Another one

Yes, I’m in. It seems the USTech100 version works much better than the latest DAX(6.2). I would put it on the trailing system that is more conservative.

Paul

PaulParticipant

Master

my approach is wrong

tradingtimes. Start dax till close s&p etc.

take every signal with no exit criteria or maybe just a stoploss. Every signal has to be of the same weight.

Create code which takes same positions as with cumulateorders=true but maintaining max 1 position

optimise or use wf and then decide exit criteria

sys-05-vectorial-us100-v5.0p

Is this the latest for US tech 100? Which one are people using now?

@Paul I cannot find any Vectorial version with v100p in the strategy title … as you show in the images you post above.

Is v100p a new version that you have developed following your new approach that you detail above?

Might you consider sharing your v100p version please?

PaulParticipant

Master

Hi GraHal

yes it’s a new approach in testing and I just picked a new version number to start off.

I don’t like to share it because it could be garbage but I can explain a bit more my effort.

A few posts back I mentioned that it could be out of sync when restarting a system or manually taking profit.

Not only that, I experienced it live, taking profit (small in hindsight), restarting the system and then it bought on a new signal on the very top before a drop and voila exit on stoploss. It would have been better to have let the original position running on trailing stop but then you wouldn’t have seen the bad buy signal on the top.

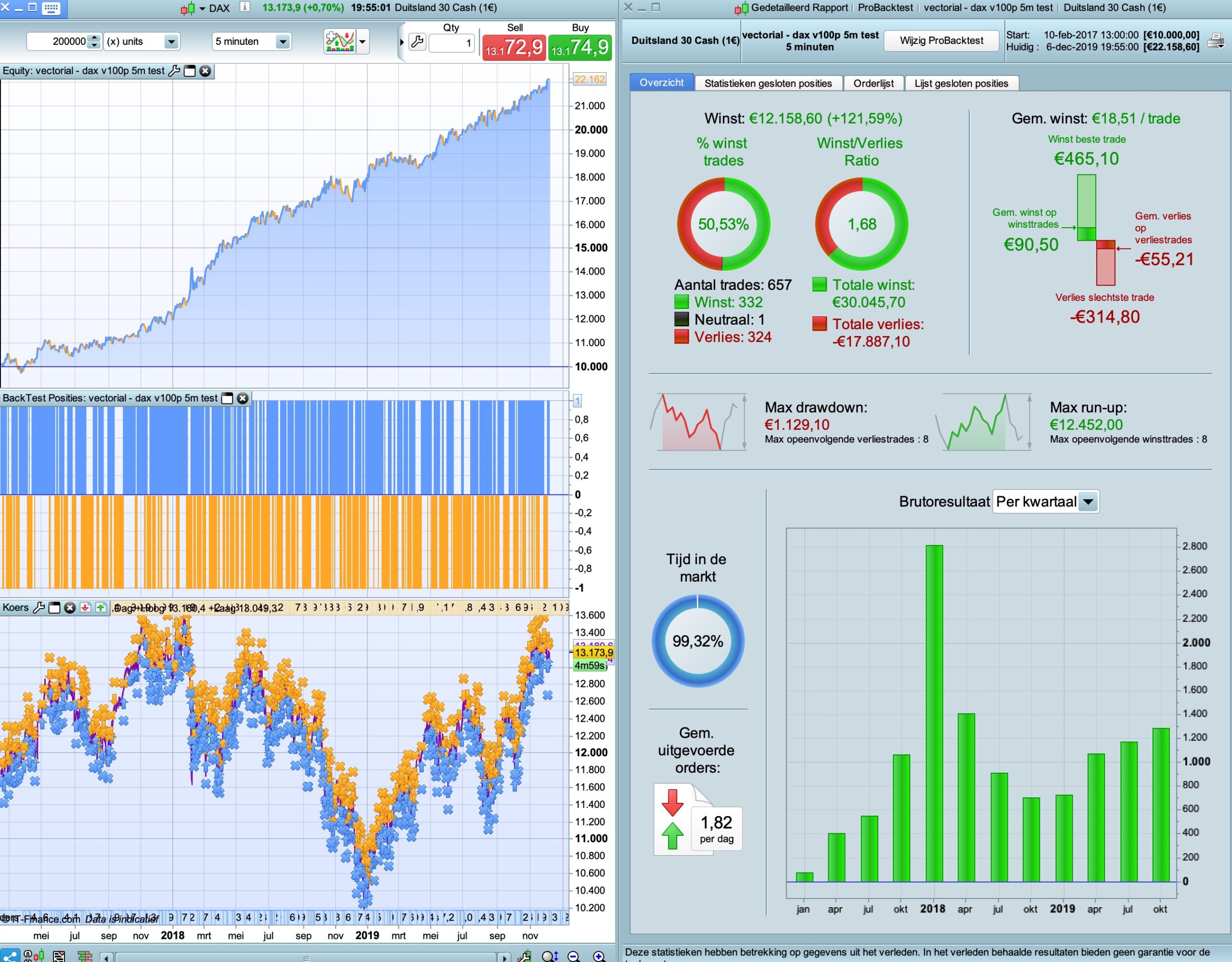

I wanted to see action on every signal. If in long position and get a signal in the same direction, close it regardless profit or loss and restart it again instantly.

Maybe that sounds wrong, but it gives different importance to every signal. The original code has be adapted a little not have many signals in a very short timeframe. The end result is a combination of pingpong between signals between 0800 to 2230 and the last position carried over to next trading day. The results in the pic are only less then 70 lines of code.

So it’s this approach above or separating long and short and still applying concept above, with normal exit-criteria like a ts and close & re-enter on same signal.

restarting the system and then it bought on a new signal on the very top before a drop and voila exit on stoploss.

That is something that a quick check with my robustness testers would have possibly highlighted. It is very easy to create a strategy that looks great but then if you start it just one bar later or two bars later then it gets completely different trades and performs badly. Randomly picking times to trade can tell us an awful lot about whether we are over optimised or just got lucky with our trade sequencing.

PaulParticipant

Master

With this approach the robustness tester shouldn’t have any big bad surprises I hope!

I will give it go with the tester and post results in that topic.

I feel strongly that we should not make emotive criticisms about Auto-Systems submitted on this Thread, any other Thread or the Library.

System Authors have spent many many hours and been kind enough to share with us their best efforts. It can be very demoralising when best efforts are described as garbage!?

Harshly criticising Systems that are ‘not putting dollars in out pockets’ will, over time, result in less and less System being shared!?

We can learn a lot from mistakes if we analyse what went wrong and then ensure we refine towards perfection.

How much better to spend time (and learn) and offer improvements (however small) rather than condemn Systems freely shared with us?

Hello everyone,

Most people who have a bad review, are people who do not share.

I am here to complete my learning, to give what I have learned and to learn from others.

I’ll be back in January after the release of PRT V11 with modifications made on vectorial.

Because there will be more history.

cordially

Hello everyone,

I wanted to give you my experience feedback on the strategy of Fifi743 (Vectorial DAX V.6) since October.

I do not understand some people who say that this strategy is overoptimized. It has nevertheless been tested by Vonasi with its robustness tester. And the result was good.

For me, all the trades in real correspond to the backtest. Of course, the month of November was not good but the month of October is good. In November, this is the first time that volatility has been so low and trendless every day. The robot does not like this configuration. As soon as the trend starts again, the robot starts to win as in the past. I think we need more time to draw a conclusion from Fifi’s robot.

I continue for the month of December where volatility will be greater.

It has nevertheless been tested by Vonasi with its robustness tester. And the result was good.

It was OK results in the robustness test but my personal feeling was that with so many combinations of entry conditions that it is actually a very good exercise in data mining on a data sample. If you write a strategy that says this happened once and it resulted in a profit so I will include that in my strategy and then this other thing happened once and it resulted in a profit once so I will include that as well then even a robustness test is going be pointless as all the trades are data mined so they are all good and the robustness test just randomly chooses bits of data mining. The future is unlikely to be the same as the past that we data mined though and it seems from the results described from those forward testing the strategy that that is being proven true.

As for insulting and rubbishing the work of others I agree that just calling something ‘garbage’ is unacceptable – however if you call it garbage and then give valid reasons for why you feel it is garbage then that is perfectly OK IMHO.

You say all Vonasi.

I have much bad operations, and i quit this operations… The results is good.

Tachaaaaan!!!

But in the future the results are bad results.

Tatatachaaaaan!!!

Every signal has to be of the same weight. Create code which takes same positions as with cumula

I’m using it live right now, since 2 weeks. Important to mention that I launch all my systems with a fixed position size of 1, and never reinvest the profits.

So far one stop loss hit (around 200points) and one green position opened still now (+86points).

I really think there is a good edge on this strategy, both for NAS and DAX, but we can’t expect it to run perfectly and with no red days. I’ll try to get back and modify V2s as they seem more “open” to me.

PaulParticipant

Master

us-versions from page 12 doing well. (backtest from 24 july from day of posting strategy)