Thanks I’ll just keep logging in and out whenever the back test issue happens then.

An that’s what I thought would happen when long reverse into short strategies, if things go well and you’re in the market 99% of the time then that should equal more profits.

Plus if you short a market you are already long on you are using way less margin over shorting a market you’re not long on and the trade you placed short isn’t any less likely to succeed just because you a short both trades could eventually be profitable.

“Trouble is that profitable trade, made during simulated trades” that’s not an issue with me personally I have the same points (take profit) for every strategy I have. So the same take profit, same stop loss and same steps and then I just the profit factor uniformly depending on the market conditions.

So it could make a million I don’t care lol just give me my £25 or £40 or whatever per trade and as long as I win a certain percentage of the time I’m good. I find this evens out the drawdowns as well as it really helps in ranging markets. The amount of times in even down markets a price goes up 8 points before falling can be significant income with smaller take profits (that’s if you can keep getting in at a the bottom of the range).

I’m like that too, I never delete anything. I always feel like you could remix your worst strategy into your best one day or it could be perfect for a future market condition.

Well if you have it then it’s part of your intellectual property and people did put them on here to share 🙂

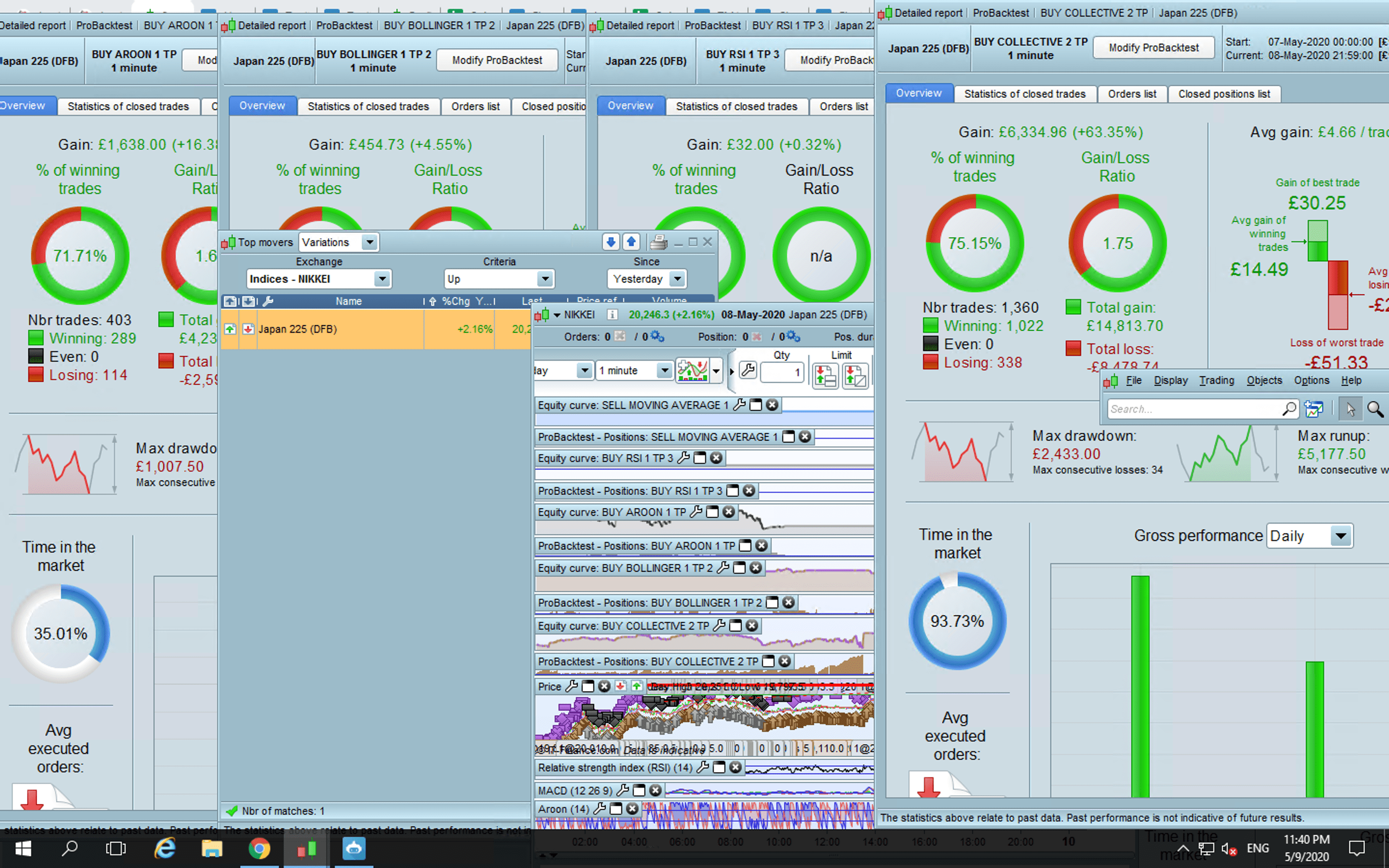

So with the 4,877 you tried on the Nikkei what would you class as consistent profitable strategy that you haven’t found? So would that be consistent profitable for a week, a month a year? How long has your best algo on the Nikkei been consistent profitable for?

I tried 4 of mine on the Nikkei and it says on Friday my best one would’ve made 6.5k from a 10k start so 16.5k and the one I added that you looked would’ve made 1.6k from a 10k start on Friday so 11.6k. So who knows how long that would be profitable on there for but at least for the moment it looks like I’ve got two strategies that may crossover well.

I’m still waiting for IG Sponsored by Pro Real Time to get approved once that’s done I’ll have access to more then one day of back testing on 1 minute charts and I can create some strategies specifically for the Nikkei but for the mean time it looks like there’s potential there.

But with all of these people on the forum trying, isn’t there someone who found a consistently profitable algo for the Nikkei who’s selling it? Isn’t that what the market place is for? Or does no one claim to have cracked the constantly profitable code on it yet? Or are their codes only profitable for short periods?

“Do strategies created on quantreex work on PRT??”

Nope not at all but I’ve found that quantreex is the best place to create strategies minus them having way less indicators purely based on the fact you back test 150 strategies on 1 stock at the click of a button or 150 stocks on 1 strategy. So even bad strategies tend to do ok on 1 in 150 stocks and then within around 10 minute for me (or however long it takes you to copy and paste 150 new tickers 10 different times) you could test each strategy on 1,500 different instruments.

So you Get a Much better overview of how well your strategy works. So the amount of times I;ll be testing a strategy on one instrument and then it works poorly on that but amazing on another one of the 150 so you stick with something and improve something that I would’ve assumed was terrible or useless if I was just back testing one instrument.

I then code all my algos from quantreex into Pro Real Time myself. Quantreex has a limit it can only connect 15 algos at a time to IG Markets. I really like there optimismation feature as well maybe pro real times one is better however I haven’t tried it yet.

“I run each strategy on 4-6 different instruments at once and all with an equal amount of pips on each one.”

I mean when live trading I run each strategy on 4-6 different instruments at once. So the strategy you looked at that I messaged you I take my overall trading budget and spread it evenly across 4-6 instruments. So for example 1 strategy £1/pip FTSE, same strategy £1/pip S&P, same strategy £1/pip DAX, £1/pip DJI, etc So the sum of my results is always the average of how those 4-6 instruments performed during the day. That’s how I’m trying to avoid drawdown.

It’s best to pick totally uncorrelated markets but I haven’t checked how correlated these markets are yet because I only started live trading again last week. So far I’ve only coded over 4 of the around 30-40 strategies I have in quantreex over to Pro Real Time so I’d assume/hope at least 3-4 of my best 5 performing strategies are still just sitting in quantreex.

“What you mean equal amount of pips?

Pips are movement in price, so 4 strategies on 4 instruments

cant make the same pips / profit”

Yeah but one strategy that I apply to 4 different instruments. So they all will have the same PIP/profit target. So obviously so could’ve made more then the target but other days they may not hit more then the profit and cost you money. So I’d rather be under the optimal profit target and aim for consistent as possible returns.

Sorry what does “flashed it over (imperfect term)” mean? I didn’t get that.

“Yes we can use £0.2 per point / pip

on UK spreadbet on DJI for example”

How? Would I have to edit that in the code instead of pro order? So instead of “BUY 1 PERPOINT AT MARKET” I’d say “BUY 0.2 PERPOINT AT MARKET” and that’ll work?

That makes thing so much easier as the DJI was the 3rd or 4th most consistent performer in the backtesting over a 30 day period.

“I hope you are doing all your testing / trials on a Demo Account for many months or at least 50 trades, preferable more?”

Nope I know that’s best to start with a demo account but I ran earlier versions of all these algos live for a whole month about a year ago via quantreex they all roughly broke even but I stopped because you can’t optimise the 17 strategies I had at the time when you can only run 15 in parallel. Then I was supposed to learn Pro Real Time straight after that but just never found the time to learn the Pro Real Time codes and software in general until last month.

So I have full confidence in older versions at least historically breaking even on quantreex so I dived straight in to live trading with the better versions here.

Plus I’ve read articles of the discrepancies between live and demo trading. Demo trades tend to be slightly skewed in your favour with slippage etc even timing wise the demo accounts hosted on a different server so the trades aren’t identical to the trades you’d make live. This doesn’t sound much but with take profits and stop losses over periods of time it all can really add up.

An yes I’m paying £75 for quantreex and I’m about to start paying $135 for Yewno their machine and stock features are really informative. It gives you a list of stocks that are effected by any one factor. So all the stocks 5g could influence or Elon Musk could influence etc. I might end up paying for Metastock and Refinitiv as a package as well. Refinitiv use news from Reuters which is probably only second to the Bloomberg Terminal on the planet.

I love the look of Meta Stock forecasting feature, I haven’t tried it yet however. Also Yewno have a patent feature that lists all the patents in a industry companies have applied for which I may try and combine with some options strategies.

I’ve never minded paying for information I’ve read and took detailed notes from like 30 books on investing, the stock market and options trading, quant trading and hours and hours of videos on day trading. Then I turned half of those notes into audio books that I listen too from time to time lol

So is there a way to keep algos open if they have a trade rejected for insufficient funds? Every time I go to sleep I seem to wake up to rejected trades I know I could just put more money in the account but is there a way to keep the algos live even after a trade has been rejected?

How do you set up a stop loss on your whole account or on a strategy that stops all strategies when your overall account is down like £500 for the day or something?

Also I get what you’re saying about entering at the most logical time but the easiest counter to that from personal experience so far is making the entry point less relevant by just lowering your take profit levels. It’s way easier to find a lower take profit level that does just as well financially by winning more often then it is to find a strategy that always enters at the logical point especially with evolving market conditions.

I’m going to test out the trailing stop and see if it improves things. Thanks for sharing it and for taking the time to get back to me 🙂