Hello everyone,

Does anyone use strategy in real?

Should it regularly optimize the strategy?

Thank you

Hello @bertholomeo

Live results since 22 july 2017

I am also running Reiner modified version with % target and losses.

Started later, both have some drawdown at the same time

Thank you Yannick, The results are good since the real is equal to the backtest. I started for a few days with the groose loss. Pity. I will continue the strategy.

i use two version in live

reiner : brent breakout m5

and an other: brent crude 2.1

the result is not the same than yours, wath version do you use?

reb

rebParticipant

Master

Hello guys,

How can you compare apples and oranges ?

You have not the same period : from 7/22 or from 7/30

I am quite sure that you don’t use the same amount of contracts

rebParticipant

Master

For the 1st time today in the strat, I see a discrepancy between live and backtest.

It s due to a difference between PRT and IG my broker. PRT uses integer numbers but IG does decimals (at the same time IG qUotes 5210.4 and PRT 5210)

The long order opened at 5157 yesterday was closed by PRT at 02:00 this morning due to stop loss

Because of decimal figures, IG didn’t close the trade (for less than 0.5pts) which is still open with a gain of 50 pts

@Reiner

Are you running your version live right now?

I stopped this one from live trading (my personal choice) because even with my modification of the time stop it did have too bad risk/reward ratio. But somebody else is maybe fine with riding the waves. 🙂

Oh sorry, I mixed up strategies. That was Francescos Hammer negated I added the time stop but I stopped this too for same reason.

Hi Kenneth,

sorry but I’am a little confuse , I think the first strategy published in the first page , seems great…

Do you use it in real ? Do you have more backtest about this strategy ?

Thanks

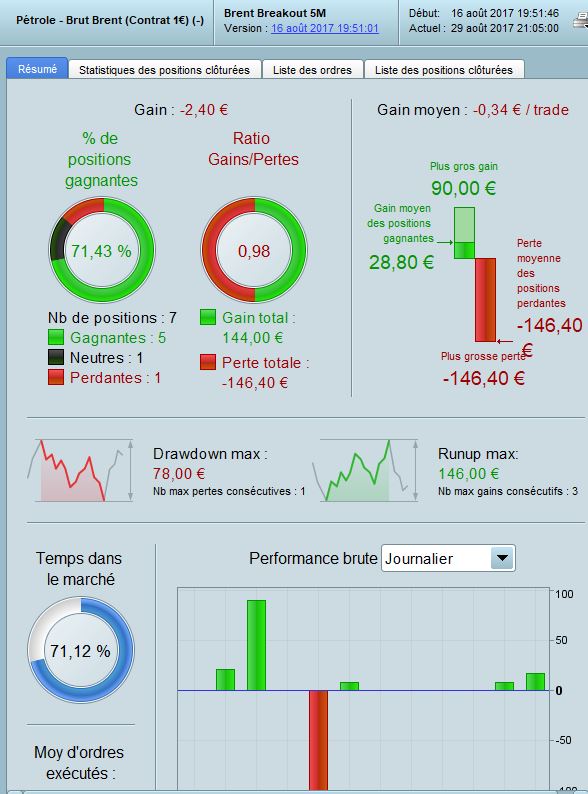

here is my liveacc, for my brent crude strategy.

start 25 july. minicontracts brent crude E1

I’m a bit late to this party but late is better than never!

From a quick test and look at the code it seems to be a little fitted. Different variables for long and short on a commodity that has equal chance of going up or down based on supply and demand seems a little fitted. Also the fact that it has made a loss on my backtest for the last two months rings alarm bells. Also I’m not too certain of the benefit of having the TakeProfit and StopLoss based on a percentage of price. Why increase TP and SL just because the commodity price is high and lower them just because the price is low?

Hopefully I’m wrong and it will work into the future and this is just a down period at the moment but I’m not planning on running it live until more forward testing is done.

Just my 2 pence worth.

@ Vonasi – Let me put forward my 1 pence (:-)) worth on the issue of using % based stops/limits. I actually prefer using them to straight points based ones for the following reasons :

- In reality every investment is ultimately assessed on a % return basis – ie if I told someone I made £100 profit last month and same again this month, they would assume that the trading performance was the same each month. But then if I told them I used £100 capital the first month but £10,000 the next to generate those profits, then the return performance is viewed much differently – 100% vs 1%

- Using absolute points levels can create issues in backtesting over the longer term especially when the underlying instruments’ value has fluctuated dramatically. For eg if you used a 60pt target level in the DAX, 10 yrs ago it would have been difficult to hit this level within a day as that would be a 1-2% range, whereas today 60-100 pt (0.5 – 0.8%) intraday moves in that index are very common. But if you actually look at the % moves in the index over the 10yrs rather than the daily points one (eg using a log chart) then it paints a very different volatility picture to a pure price chart. Therefore trying to optimise using points rather than % limits would create very different results that are less realistic because you are trying to “fit” one fixed number across a longer timeframe.

- Markets generally tend to move in % based increments because thats how investment managers, funds, traders, HFT algos etc view and therefore trade their returns (even margin requirements are stated in % terms). For eg. in equity indices the index move is determined by the underlying constituents’ % mkt cap moves (ie value) and not their absolute price moves (the Dow is an exception) so therefore it makes more sense to use this format when testing out strategies. In some markets it’s less relevant but even in parts of FX trading, correlation and carry trade strategies are always evaluated on a % basis.

So broadly speaking, if you are backtesting a strategy on a shorter term then it may be ok to use points rather than % as in that short a term, the instrument value and inherent volatility may be fairly similar over that period. But If you are looking at a longer period I would prefer to code %’s so as to perform a more robust backtest that could be more likely to accurately reflect future movements and performance.

This is just my humble opinion and a few thoughts for others who may find it useful, I’m by no means suggesting it’s the only way to go as it depends upon the strategy and your personal preference, I myself use some points based systems where relevant. In fact, in this case where we are limited by the short time range data set available, I would guess that optimising either on a % or points basis would probably make little difference to the overall results.

Thanks for your reply Manel. You raise some interesting points. I’m still not sure of the merits of % over fixed points as I would have thought that if % worked over all prices then big market players would be holding out for bigger price movements as price increased before closing trades and so average true range would increase as price increased so as to match this – but it doesn’t. I would like to have TP and SL levels linked to average true range rather than a % of price but I am coming to believe that ATR is like all averages either too laggy or too fast depending upon what period you use. The best I have come up with is an ATR based on the lowest of two ATR periods – a fast one and a slow one – but is is a test in progress. Maybe a % level based on a lowest of two ATR’s is the next step!

Thanks for your thoughts.

You guys ære way more advanced than me. But i use my own code with pip target and stop. I can only show my live acc. And works ok for now. See pic.