I was just working on a Bot on AUD/USD and the spread currently is 4.1 which did little for my equity curve ;). I found the site below … shows avarage spread as 1.4.

Anybody know of a better / similar source of data on average spreads for the various individual markets / instruments? Useful to know value to enter as spread in the ‘Bot spread-box’ for backtesting.

http://www.myfxbook.com/forex-broker-spreads/IG-AUDUSD-real-spread/1768,11

GraHal

I’ve gone through my live trades VS backtest and the results show the average is around the 1.4 spread mark for AUDUSD on IG.

NOTE: IG claims an AUDUSD average spread of 0.75 https://www.ig.com/au/forex but I don’t get 0.75 when I compare the backtest to the live trades.

Although there can be 1 – 3 milliseconds difference of time when the trade is executed on the live account (eg. 14:00:03) and the backtest (eg. 14:00:00) takes the price at the exact time/hour so this could be the margin of difference?

When I looked at myfxbook again it showed a spread average of 0.6 – 0.8 however IG is no longer listed there as an option but GraHal’s link still works.

I built a Google Spreadsheet web scraper a few weeks ago to store the data from IG’s live website but its not that reliable.

Eric

EricParticipant

Master

NOTE: IG claims an AUDUSD average spread of 0.75 https://www.ig.com/au/forex but I don’t get 0.75 when I compare the backtest to the live trades.

Although there can be 1 – 3 milliseconds difference of time when the trade is executed on the live account (eg. 14:00:03) and the backtest (eg. 14:00:00) takes the price at the exact time/hour so this could be the margin of difference?

When I looked at myfxbook again it showed a spread average of 0.6 – 0.8 however IG is no longer listed there as an option but GraHal’s link still works.

I built a Google Spreadsheet web scraper a few weeks ago to store the data from IG’s live website but its not that reliable.

“3 Average spread (Monday 00:00 – Friday 22:00 GMT) for the twelve weeks ending 7 October 2016”

EricParticipant

Master

“* Average spread (Monday 00:00 – Friday 22:00 GMT) for the 12 weeks ending 24 February 2017.”

this one also old

higher volatility today?

https://www.ig.com/uk/help-and-support/spread-betting-and-cfds/fees-and-charges/what-are-igs-forex-spread-bet-product-details

EricParticipant

Master

BC

BCParticipant

Master

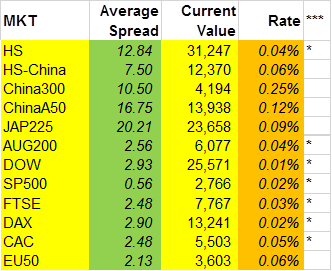

I calculated the average spread for most major market on Jan 2018.

I have re-done the actual vs backtest on a limited data set and it looks like AUDUSD is 0.8 – 1. There’s one nasty outlier of 7.

My method was to run the backtest with 0 spread and then compare the difference with the live result. I made this spreadsheet here. If you think there’s a better method please let me know or feel free to improve what I’ve done.

@Bin do you mind sharing your method?

I just thought about my spreadsheet and I think I initially had the logic incorrect for the SELL (exit), which would now mean that outlier of 7 is actually favourable if that’s the case this probably should treated as an error. Furthermore I really cannot imagine IG be so generous to offer a better spread than 0.6 so maybe this method is unreliable.

Now I thought of a very easy way to record the spread. Run 2 systems in the demo account for each side long and short and then see what the price difference is for each time trade.

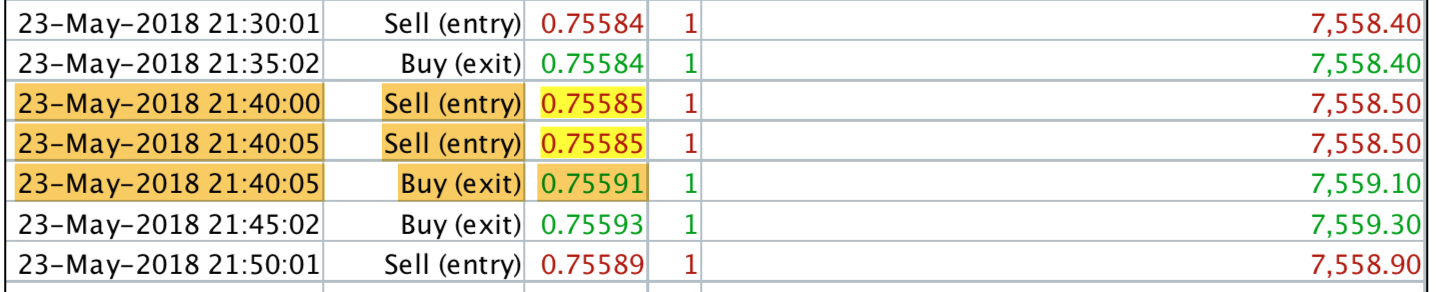

I found some time to start looking into the spreads again. While building my database and checking for errors in the data I found this error. The system is SELLING to OPEN and then BUYING to CLOSE.

You will see 3 trades executed at ~ 23-May-2018 21:40:0# which is impossible. As per the sequence it should have been 1 SELL to OPEN only.

So this is raw and really we should not trade the FX market open which adds some outliers but for completeness – here’s a data table – scroll down to 22:00-23:00 rollover time :).

SUMMARY

AUDUSD

m5 spreads

02-May-2018

to

25-May-2018

Min

-4.00000

Max

110.00000

Mean

8.10101

Count < Mean

3217

81.2%

Count > Mean

743

18.8%

StDev

6.18285

Wow very enlightening David, thank you for sharing the full spreadsheet with us.

I see Pareto 80/20 shows up (18.8% > Mean).

More coffee and toast and another study of the spreadsheet! 🙂

Hi All,

I just noticed this thread about spreads, and yet I have never heard anyone mention here that on PRT when you are back-testing you do not have the ability to input different spreads for different times of the day. For example with IG, the biggest broker around (and the other brokers), on the DAX (and all the instruments) you have 3 spreads typically throughout the day, a spread of 1 pt at 8am – 4.30 pm (UK time) and then 2pts and then 5 pts after 9pm. If whilst BT’ing you cannot input this info all you get is inaccurate BT results which is frankly shocking. Yes you could put in an ‘average’ spread but again this is actually totally wrong – as when in the real market the spread is not at that ‘average’ ! You therefore get incorrect BT data, by inputting an ‘average’ figure.

Oscar / UK

If whilst BT’ing you cannot input this info all you get is inaccurate BT results which is frankly shocking.

I agree … please put it forward to PRT as a suggestion that we need the option to input 3 different spreads for 3 different time bands in the Backtesting parameters.

With end of day strategies the varying spread becomes less critical in backtesting as it is pretty steady at midnight for most of the popular markets. The down side is that it is also pretty big.

Varying spread is one of the many reasons why forward testing is so critical before going live. If a good backtest at varying fixed spreads works well for a strategy then it might be fairly robust. Forward testing with live varying spreads is the finally quality check.