakevenAt/80)

PointsToKeep =4

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

IF ONMARKET AND close-tradeprice(1)>=startBreakeven THEN

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

IF breakevenLevel>0.5 THEN

SELL AT breakevenLevel STOP

ENDIF

//==========================================================

//Leading breakout direction

Timeframe (5 MINUTE)

EMA1 = ExponentialAverage[22](close)

EMA2 = ExponentialAverage[3](close)

IF EMA1 > EMA2 AND EMA1 > EMA1[1] AND EMA2 > EMA2[1] THEN

LongNotShort = 1

ENDIF

IF EMA1 < EMA2 AND EMA1 < EMA1[1] AND EMA2 < EMA2[1] THEN

LongNotShort = 0

ENDIF

IF abs(EMA1 - EMA2) < 1 THEN

LongNotShort = 0.5

ENDIF

//==========================================================

//Entry timeframe

Timeframe (1 minute)

OpenUK = 080000

Start = time >=OpenUK

if openTime = 070000 then

myHighest = high

myLowest = low

endif

if openTime >= 070000 and openTime <=075955 then

myHighest = max (myHighest,high)

myLowest = min (myLowest,low)

endif

//==========================================================

If Start and Trade and timeEnterAfter and not daysForbiddenEntry then

// Conditions to enter long positions (0.5pt break)

IF LongNotShort = 1 THEN

BuyPrice = myHighest + SpreadEntry + 0.6

BUY stake PERPOINT AT BuyPrice stop

ENDIF

// Conditions to enter short positions

IF LongNotShort = 0 THEN

SellPrice = myLowest - SpreadEntry - 0.6

SELLSHORT stake PERPOINT AT SellPrice stop

ENDIF

SET STOP LOSS Maxstop

SET TARGET pPROFIT TakeProfit

endif

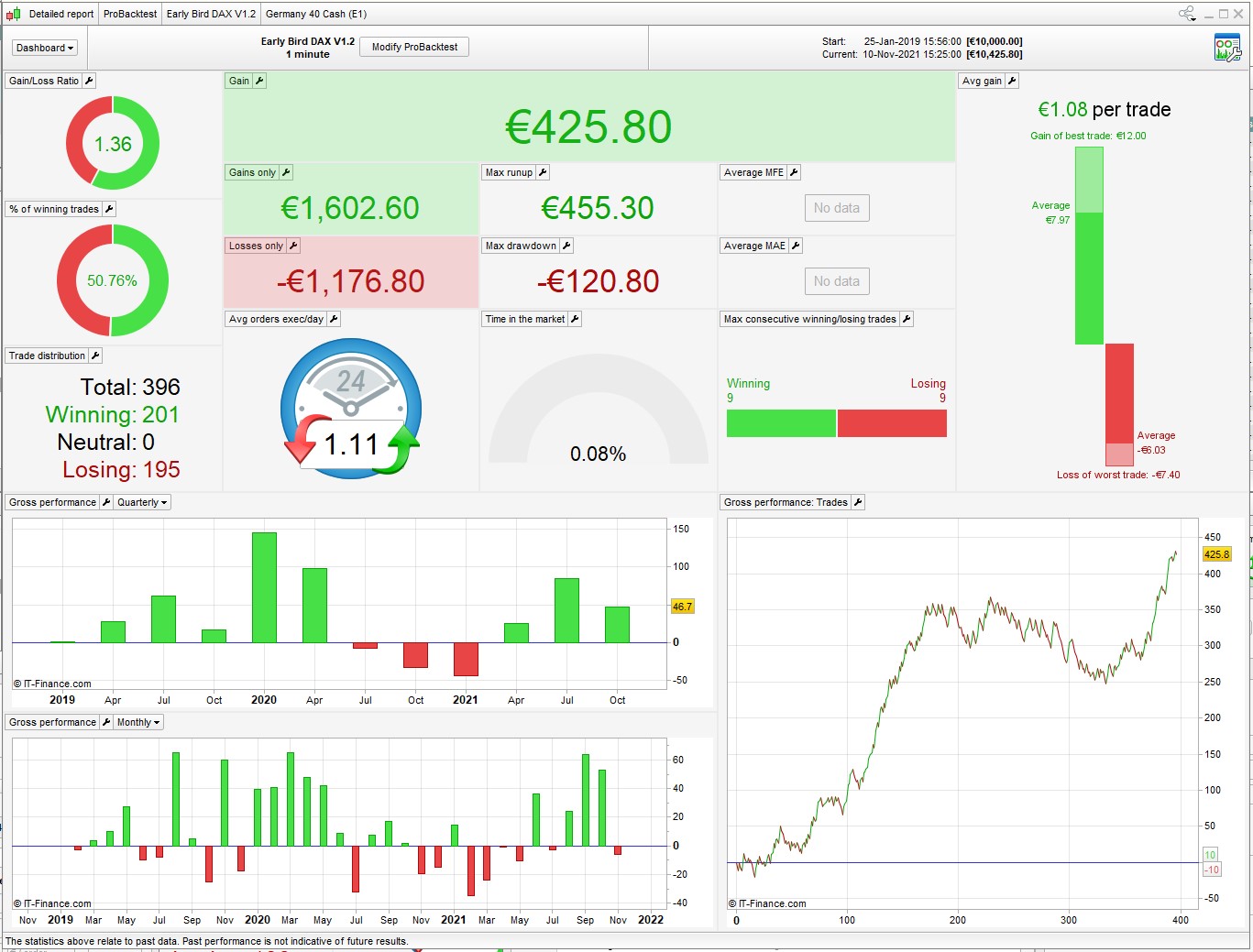

1m bar backtest, stake = 1 (for easier comparison to other algos)

TBT, no additional spread

€ 1 per trade profit on average?

smpParticipant

Average

I don’t see that as relevant at all. Risk and therefore should be based on the bank size and not on pip size. My bench for testing is £10k bank size and my base risk is 1% of the bank.

The 1% is a constant.

Pip size is not

I don’t see that as relevant at all. Risk and therefore should be based on the bank size and not on pip size. My bench for testing is £10k bank size and my base risk is 1% of the bank. The 1% is a constant.

Yes, but for backtesting and for the comparability its allays better to use 1 pip/point. I can immediately see how many points the setup is generating, and don´t have to convert. Its more usefull for all viewers

I meant something else. You invest 10 € and with a 50% hit rate you get 11 € … so one euro profit per trade. that’s not much when you consider that this is a back test and the slippage is on top of that.

smpParticipant

Average

That’s not what the back says. Plus your hypothesis is flawed, sorry. It’s all-around risk management and ROI.

The correct backtesting identifies over a 69% hit rate with a return of over 1:1.7

If I gave someone £1 and they gave me back £2.7 I would take that all day (don’t forget the £1 you risk you don’t spend

The strategy is from someone else, it did not work and so I wrote a programme to deliver one that would work and based on the loose requirement – let’s not forget this.

Personally, my BOTs deliver… worst case 20% *12 trades per year (88% win rate) to high frequently BOTs delivering 45% per year. Mixing these bots (over 12 active BOTs these do very nicely)

This early bird bot potentially trades 144 per year (roughly) with a potential outturn of 80%+ On a £10k account that’s £8k or £55 per trade! No matter what you are doing

Can you trade manually, and consistently with these ratios, most cannot!

smpParticipant

Average

VinzentVega 2 minutes does look good 👍🏻

I never looked at that time frame

smpParticipant

Average

2 mins, interesting. Can you post your code as MTF does not support 2 mins

It would be interesting to see what you have done?

2 mins, interesting. Can you post your code as MTF does not support 2 mins

It would be interesting to see what you have done?

Pls find attached the file.

smpParticipant

Average

Thanks for the file. The strategy actually loses money!

Also, it’s a completely different strategy! The strategy is a break put of 8:00, not 9 am! We are discussing the 8:00 breakout using the 7am to 8am timeframe, and not the 8am to 9am as you have! I thought something was wrong.! Thanks for sharing anyway.

I wrote a 9am breakout also like yours and has 100% trading record at 5 trades per 3-month cycle, happy to stick with this

Thanks for sharing though

Eric

EricParticipant

Master

For those that are not afraid of slippage, take a look at Hang Seng at the open

Did some breakouts testing on that beast, but gave it up

Too brutal for me