defparam cumulateorders = false

defparam preloadbars = 10000

//defparam flatbefore = 080000

//defparam flatafter = 220000

once period1=7

once period2=14

once ValueX =period1

once Valuey =period2

ONCE ResetPeriod = 25

HeuristicsCycleLimit = 2

// ONCE HeuristicsCycle=1

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 0

HeuristicsAlgo1 = 1

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 0

HeuristicsAlgo2 = 1

EndIf

HeuristicsCycle = 0

EndIf

//If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

//

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

StartingValue = period1

//Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 7 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 2 //Minimum allowed value

MaxValue = 14 //Maximum allowed value

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

ONCE ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

once WinCountB = 3 //Initialize Best Win Count

GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

Graph StratAvgA*-1 as "StratAvgA"

once BestA = 300

GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

once BestB = 300

GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

//ElsIf HeuristicsAlgo2 = 1 Then

//

//// Heuristics Algorithm 2 Start

//

//If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

//optimize2 = optimize2 + 1

//EndIf

// StartingValue2 = period2

//ResetPeriod2 = 3 //Specify no of months after which to reset optimization

//Increment2 = 1

//MaxIncrement2 = 7 //Limit of no of increments either up or down

//Reps2 = 3 //Number of trades to use for analysis

//

//MinValue2 = 15 //Minimum allowed value

//MaxValue2 = 28 //Maximum allowed value

//

//If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

//MonthDays2 = 31

//ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

//MonthDays2 = 30

//ElsIf monthinit2 = 2 Then

//If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

//MonthDays2 = 29 //leap year

//Else

//MonthDays2 = 28

//EndIf

//EndIf

//

//If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

//ValueY = StartingValue2

//WinCountB2 = 0

//StratAvgB2 = 0

//BestA2 = 0

//BestB2 = 0

//dayinit2 = day

//monthinit2 = month

//yearinit2 = year

//EndIf

//

//once ValueY = StartingValue2

//once PIncPos2 = 1 //Positive Increment Position

//once NIncPos2 = 1 //Neative Increment Position

//once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

//once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

//

//If Optimize2 = Reps2 Then

//WinCountA2 = 0 //Initialize current Win Count

//StratAvgA2 = 0 //Initialize current Avg Strategy Profit

//HeuristicsCycle = HeuristicsCycle + 1

//

//For i2 = 1 to Reps2 Do

//If positionperf(i) > 0 Then

//WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

//EndIf

//StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

//Next

//StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

//If StratAvgA2 >= StratAvgB2 Then

//StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

//BestA2 = ValueY

//EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

//If WinCountA2 >= WinCountB2 Then

//WinCountB2 = WinCountA2 //Update Best Win Count

//BestB2 = ValueY

//EndIf

//

//If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

//Mode = 0

//ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

//ValueY = ValueY - (Increment2*NIncPos2)

//NIncPos2 = NIncPos2 + 1

//Mode2 = 2

//ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

//ValueY = ValueY + (Increment2*PIncPos2)

//PIncPos2 = PIncPos2 + 1

//Mode = 1

//ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

//ValueY = ValueY + (Increment2*PIncPos2)

//PIncPos2 = PIncPos2 + 1

//Mode2 = 1

//ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

//ValueY = ValueY - (Increment2*NIncPos2)

//NIncPos2 = NIncPos2 + 1

//Mode2 = 2

//EndIf

//

//If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

//If BestA2 = BestB2 Then

//ValueY = BestA

//Else

//If reps2 >= 10 Then

//WeightedScore2 = 10

//Else

//WeightedScore2 = round((reps2/100)*100)

//EndIf

//ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

//EndIf

//NIncPos2 = 1

//PIncPos2 = 1

//ElsIf ValueY > MaxValue2 Then

//ValueY = MaxValue2

//ElsIf ValueY < MinValue2 Then

//ValueY = MinValue2

//EndIF

//

//Optimize2 = 0

//EndIf

//

//// Heuristics Algorithm 2 End

//

//EndIf

c1=average[valuex](close)

c2=average[valuey](close)

//

condbuy =c1 crosses over c2 and rsi[14](close)<70

condsell=c1 crosses under c2 and rsi[14](close)>30

//

if condbuy then

buy at market

endif

if condsell then

sellshort at market

endif

//pp=positionperf(0)*100

//if pp<-0.125 then

//sell at market

//exitshort at market

//endif

set stop %loss 0.5 // exit sooner on performance criteria above

set target %profit 0.25

//GRAPH OPTIMIZE

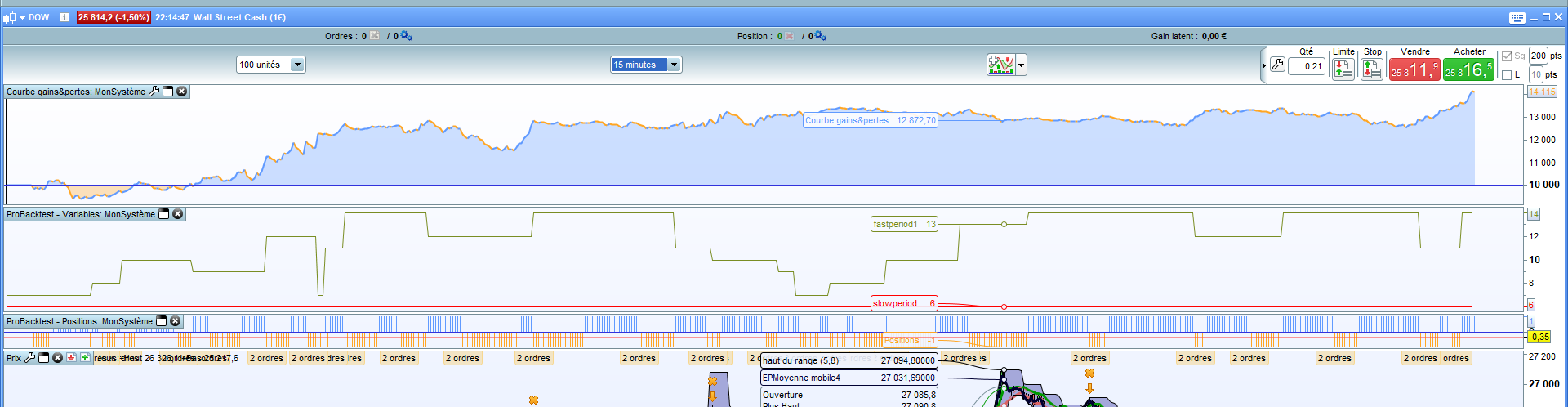

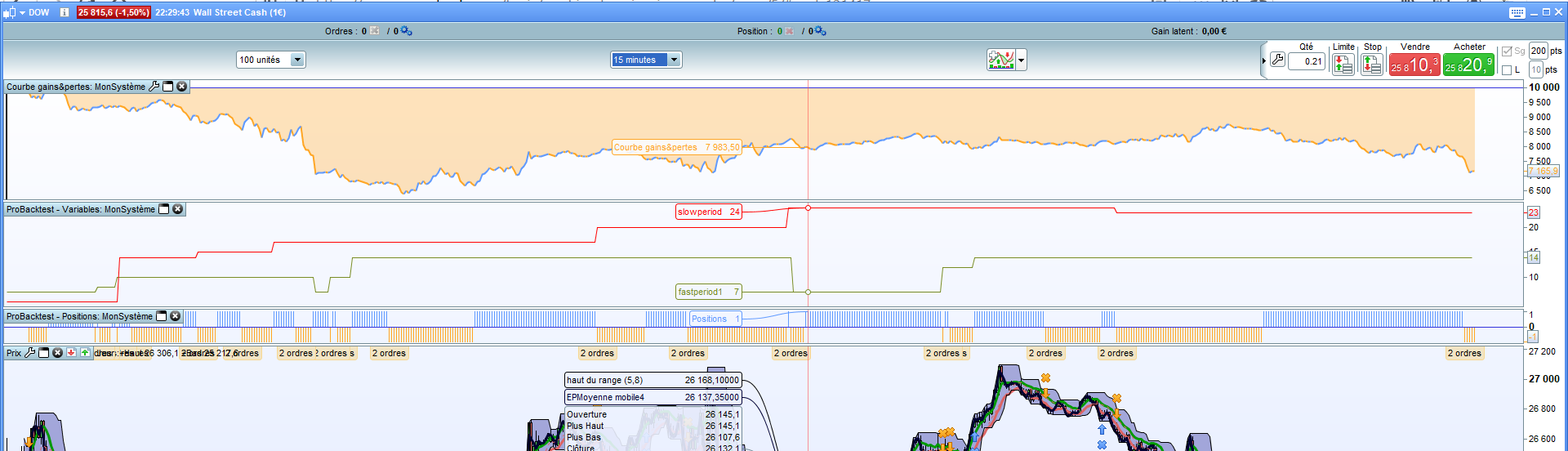

graph ValueX coloured(121,141,35,255) as "fastperiod1"

graph ValueY coloured(255,0,0,255) as "slowperiod"

GRAPH dayinit + ResetPeriod

GRAPH ResetPeriod

GRAPH monthinit

graph dayinit

Good evening,

Unable to initialize variables

Monthinit

Dayinit

removing some of the code works.

SHOULD we initialize it is variable?

if not onmarket then

dayinit = day

monthinit = month

yearinit = year

endif

@fifi743 … got ValueY working so my (now deleted) comment is no longer needed.

only a single increment is made either up or down

Is the 1 x increment of the value set as increment?

So if I set increment = 2 then in any one bar, ValueX or Value Y should not change by more than ‘2’ (up or down)?

only a single increment is made either up or down

Is the 1 x increment of the value set as increment?

So if I set increment = 2 then in any one bar, ValueX or Value Y should not change by more than ‘2’ (up or down)?

Correct, unless the increment limit value has been reached, after which ValueX will revert to the new Average best performing value

for test :

Depending on the month it changes from HeuristicsAlgo1 to HeuristicsAlgo2

I moved valuey to line 40

defparam cumulateorders = false

defparam preloadbars = 10000

//defparam flatbefore = 080000

//defparam flatafter = 220000

period1=7

period2=14

if not onmarket then

dayinit = day

monthinit = month

yearinit = year

endif

HeuristicsCycleLimit = 2

IF monthinit mod 2 = 1 then

HeuristicsAlgo1 = 1

elsif monthinit mod 2 =0 then

HeuristicsAlgo2 = 1

endif

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

StartingValue = period1

valuey= PERIOD2

ResetPeriod = 3//Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 3//Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 2 //Minimum allowed value

MaxValue = 14 //Maximum allowed value

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 1 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 0 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

Graph StratAvgA*-1 as "StratAvgA"

once BestA = 0

GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

once BestB = 0

GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

ElsIf HeuristicsAlgo2 = 1 Then

// Heuristics Algorithm 2 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize2 = optimize2 + 1

EndIf

StartingValue2 = period2

valuex=period1

ResetPeriod2 = 3//Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 5//Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MinValue2 = 15 //Minimum allowed value

MaxValue2 = 30 //Maximum allowed value

If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

MonthDays2 = 31

ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

MonthDays2 = 30

ElsIf monthinit2 = 2 Then

If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

MonthDays2 = 29 //leap year

Else

MonthDays2 = 28

EndIf

EndIf

If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

dayinit2 = day

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 1 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

once WinCountB2 = 3 //Initialize Best Win Count

GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

once StratAvgB2 = 0 //Initialize Best Avg Strategy Profit

GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

Graph StratAvgA2*-1 as "StratAvgA2"

once BestA2 = 0

GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

once BestB2 = 0

GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

EndIf

pp=positionperf(0)*100

IF pp<-0.02 and HeuristicsAlgo2 and longonmarket then

HeuristicsAlgo1=1

SELL AT MARKET

elsif pp<-0.05 and HeuristicsAlgo1 and shortonmarket then

HeuristicsAlgo2=1

EXITSHORT AT MARKET

endif

c1=average[valuex](close)

c2=average[valuey](close)

//

condbuy =c1 crosses over c2 and rsi[14](close)<50

condsell=c1 crosses under c2 and rsi[14](close)>40

//

if condbuy then

buy at market

endif

if condsell then

sellshort at market

endif

//

//if pp<-0.125 then

//sell at market

//exitshort at market

//endif

set stop %loss 0.5 // exit sooner on performance criteria above

set target %profit 3

graph pp

graph valuex coloured(121,141,35,255) as "fastperiod1"

graph valuey coloured(255,0,0,255) as "slowperiod"

I just had a little play with the first code that Juanj posted and I noticed that I could sometimes get the ‘Periods’ variable to go negative. You might want to add a minimum value allowed to prevent this as it could cause a strategy to be stopped.

@Vonasi, if you consider the latest version of the algorithm (not the one from a few years back), there is a minimum value and as long as MinValue is specified as a positive value a negative value shouldn’t occur

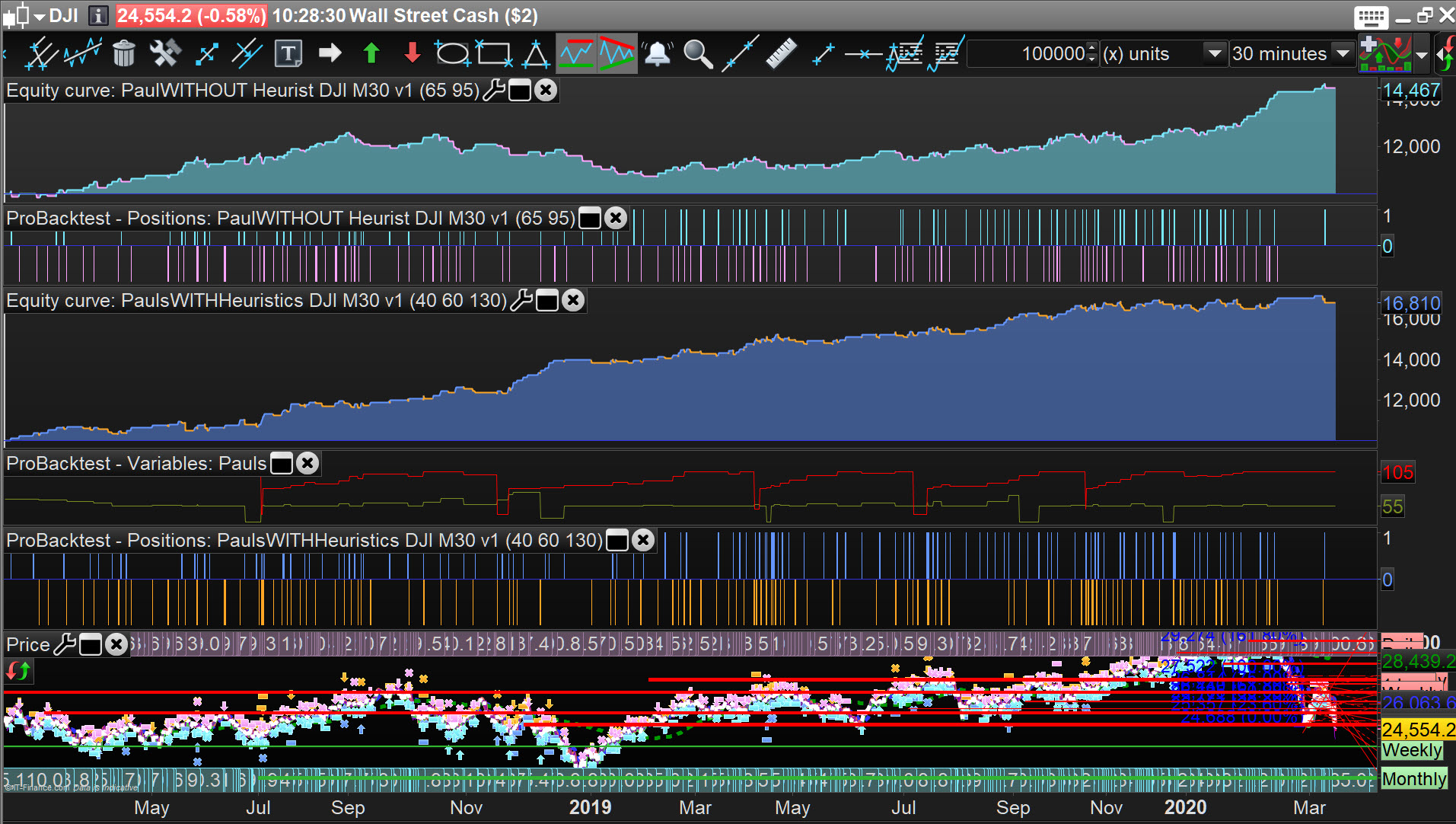

Attached results using Paul’s System.

- Top Curve WITHOUT Heuristics (code is bare System / Paul’s original code only).

- Bottom Curve WITH Heuristics.

Bottom Curve … Heuristic Algo1 and Algo2 are both working at the same time.

I found that it is not a case of adding Heuristics on top of a best effort bare code.

I am going to start my version on Forward Test now to establish that my version is not just a massive curve fit of the Heuristics!? 🙂

I am posting my results as encouragement / to show that JuanJ code does work.

Maybe you can get JuanJ code to work with even better results on Paul’s System than attached?

Jan

JanParticipant

Veteran

Hi Juan,

I try to understand the concepts of what you are trying to obtain with this machine learning, could you explain this ?

Normally you develop a strategy with fixed settings (eg like a Macd crossing strategy) based upon past data, and assuming the future movements of price are relatively similar, and you let run your trading-algo.

With this machine learning concept, are you trying to further optimize the following of past changes in price movements, then with those optimized findings approaching the future price movements with the new strategy ?

Or when running a algo-strategy, with this machine learning concept, it adjust the setting of the variables automatically given the structure of price movements ?

(I hope my question is clear, in this case it would be great to discuss this kind of topics face to face in a meeting with others, to avoid misunderstandings)

JanParticipant

Veteran

Hi Grahal or others,

Could you be so kind to spend a few words to explain the concepts of the “Heuristics” ? Is it daily optimising of a fixed setting, and yes, what is the base of the adjustment, how many bars backwards ?

I am sorry, but I missed that out of lots of interesting code.

Thanks in advance for your help !

Your comment “Attached results using Paul’s System.

- Top Curve WITHOUT Heuristics (code is bare System / Paul’s original code only).

- Bottom Curve WITH Heuristics. “

when running a algo-strategy, with this machine learning concept, it adjust the setting of the variables automatically given the structure of price movements ?

It is above. (I am commenting as JuanJ is probably busy trading or mentoring etc)

I have found though that the starting value for ValueX is important to get good results.

Also a few other variables in the Heuristics are important re initialisation value. This is understandable else the Heuristics would be the panacea for all!? 🙂

how many bars backwards ?

This is a setting in the Heuristics Algo (Halgo), but it is set by number of Trades backwards.

So to use an example … the results of the last 3 Trades Trades 1, 2 and 3 are used to vary the Halgo variables in order to produce an optimum ValueX to go forward with for the next Trade (4).

Then it is my understanding that … Trade4 would be used together with Trade3 and Trade 2 to repeat above.

I will try and decide … from the code … if it is above or is it … the Halgo variables are next optimised after Trade 6 using Trade 4, 5 and 6??

@Jan you are far better at coding than I so maybe you can read JuanJ code and decide??

Whoever finds out first, post on here, unless JuanJ passes by and tells us first?