Raul. Smallest stop allowed on FTSE 1€ at IG is 4points

@ GraHal – you need to move back the times in the code by 1hr for UK timings, then you will get similar results to what everyone is discussing. The reason why you get a great result with tick by tick turned off is because of the well known zero bar issue.

Kind Regards

Hi,

here is my analysis with my version day-to-day … actually on Friday the system is less powerful but still in profit.

| from 17_september to 23 january |

| Day |

Gain-loss |

|

Day |

Gain |

Loss |

| Monday |

6.784,50 |

|

Monday |

9.051,40 |

-2.266,90 |

| Tuesday |

7.569,70 |

|

Tuesday |

9.951,30 |

-2.381,60 |

| Wednesday |

5.886,90 |

|

Wednesday |

7.965,30 |

-2.078,40 |

| Thursday |

3.946,20 |

|

Thursday |

6.701,70 |

-2.755,50 |

| Friday |

841,60 |

|

Friday |

3.382,60 |

-2.541,00 |

| Total |

25.028,90 |

|

Total |

37.052,30 |

-12.023,40 |

On Friday, historically this year and a half fail, and although of benefits, is a program of accumulation of contracts, therefore, if you fail a particular day in a habitual way, divide between two contracts cutting good spins. As in catching the program from Monday to Thursday greatly improves the performance of the program only from Monday to Thursday

@ Arcane. Thanks for the heads-up. Please can you confirm that for the Dow the 9 unit minimum SL is all day? I understood it was just before the open and after the open it moved to 6? Thanks again

CN

CNParticipant

Senior

Order 11570, no entry and then it rmved the order. Why?

Good Morning,

I confirm that in my demo account the latest versions of the robot: DAX-5-MIN-TSL5.itf, DAX-5-MIN-TSL5-GR-MOD.itf, DAX-5MIN-TSL5-CON-GSTOR-RIESGO.itf and DAX -5-MIN-TP5-SL10.itf, have not executed order today.

However, the first version “DAX strategy 5min” if it has released order today, it has been negative.

Regards

Jesús

@CN

Because pending order only last one bar and then you’ll have to set it again.

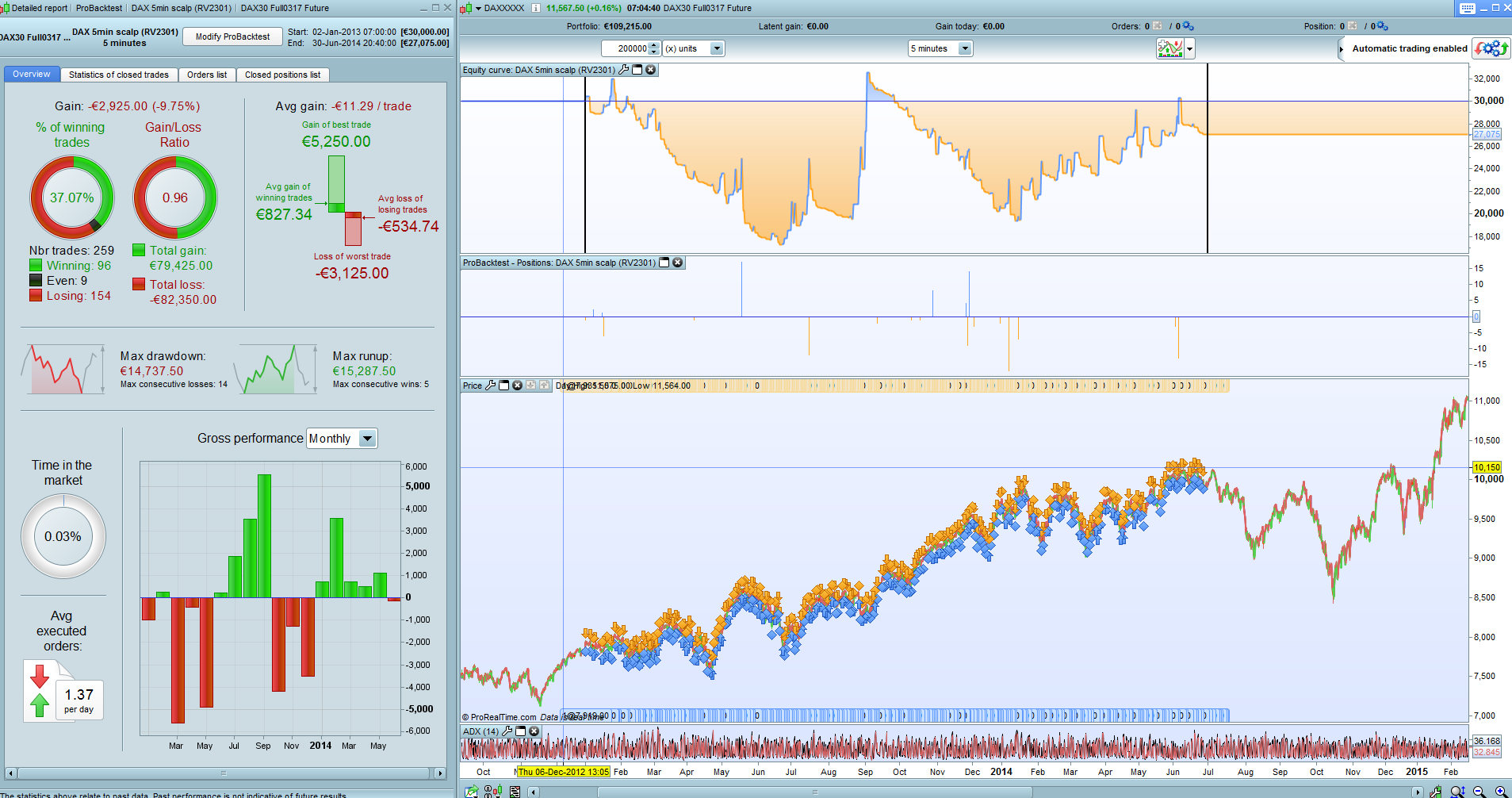

@ Raul. I ran your code exactly as you posted it yesterday. Had to increase starting equity to EUR30k.

I had the same problem as before with running the backtest with “ptrailing”. Something wrong with the data in July 2014. The same error message appeared. (It was fine if I used a fixed SL and target as before). I therefore had to split the test in two and I attach the results: 1) from Jan 2013 until 30 June 2014; and 2) 1 Aug 2014 until yesterday.

Hope this helps.

@JONJON

Hi,

which version do you have used for back ? Thanks

The enormous difference between the two periods is incredible. In one huge ups and downs and in the other everything smoother

@volpiemanuele. I’m using v 10.3

@Raul. I agree. Could be suspicious. I can’t verify the underlying data. However bear in mind that the test up to June 2014 is zoomed in. Not comparing like with like with regards to the scales.

The only consistent thing I have seen with my backtests is that 2013 wasn’t too great a year no matter whether you has a SL or a pTrailing

Hey!!!!

I was trying some backtest playing with the parameters n=x and the capital to figure out which one is the initial capital to the strategy. I realised that how much n=x add the code more % sucess i got (attach below). I am thinking in put the strategy in my real account so basicly guys i would like to get some help.

Could be real with n=1 and 1000€ as initical capital?

Which capital do you recomend for default n=6 ?

Regards.

I think your backtest with n6 has not been made in “tick by tick” mode. You should try another time, because I noticed that the first time it is launched, the results are often not “tick by tick”, and you have to launch once more, after clicking “titck by tick mode”, to have the real results.