Hola Nicolás,

A ver si es tan amable de traducir este código de mq4 a PRT.

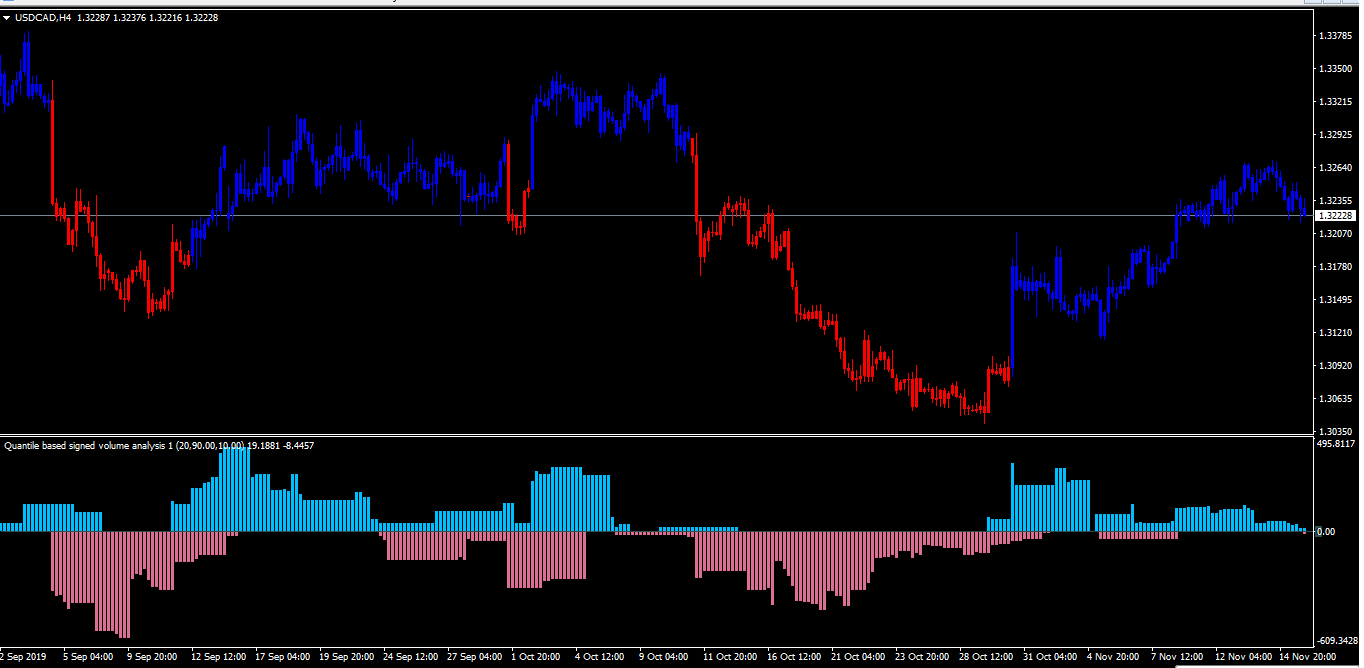

Se basa en el indicador ATR y el volumen.

Creo que sería un indicador de gran utilidad.

Un saludo y gracias.

//+------------------------------------------------------------------+

//| Quantile based signed volume analysis |

//+------------------------------------------------------------------+

#property copyright

#property link

#property indicator_separate_window

#property indicator_buffers 2

#property indicator_color1 DeepSkyBlue

#property indicator_color2 PaleVioletRed

#property indicator_width1 2

#property indicator_width2 2

//

//

//

//

//

extern int Periods = 20;

extern ENUM_APPLIED_PRICE Price = PRICE_CLOSE;

extern double UpQuantilePercent = 90;

extern double DownQuantilePercent = 10;

extern double AtrUpperPercent = 75;

extern double AtrLowerPercent = 25;

extern bool LimitToZeroes = true;

extern bool UseRealVolume = false;

//

//

//

//

//

double bufferUp[];

double bufferDn[];

double quantUp[];

double quantDn[];

double prices[];

double trend[];

//+------------------------------------------------------------------+

//| |

//+------------------------------------------------------------------+

//

//

//

//

//

int init()

{

IndicatorBuffers(6);

SetIndexBuffer(0,bufferUp); SetIndexStyle(0,DRAW_HISTOGRAM);

SetIndexBuffer(1,bufferDn); SetIndexStyle(1,DRAW_HISTOGRAM);

SetIndexBuffer(2,quantUp);

SetIndexBuffer(3,quantDn);

SetIndexBuffer(4,prices);

//

//

//

//

//

Periods = MathMax(Periods,1);

UpQuantilePercent = MathMax(MathMin(UpQuantilePercent,100),0);

DownQuantilePercent = MathMax(MathMin(DownQuantilePercent,100),0);

IndicatorShortName("Quantile based signed volume analysis 1 ("+Periods+","+DoubleToStr(UpQuantilePercent,2)+","+DoubleToStr(DownQuantilePercent,2)+")");

return(0);

}

int deinit() { return(0); }

//+------------------------------------------------------------------+

//| |

//+------------------------------------------------------------------+

//

//

//

//

//

int OnCalculate (const int rates_total, // size of input time series

const int prev_calculated, // bars handled in previous call

const datetime& time[], // Time

const double& open[], // Open

const double& high[], // High

const double& low[], // Low

const double& close[], // Close

const long& tick_volume[], // Tick Volume

const long& volume[], // Real Volume

const int& spread[] // Spread

)

{

int counted_bars=IndicatorCounted();

int i,limit;

if(counted_bars<0) return(-1);

if(counted_bars>0) counted_bars--;

limit=MathMin(Bars-counted_bars,Bars-1);

//

//

//

//

//

for(i=limit; i>=0; i--)

{

prices[i] = iMA(NULL,0,1,0,MODE_SMA,Price,i);

quantUp[i] = iQuantile(Periods,UpQuantilePercent ,i);

quantDn[i] = iQuantile(Periods,DownQuantilePercent,i);

//

//

//

//

//

bufferUp[i] = 0;

bufferDn[i] = 0;

for (int k=0; k<Periods; k++)

{

double atr = iATR(NULL,0,1,i+k);

double sign = 0;

if (prices[i+k] > Low[i+k]+atr*AtrUpperPercent/100.0 && prices[i+k]>prices[i+k+1]) sign = 1;

if (prices[i+k] < Low[i+k]+atr*AtrLowerPercent/100.0 && prices[i+k]<prices[i+k+1]) sign = -1;

if (!UseRealVolume)

{

if (prices[i+k] > quantUp[i+k]) bufferUp[i]+= sign*tick_volume[i+k]*prices[i+k]*atr;

if (prices[i+k] < quantDn[i+k]) bufferDn[i]+= sign*tick_volume[i+k]*prices[i+k]*atr;

}

else

{

if (prices[i+k] > quantUp[i+k]) bufferUp[i]+= sign*volume[i+k]*prices[i+k]*atr;

if (prices[i+k] < quantDn[i+k]) bufferDn[i]+= sign*volume[i+k]*prices[i+k]*atr;

}

}

if (LimitToZeroes)

{

bufferUp[i] = MathMax(bufferUp[i],0);

bufferDn[i] = MathMin(bufferDn[i],0);

}

}

return(0);

}

//+------------------------------------------------------------------+

//| |

//+------------------------------------------------------------------+

//

//

//

//

//

double quantileArray[];

double iQuantile(int period, double qp, int i)

{

if (ArraySize(quantileArray)!=period) ArrayResize(quantileArray,period);

for(int k=0; k<period && (i+k)<Bars; k++) quantileArray[k] = prices[i+k];

ArraySort(quantileArray);

//

//

//

//

//

double index = (period-1)*qp/100.00;

int ind = index;

double delta = index - ind;

if (ind == NormalizeDouble(index,5))

return( quantileArray[ind]);

else return((1.0-delta)*quantileArray[ind]+delta*quantileArray[ind+1]);

}