PZonda5 – please use the ‘Insert PRT Code’ button when putting code in your posts as it makes it far easier for others to read.

I have tidied up your post for you. 🙂

Yeah, sorry for the messy post.

I just added the ITF files to keep it clean.

wp01

wp01Participant

Master

Hi PZonda5,

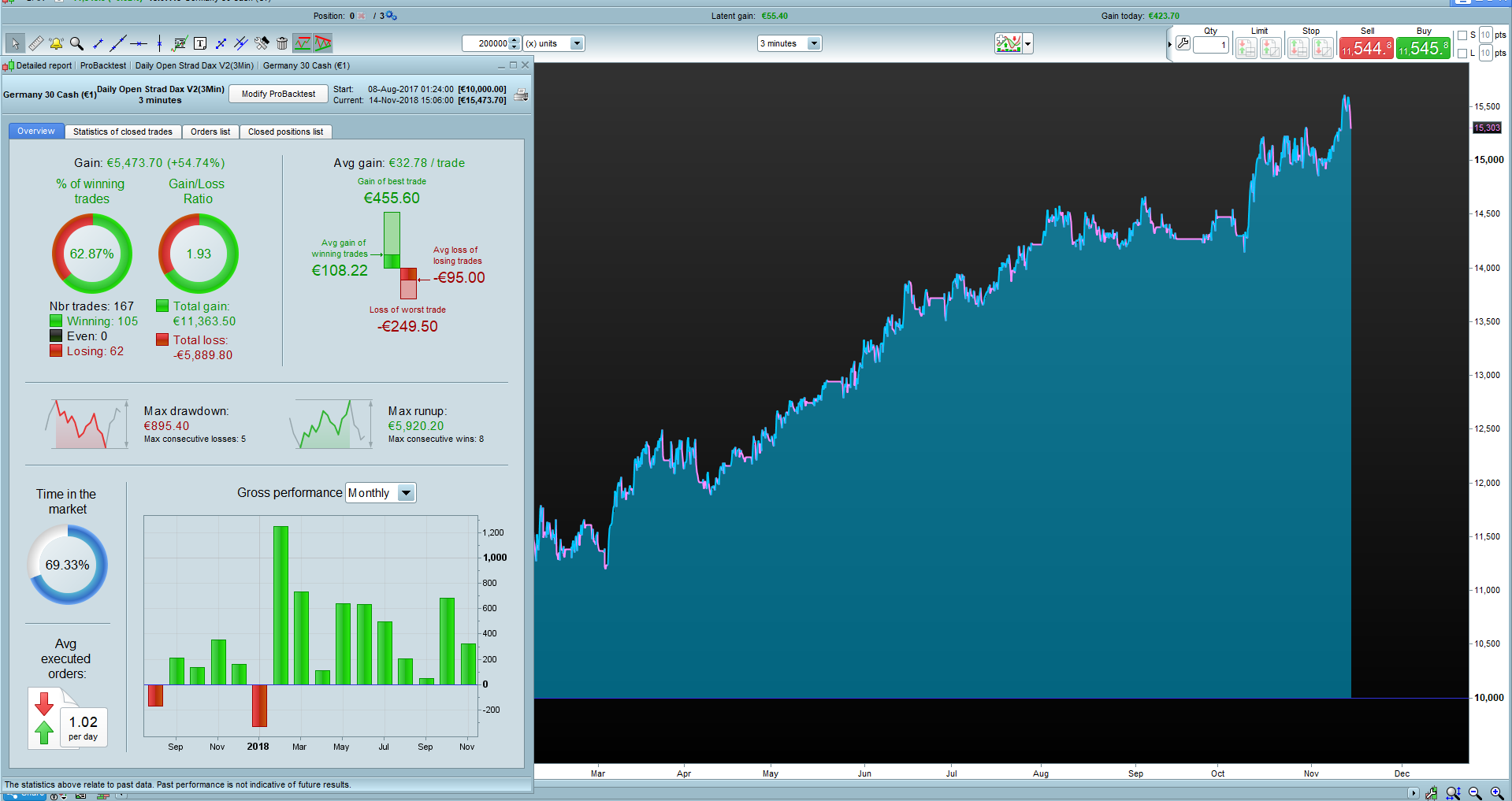

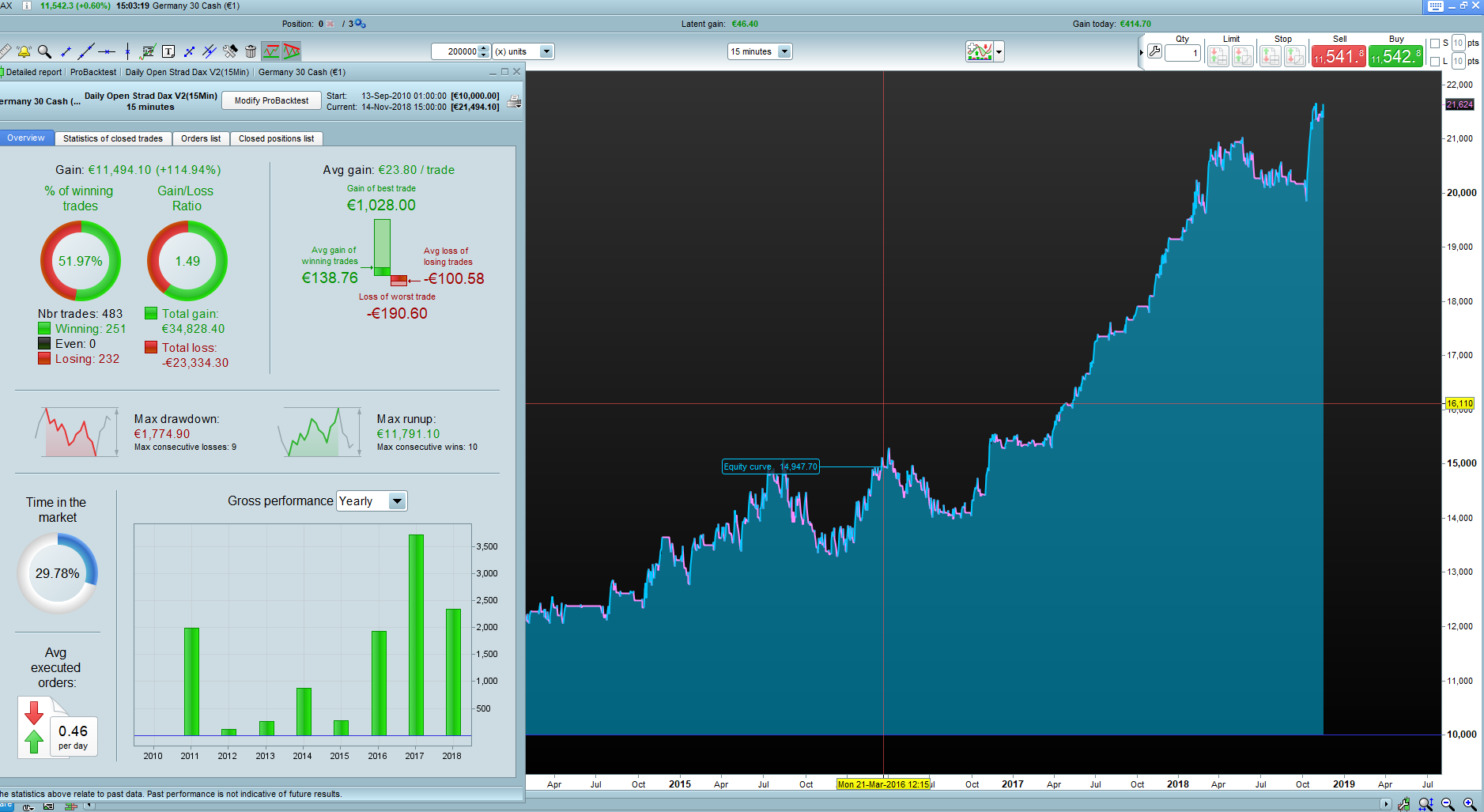

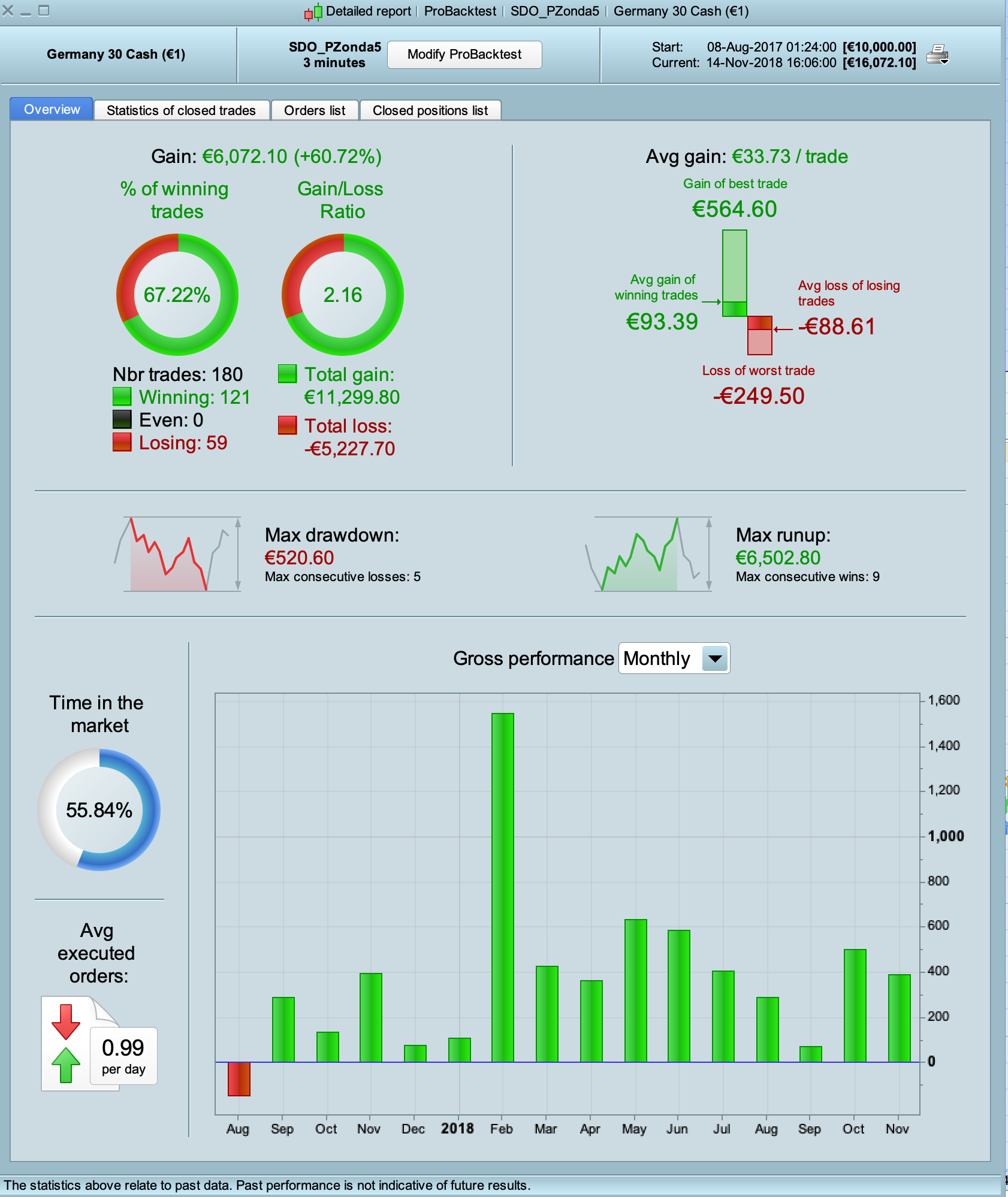

Please find attached the results of your itf. files on 200K bars for 3M, 10M and 15M.

Hope they match with your results.

Kind regards,

Paul

PaulParticipant

Master

Hi Pzonda5 Interesting idea.

I want to make an extra addition to the code.

if longonmarket and date > date[1] and ecshort then

sell at market

endif

if shortonmarket and date > date[1] and eclong then

exitshort at market

endif

date > date[1] and ecshort

do you mean tcshort?

I have no ecshort in the code version I am using? 🙂

wp01Participant

Master

@GraHal,

I just put it in the version of PZonda5. In that version it works. I got the same results Paul posted.

I just put it in the version of PZonda5

Did you put it in one of PZonda5 .itf’s?

I checked back and Paul’s version in the post below does contain ecshort and eclong.

Here’s an update of the code.

I feel like I’ve lost it!!

I’ve just put Paul’s code and PZonda5’s code (from his 3 min .itf ) on the diff checker site below and the codes are nothing like each other!? 🙂

I’ll try again in the morning.

https://www.diffchecker.com/diff

Dear all, who could help me to put a code in the system.

I want to double a positionsize only after a losing trade. Thanks in advance.

the codes are nothing like each other!?

Sorted! Something got screwed up somehow!

There are about 9 differences and ecshort eclong are in both versions!

do you mean tcshort?

The tcshort I referred to above was part of Paul’s original code in the Library.

So I’m not losing it after all! 🙂

Goodnight All

wp01Participant

Master

pippo999,

I’m not sure if this is the right way to think. Sounds more like a roulette system.

I think it is better to reinvest the profits.

“I want to skip the first 2 weeks every year since those two are bad for trading.”

Isn’t that overoptimizing? is your reason just bad performance?

thanks for sharing the strategy though.

PaulParticipant

Master

@Harrys

To me it isn’t over-optimising, for you maybe it is. In my opinion markets tend to behave differently on holidays and maybe even the day before or after because of low volume. Even when the markets in the VS are closed can have some impact.

Skipping first weeks of the year gives the market a bit of time to get back to normal after the holidays. Indeed the performance was not good for couple of years.

In general, I don’t want to trade every trading-day.

@harrys

To me it isn’t over-optimising, for you maybe it is. In my opinion markets tend to behave differently on holidays and maybe even the day before or after because of low volume. Even when the markets in the VS are closed can have some impact.

Skipping first weeks of the year gives the market a bit of time to get back to normal after the holidays. Indeed the performance was not good for couple of years.

In general, I don’t want to trade every trading-day.

Ok, thanks for you answer and reasoning!

Isn’t that overoptimizing? is your reason just bad performance?

You might be interested in this topic:

Weekly Seasonality Analysis

The images in the first post show all time performance for opening a position in each week of the year and then closing it based on very simple exit criteria in four popular markets. Historically some markets have performed better or worse depending upon the time of year – such as the FTSE Santa rally and the sell and go away in May theories. These results seem to confirm that. Whether the seasonality continues in the future is any ones guess but with the rolling look back indicator that I coded I am trying to test whether only trading in historically good weeks would have given any edge.