does not look like this is correct

Make it easier for us … please post the snippet of code you are referring to and a link to the post in which that snippet appears.

or can you explain in plain english what a buy signal for this system is?

Paul

PaulParticipant

Master

min1 = MIN(dhigh(0),dhigh(1))

min2 = MIN(dhigh(1),dhigh(2))

This code above finds the lowest value from the daily high’s, today, yesterday and day before

tcxLong = high < MIN(min1,min2)

This code above checks that the high of the i.e. 10min bar is lower than the lowest value from first code.

My reasoning for this long criteria, is that a previous daily high’s are a selling level, a resistance.

So, if the current high is below that, it has generally speaking a bit of room to increase and therefore also has more chances to make a profit.

min1 = MIN(dhigh(0),dhigh(1))

min2 = MIN(dhigh(1),dhigh(2))

min1 = MIN(dhigh(0),dhigh(1))

min2 = MIN(dhigh(1),dhigh(2))

This code above finds the lowest value from the daily high’s, today, yesterday and day before

tcxLong = high < MIN(min1,min2)

tcxLong = high < MIN(min1,min2)

This code above checks that the high of the i.e. 10min bar is lower than the lowest value from first code.

My reasoning for this long criteria, is that a previous daily high’s are a selling level, a resistance.

So, if the current high is below that, it has generally speaking a bit of room to increase and therefore also has more chances to make a profit.

could you explain in the most simple english what a buy signal for this system is? if i would like to try it manually

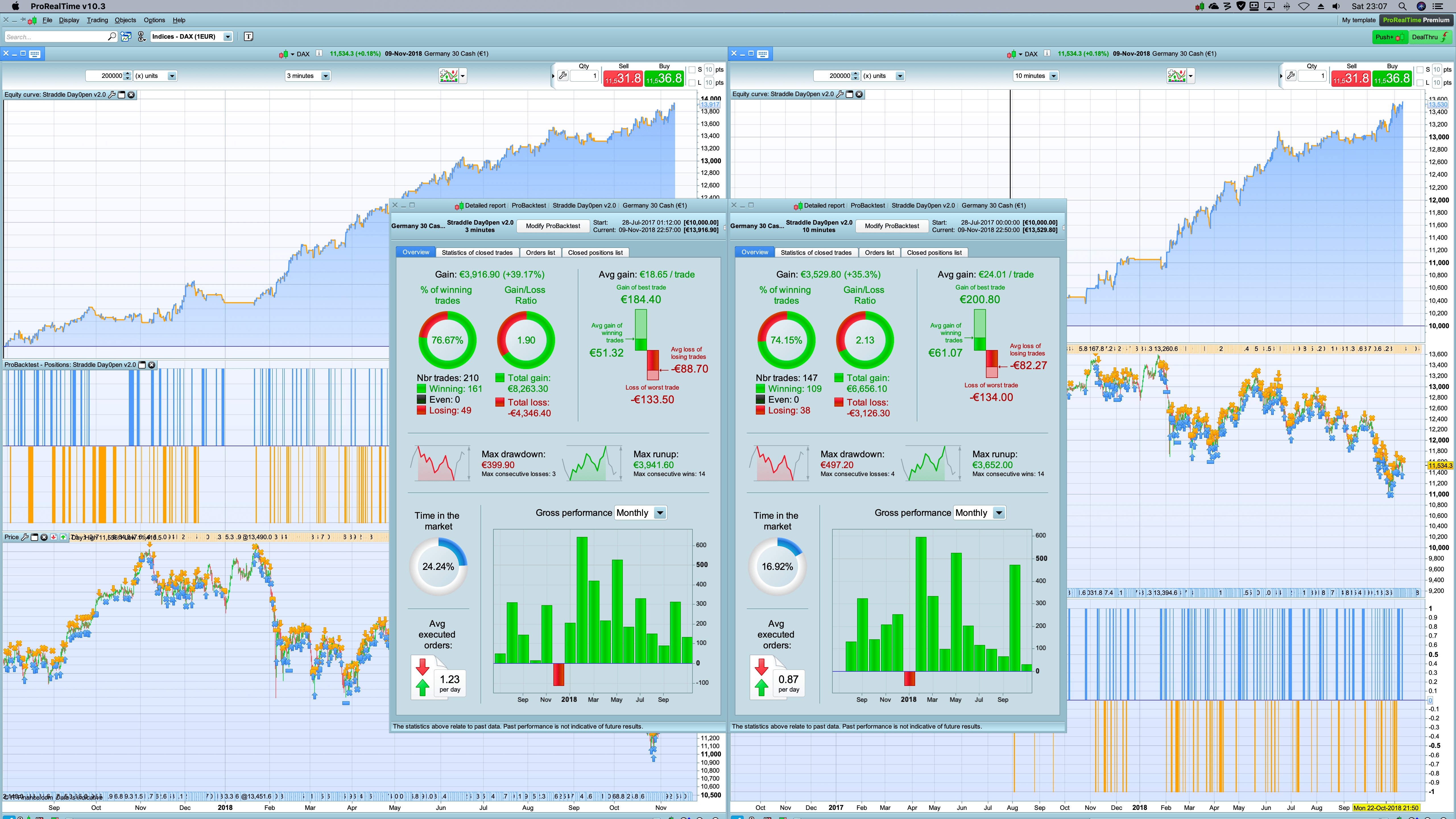

Hi, It make some optimisation with time frame 3 minute and 10 minute with the combine william & trailing and the result are very good. In your opinini which time frame is the best ? Thanks

sl = 0.94 // % Stoploss

pt = 1.41 // % Profit Target

ts = 0.35 // % MFETrailing

// indicator settigns

NOP=15 //number of points

sl = 1.15 // % Stoploss

pt = 1.5 // % Profit Target

ts = 0.35 // % MFETrailing

// indicator settigns

NOP=24 //number of points

PaulParticipant

Master

Good results!

You can optimise each timeframe to to smallest details. However I like to compare it with the same basic parameters.

SL 1.0, PT 1.5 and MFE 0.35

Also important. take 200k bars for the 3minute and set the same startdate to the 10 minute timeframe.

Now you compare the same periode, with the same basic parameters.

That’s means only the NOP is left. (number of points difference to dayopen at 9u)

In testing it seemed that the NOP for long can be a bit lower then NOP for short. So you can split them and have better results.

for 3 min. NOP long at 12, NOP short at 15 (i use 3 points incremental)

for 10 min NOP long at 18, NOP short at 21 or 24

Thank you Paul for your strategy.

Probabiliste looks interesting. I was even close to go live but i left them on “incubation” for couple of trades. Will see.

However, instead of Nop in pts, i replaced it by:

// indicator settigns

NOP= (close*0.0022)/pointsize

It seems more adaptative (IMO).

PaulParticipant

Master

Thnx for your input.

At the moment the code has an option to use a percentage.

If Usepercentage Then

Nopl=(Dayopen/100)*0.15

Nops=(Dayopen/100)*0.15

Else

Nopl=27

Nops=25

Endif

I changed that now so it uses also pointsize.

If Usepercentage Then

Nopl=((Dayopen*0.27)/100)/pointsize

Nops=((Dayopen*0.25)/100)/pointsize

Else

Nopl=27

Nops=25

Endif

PaulParticipant

Master

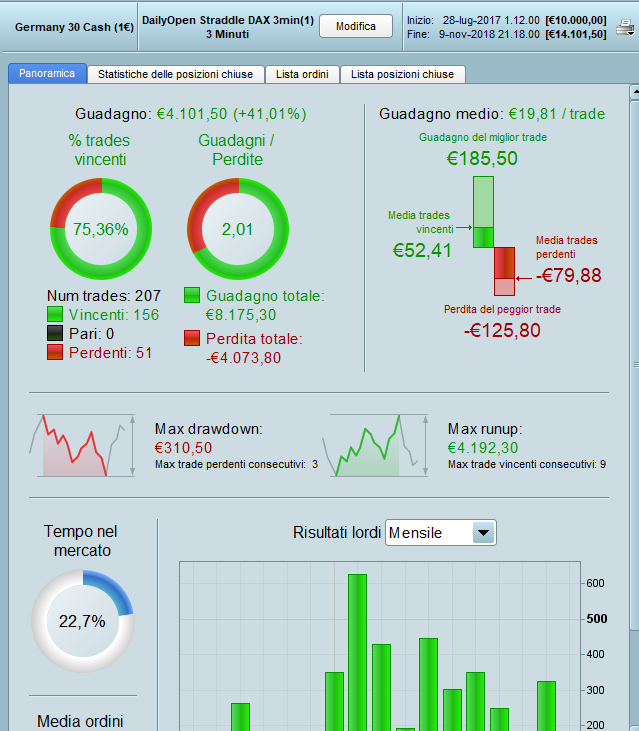

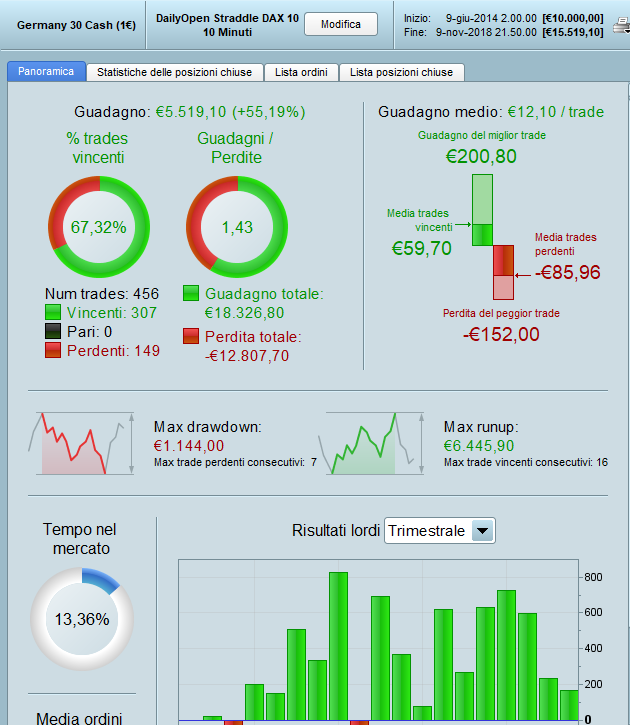

Here’s an update of the code. If anyone find improvements or other markets plz post!

Attached screenshot of 3 min bar 200k and same period for 10 minutes.

//-------------------------------------------------------------------------

// Main Code : Straddle Dayopen V2.0

//-------------------------------------------------------------------------

// Test On DAX 30 Cash 10 Minute Timeframe 200k bars or from 1/1/2015

// Common Rules

Defparam Cumulateorders = False

Defparam Preloadbars = 1000

// On/off

Extratradecriteria = 1 // I.e. Long; Only Enters When The Current Bar High Is Lower Then The Lowest Daily High From Today, Yesterday And Day Before.

Usepercentage = 0 // The Minimum Difference In Percentage [[1] From Dayopen Or In Points [0] From Dayopen

Mfetrailing = 1 // Mfe Trailing Stop

Wtrailing = 1 // Williams 3 Bar Trailing Stop

Breakevenstop = 1 // Breakevenstop, Move Stoploss When Position Is In Profit.

Excludefirsttwoweeks = 1 // Exclude The First 2 Weeks Of Every Year (Weeknumber 1 And 2)

// Settings

Positionsize = 1

SL = 1.00 // % Stoploss

PT = 1.50 // % Profit Target

MFETS = 0.35 // % Mfe Trailing Stop

BES = 0.35 // % Break Even Stop

BESMP = 0.05 // % Break Even Stop Minimum Profit

WTSMP = 0.50 // % Williams Trailing Stop Minimum Profit If Mfe Trailing Stop Is Not Used

ETD = 0 // Exclude a Trade Day; Sunday = 0

If Usepercentage Then

Nopl=((Dayopen*0.15)/100)/pointsize

Nops=((Dayopen*0.15)/100)/pointsize

Else

Nopl=24 //number of points long

Nops=24 //number of points short

Endif

// Day & Time

Once Entertime = 090000

Once Lasttime = 100000

Once Closetime = 240000 // Greater Then 23.59 Means It Continues Position Overnight

Once Closetimefr=173000

If Excludefirsttwoweeks=1 Then

If Year=2015 And Month=1 And (Day>=1 And Day<=18) Then

Notrading = 1

Elsif Year=2016 And Month=1 And (Day>=1 And Day<=24) Then

Notrading = 1

Elsif Year=2017 And Month=1 And (Day>=1 And Day<=22) Then

Notrading = 1

Elsif Year=2018 And Month=1 And (Day>=1 And Day<=21) Then

Notrading = 1

Elsif Year=2019 And Month=1 And (Day>=1 And Day<=20) Then

Notrading = 1

Else

Notrading = 0

Endif

Endif

Tt1 = Time >= Entertime

Tt2 = Time <= Lasttime

Tradetime = Tt1 And Tt2 and Notrading = 0 And Dayofweek <> ETD

// Reset At Start

If Intradaybarindex = 0 Then

Longtradecounter = 0

Shorttradecounter = 0

Tradecounter = 0

Mclong = 0

Mcshort = 0

Endif

// [pc] Position Criteria

Pclong = Countoflongshares < 1 And Longtradecounter < 1 And Tradecounter < 1

Pcshort = Countofshortshares < 1 And Shorttradecounter < 1 And Tradecounter < 1

// [mc] Main Criteria

If Time = Entertime Then

Dayopen=open

Endif

If High > Dayopen+nopl Then

Mclong=1

Else

Mclong=0

Endif

If Low < Dayopen-nops Then

Mcshort=1

Else

Mcshort=0

Endif

// [ec] Extra Criteria

If Extratradecriteria Then

Min1 = Min(Dhigh(0),dhigh(1))

Min2 = Min(Dhigh(1),dhigh(2))

Max1 = Max(Dlow(0),dlow(1))

Max2 = Max(Dlow(1),dlow(2))

Eclong = High < Min(Min1,min2)

Ecshort = Low > Max(Max1,max2)

else

Eclong=1

Ecshort=1

Endif

// Long & Short Entry

If Tradetime Then

If Pclong and Mclong And Eclong Then

Buy Positionsize Contract At Market

Longtradecounter=longtradecounter + 1

Tradecounter=tradecounter+1

Endif

If Pcshort and Mcshort And Ecshort Then

Sellshort Positionsize Contract At Market

Shorttradecounter=shorttradecounter + 1

Tradecounter=tradecounter+1

Endif

Endif

// Break Even Stop

If Breakevenstop Then

If Not Onmarket Then

Newsl=0

Endif

If Longonmarket And close-tradeprice(1)>=((Tradeprice/100)*BES)*pipsize Then

Newsl = Tradeprice(1)+((Tradeprice/100)*BESMP)*pipsize

Endif

If Shortonmarket And Tradeprice(1)-close>=((Tradeprice/100)*BES)*pipsize Then

Newsl = Tradeprice(1)-((Tradeprice/100)*BESMP)*pipsize

Endif

If Newsl>0 Then

Sell At Newsl Stop

Exitshort At Newsl Stop

Endif

Endif

// Exit Mfe Trailing Stop

If Mfetrailing Then

Trailingstop = (Tradeprice/100)*MFETS

If Not Onmarket Then

Maxprice = 0

Minprice = Close

Priceexit = 0

Endif

If Longonmarket Then

Maxprice = Max(Maxprice,close)

If Maxprice-tradeprice(1)>=trailingstop*pipsize Then

Priceexit = Maxprice-trailingstop*pipsize

Endif

Endif

If Shortonmarket Then

Minprice = Min(Minprice,close)

If Tradeprice(1)-minprice>=trailingstop*pipsize Then

Priceexit = Minprice+trailingstop*pipsize

Endif

Endif

If Onmarket And Wtrailing=0 And Priceexit>0 Then

Sell At Market

Exitshort At Market

Endif

Endif

// Exit Williams Trailing Stop

If Wtrailing Then

Count=1

I=0

J=i+1

Tot=0

While Count<4 Do

Tot=tot+1

If (Low[j]>=low[i]) And (High[j]<=high[i]) Then

J=j+1

Else

Count=count+1

I=i+1

J=i+1

Endif

Wend

Basso=lowest[tot](Low)

Alto=highest[tot](High)

If Close>alto[1] Then

Ref=basso

Endif

If Close<basso[1] Then

Ref=alto

Endif

If Onmarket And Mfetrailing=0 And Positionperf>WTSMP Then

If Low[1]>ref And High<ref Then

Sell At Market

Endif

If High[1]<ref And Low>ref Then

Exitshort At Market

Endif

Endif

If Onmarket And Mfetrailing=1 And Priceexit>0 Then

If High<ref Then

Sell At Market

Endif

If Low>ref Then

Exitshort At Market

Endif

Endif

Endif

// Exit At Closetime

If Onmarket Then

If Time >= Closetime Then

Sell At Market

Exitshort At Market

Endif

Endif

// Exit At Closetime Friday

If Onmarket Then

If (Currentdayofweek=5 And Time>=closetimefr) Then

Sell At Market

Exitshort At Market

Endif

Endif

// Build-in Exit

Set Stop %loss SL

Set Target %profit PT

//graph 0 Coloured(300,0,0) As "Zeroline"

//graph (Positionperf*100)coloured(0,0,0,255) As "Positionperformance"

@paul

Hello, in the end we arrived at the same result. After the post I made the comparisons on 200k starting from the same period for 3 minutes and 0 minutes.

Also I thought of dividing Nops between long and short. The results between 3 minutes and 10 minutes are similar. In your opinion, therefore, is it useful to use time frames 3 minutes or 10 minutes? Thanks

@Paul, thanks a lot for sharing.

Do you use the mentioned code in a real account ?

What is the capital minimum required for this strategy ?

what would be the easiest way to spot an entry manually? Could someone write in simple english the entry rules? Dont understand all the coding…

PaulParticipant

Master

@pippo999, yeah real account. 1 contract minimum is about €600 (dax 30 1€), but to cover initial losses you should’ve €1200 capital to be comfortable.

@volpiemanuele. Both are good and tradable. If you look at the profits, I would say they complement each other.

PaulParticipant

Master

Sorry can’t help you Jonas, I tried. But maybe someone else can!

Sorry can’t help you Jonas, I tried. But maybe someone else can!

where did you try? have not seen a reply to my comment?