can you post the code or the ITF ? thank you

The code is on the original post on Page 1.

Try to add a a defparam preloadbards = 1000 at the top of the code.

You should also calculate your position size only before entering a new order, because now the “n” variable is calculating on each bar, even if you don’t meet the requirement to open a new position at market. So move the martingale code before line 79 and 91.

Now it’s working! About calculating on every bar is useless, but could make it calculate only if Cbuy or Csell is true to don’t duplicate the 15 rows of code 🙂

Good morning,

The minimum stop this morning is 1095 point see attached picture

Haha that’s perfect for a scalp code!

I’m quite puzzled by the result between demo and backtest.. They are really different.. regarding the candles for example.. thus, the result..

it makes me say that the strategy on 1 second is very difficult.. especially in these time and this current volatility !

i doubt the transmission time of the order until IG platform.. , the spread, volatility.. and so one..

it takes time to perfect this strategy using volatility indicator…

if you use this strategy, i’m curious to have your feelings..

True, I don’t think it’s the best to go with 1 sec strategy. I will have it on my demo proorder to see how it’s work from now on with the spread and volatility.

Have you tried re-optimise of the 1 Sec Strategy 1 time every day or at least 1 time every 2 days?

There are 86,400 1 x second bars in a 24 hour period.

Wouldn’t you, for example, re-optimise a 1 x hour TF Strategy after 14 years (86,400 1 x hour bars = 14.4 years)

@grahal

you are right but my goal is to not re-optimize every day

when i will be on the top of the mountain, i will not have my computer to do it.. 🙂

but regarding the result, even within a day, not the same result with this f…king volatility.. 😉

It was too good to have 8% per day..

i will let in run in demo… “Renko is maybe the graal for this unit.. ” i’m going to try some tricks to optimize the boxsize and why not turnaround strategy with renko (after x green box or red box.. ), and M top or W bottom

SET STOP pLOSS 5

trailingstart = 15 //trailing will start @trailinstart points profit trailingstep = 5 /

Did you do a decent backtest with tick by tick enabled (very important tick by tick enabled, useless without)?

With SL of 5 and TS of 15 and a step of 5 then nearly all trades will get stopped out as there is not enough room for retrace etc.

Even on a 1 sec TF, a Strategy needs room to allow for fib retrace; unless it’s a true Scalper … but until we get Arrays working I can’t see us having a true scalper??

@Grahal

of course, tick by tick every time

Sure, you are right about the breathing of SL..

I played a little.. initial SL, trailing and treshold updated

initial SL, trailing and treshold updated

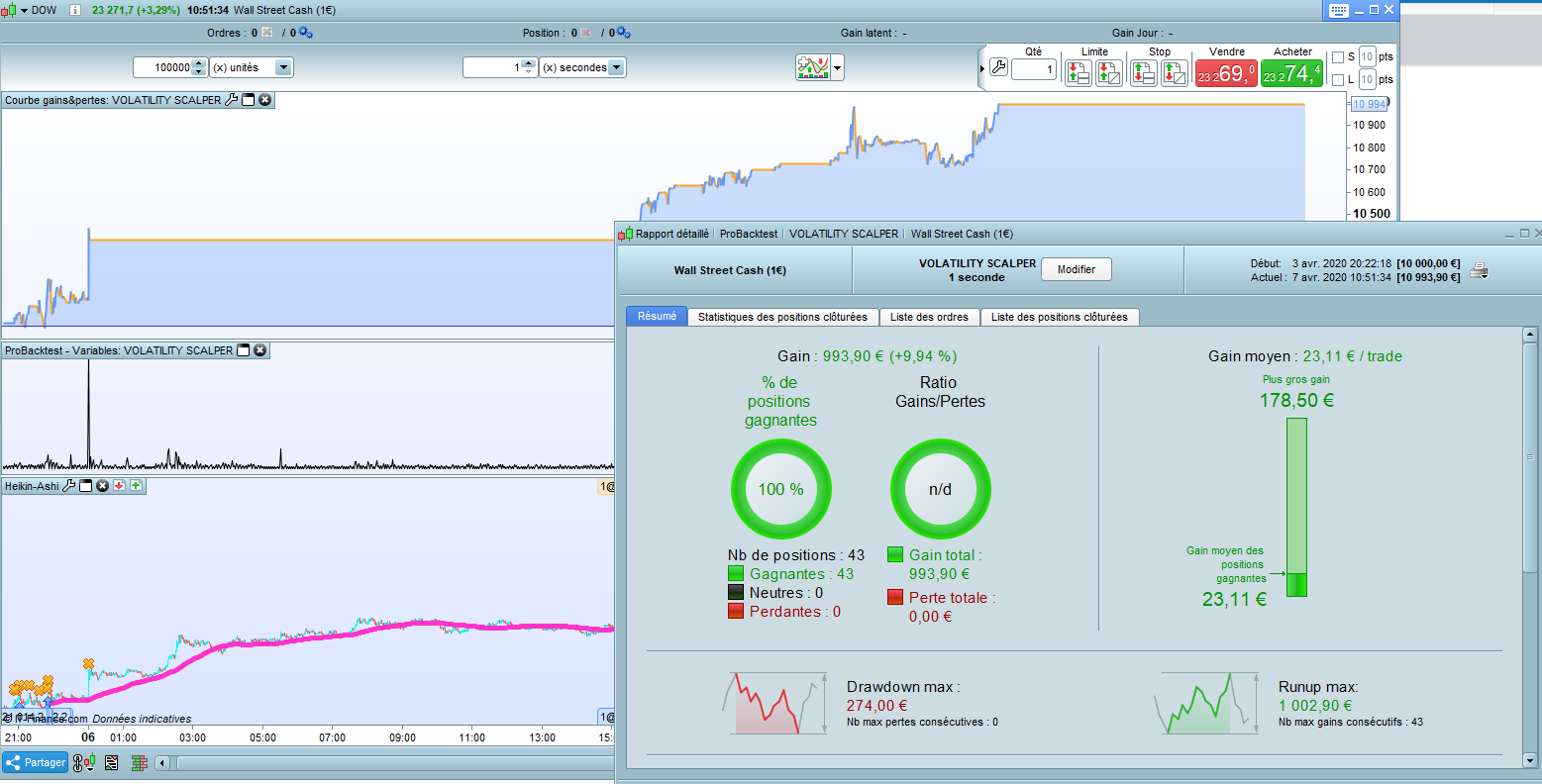

Looks well good (43 out of 43!) … you going to share your settings please?

Did you also make any other changes?

threshATRPeriod = 4

SET STOP pLOSS 300

trailingstart = 15 //trailing will start @trailinstart points profit

trailingstep = 7 //trailing step to move the “stoploss”

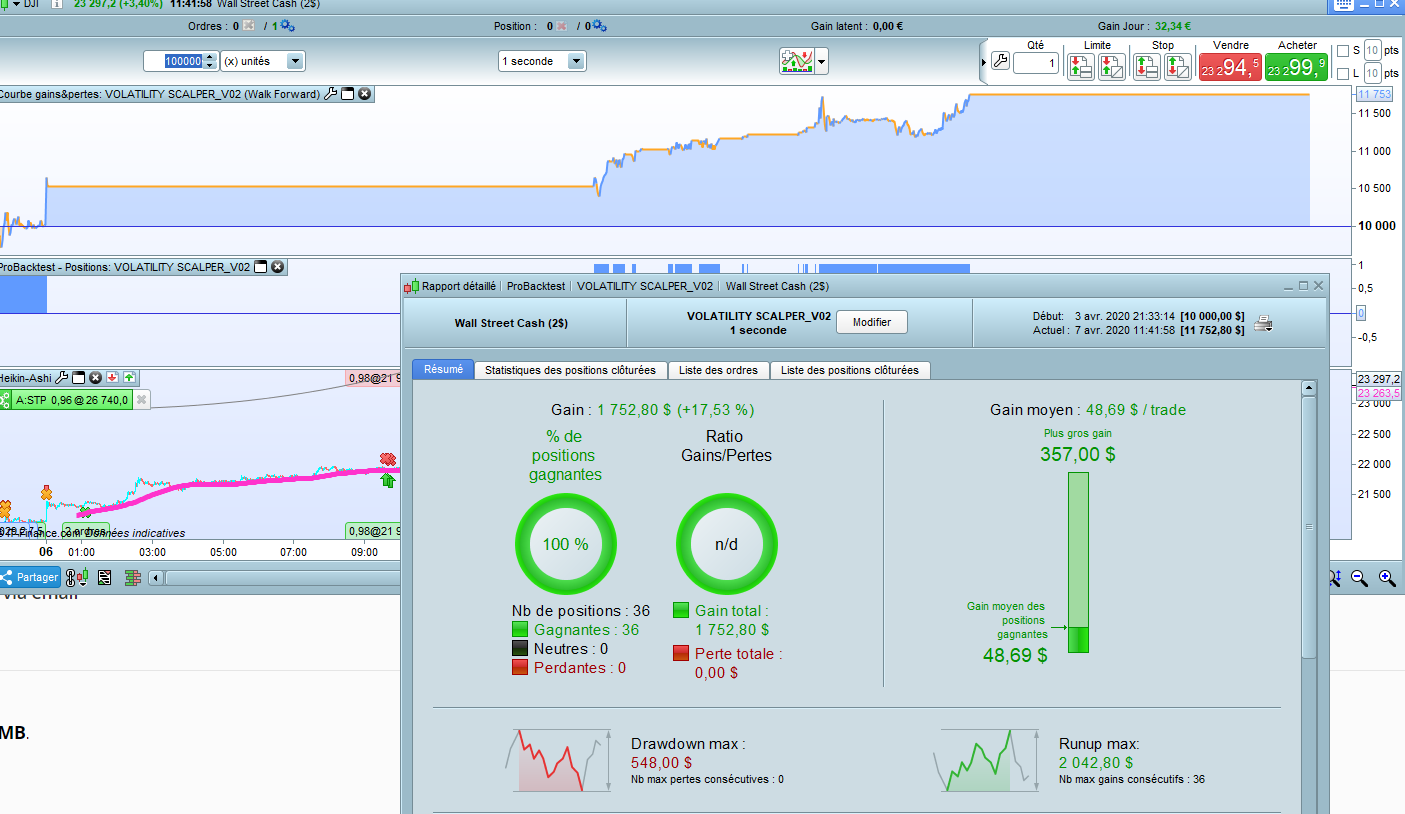

last test, with DJI 2$, spread 2

i just have a conscience problem with the initial stop.. i have a dilemma between this high value of SL or to change it with ATR.. but results aren’t same

Do you have an idea to use good calculation of ATR for initial stop ? or maybe tt include an ATRS too

************************

Typical ATR time periods used vary between 5 and 21 days. Wilder originally suggested using 7 days, short-term traders use 5, and longer term traders 21 days. Multiples between 2.5 and 3.5 x ATR are normally applied for trailing stops, with lower multiples more prone to whipsaws.

The default is set as 3 x 21-Day ATR.

Closing Price is set as the default option. The alternative is HighLow (see Formula below).

See Indicator Panel for directions on how to set up an indicator — and Edit Indicator Settings to change the settings.

Trailing stops are normally calculated relative to closing price:

- Calculate Average True Range (“ATR”)

- Multiply ATR by your selected multiple — in our case 3 x ATR

- In an up-trend, subtract 3 x ATR from Closing Price and plot the result as the stop for the following day

- If price closes below the ATR stop, add 3 x ATR to Closing Price — to track a Short trade

- Otherwise, continue subtracting 3 x ATR for each subsequent day until price reverses below the ATR stop

- We have also built in a ratchet mechanism so that ATR stops cannot move lower during a Long trade nor rise during a Short trade.

The HighLow option is a little different: 3xATR is subtracted from the daily High during an up-trend and added to the daily Low during a down-trend.

hello

I copy the code from page 1 but it doesn’t work. can you post the code again with the last modifications so that I test in my turn? thank you very kindly Bertrand

Thank You for sharing.

It be good if you can get some reasonable performance from Shorts only.

Reason: DJI has had a good couple of days for Longs, but it will turn down and unless a System can cope with Shorts also then Profit may turn into a Loss of it all?

It is good to show all positions on screen shots (not double up / hide under a screen shot as you have ) as probably your 43 out of 43 are all Longs?? So maybe, just maybe, your settings may not stand up to a downturn? But then again, this is why I have come round to a daily oprimisation … so settings keep up with events / price action?

Heck if I was making consistent money because of it … I would optimise every hour!? 🙂

Re Stops … have you tried SuperTrend or Parabolic SAR … you can optimise the settings of these Indicators and if they work they are an easy bit of code to pop in to a System to Filter on Entry and use as a dynamic Stop for Exit?

Better still if the above work on default settings as the herd would be in and out of default settings, but it’s surprising how much different results can be when the settings are optimised.

not double up / hide under a screen shot

Btw I didn’t mean that you were trying to hide anything from us … bad choice of words on my part, apologies! 🙂