Hi,

the latest stable version in which I can insert my MM to make backtest is the V 5.0 for both dax and us100 ? Thank you

Paul

PaulParticipant

Master

Yes 5.0 is the latest. If it’s stable enough you only find out in live trading.

ok thanks,

but in order to to make my money management work that I need to change?

/ [pc] position criteria (also set a limit to the number of trades a day) (set all high for no impact)

// is influenced by which reset criteria is used

if resetcounter then

pclong = countoflongshares < 2 and longtradecounter < 100 and tradecounter < 3

pcshort = countofshortshares < 2 and shorttradecounter < 100 and tradecounter < 3

else

pclong = countoflongshares < 1 and longtradecounter < 100 and tradecounter < 100

pcshort = countofshortshares < 1 and shorttradecounter < 100 and tradecounter < 100

endif

// has influence on Money Management

PaulParticipant

Master

no changes perhaps? I would use resetcounter=0 and test

@Paul

I insert my MM and set resetcounter=0 and my MM don’t run. The same problem with the version 5.0 on dax. The version 4.2 on dax run very well on my MM. Can you solve the problema. Attach v 5.0 of US100 with my MM. (the same problem in v. 5.0 on dax). Tanks

PaulParticipant

Master

one to many lotti entry in the code! That don’t work.

I’ve changed few settings to adapt the strategie with 1 minute timeframe.

Can anyone show me the backtest with premium PRT? (spread:1, timeframe:1min, market:dax)

Thank you

//-------------------------------------------------------------------------

// Code principal : DAX, 1min, Vectorial V4.2

//-------------------------------------------------------------------------

// ROBOT VECTORIAL DAX v4.2p

// M5

// SPREAD = 1

// by BALMORA 74 - APRIL 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

once enablesl = 1 // stoploss

once enablept = 0 // profit target

once enablets = 1 // trailing stop

// when set display to 1, uncomment graphonprice to have affect visually (comment out graphonprice for trading)

once displaysl = 1 // stop loss

once displaypt = 1 // profit target

once displayts = 1 // trailing stop

once usetimecriteria = 1 // [1] included extra timeschedules not to trade

once holiday = 1 // [1] prevent trading on a german public holiday

once positionweekend = 1 // [1]=keep weekend position then ignore times below

once fridaylastentry = 174500

once fridayclosetime = 225500 // close on last candle on friday to prevent gaps over weekend

sl = 1.5 // % stoploss

pt = 2 // % profit target

// reset at start

if intradaybarindex= 0 then

tradeday = 1

endif

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

longtradecounter= 0

shorttradecounter = 0

tradecounter=0

endif

// [pc] position criteria (also set a limit to the number of trades a day) (or set high for no impact)

// tradecounter means taking x trades a day max (long / short combined)

// with moneymanagement; set all to 100 to have no effect on moneymanagement

// without moneymangement; i.e. max 1 trade a day set all values to 1

pclong = countoflongshares < 3 and longtradecounter < 10 and tradecounter < 5

pcshort= countofshortshares < 3 and shorttradecounter < 10 and tradecounter < 5

// Money Management

Lotti = 1

// Money Management End

// used for sl/pt/ (not used for ts)

underlaying=100

// not to be optimized !

// underlaying security / index / forex

// profittargets and stoploss have to match the lines

// 0.01 forex [i.e. gbpusd=0.01]

// 1.00 securities [i.e. aapl=1 ;

// 100.00 indexes [i.e. dax=100]

// 100=xauusd

// 100=cl us crude

if holiday then

// prevent trading first week in a new year

if year=2015 and month=1 and day<=4 then

tradeday = 0

elsif year=2016 and month=1 and day<=3 then

tradeday = 0

elsif year=2017 and month=1 and day<=8 then

tradeday = 0

elsif year=2018 and month=1 and day<=7 then

tradeday = 0

elsif year=2019 and month=1 and day<=6 then

tradeday = 0

// prevent trading yearly common holiday's

elsif month=12 and day=25 then // Christmas Day

tradeday = 0

elsif month=12 and day=26 then // Christmas Day

tradeday = 0

// prevent trading on a public holiday in germany; market can be open

elsif year=2019 and month=4 and day=19 then // holiday in germany; Good Friday

tradeday = 0

elsif year=2018 and month=3 and day=30 then // holiday in germany; Good Friday

tradeday = 0

elsif year=2017 and month=4 and day=14 then // holiday in germany; Good Friday

tradeday = 0

elsif year=2019 and month=4 and day=22 then // holiday in germany; Easter Monday

tradeday = 0

elsif year=2018 and month=4 and day=2 then // holiday in germany; Easter Monday

tradeday = 0

elsif year=2017 and month=4 and day=17 then // holiday in germany; Easter Monday

tradeday = 0

elsif month=5 and day=1 then // holiday in germany; Labour Day

tradeday = 0

elsif year=2019 and month=5 and day=30 then // holiday in germany; Ascension Day

tradeday = 0

elsif year=2018 and month=5 and day=10 then // holiday in germany; Ascension Day

tradeday = 0

elsif year=2017 and month=5 and day=25 then // holiday in germany; Ascension Day

tradeday = 0

elsif year=2019 and month=6 and day=10 then // holiday in germany; Whit Monday

tradeday = 0

elsif year=2018 and month=6 and day=21 then // holiday in germany; Whit Monday

tradeday = 0

elsif year=2017 and month=6 and day=5 then // holiday in germany; Whit Monday

tradeday = 0

elsif month=10 and day=3 then // holiday in germany; Unity Day

tradeday = 0

//

else

tradeday = 1

endif

endif

//TRADING TIME

tradetime = time >= 095500 and time < 174500

//tradetime = time >= 160000 and time < 214500

if usetimecriteria then

notradetime=(time>=113000 AND time<120000) OR (time>=133000 and time<160000)

//notradetime = 0

notradetime=not notradetime

else

notradetime=tradetime

endif

//STRATEGY

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

ONCE lag = 0.5

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO))

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

//BUY CONDITIONS

CondBuy1 = ANGLE >= 30

CondBuy2 = (pente > trigger) AND (pente < 0)

CondBuy3 = average[100](close) > average[100](close)[1]

CONDBUY = CondBuy1 and CondBuy2 and CondBuy3

//SHORT CONDITIONS

CondSell1 = ANGLE <= - 30

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

CondSell3 = average[10](close) < average[10](close)[1]

CONDSELL = CondSell1 and CondSell2 and CondSell3

//POSITION LONGUE

if tradetime then

IF positionweekend and TRADEDAY THEN

IF pclong and CONDBUY and notradetime THEN

buy lotti contract at market

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

ENDIF

//POSITION COURTE

IF pcshort and CONDSELL and notradetime THEN

Sellshort lotti contract at market

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

ENDIF

elsif positionweekend=0 and TRADEDAY THEN

if currentdayofweek<=4 or (currentdayofweek=5 and time<fridaylastentry) then

IF pclong and CONDBUY and notradetime THEN

buy lotti contract at market

longtradecounter=longtradecounter + 1

tradecounter=tradecounter+1

ENDIF

//POSITION COURTE

IF pcshort and CONDSELL and notradetime THEN

Sellshort lotti contract at market

shorttradecounter=shorttradecounter + 1

tradecounter=tradecounter+1

ENDIF

endif

endif

endif

//TRAILING STOP

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if enablets = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

if displayts then

//graphonprice PREZZOUSCITA coloured(0,0,255,255) as "trailingstop"

endif

ENDIF

// set stoploss

if enablesl then

if not onmarket then

sloss=0

elsif longonmarket then

sloss=tradeprice(1)-((tradeprice(1)*sl)/underlaying)*pointsize

elsif shortonmarket then

sloss=tradeprice(1)+((tradeprice(1)*sl)/underlaying)*pointsize

endif

SET STOP %LOSS sl

if displaysl then

//graphonprice sloss coloured(255,0,0,255) as "stoploss"

sloss=sloss

endif

endif

// to display profittarget

if enablept then

if not onmarket then

ptarget=0

elsif longonmarket then

ptarget=tradeprice(1)+((tradeprice(1)*pt)/underlaying)*pointsize

elsif shortonmarket then

ptarget=tradeprice(1)-((tradeprice(1)*pt)/underlaying)*pointsize

endif

SET TARGET %PROFIT pt

if displaypt then

//graphonprice ptarget coloured(121,141,35,255) as "profittarget"

ptarget=ptarget

endif

endif

// close position on friday

if positionweekend=0 then

if onmarket then

if currentdayofweek=5 and time=fridayclosetime then

sell at market

exitshort at market

endif

endif

endif

//pp=(positionperf*100)

//graph pp

PaulParticipant

Master

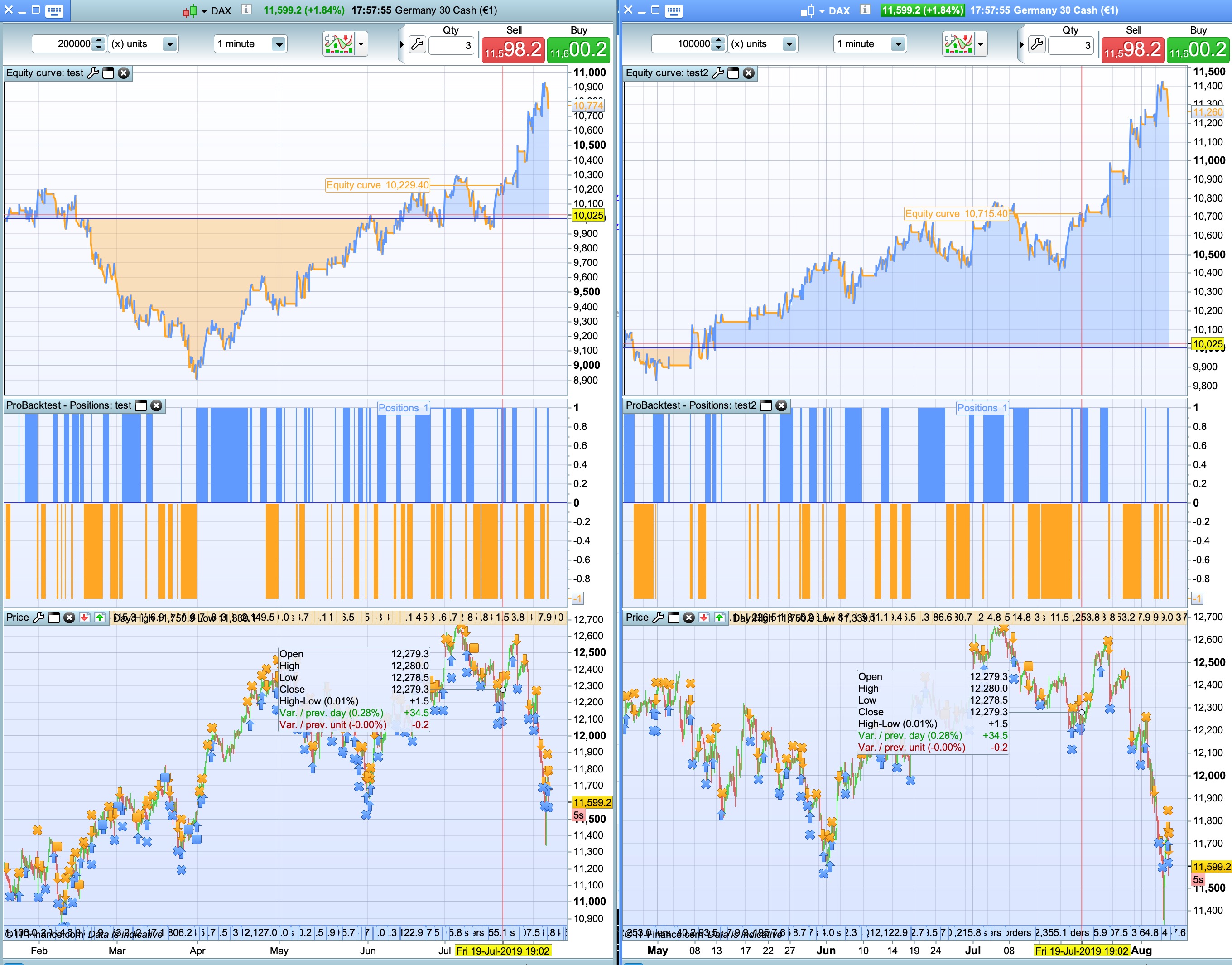

results with your code copy&paste; spread 1

left 200k, right 100k backtest

I found that for this strategy (5min) it’s better to use a different trailingstop, like the one used in dayopen straddle.

hi everybody

This morning, started “Vetorial DAX V5.0” upon my live account.

parameters :

once tradeschedule = 0 //[0]=full; [1]=morning; [2]=lunch; [3]=afternoon

once resetcounter = 1 //[0]=default; [1]=experiment (both connected by position criteria)

once enablesl = 1 // stoploss

once enablept = 0 // profit target

once enablets = 1 // trailing stop

once enablebb = 0 // bollingerband exit (add bb as indicator to have it visually) (all can be combined)

// when set display to 1, uncomment graphonprice to have affect visually (comment out graphonprice for trading)

once displaysl = 0 // stop loss

once displaypt = 0 // profit target

once displayts = 0 // trailing stop

once usetimecriteria = 1 // [1] included extra timeschedules not to trade

once holiday = 1 // [1] prevent trading on a german public holiday

once positionweekend = 1 // [1]=keep weekend position then ignore time below

once fridayclosetime = 225500 // close on last candle on friday to prevent gaps over weekend

once fridaylastentry = 174500

once closeonweekendprofit = 1 // close position in profit before weekend (to lower risk of gaps against position)

once closeonholidayprofit = 0 // close position in profit on a holiday

sl = 2 // % stoploss

pt = 1 // % profit target

positionsize=0.5

I’ll let you know about performance, about each week.

regards

vince

positionsize=0.5 ?

minimum is 1 contact on algos?

@StefanB

With IG markets and CFD Allemagne 30 the minimum position size is 0.5 (see the screenshot below).

Strange, Auto trading(algo?)

When I try to take less than 1 contract on DAX 30, PRT it does not work.

Manual trading works with 0.5 contract but not auto.

Hmm

With IG the minimum of contract is different in Demo and Real. For DAX its 0.5 real, 1 demo.

In real I dont have any problem with 0.5 contract with PRT on DAX.

auto trading does work with position size = 0.5 (DAX 30, at least)