Thanks for the link to spread time table. It never even occurred to me that one would exist lol

Yes I do close the results tables. Sometimes I have to close every table and chart accept for the one I’m looking at a an dI can’t run a back test until I click the black x on the last strategy I run. Maybe there’s is some type of cache that takes time to be cleared or updates because it only happens after I’ve ran several back tests before and then deleted them.

Loool “I doubt the Author understands them easily a few weeks late!!?? 🙂”. That make me feel so much better. Some of the codes looked really complicated to me and I just assumed everyone understood them. So at least now I have some perspective 🙂

I’ve watched the free video training but I’ll definitely look into the fee paid programming and hopefully I can find someone offering mentorship. Thanks for the links.

Do most of your strategies go long and short inside one strategy? or do you have your long only strategies and short only strategies?

I seem to have created some fairly consistent strategies but I’m not sure if long and short strategies in general would experience more drawdown because you are making more trades or less because they should be more market neutral?

Also I’d suspect that long and short combined strategies are usually the most profitable because they make more trades or are they just less profitable because it’s harder to create a consistent long and short strategy?

Yep a utopia sounds nice. I have a friend who works managing a section fo a quant devision and he suggested the 24 hour strategy. It sounds like I’d have a lot of work cut for me.

I read this article https://www.prorealcode.com/blog/learning/how-to-improve-a-strategy-with-simulated-trades-1/ and this article https://www.prorealcode.com/blog/trading-strategy-profit-curve/

In the comments section it sounds like there was some issues with code in the comments section but it was years ago so maybe it’s been resolved but in theory wouldn’t it be easy to sleep if the Algo went into only simulated trades once the trades became unprofitable and then started back up only once the simulated trades were profitable?

That way you should wake up a profit or only a minimal loss. Do you think I could pay to have a cross between these techniques coded for me? So then I could trade overnight easier.

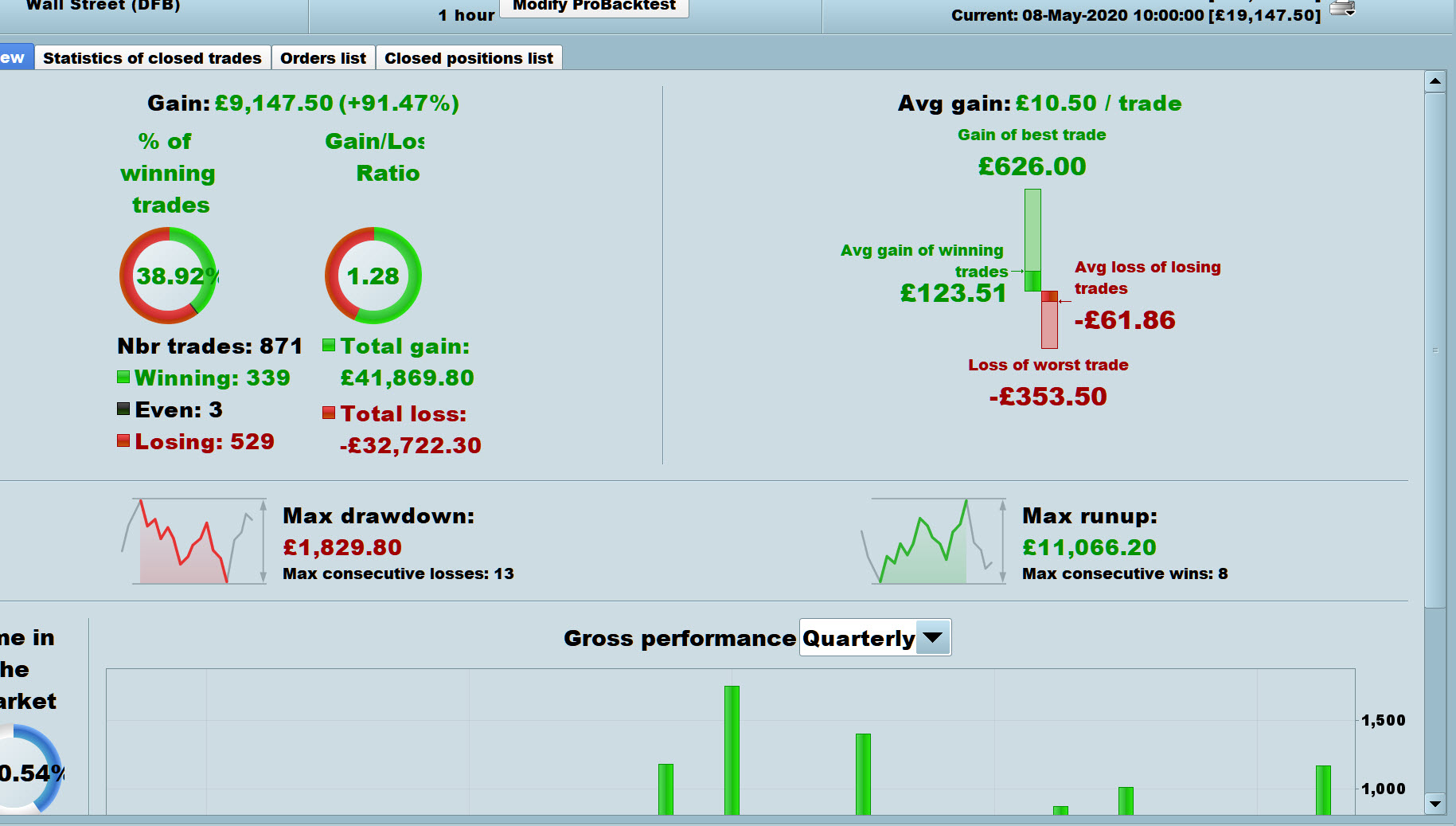

Well done coding 4,000 is an achievement in itself. I’ve done around 40 so far. 20 of them was from last year but with a few tweaks still work fine at the moment. I focus a lot on out of sample testing. An I’ve been using the optimisation engine on quantreex which seems to work well.

Is there any indicators that really seems to make a difference for you that is a recurring theme in the 4,000? Personally Aroon up/down seems to be pivotal and RSI overbought/oversold level cut offs really seem to help quite a few of my strategies over time.

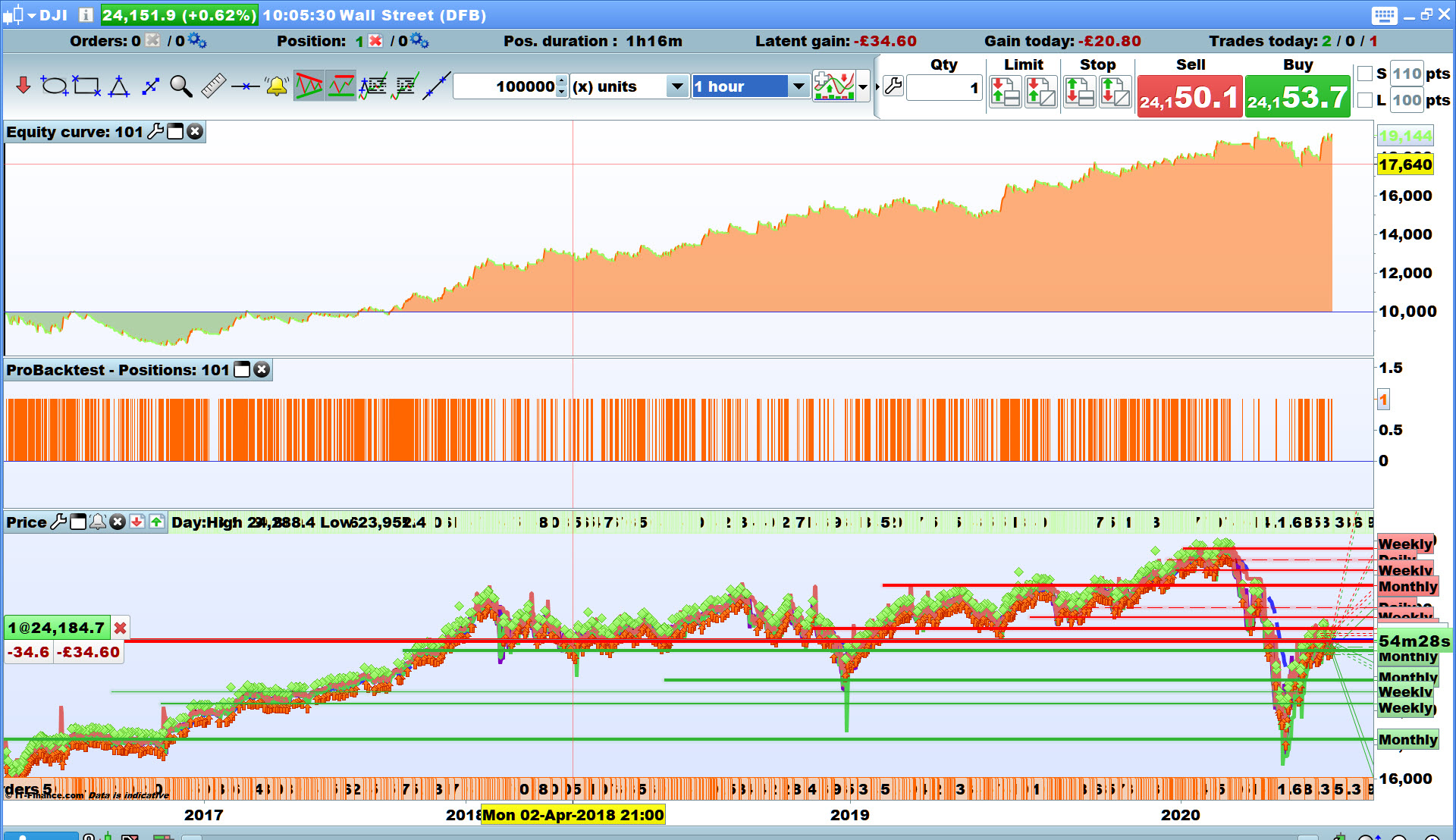

With the strategies I coded for it’s displayed in the code so look for “TIMEFRAME 15 minutes” AND “TIMEFRAME 1 minute”. So some things have to happen on a 15 minute chart simultaneously with other things happening on a 1 minutes chart.

It’s been pretty consistent so far at least relative to the markets. So I’ve been chopping and changing a lot with the changes in market conditions lately but on average I run each strategy on 4-6 different instruments at once and all with an equal amount of pips on each one.

This is an effort to just diversify the portfolio and minimise the drawdown. Plus my friend said that’s how they programme the algorithms where he works. I’ve tried maybe 15-20 different instruments and settled on the most consistent 4-7 as France 40, FTSE 100, German DAX (Excluding overnight), EU Stocks 50, AUD/CHF, NZD/JPY and AUD/CHF

When you say “flashed it over DJI TF’s from 10 sec to 4 hours” is there a code to do that simultaneously or do you do that one by one?

Also yes I noticed during back testing DJI was the 4th best performer all month but in Pro Order you can’t do less then 1/pip so with diversifying with 4-6 instruments at all times the DJI has been too expensive to try so far.

I know you can use mini lots with manual trading but pro order does seem to go under 1/pip Is there any way around that?

Also with the drawdown I want to set a daily stop loss do you know how to do that? Some days the market conditions just don’t suit a strategy/ instrument pairing so just pausing it at a maximum drawdown and then starting back up the next day and repeating until the market conditions become more favourable will mitigate drawdown plus with 4-6 instruments at all times drawdown should be minimised already.

I need to code some of short sell strategies over from quantreex to make everything market nuetral as well.

That’s a really interesting test how long do you check the buy and hold period for? So what would’ve happened if you held a month or a fortnight or a day etc?