I am a bit reluctant to post this because it seems to have a negative stance. Still it is far from that as it is the greatest hobby I ran into throughout my life.

Hopefully some decent answers :

I never test on Demo but for maybe not common reasons :

- For me this is a waste of time.

- Demo exhibits a lot more System Stops than Live (say 10 times more). N.b.: A System Stop is that the AutoTrading System is killed from the server – you will have to restart it.

- Demo does not force me to do it right.

- I calculate-in $ for failures (which are my own but which are also mainly broker errors; sometimes these are errors from PRT which relate to broker errors, but these are more rare.

Ad 2.:

This is harder to explain without many pages of writing. Almost nobody knows this because relatively few people run systems on Live and compare.

There is no usefulness in working around problems which exhibit in Demo only. This, while it takes months (you have my guarantee) to get along with Live and work around the issues

there. Issues : again stopped systems. Some issues can’t be worked around and will stay forever. You win some on it, you may lose some. N.b.: A System which is killed may leave you with a running system which is in a loss and which you can’t control automatically any more. Now its your turn again as a manual trader, but hey …

Ad 4:

Following the latter text, it will cost money because of “errors” (I don’t call those bugs because it is merely bad behaviour of the broker – this forum is full with examples (not for this topic/thread)). But it surely will cost money because of your own bugs or things you did not take into account.

A not-so-nice part of it all is that we have IG for broker and we have IBKR for broker and both have their own issues while both can not be dealt with by PRT decently. But, we can work around it, once you have experienced the issues. This will be different for everybody. And it is (thus) also different for IG and IB; when I had IG up and running and covered for all what I saw happening “to me”, I could start over with IB. Luckily I have a vast experience with IB and manual trading – I could see the issues coming before IB Autotrading was even live (now 3 months or so back). The time involved is almost immense, because it takes so much

throughput time. I mean, apply your solution and retry – and wait for the situation to occur and see whether it helped. Ah, it did not help ? then undoubtedly you will lose some money again. Oh, try it on Demo first ? no no, because there your system will blow up because of “demo reasons”.

You may well think that I over-exaggerate things, but all I do is do “more” than what is common. Still in the end it is your prospectus.

Ad 3.:

Only because you work with real money, you are forced to think in solutions, instead of letting it go and do something else. At least for me it works like that.

Maybe someone recognizes this : when you perform a dangerous hobby or sport, this can’t be practiced outside of the real game. I know this from driving Ralleys; there is no way to practice this as you will drive slower in order to avoid trees and such. With the real thing you don’t think of trees (and just run into them when it so happens). And so the practicing occurs when performing the real thing. Do it more and you will eventually

know more and be better at it. This in itself costs money; it must be calculated-in.

how long do you leave a system operating on a demo account before unleashing on LIVE?

Still it is a valid question, or at least a decent answer could be useful. Here is my attempt :

With the so-called knowledge that waiting for Demo to work out is a serious waste of time, plus the other arguments, the skill has thus to be in backtesting. Well, I suppose one could graduate on that when one has that under control. Of course I think I do, or else I should not be writing this. Still, mind you please, it is FWIW.

I don’t know how many pages the book will be that could explain the pitfalls, what to look at, what to avoid, how to teach yourself not to over-optimize, how to see that you did that after all while you were sure you did not … I guess that book will be thick. At least I can honestly say that I am still learning new things on a say weekly basis, which is quite crazy for someone who is working on it almost full time, for at least the past two years. These two years can be extended by another four, if I take into account the weekend-work I applied the first four years. Anyway, six years in total and I still learn.

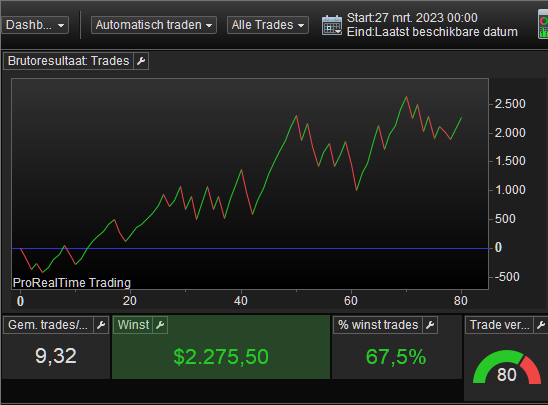

July 2022 was the first time I let go the first system on Live. This was not yet unattended, but at least I dared to do it. Next this required updates each week, sometimes more often because things plainly went wrong. Anyway, the versions of that system are “uncountable”, but let’s say close to a 100 – they all ran Live. Today they run really unattendedly since end of 2022. They do their work as observation post for things which occur at the broker (IG). In the mean time I started working on IB and today this is finished (that runs unattendedly for a month or so). When this week PRT will unveil the new quantities to trade, I will dive on to that immediately (currently this is limited because in Beta).

This seems to be for discouragement. But the opposite is true : if you want to earn some money by means of AutoTrading, then better think twice instead of thinking that you can let run

any system you find in here. Take into account the many years it will take, so that you won’t be discouraged half-way. See it as a hobby and not as a means of income.