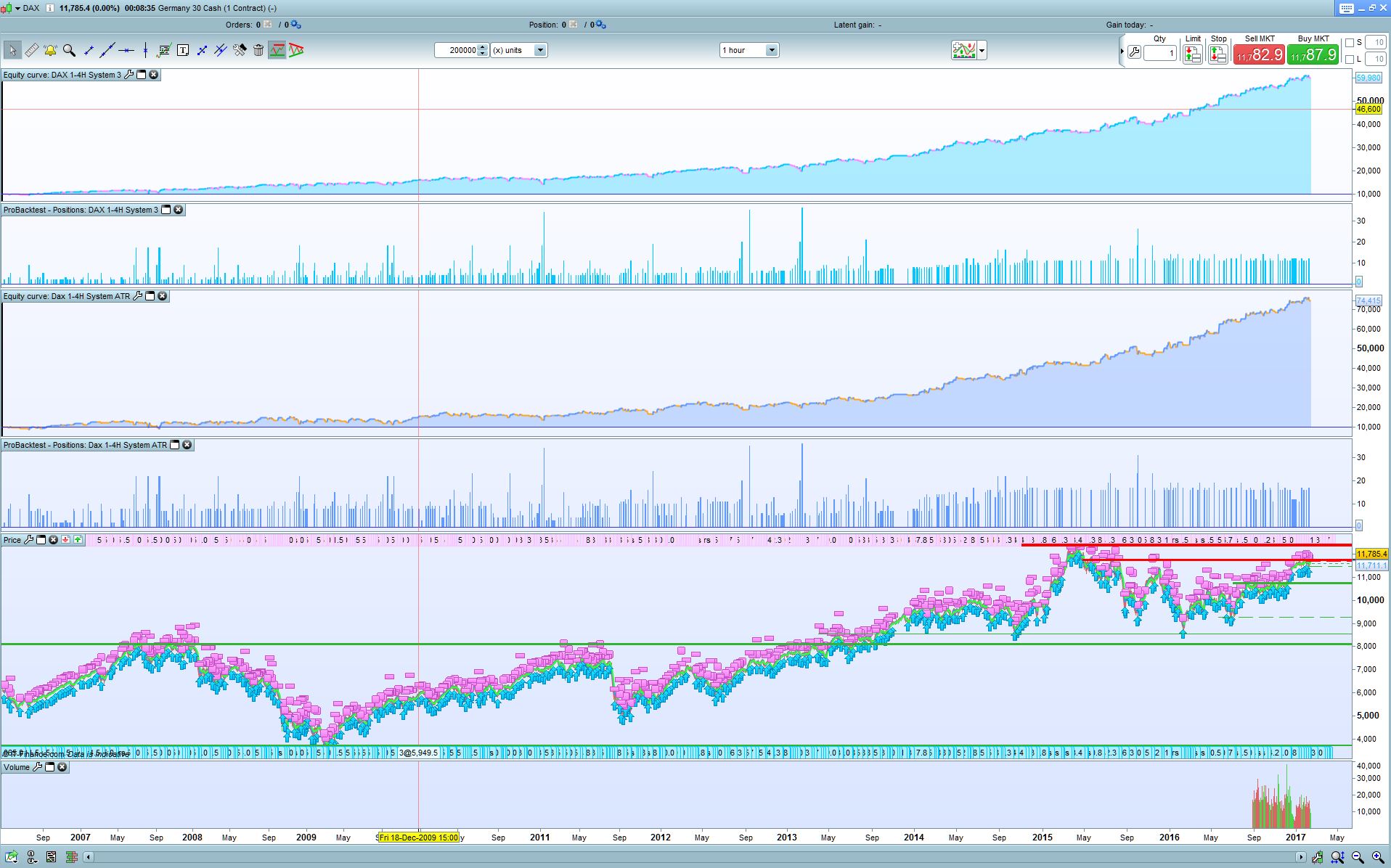

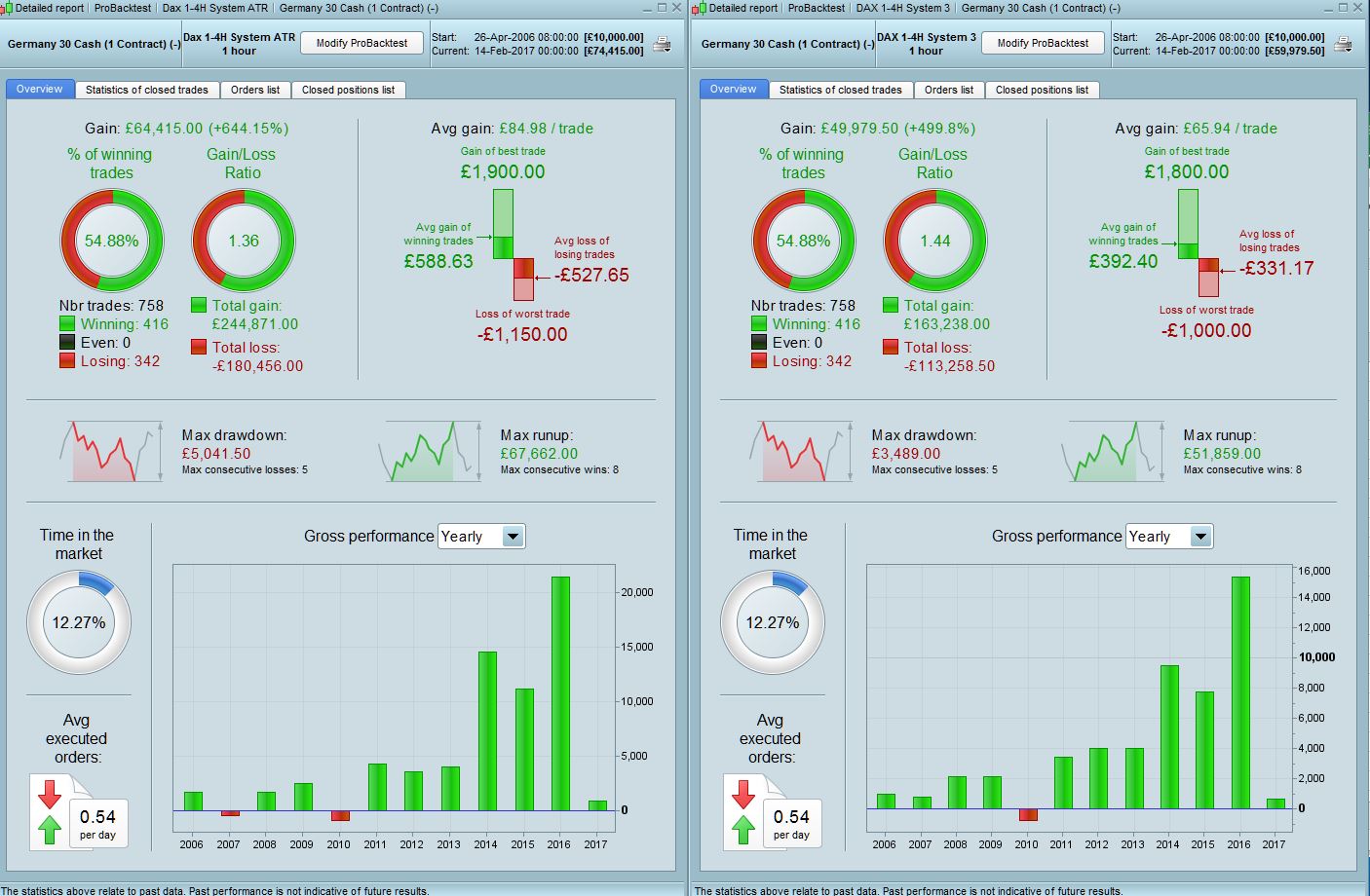

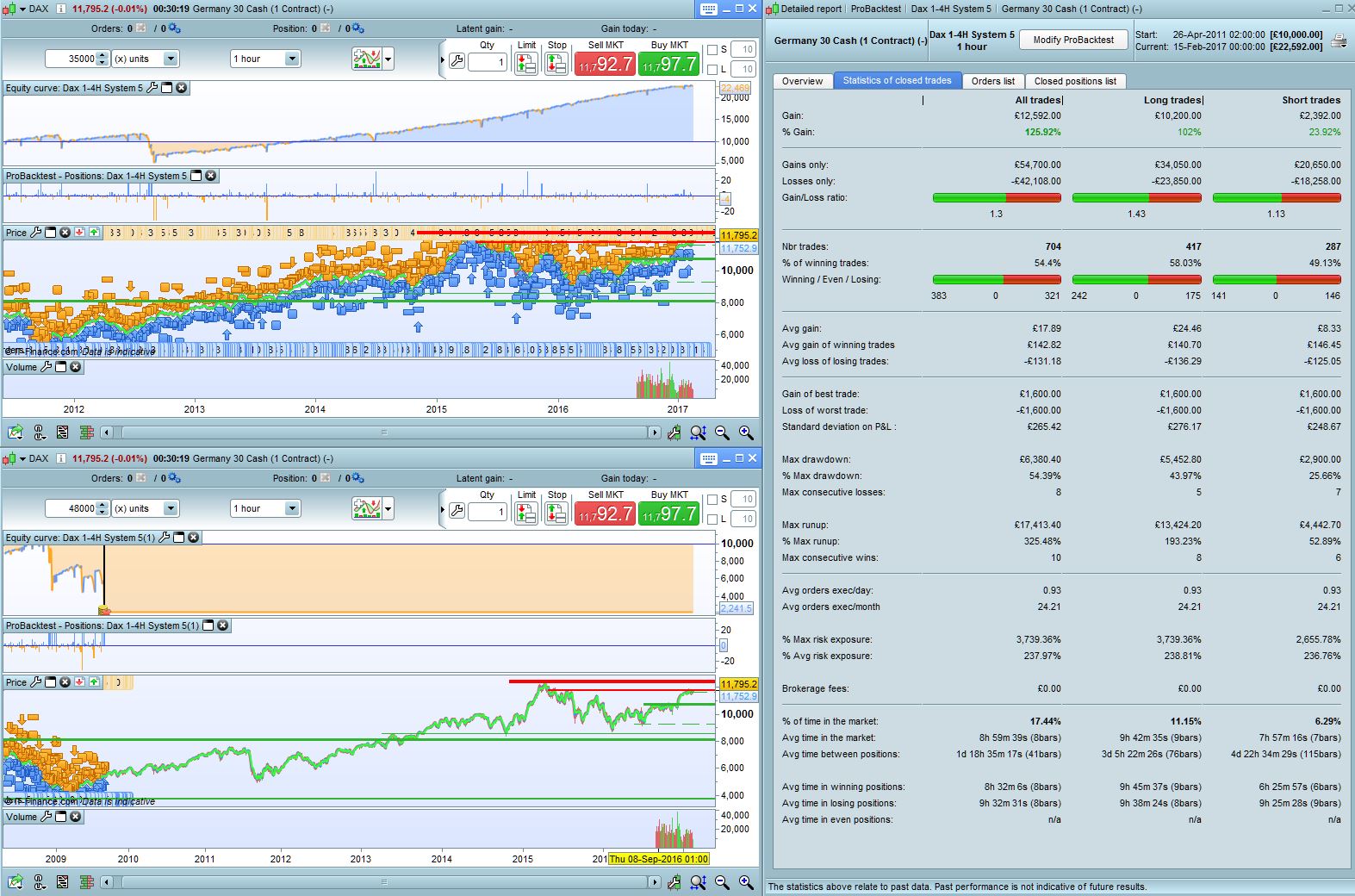

ATR system looks pretty good I’d say. At least there is some decent growth in the first 5 years as opposed to none with most other systems. Draw is is only 10% so not high at all. 20% of trades and profits are zero bar which is again in line with expectations.

Comparison with system 3 below as well. They are pretty much identical results for the first 6yrs and then ATR starts outperforming gradually over the longer term.

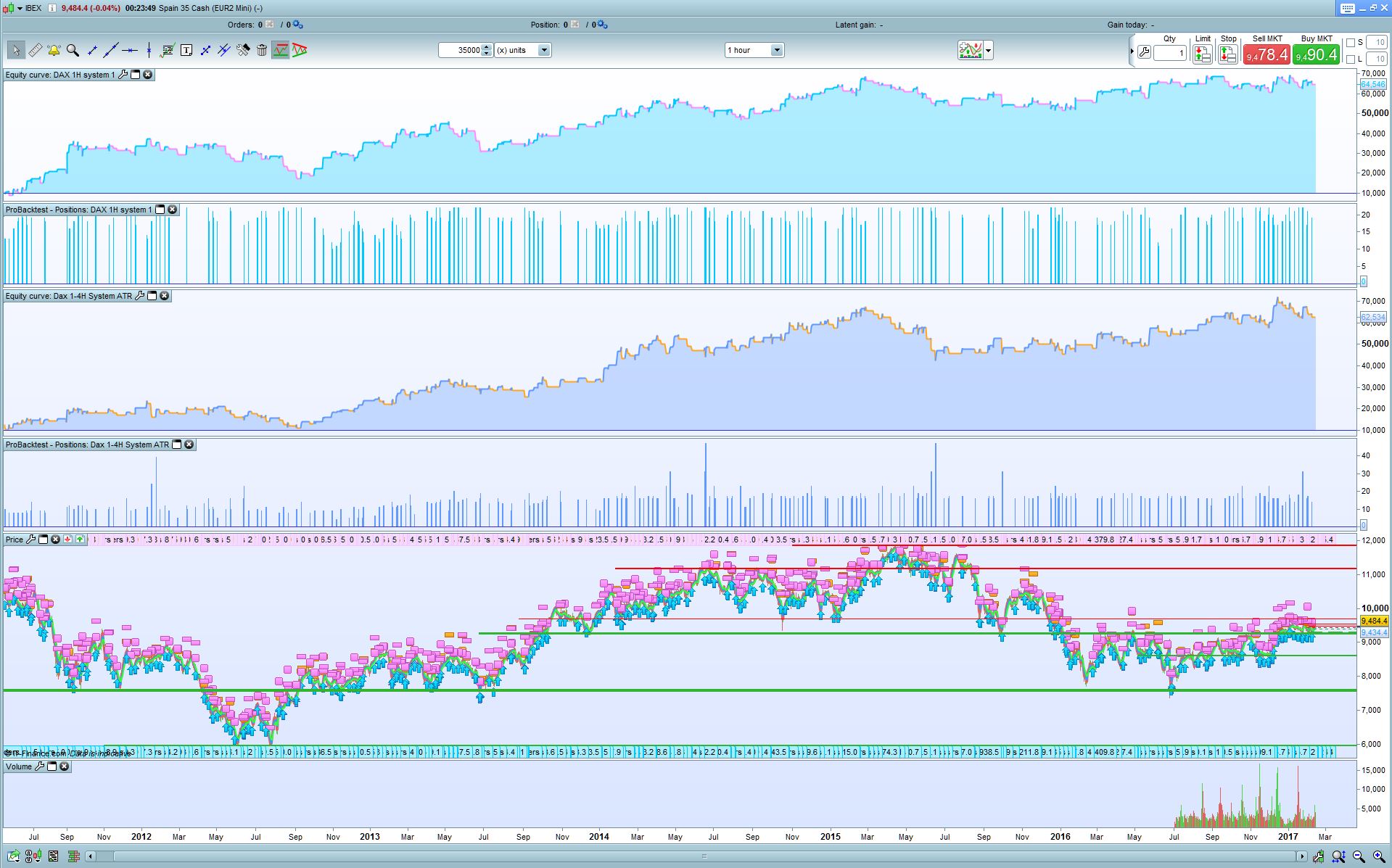

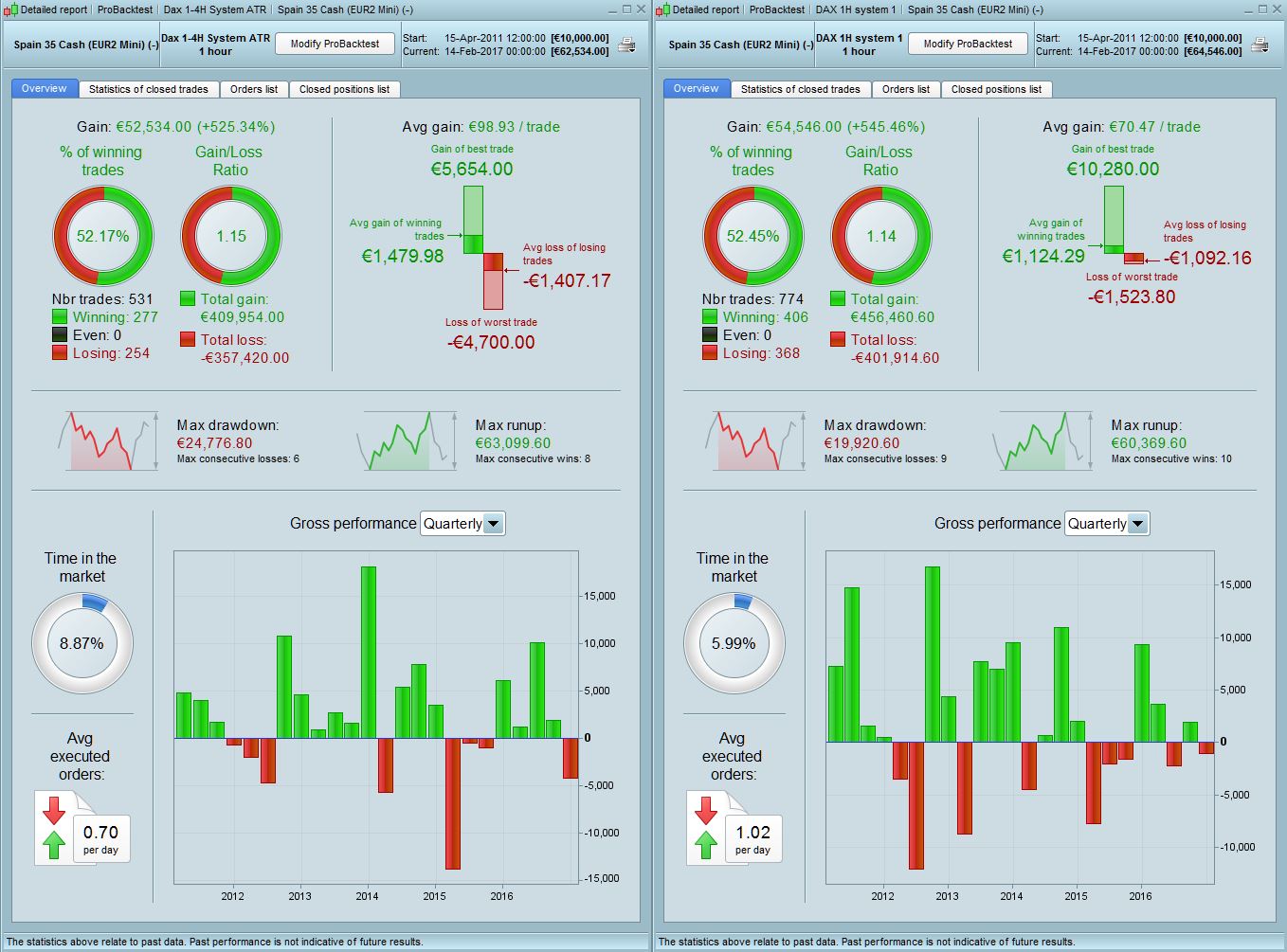

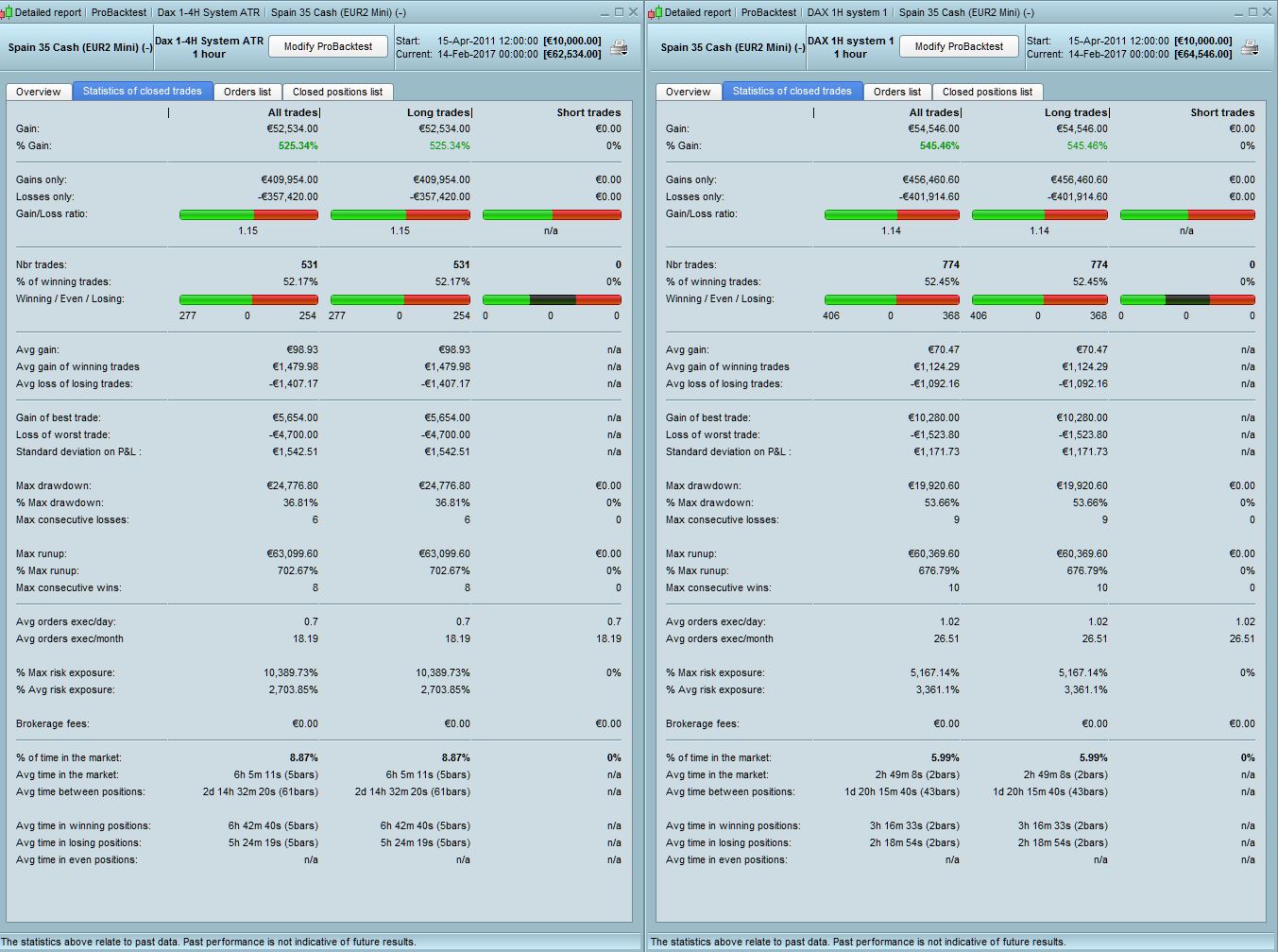

And here are the Ibex results – ATR vs System 1. See earlier post for first round results for this index. But in this revised ATR system the risk has certainly been reduced. The draw is now 37% instead of 54% and the no of consecutive losses has dropped to 6 from 9. It makes 30% less trades for the same total gain i.e is more efficient. Only slight negative is that the biggest single loss is 3x greater. But overall the system has definitely made a positive difference to the performance and risk taken.

I have tried to include as a condition of purchase that ATR is above 20. And on the other hand the condition that ATR is below 20, to see if in the DAX it is significant that this indicator signals us or not. I see that both this below and above 20, the system is a winner, I do not think that in this case ATR is a determining factor in which the operation wins or loses. Adding condition c111 or c1111

screenshot 1

If d1 And t1 and c1 and c11 and c12 and c13 and c111 THEN

screenshot 2

If d1 And t1 and c1 and c11 and c12 and c13 and c1111 THEN

Interesting. So I guess it’s as we thought, low vol conditions are not great for producing trade entry conditions and/or profits as the results show.

No trades in Live or backtesting for the DAX or CAC systems today by the way. Should hopefully get a trade next Tuesday that gives us some live data to compare.

According to the conditions it has to operate from Tuesday at 9am until Thursday at 6pm. That is, tonight or tomorrow could also operate. Yes, it is more beneficial with great volume, but I see that with little volume does not come out negative, there are no losses, I see that these last years has increased the volume as we said. But I do not see that there is a negative result in any case. I will try with some other condition to see if I can refine it, but I certainly see good expectations for this robot in both dax and cac. You could look to see 60 put take to see if they change much the results and get a little more in each operation

Yes, I agree, that’s my conclusion as well. The way it is works is pretty good for now (hence my decision to take it into live). The main thing is that in unprofitable or slow periods it is not losing any big money and that is what our testing over the last few days has shown. So I’m happy with that. This means like I said earlier, you just have to be patient and implement this over a long time horizon. We could try alternate periods but I don’t want to overfit. Maybe we could look at that at a later stage when the system is performing well.

Re. your comment – Are you sure about more entry trades possible tom/thurs ? I interpret the code as saying that entry is only on Day 2 and exit can be anytime up until Day 4/5 5pm.

If d1 And t1 and c1 and c11 and c12 and c13 THEN

if not onmarket then

IF c1 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize*2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize = 1

if ordersize<1 then

ordersize=1

ENDIF

endif

buy ordersize+n Contract At Market

Endif

If d2 and t2 then

sell at market

endif

endif

endif

Yes, sorry, you’re right, I think I’ve confused myself with code, I’ll try without limiting the trading day to see it coming out

Ok, no problem. I did some testing early on to change the days to other days of the week to see what the effect was but apart from a couple of cases in some instruments, for some reason Tuesday looked like being the best day for this system.

So you are still using the same profit and loss (fixed values, not dynamic ones) and you added ATR as a condition to enter market?

to try…

DEFPARAM CumulateOrders = true

once ordersize=1

// Conditions

MA1 = Average [1]

MA2 = Average [2]

c1 = Ma1>MA2

t1 = time >= 090000

t2 = time = 180000

d1 = dayofweek = 2

d2 = dayofweek = 4

if strategyprofit<=30000 then

if ordersize>16 then

ordersize=16

endif

endif

if strategyprofit>30000 then

if ordersize>64 then

ordersize=64

endif

endif

// buy

indicator13 = MACD[12,26,9](close)

c13 = (indicator13 < 30)

indicator11 = ExponentialAverage[20](close)

c11 = (close >= indicator11)

indicator1 = MACDline[12,26,9](close)

indicator2 = ExponentialAverage[12](indicator1)

c12 = (indicator1 > indicator2)

//sell

indicator1111 = ExponentialAverage[20](close)

c1111 = (close <= indicator1111)

indicator111 = MACDline[12,26,9](close)

indicator2111 = ExponentialAverage[9](indicator111)

c1211 = (indicator111 < indicator2111)

if not onmarket then

If d1 And t1 and c1 and c11 and c12 and c13 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize*2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize = 1

if ordersize<1 then

ordersize=1

ENDIF

endif

buy ordersize Contract At Market

Endif

If d1 And t1 and c1 and c1111 and c1211 THEN

IF PositionPerf(1) < 0 THEN

OrderSize = OrderSize*2

if ordersize<1 then

ordersize=1

ENDIF

ELSIF PositionPerf(1) > 0 THEN

OrderSize = 1

if ordersize<1 then

ordersize=1

ENDIF

endif

sellshort ordersize Contract At Market

Endif

endif

If d2 and t2 then

exitshort at market

endif

Set Stop Ploss 50 // from Trade

Set Target PProfit 50 // from Trade

@ Nicolas – Yes in respect to results shown in #25026 above, there is a fixed 50pt stop and limit and ATR has to be >20 for entry trade condition to be satisfied.

Results are not good. System only works from mid 2012 but that too with a 54% draw. Prior to that it’s a 100% loss in 08.

With regards to the ATR I suppose there may be some value in testing to see if linking the take profit/loss to the ATR produces better results. Maybe it could improve performance in the earlier years as well where the signal is correct but the take profits are too high.

Manel – I think the results are great! The only problem is that it only works in bulltrend. You have to be convinced that the market is in a bulltrend if you´re going to start it.