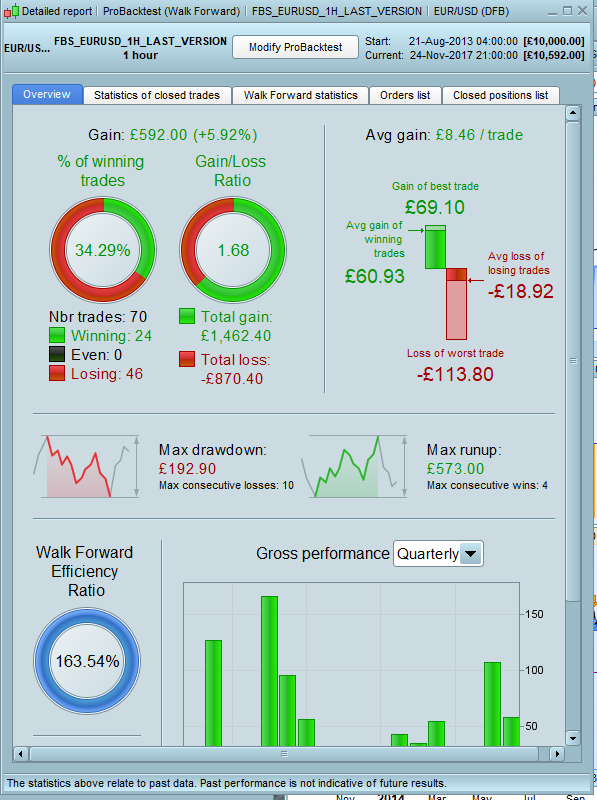

Here,

a 200000 backtest.

it seem good, but the problem with this strategy are the slippage and spread during news or big event?

what do you think about this?

@rejo007: Looks pretty nice. Only drawdown missing, probably because of that bug when testing…

yes, i have lot of time this problem of withdraw…

ALE

ALEModerator

Master

NEW VERSION

DEFPARAM CumulateOrders = FALSE// Posizioni cumulate disattivate

ONCE trailingStopType = TRT // 0 NONE, 1 TRAILING

ONCE percprofit = TP // 0.5

ONCE percloss = SL // 1

ONCE barlong = BXL //15

ONCE barshort = BXS //15

ONCE atrtrailingperiod = ATRSP //200

ONCE minstop = MINSTP //5 Pipsize - least distance of the stop for IG

ONCE trailingstoplong = TSL //15 Trailing stop start and distance

ONCE trailingstopshort = TSS // 15

// FRACTAL

ONCE CP = CPI // 120

// MOVING AVERAGE

ONCE avgLongPeriod = AVGL // 80

// CUMMRSI

ONCE CumRsiPer = CRP // 2

ONCE cumrsiEnterLongThreshold = CREL // 160

ONCE cumrsiEnterShortThreshold = CRES // 60

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pointsize)

//atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pointsize)/1000 // for indices divided for 1000

trailingstartl = round(atrtrail*trailingstoplong) //trailing stop start and distance

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

// FILTER SETTING

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

if Close[cp] >= highest[2*cp+1](Close) then

LH = 1

else

LH = 0

endif

if Close[cp] <= lowest[2*cp+1](Close) then

LL = -1

else

LL = 0

endif

if LH = 1 then

HIL = Close[cp]

endif

if LL = -1 then

LOL = Close[cp]

endif

PTN01 = (close CROSSES OVER HIL)

PTN02 = (close CROSSES UNDER LOL)

// CUMRSI

CUMRSI = SUMMATION[CUMRSIPER](RSI[CUMRSIPER](close))

// ENTRY

cumrsiFilterEnterLong = (cumrsi > cumrsiEnterLongThreshold)

cumrsiFilterEnterShort = (cumrsi < cumrsiEnterShortThreshold)

//MOVING AVERAGE

longAvg = Average[avgLongPeriod] (close)

//Enter

avgFilterEnterLong = (close>longAvg)

avgFilterEnterShort = (close<longAvg)

//--------------------------------------------------------------------------------------------------

// STRATEGY

//--------------------------------------------------------------------------------------------------

if (time >=100000 and time < 230000) then

IF NOT LongOnMarket AND avgFilterEnterLong AND PTN01 AND cumrsiFilterEnterLong THEN

BUY 1 CONTRACT AT MARKET

ENDIF

IF NOT ShortOnMarket AND avgFilterEnterShort AND PTN02 AND cumrsiFilterEnterShort THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

ENDIF

// Condizioni per uscire da posizioni long

IF POSITIONPERF<0 THEN

IF LongOnMarket AND BARINDEX-TRADEINDEX(1)>= barLong THEN

SELL AT MARKET

ENDIF

ENDIF

IF POSITIONPERF<0 THEN

IF shortOnMarket AND BARINDEX-TRADEINDEX(1)>= barshort THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

SET STOP %LOSS percloss

SET TARGET %PROFIT percprofit

GRAPH TGL

GRAPH TGS

ATTENTION TO THE TRAILING STOP, NEEDS TO DIVIDE THE DECIMAL, AS SUITABLE ONES TO TRY USING THE FUNCTION GRAPH

Hello ALE. It doesn’t seem to fair too well in 100K WF testing. Not many trades to base it on though. Do you get similar results?

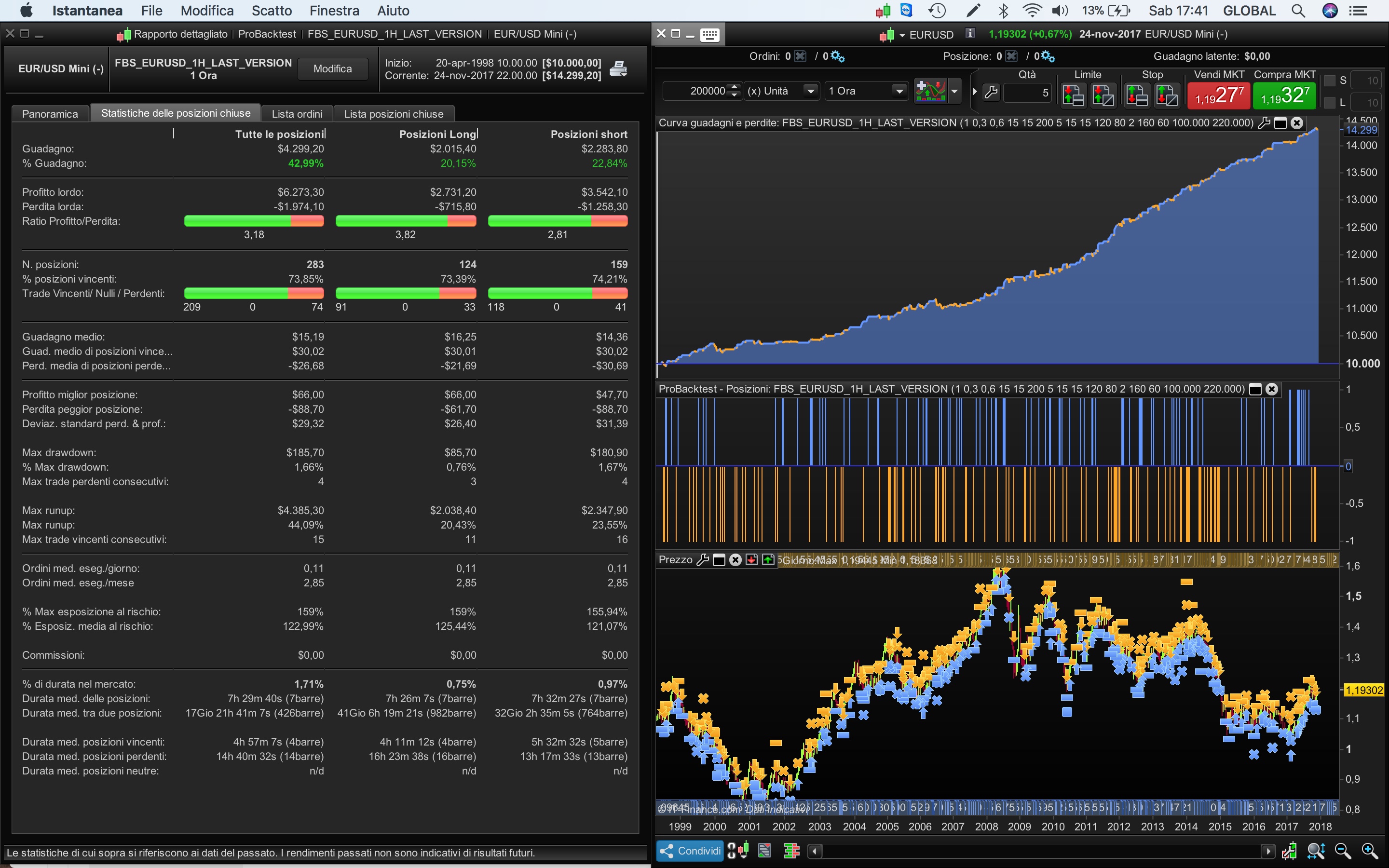

HI Ale,

interest concept , did you test with 200k bar also ?

Thansk

ALEModerator

Master

Hello,

I’ve work since 2010 to test tick by tick, because we have had many different from real version and backtest, anyway I’ve attached my result with 1 pip spread :

Those are interesting results ALE. I guess you could call my 100k WF test an in sample test which although profitable the WF results would give reason for doubts about robustness. Then your 200k test provides an out of sample period where strategy performance is comparable. This gives some confidence that it may continue working. My only concern is the number of trades – 129 is not many. Glad to see that my Cumulative RSI idea has been kept in the strategy though!

Definitely one to watch.

ALEModerator

Master

On 1 hour time frame , It’s difficult to speake about robustness, I suggest to look for high Gain/loss value.

On 1 hour time frame , It’s difficult to speake about robustness, I suggest to look for high Gain/loss value.

That is very interesting that you say that as I have been struggling to persuade myself that my shorter time frame strategies (1Hour or less) are any good and finding that my longer (daily and 4Hr) are proving more robust after WF testing. Maybe you are right and WF testing is less relevant to shorter time frame strategies but I cannot think why that would be. Have you run a WF on your 200K period or back to 2010 period using a dummy value to see how it fairs?

Regarding WF on short time frame strategies – maybe we just need to be happy that it is profitable in every OS period tested rather than getting hung up on the actual number and looking for the perfect result?

Hello,

Could you post the files without variables, because I have problem to run it.

Thanks a lot

Usdjpy and gbpusd could be a good pair for this strategy

With the permission of ALE,

Here is the file without the graphics and the variables, so you can run it in DEMO.

btw, Very nice job of improvement of the original code.

Saludos,

Juan

ALEModerator

Master

THANK YOU VERY MUCH JUAN!… 😉

ALEModerator

Master

@Vonasi,

as we know the problem is the unpredictable movement of the market under daily time frame. The best and simple strategy that we can find are often on daily time frame. The WF work good, the problem it’s unpredictability and the and the ever-changing market movements on low time frames.