I dont have intraday data for ASX stocks, better to provide examples of failed detection for Euronext, NYSE or NASDAQ stocks, thank you.

That filter: “volume traded is at least 1.5 time the previous day’s volume”

I consider the exchanged volumes of today (so only for the first 15 minutes) compared to the complete day previous ones, is it correct?

And since I’m counting the bars quantity, it is possible that there is a problem when there are missing bars, like in the chart you attached. I should try something different in this case..

EDIT: do you have at least some results on a 1-min timeframe with the screener? I’m asking because it seems to crash because before getting any result (i’m suspecting a division by zero error somewhere in ProScreener..).

Hi Nicolas,

The volume traded filter is supposed to compare (1) volume traded before the vwap/ema cross on the day it occurs (e.g. 10:15) with the volume traded at the same time (10:15) on the previous day. Sorry, my instructions should have been clearer on that aspect.

I guess it’s possible that it doesn’t respond when there are missing bars. But I would have thought that it would simply count the green ones and not count the others. I’m your hands here.

Pretty sure I’m getting results on a 1min TF in the screener. Will double check today.

I don’t have access to other markets, so not sure how to provide. I’ll keep working on that while you work on the bits above.

Best, JOMINA

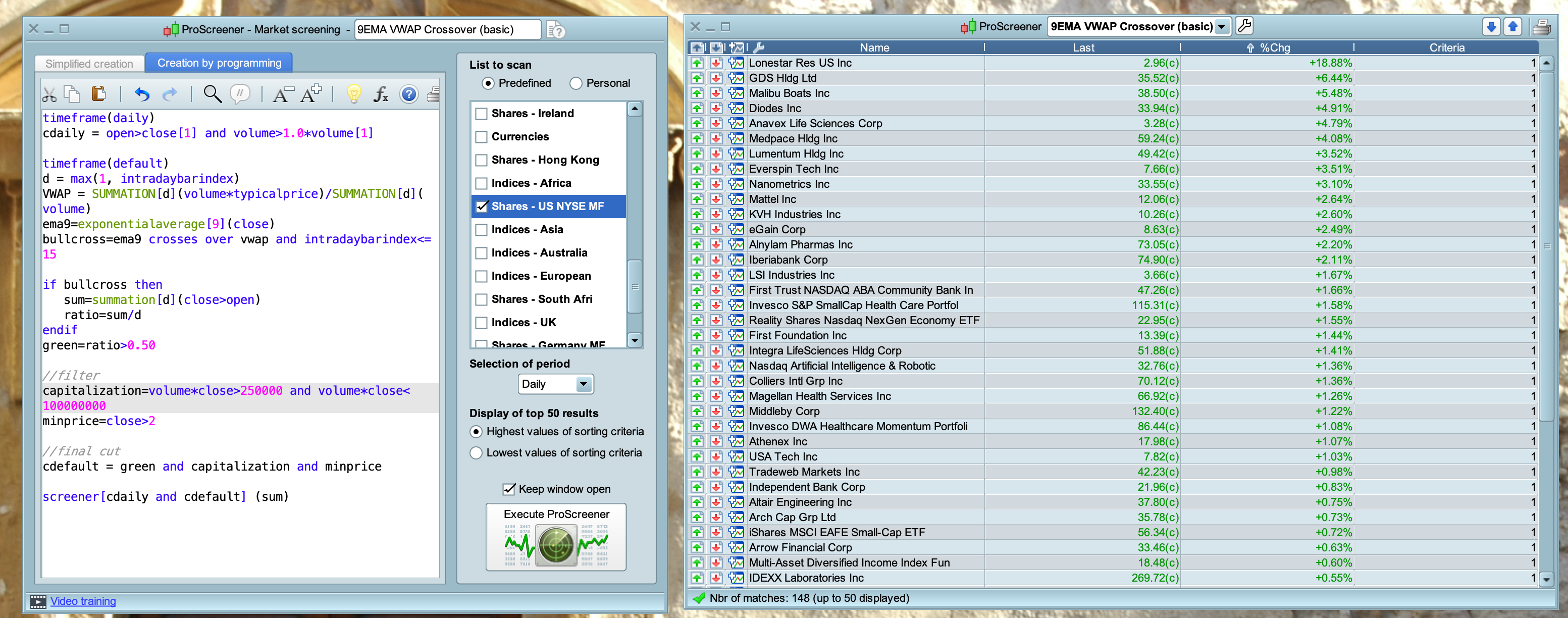

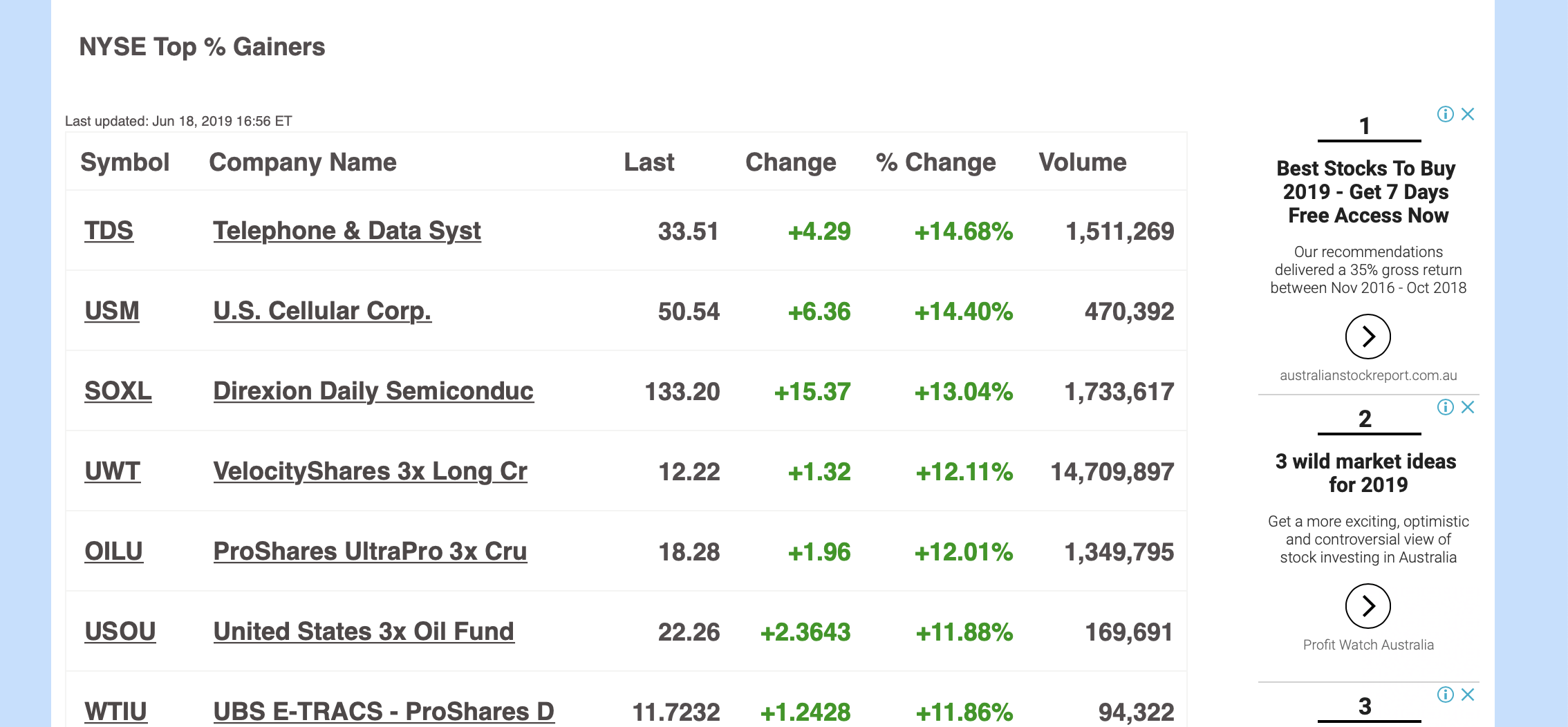

Nicolas, I’ve attached a few pics. The first is of the scanner picking up NYSE stocks. you’ll see that the top gainers list (online source) for the same day contains a stocks that haven’t been picked up. I’ve attached two examples.

Look forward to your thoughts on this.

The volume traded filter is supposed to compare (1) volume traded before the vwap/ema cross on the day it occurs (e.g. 10:15) with the volume traded at the same time (10:15) on the previous day

Far more complex! and impossible to achieve in timeframe such as the 1-minute one.. ProScreener only have 254 bars of data history, so we can’t lookback that far in the past to get the volumes traded the day prior the detection.

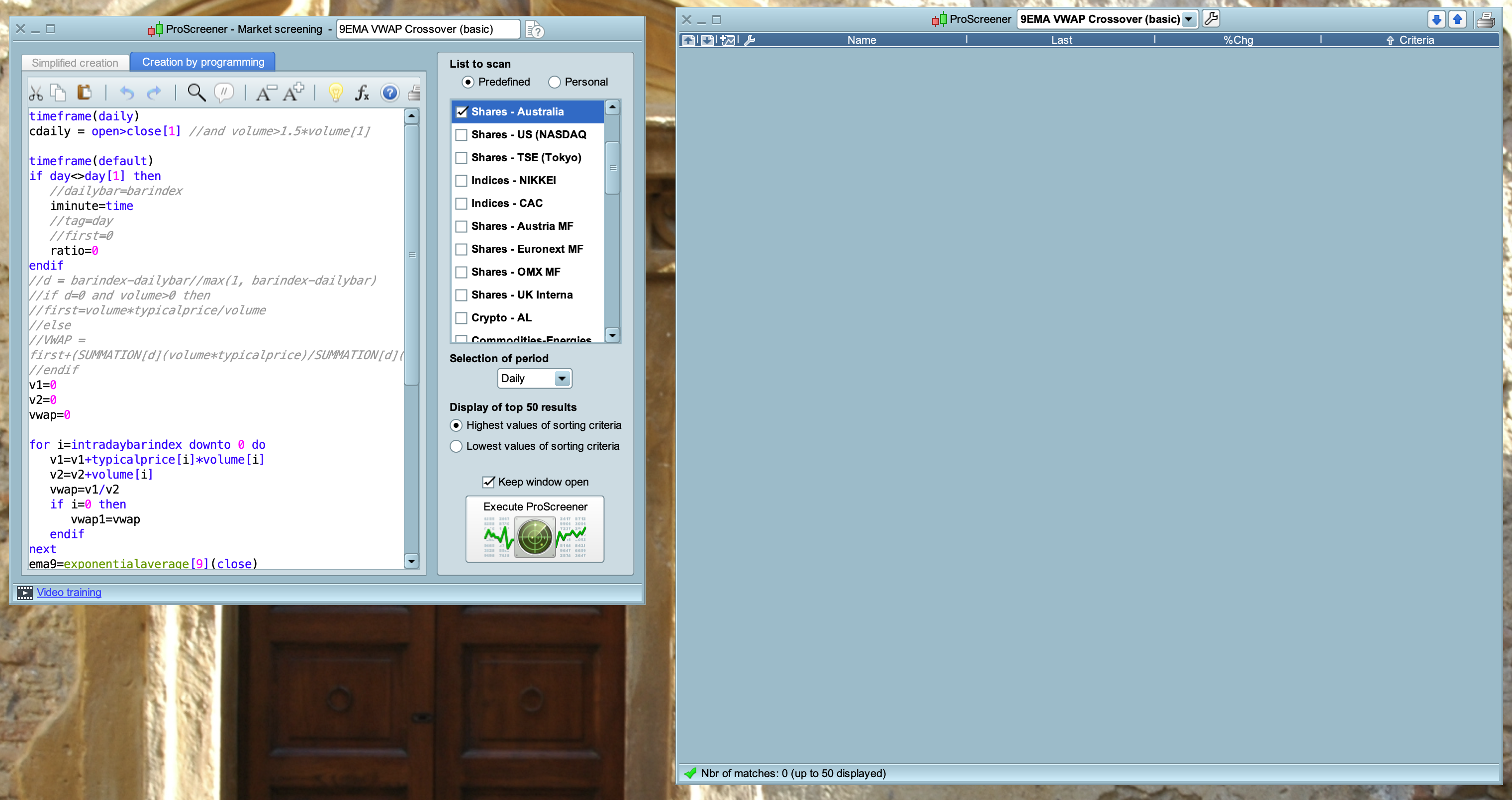

This is a new version, I deleted the volume condition:

timeframe(daily)

cdaily = open>close[1] //and volume>1.5*volume[1]

timeframe(default)

if day<>day[1] then

//dailybar=barindex

iminute=time

//tag=day

//first=0

ratio=0

endif

//d = barindex-dailybar//max(1, barindex-dailybar)

//if d=0 and volume>0 then

//first=volume*typicalprice/volume

//else

//VWAP = first+(SUMMATION[d](volume*typicalprice)/SUMMATION[d](volume))

//endif

v1=0

v2=0

vwap=0

for i=intradaybarindex downto 0 do

v1=v1+typicalprice[i]*volume[i]

v2=v2+volume[i]

vwap=v1/v2

if i=0 then

vwap1=vwap

endif

next

ema9=exponentialaverage[9](close)

bullcross=ema9 crosses over vwap1 and time-iminute<=15

if bullcross then

d=max(1,intradaybarindex)

sum=summation[d](close>open)

ratio=sum/d

tag=ratio

endif

green=ratio>0.75

//filter

capitalization=volume*close>500000 and volume*close<2000000

minprice=close>2

//final cut

cdefault = green and capitalization and minprice //and barindex-dailybar=intradaybarindex

screener[cdaily and cdefault] (tag)

Note that if the today’s bars count exceed 254, the screener will not work anymore on a 1-min TF, because of not sufficient history available to get the EMA cross condition on the first 15 minutes after market open.

Hi Nicolas,

Ran the screener today. No results whatsoever. Thoughts?

Seems that you ran it on a daily timeframe, while it is programmed for an intraday VWAP calculation.

Hi Nicolas,

I simply cut and paste your code into the pro screener. Is there something else I need to do at this end? Or does the code need to be tweaked?

If you want to get the results of a 1-minute chart, select that timeframe in the dropdown list of available timeframes in the ProScreener window.

Hi Nicolas, tried on both a 1m period and 5min period. Still nothing coming up.