Wow, thanks very much, that was quick @Vonasi!

The indicator signals may be poor but it is referring to whether you’re a buyer or seller (writer) of Puts and Calls. It maybe that using a 50% mean value IVR/IVP ratio and expecting meaningful signals maybe naive given the way option premiums can explode and remain high for extended periods of time. (Pls refer to £/$ weekly Call options that have increased by 100’s of percent and remained high since the 11th October due to a possible Brexit deal).

When IVR / IVP < 50, buy call or put options (because premiums are cheap and should rise to the mean value). When IVR / IVP > 50 sell (write) call or put options (because premiums are expensive and should reduce so you can buy them back cheap and close the position for a profit).

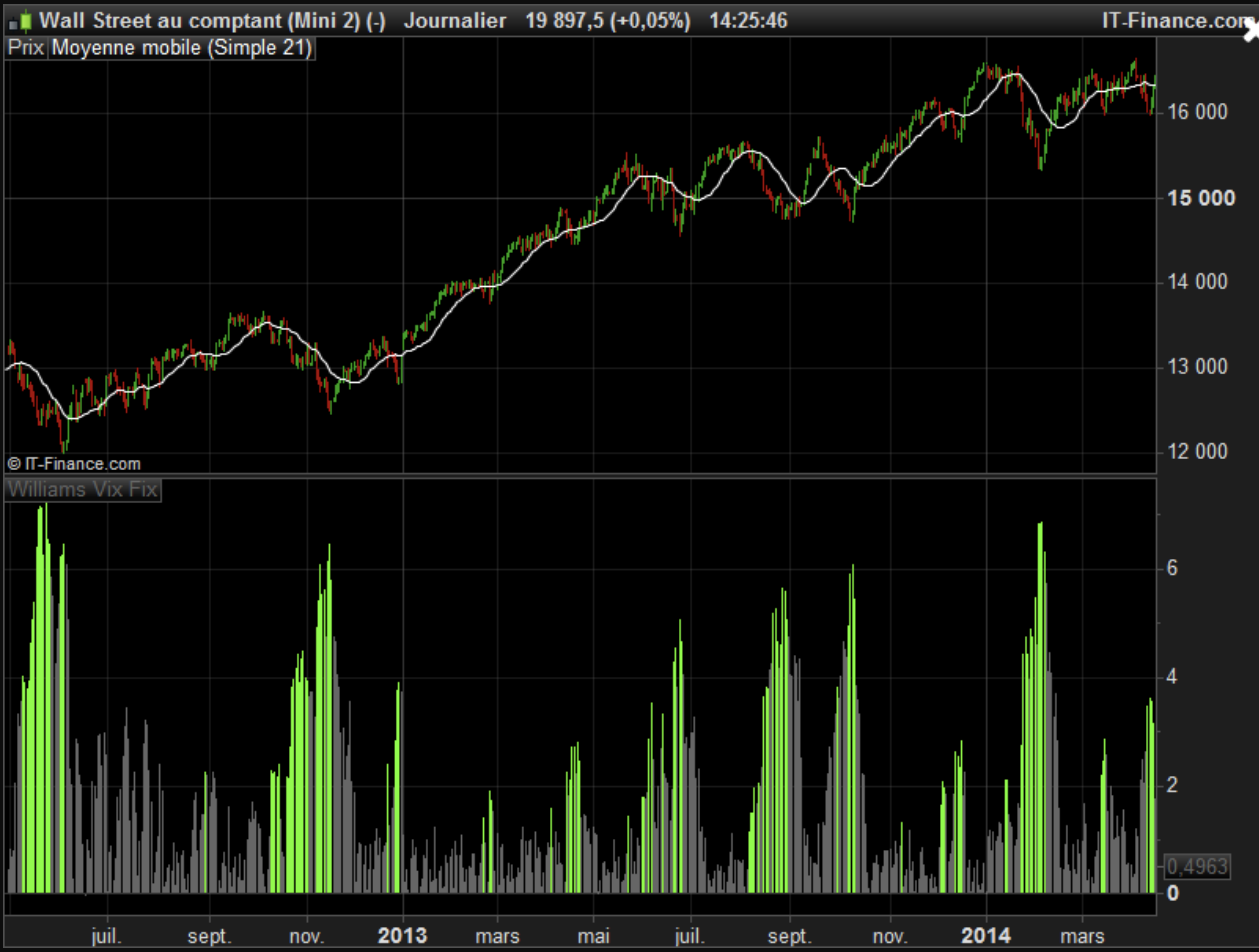

I’ve been reading more on this! Is this best way to make a IVR / IVP Indicator? The PRC Vix Fix green spike barchart is very clear. Are the substitute formulas to approximate for Implied Volatility (which predicts an assets expected future movement) and Historical Volatility good enough though?

Implied Volatility:

The Vix represents future 30 day Implied Volatility for the S&P 500. Larry Williams’ I Really Trade website: https://www.ireallytrade.com/newsletters/VIXFix.pdf

explains how high readings = high volatility (good for option (short) sellers of Calls or Puts as premiums explode in value). Williams’ duplicates this implied volatility Vix index with his simple formula:

WVF = (Highest (Close,22) - Low)/(Highest(Close,22))*100

and the VIX and WFV chart indicators look pretty similar.

Obviously the only real way to work out IV is to back calculate it out of the Black Scholes (BS) option Pricing Model using an options calculator as it has to reference the strike price and underlying price and represents a 1 std deviation move on an annual basis. I see formulas on Trading View using 365 days and 252 days, the former makes more sense as the BS Model references the risk free interest rate — for example — annual Gilt or Treasury Bill Rates.

Examples of Implied Volatility Calculations:

US Crude Price = $66

Strike Price for a Put option = $63

Implied Volatility = 24.95% (annual)

Therefore there is a 68% chance of the price being +/- $16.46 within a year ($66 x 0.2495).

Therefore expect:

1 Std Dev – 68% probability of the oil closing between $49.54 and $82.46 a year from now

2 Std Dev – 95% probability of the oil closing between $33.08 and $98.92 a year from now

3 Std Dev – 99.7% probability of the oil closing between $16.62 and $115.38 a year from now

Percentages are derived from the BS Model:

Strikes with a probability of 16% being In the Money at expiration make them more likely to be profitable for a buyer of Calls and Puts) / 84% Out the Money at expiration make them more likely to be profitable for a buyer of Calls and Puts) and these percentages capture a 1 standard deviation range for an OTM option.

Strikes with a probability of 2.5% ITM / 97.5% OTM capture a 2 standard deviation range for an OTM option.

(Stock price) x (Annualised Implied Volatility) x (Square Root of [days to expiration / 365]) = 1 standard deviation.

Example of AAPL that is trading at $323.62. The current Implied Volatility is 31.6%.

JAN options expire in 22 days, that would indicate that standard deviation is: $323.62 x 31.6% x SQRT (22/365) = $25.11

That means that there is a 68% chance that AAPL will be between $298.51 and $348.73 in January expiration.

https://www.optionsanimal.com/using-implied-volatility-determine-expected-range-stock/

Historical Volatility:

From Trading View: https://www.tradingview.com/script/lqwz92Fm-Historical-Volatility-Rank/

study(title="Historical Volatility Rank")

Length = input(20, minval=1)

annualVol = input(365, minval=1)

Price = log(close / close[1])

periods = iff(isintraday or isdaily, 1, 7)

sigma = stdev(Price, Length)

HVol = (sigma * sqrt(annualVol / periods)) * 100

lowVol = lowest(HVol, 365)

HVrankUp = HVol - lowVol

maxVol = highest(HVol, 365)

HVrankLow = maxVol - lowVol

HVR = HVrankUp / HVrankLow

plot(HVR, color = blue)

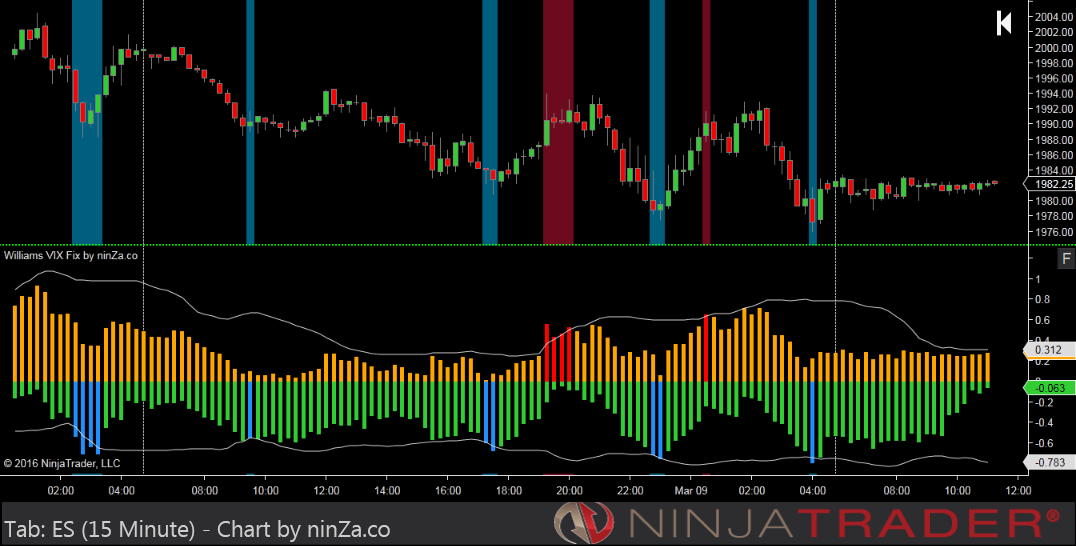

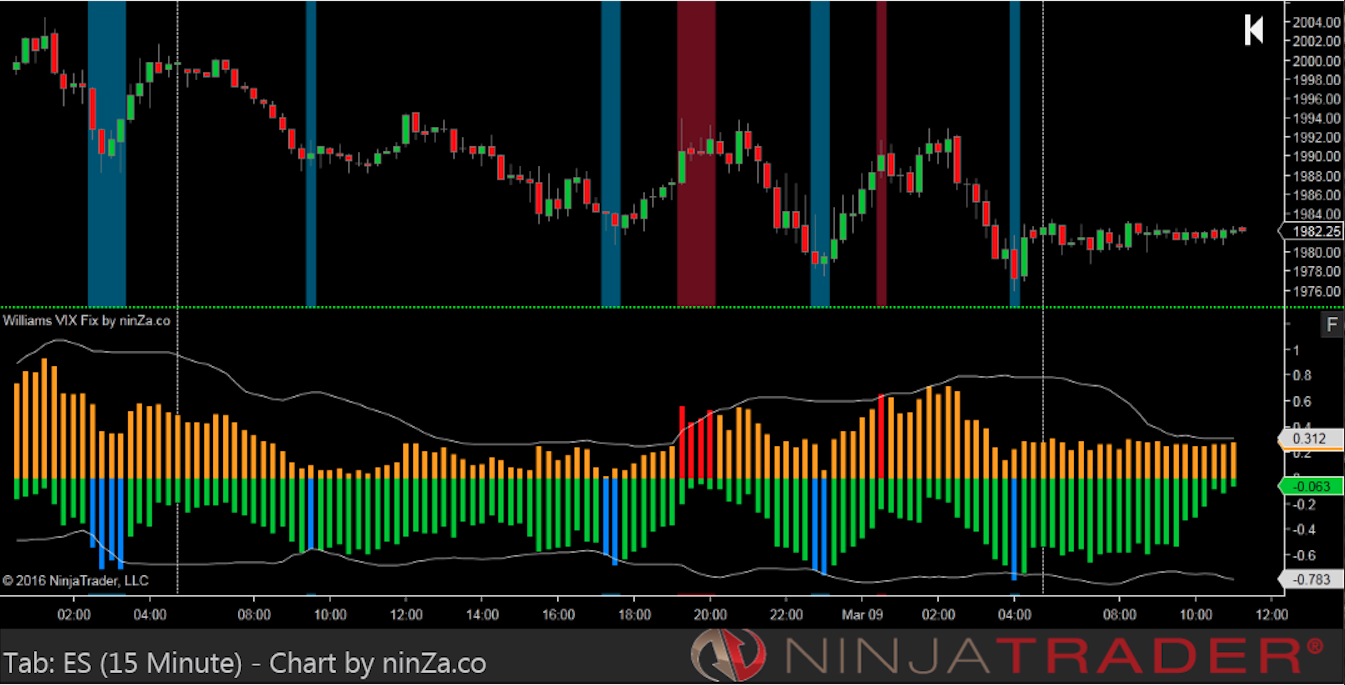

Referring back to the original Vix Fix post: https://www.prorealcode.com/topic/indicator-request-for-nic/#post-110244

and http://ninza.co/product/williams-vix-fix

Imagine an indicator as good as the PRC green high Vix Fix Volatility spike bar but also with Low spikes included to spot extreme measures of greed (for Shorting) and then also with an IVR/IVP ratio threshold showing perhaps better extremes like 20%, (and the mean threshold of 50%) and 80%. Pls see images.

Do any of these “musings” help you any Vonasi !?

Ps/ Why could I not get the PRC Vix Fix code to show green extreme bars?