Paul

PaulParticipant

Master

Here’s the code I was thinking about. In general I don’t like to keep a position over the weekend, but if there is one. Put the gap 50 to 0 to have it always active with or without positionperformance.

if onmarket then

if dayofweek=0 and (hour=0 and minute>=57) and abs(dopen(0)-dclose(1))>50 and positionperf(0)>0 then

if shortonmarket and close>dopen(0) then

exitshort at market

endif

if longonmarket and close<dopen(0) then

sell at market

endif

endif

endif

I think this could be very useful! This fraiday I had an order that starts at 20:10 and was about to get an over weekend position so I cuted i in the positive as I didn’t want to keep it!

@Paul, do you have any ideas that you’d like to test or changes to make that you think of and that I could try and give you feedback on to get more gain. I run out of ideas…

PaulParticipant

Master

well atm I ran out of idea’s too. What I wonder instead of increasing the gains, not to prevent a bad entry, but how to react to a bad entry such as today. Just to watch the market going opposite and al you can do is hope it will reverse course.

Something like if there are no certain gains made after the position is entered, close after xx bars=time.

here’s something to test 🙂

So you need to see a gain of atleast 20 points in 3 hours after a position is taken or else close it.

I don’t know if I want to go down this road with curvefitting. There’s already plenty!

if longonmarket and highest[barindex-tradeindex(1)](high)-tradeprice(1)<20 and barindex-tradeindex>80 then

sell at market

endif

if shortonmarket and tradeprice(1)-lowest[barindex-tradeindex(1)](low)<20 and barindex-tradeindex>80 then

//exitshort at market

endif

THAT’S EXACTLY WHAT I WAS TRYING NOW! 😀

I think it could be a great way to cut some positions sooner to prvent losses 🙂

I am also trying to get this system with a stochastic momentum index more than bars, I’ll try both and see 😉

And in you’re code you wrote 80 bars which is 4 hours and not 3 just ! 😉

I tried this, bit better ratio but less gain obviously….

//SL above 0 if more than X hours and positive

SLafterXhours=0

if longonmarket and barindex-tradeindex>60 then

if close-tradeprice(1)>=2 then

sell at SLafterXhours STOP

endif

endif

if shortonmarket and barindex-tradeindex>40 then

if tradeprice(1)-close>=2 then

EXITSHORT at SLafterXhours STOP

endif

endif

PaulParticipant

Master

I would refrain from using stop orders and use market, especially on fast timeframe. Then you don’t have to mess with rejections etc.

Actually there is already an already exit available in the code but it wasn’t used. (spreaking v3p5)

Maybe this one can be improved? Short was already active but for long was not used. If it was active with value minrangedistL=1 it would h’ve exit long way earlier.

Using it as is, with addition that if there is not enough gains, the minrangedistance gets reduced. So start at 3 and reducing it to 1.

// reversal exit

once longexit =1

once shortexit=1

if longexit then

if longonmarket then

minrangedistL=1

cl1=close<open and close[1]<open[1] and close[2]<open[2]

cl2=(close=low or close[1]=low[1] or close[2]=low[2])

cl3=(range>(close/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL)

if cl1 and cl2 and cl3 then

sell at market

endif

endif

endif

if shortexit then

if shortonmarket then

minrangedistS=1.5

cs1=close>open and close[1]>open[1] and close[2]>open[2]

cs2=(close=high or close[1]=high[1] or close[2]=high[2])

cs3=(range>(close/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS)

if cs1 and cs2 and cs3 then

exitshort at market

endif

endif

endif

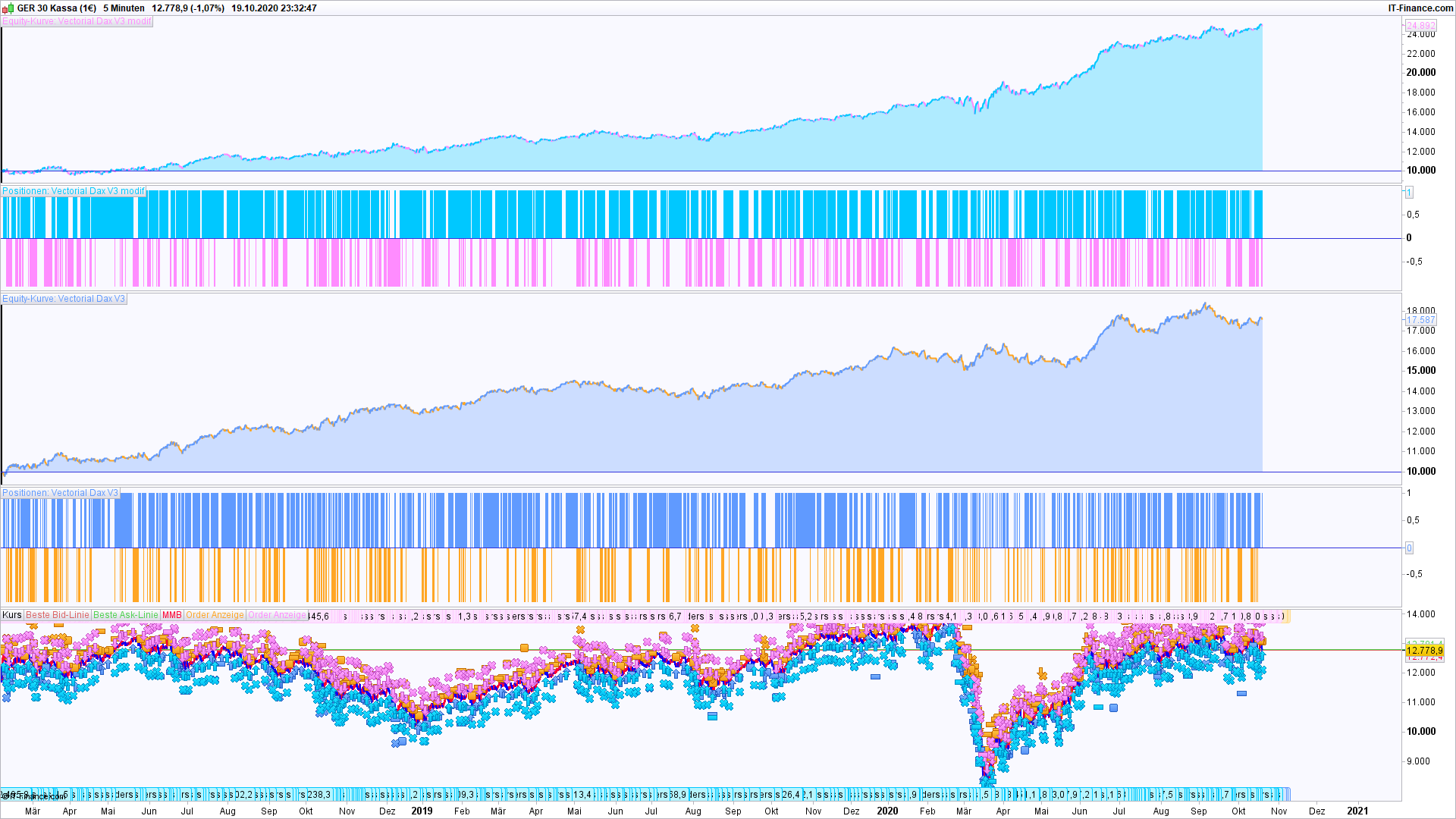

Just replaced the trailing stops with an ordinary trailing stop, and added a new profit taking routine to the old version Vectorial Dax V3 (04/13/2019, #96328). Code is shorter, and after some nice curve fitting, gain has doubled.

PaulParticipant

Master

an ordinary trailing-stop is not a ptrailing stop used in one strategy as in general it’s not recommended. But it’s good to take a step back sometimes and have a short & effective code. Whatever works!

LR = LinearRegression[1]

LRslope = LR[0] - LR[1]

LRslopebuy = LRsplope > 0

I added this condition for the uptrend. Yesterday’s trade was really catastrophic..

It’s another version of Vectorial .. but maybe an idea around that

The yesterdays SL was the 4th full SL (2%) and the 8th SL bigger than 1% this year. Actually the profit rate in October is bad. To many small winners on one side, and to many loosing trades on the other side. But up to now, this month ist not negativ. But also, it don´t needs one more big looser again.

Hello Paul,

You mean like that? Because implementing it this way didn’t get pretty good results…

//-------------------------------------------------------------------------

// Code principal : Vectorial DJ 3 min V3

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Code principal : DJ 3m Vectorial V3

//-------------------------------------------------------------------------

// VECTORIAL MM - DJ 3m

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1

ENDIF

if MM = 1 then

ONCE startpositionsize = .2

ONCE factor = 10 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.05) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.05)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // IG first tier margin limit

ONCE maxpositionsize = 550 // IG tier 2 margin limit

ONCE minpositionsize = .2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = startpositionsize + Strategyprofit/(factor*margin)

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = minpositionsize //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = maxpositionsize// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

//HORAIRES DE TRADING

Ctime = time >= 153000 and time < 210000

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

i1 = HistoricVolatility[10](close)

c1 = (i1 >= 0.06)

ONCE PeriodeA = 4

ONCE nbChandelierA= 30

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CB1 = ANGLE >= 32

CS1 = ANGLE <= - 44

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 30

ONCE nbChandelierB= 35

lag = 0

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CB2 = (pente > trigger) AND (pente < 0)

CS2 = (pente CROSSES UNDER trigger) AND (pente > - 0.5)

mx = average[110,0](close)

CB3 = mx > mx[1]

mx2 = average[20,0](close)

CS3 = mx2 < mx2[1]

//ENTREES EN POSITION

CONDBUY = CB1 and CB2 and CB3 and CTime and c1

CONDSELL = CS1 and CS2 and CS3 and Ctime and c1

//POSITION LONGUE

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 2.6

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort positionsize contract at market

SET STOP %LOSS 0.6

ENDIF

//SET TARGET %PROFIT 2

//Break even

breakevenPercent = .13

PointsToKeep = 1

startBreakeven = tradeprice(1)*(breakevenpercent/100)

once breakeven = 1//1 on - 0 off

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

// reversal exit

once longexit =1

once shortexit=1

if longexit then

if longonmarket then

minrangedistL=1

cl1=close<open and close[1]<open[1] and close[2]<open[2]

cl2=(close=low or close[1]=low[1] or close[2]=low[2])

cl3=(range>(close/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL or range[1]>(close[1]/1000)*minrangedistL)

if cl1 and cl2 and cl3 then

sell at market

endif

endif

endif

if shortexit then

if shortonmarket then

minrangedistS=1.5

cs1=close>open and close[1]>open[1] and close[2]>open[2]

cs2=(close=high or close[1]=high[1] or close[2]=high[2])

cs3=(range>(close/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS or range[1]>(close[1]/1000)*minrangedistS)

if cs1 and cs2 and cs3 then

exitshort at market

endif

endif

endif

I just tried both of your versions with 200k . It’s looking quite good but I wouldn’t let it alone in real. The profit factor is too small for a 45% winning strategie…!

I tried to change few things but doesn’t work 🙁

PaulParticipant

Master

Tanou something like that, but using long didn’t work. How’s short only?

ps nobody uses WF or HE?

In the code that I put above both long and short were active if I’m not wrong!

What do you mean by WF and HE?