Here is a strategy copyed from here and adjusted for the brentcrude oil E1 5 min chart.

Any sugestions or coments are welcome.

Have not started it live since I whant to test it in V.10.3 PRT for IG users:)

reb

rebParticipant

Master

Hi Kenneth

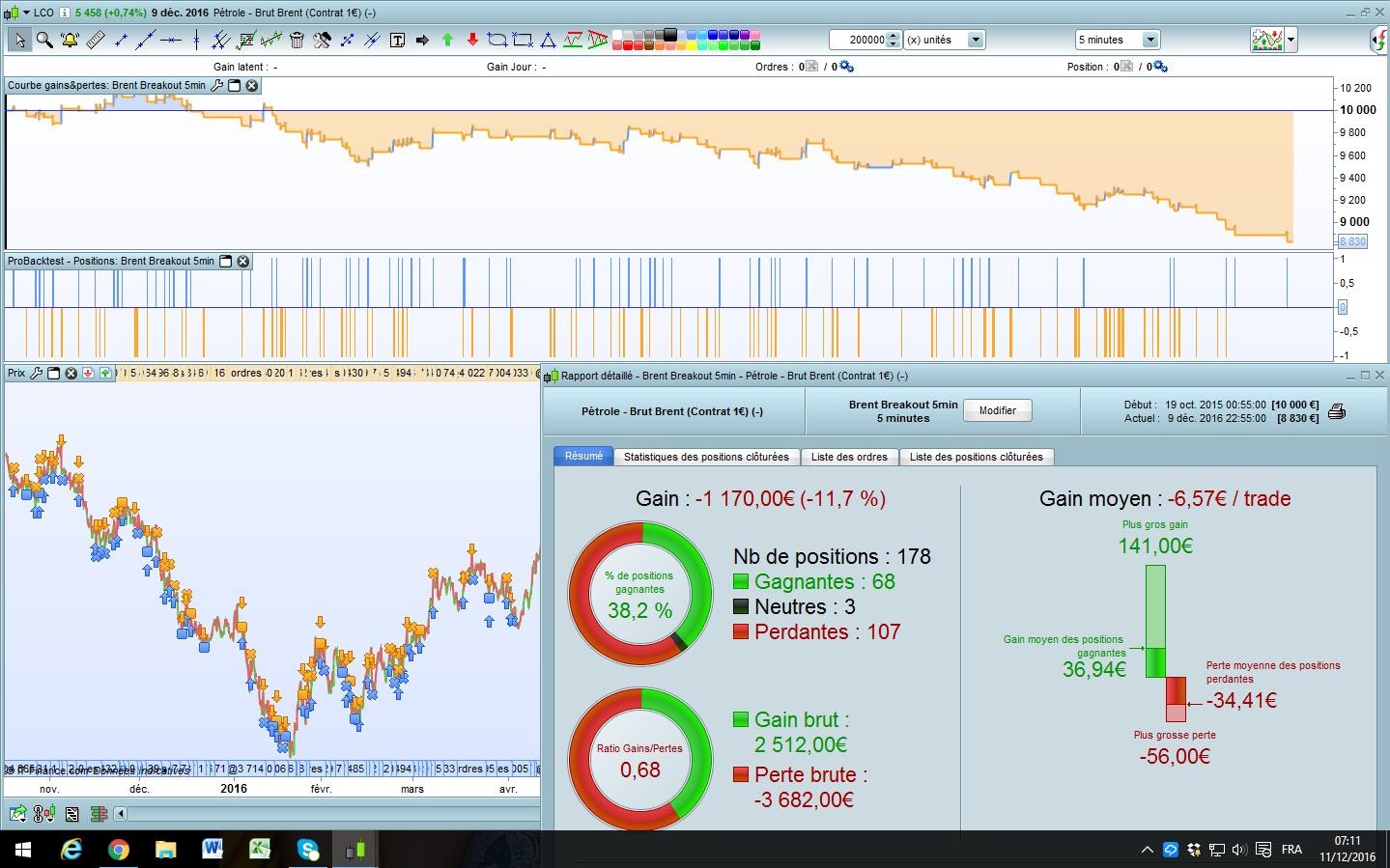

I uploaded the itf file then launched the strategy in 5 min on the LCO Crude Brent

I don’t have the same results as you, did I do something wrong ?

Reb

rebParticipant

Master

I checked a bit the code and I see some differences between the comments and the code :

// The position is closed at 9:45 p.m., local market time (France).

DEFPARAM FlatAfter = 225500

// No new position is taken after the candlestick that closes 5:15 p.m.

LimitEntryTime = 154500//154500

// The market analysis strats at the 15-minute candlestick which closes at 9:30 a.m.

StartTime = 151500

As french I have the time zone as you, why did did you mention 214500as comment and 225500 in your code ?

Could it be the reason of the big difference in term of results ?

Didn’t test it myself, but check out spread maybe..

rebParticipant

Master

I use a spread of 3 like IG does

Hi.

I dont kow why results are different. Is probably somtheing with the timeframe to do.

I use 5 min chart 100 000units witch is max history for me.

Spread is 3.

STrategy starts 1515 and can not trade after 1545. (Norway local time) this has to be adjusted to your time Reb. Were are you from?

Position can be open to 21.45 or later, you can choose.

It also has Nicolas mef stop code witch I know works good in live trading(no bugs)

rebParticipant

Master

hi Kenneth

As french, I think we have the same time zone

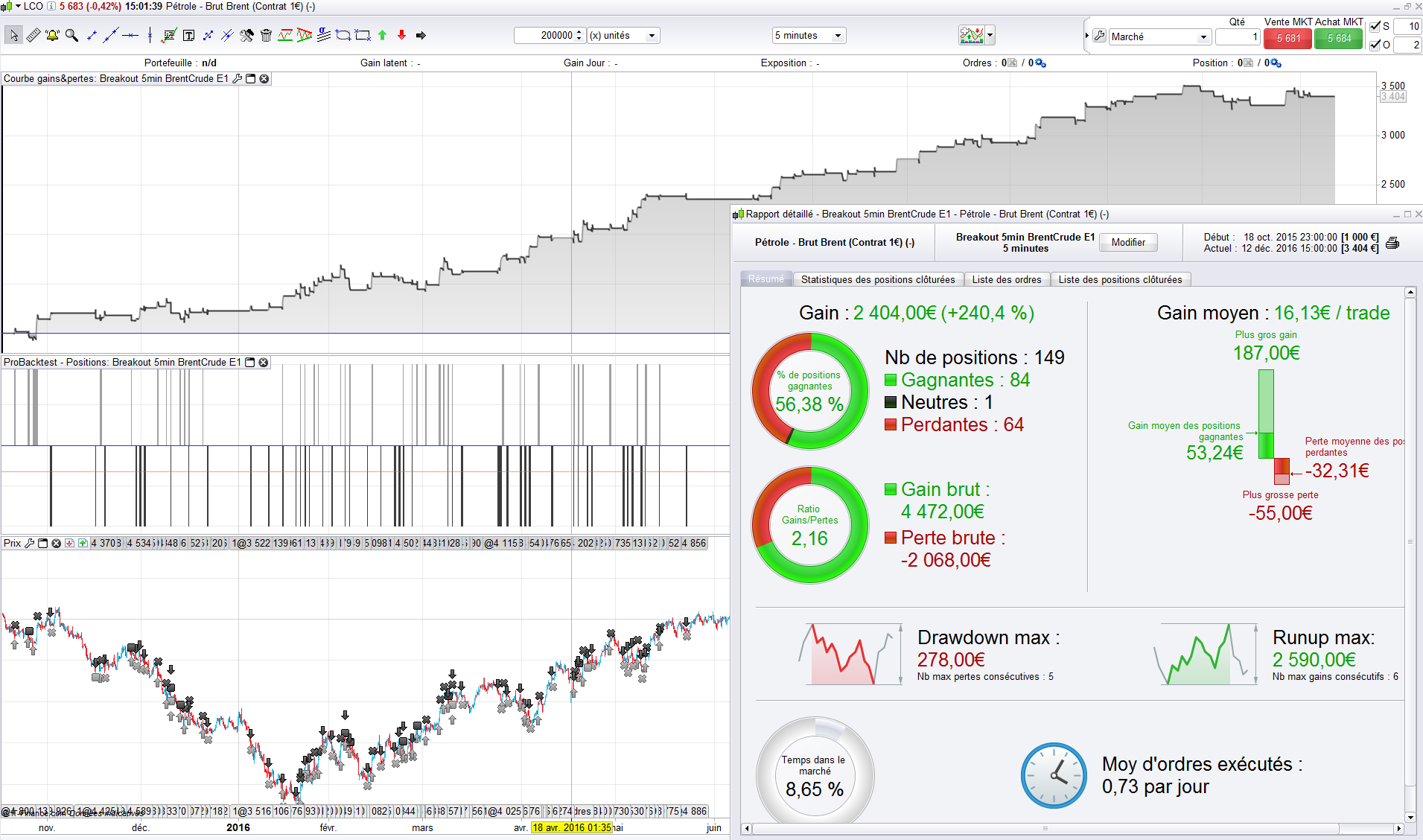

Then I am sorry and dont.know why its a diffrence. I use mini brent crude e1 lco. I WILL check out the itf. File with a friends acc. Later and see if its same for him.

Get the same results as Kenneth has. Picture attached.

rebParticipant

Master

ok

I don’t understand, I tested this strat on PRT complete and PRT premium

I have the same results as I posted

Where is the issue ?

LCO 5min, spread 3, no modification on the code (pnly uploaded)

Alco

AlcoParticipant

Senior

Hi reb,

I also had a different result on default settings.

Try this code. I changed time and it did work for me.

Let me know if it changed for you.

Alco

// We don't load data before the start of the system.

// As a result, if the system is started in the afternoon,

// it will wait until the next day before placing any orders.

DEFPARAM PreLoadBars = 0

// The position is closed at 9:45 p.m., local market time (France).

DEFPARAM FlatAfter = 235500

// No new position is taken after the candlestick that closes 5:15 p.m.

LimitEntryTime = 164500//154500

// The market analysis strats at the 15-minute candlestick which closes at 9:30 a.m.

StartTime = 161500

// Some holidays such as the 24th and 31st of December are excluded

IF (Month = 5 AND Day = 1) OR (Month = 12 AND (Day = 24 OR Day = 25 OR Day = 26 OR Day = 30 OR Day =31)) THEN

TradingDay = 0

ELSE

TradingDay = 1

ENDIF

// Variables which can be adapted based on your preferences

PositionSize = 1

AmplitudeMax = 80//58//80

AmplitudeMin = 13//11//12

OrderDistance = 4//4

MinPercent = 35//30

// We initialize this variable once at the beginning of the trading system.

ONCE StartTradingDay = -1

// The variables which can change during the day are initialized

// at the beginning of each new trading day.

IF (Time <= StartTime AND StartTradingDay <> 0) OR IntradayBarIndex = 0 THEN

BuyLevel = 0

SellLevel = 0

BuyPosition = 0

SellPosition = 0

StartTradingDay = 0

ELSIF Time >= StartTime AND StartTradingDay = 0 AND TradingDay = 1 THEN

// We store the index of the first bar of the trading day

IndexStartDay = IntradayBarIndex

StartTradingDay = 1

ELSIF StartTradingDay = 1 AND Time <= LimitEntryTime THEN

// For each trading day, the highest and lowest price of the instrument

// are recorded every 15 minutes since StartTime

// until the buy and sell levels can be defined

IF BuyLevel = 0 OR SellLevel = 0 THEN

UpperLevel = Highest[IntradayBarIndex - IndexStartDay + 1](High)

LowerLevel = Lowest [IntradayBarIndex - IndexStartDay + 1](Low)

// Calculation of the difference between the highest

// and lowest price of the instrument since StartTime

DayDistance = UpperLevel - LowerLevel

// Calculation of the minimum distance between the upper level and lower level

// to consider a breakout of the upper or lower level to be significant

MinDistance = DayDistance * MinPercent / 100

// Calculation of the buy and sell levels for the day if the conditions are met

IF DayDistance <= AmplitudeMax THEN

IF SellLevel = 0 AND (Close - LowerLevel) >= MinDistance THEN

SellLevel = LowerLevel + OrderDistance

ENDIF

IF BuyLevel = 0 AND (UpperLevel - Close) >= MinDistance THEN

BuyLevel = UpperLevel - OrderDistance

ENDIF

ENDIF

ENDIF

// Creation of buy and sell short orders for the day if the conditions are met

IF SellLevel > 0 AND BuyLevel > 0 AND (BuyLevel - SellLevel) >= AmplitudeMin THEN

IF BuyPosition = 0 THEN

IF LongOnMarket THEN

BuyPosition = 1

ELSE

BUY PositionSize CONTRACT AT BuyLevel STOP

ENDIF

ENDIF

IF SellPosition = 0 THEN

IF ShortOnMarket THEN

SellPosition = 1

ELSE

SELLSHORT PositionSize CONTRACT AT SellLevel STOP

ENDIF

ENDIF

ENDIF

ENDIF

// Definition of the conditions to exit the market when a

// buying or selling position is open

//////////////////////////////////////////////////////////////////////////

////Trailing stop logikk

//////////////////////////////////////////////////////////////////////////

//trailing stop

trailingstop = 45//15

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//////////////////////////////////////////////////////////////

///Trailing stop logikk

//////////////////////////////////////////////////////////////

SET STOP ploss 55//55

AlcoParticipant

Senior

My results are even better than Nicolas. But it has 6 ”0” bars. I don’t know if this is bad?

@Alco

Did you add spread? 0 bars trades are not a big problem if they are losers!

AlcoParticipant

Senior

Ok great! Spread = 3. I didn’t changed it from the original code.