la modification ne change rien…. 🙁

ci-dessous l’erreur remontée

// Définition des paramètres du code

Defparam CumulateOrders = False

Defparam Preloadbars = 30000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Distance = 15

LookBack = 15000

SR = 9

// Timeframe SRLevel

timeframe (30 minutes, updateonclose)

// --- icihmoku support and resistance

kijun = (highest[26](high)+lowest[26](low))/2

SSB = (highest[52](high[26])+lowest[52](low[26]))/2

kijunp = summation[SR](Kijun=Kijun[1])=SR

ssbp = summation[SR](SSB=SSB[1])=SR

if kijunp then

kijunPrice = kijun

endif

if ssbp then

ssbPrice = SSB

endif

if kijunprice = ssbprice then

SRlevel = kijunprice

endif

//Timeframe en UT de Trading

Timeframe (10 seconds, default)

//************************************************************************

levier = 2

capital = 500 + (strategyprofit*2/5)

z = (capital / (close/20)) * levier

//************************************************************************

//Position acheteuse

buycondition = rsi[14] crosses over 50

buycondition2 = x Crosses Over 0.7 and Summation[2](x > 0.5) = 2

if Buycondition and not onmarket and not daysForbiddenEntry then

allowtrading = 1

for iSRB = 0 to lookback -1 do

dist = abs(close-SRlevel[iSRB]) < distance*pipsize

if dist then

allowtrading = 0 //no trading is allowed we are near a SR!

break //break the loop, no need to continue, trading is not allowed anymore!

endif

next

If BuyCondition2 then

Entry = Barindex

endif

if Barindex-Entry <= 2 then

if allowtrading then

buy z share at market

endif

endif

endif

//Position Vendeuse

sellcondition = rsi[14] crosses under 50

sellcondition2 = x Crosses Over 0.7 and Summation[2](x > 0.5) = 2

if SellCondition and not onmarket and not daysForbiddenEntry then

allowtrading = 1

for iSRV = 0 to lookback -1 do

dist = abs(close-SRlevel[iSRV]) < distance*pipsize

if dist then

allowtrading = 0 //no trading is allowed we are near a SR!

break //break the loop, no need to continue, trading is not allowed anymore!

endif

next

if SellCondition2 then

Entry = Barindex

endif

If Barindex-Entry <= 2 then

if allowtrading then

sellshort z share at market

endif

endif

endif

//************************************************************************

//Stop Loss & Trailing function

Set stop $loss capital*levier*4/100

Set Target $Profit capital*levier*5/100

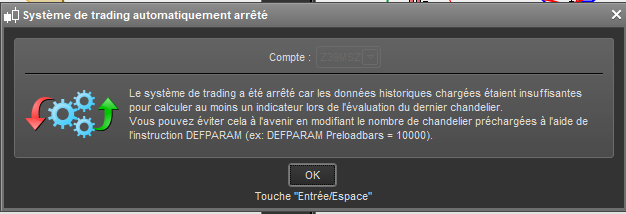

Ci-dessus, la partie du code qui semble poser problème.

je me demande si ce n’est pas un problème de preloadbars entre les deux timeframe…

Un lookback de 15.000 bars est énorme ! Une boucle sur 15000 chandeliers c’est beaucoup trop, même si celle-ci n’ira jamais jusqu’au bout, puisqu’on trouvera un support ou une résistance avant d’arriver au terme de celle-ci.

Bref, le problème principale dans ton cas, c’est surtout que ProOrder ne peut pas charger plus de 10.000 unités d’historique, donc ta boucle ne peut pas dépasser cette valeur !

Je vais faire quelques tests… Je te revient lorsque j’ai réglé le soucis…. Je vais baisser la valeur à 10.000 dans un premier temps….

Merci du retour

Bjr Nicolas,

Problème réglé!

baisser LookBack à 9999 à réglé les arrêts.

Merci pour le retour.

Defparam CumulateOrders = False

Defparam Preloadbars = 43200

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Distance = 8

LookBack = 5000

SRk = 5

SRs = 8

// --- icihmoku support and resistance

kijun = (highest[26](high)+lowest[26](low))/2

SSB = (highest[52](high[26])+lowest[52](low[26]))/2

kijunp = summation[SRk](Kijun=Kijun[1])=SRk

ssbp = summation[SRs](SSB=SSB[1])=SRs

if kijunp then

kijunPrice = kijun

endif

if ssbp then

ssbPrice = SSB

endif

if kijunprice = ssbprice then

SRlevel = kijunprice

if SRLevel > Close then

ResLevel = SRlevel

elsif SRLevel < Close then

SupLevel = SRlevel

endif

endif

//************************************************************************

levier = 2

capital = 500 + (strategyprofit*2/5)

z = (capital / (close/20)) * levier

//************************************************************************

//Buy Conditions

buycondition = rsi[14] crosses over 50

buycondition2 = x Crosses Over 0.7 and Summation[2](x > 0.5) = 2

if Buycondition and not onmarket and not daysForbiddenEntry then

allowtrading = 1

for iSRB = 0 to lookback -1 do

dist = (Reslevel[iSRB] - Close) < distance*pipsize

if dist then

allowtrading = 0 //no trading is allowed we are near a SR!

break //break the loop, no need to continue, trading is not allowed anymore!

endif

next

If BuyConditionL then

Entry = Barindex

endif

if Barindex-Entry <= 2 then

if allowtrading then

buy z share at market

endif

endif

endif

//Sell Conditions

sellcondition = rsi[14] crosses over 50

sellcondition2 = x Crosses Over 0.7 and Summation[2](x > 0.5) = 2

if sellcondition and not onmarket and not daysForbiddenEntry then

allowtrading = 1

for iSRV = 0 to lookback -1 do

dist = (close-Suplevel[iSRV]) < distance*pipsize

if dist then

allowtrading = 0 //no trading is allowed we are near a SR!

break //break the loop, no need to continue, trading is not allowed anymore!

endif

next

if SellCondition2 then

Entry = Barindex

endif

If Barindex-Entry <= 2 then

if allowtrading then

sellshort z share at market

endif

endif

endif

//************************************************************************

//Stop Loss & Trailing function

Set stop $loss capital*levier*4/100

Set Target $Profit capital*levier*5/100

Quelques corrections sur le code.

De cette manière les Supports et Résistances sont clairement identifiés.

Dans le même registre, est ce qu’il est possible de créer une boucle sur les mêmes conditions de distance, avec les supports et résistances du pivot (pivot compris)

Pivot = (Dhigh(1) + Dlow(1) + Dclose(1) + Dopen(0))/4 //Pivot

Res3 = Dhigh(1)+(2*(Pivot-Dlow(1))) //Res3

Res2 = Pivot+(Dhigh(1)-Dlow(1)) //Res2

Res1 = (2*Pivot) - Dlow(1) //Res1

Sup1 = (2*Pivot) - Dhigh(1) //Sup1

Sup2 = Pivot-(Dhigh(1)-Dlow(1)) //Sup2

Sup3 = Dlow(1)-(2*(Dhigh(1)-Pivot)) //Sup3

Merci pour l’aide.

J’ai géré comme ci-dessous:

//Pivot (H + L + C + O)/4

If OpenDayOfWeek = 1 Then

Ht = DHigh(2)

Bs = DLow(2)

C = DClose(2)

O = DOpen(0)

Endif

If OpenDayOfWeek => 2 and dayofweek < 6 Then

Ht = DHigh(1)

Bs = DLow(1)

C = DClose(1)

O = DOpen(0)

Endif

Pivot = (Ht + Bs + C + O)/4

Res4 = Ht + (3*(Pivot - BS))

Res3 = Ht + (2*(Pivot - Bs))

Res2 = Pivot + (Ht - Bs)

Res1 = (2*Pivot) - Bs

Sup1 = (2*Pivot) - Ht

Sup2 = Pivot-(Ht - Bs)

Sup3 = Bs - (2*(Ht - Pivot))

Sup4 = Bs - (3*(Ht - Pivot))

// Position acheteuse

if close > pivot then

//above Pivot

iPivt = 1

while iPivt =< 4 do

if iPivt = 1 then

Floor = Pivot

Ceil = Res1

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 2 then

Floor = Res1

Ceil = Res2

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 3 then

Floor = Res2

Ceil = Res3

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 4 then

Floor = Res3

Ceil = Res4

if close > Floor and close < Ceil then

break

endif

endif

iPivt = iPivt + 1

wend

elsif close < Pivot then

//below Pivot

iPivt = 1

while iPivt <= 4 do

if iPivt = 1 then

Floor = Sup1

Ceil = Pivot

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 2 then

Floor = Sup2

Ceil = Sup1

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 3 then

Floor = Sup3

Ceil = Sup2

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 4 then

Floor = Sup4

Ceil = Sup3

if close > Floor and close < Ceil then

break

endif

endif

iPivt = iPivt + 1

wend

endif

For IPivt = 1 to 4 do

dist = (Ceil - Close) < distance*pipsize

If Dist then

allowtrading = 0

Break

endif

next

// Position vendeuse

if close > pivot then

//above Pivot

iPivt = 1

while iPivt =< 4 do

if iPivt = 1 then

Floor = Pivot

Ceil = Res1

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 2 then

Floor = Res1

Ceil = Res2

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 3 then

Floor = Res2

Ceil = Res3

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 4 then

Floor = Res3

Ceil = Res4

if close > Floor and close < Ceil then

break

endif

endif

iPivt = iPivt + 1

wend

elsif close < Pivot then

//below Pivot

iPivt = 1

while iPivt <= 4 do

if iPivt = 1 then

Floor = Sup1

Ceil = Pivot

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 2 then

Floor = Sup2

Ceil = Sup1

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 3 then

Floor = Sup3

Ceil = Sup2

if close > Floor and close < Ceil then

break

endif

elsif iPivt = 4 then

Floor = Sup4

Ceil = Sup3

if close > Floor and close < Ceil then

break

endif

endif

iPivt = iPivt + 1

wend

endif

For IPivt = 1 to 4 do

dist = (Close - Floor) < distance*pipsize

If Dist then

allowtrading = 0

Break

endif

next

ça a l’air de fonctionner, mais j’ai l’impression que c’est interminable…!

y a t’il moyen de simplifier?

Très bien, j’ai créé une stratégie toute simple qui prendra ses ordres si “allowtrading” est égal à 1 (égal à 0 si trop proche d’un SR).

Dans la boucle on teste une proximité de “distance” avec un support/resistance détecté dans les “lookback” derniers chandeliers.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

|

defparam cumulateorders=false

// — settings

distance = 15 //no orders if there is a SR within X points

lookback = 1000 //lookback in bars to check recent SR

tp = 30 //takeprofit in points

sl = 10 //stoploss in points

// ———————————-

// — icihmoku support and resistance

kijun = (highest[26](high)+lowest[26](low))/2

SSB = (highest[52](high[26])+lowest[52](low[26]))/2

kijunp = summation[9](Kijun=Kijun[1])=9

ssbp = summation[9](SSB=SSB[1])=9

if kijunp then

kijunPrice= kijun

endif

if ssbp then

ssbPrice= SSB

endif

if kijunprice=ssbprice then

SRlevel= kijunprice

endif

// ———————————-

// — dummy strategy

buycondition = rsi[14] crosses over 50

sellcondition = rsi[14] crosses under 50

if buycondition or sellcondition then

//check if the current price is distant from at least “distance” from recent support or resistance

allowtrading=1

for i = 0 to lookback–1 do

dist= abs(close–srlevel[i])<distance*pointsize

if dist then

allowtrading=0 //no trading is allowed we are near a SR!

break //break the loop, no need to continue, trading is not allowed anymore!

endif

next

//trigger orders or not

if allowtrading then

if buycondition then

buy 1 contract at market

endif

if sellcondition then

sellshort 1 contract at market

endif

endif

set target pprofit tp

set stop ploss sl

endif

// ———————————-

graph allowtrading as “0=near a SR , don’t trade!”

|

Bjr Nicolas,

j’ai ajusté un peu les plats Kijun et SSB:

SRk = 5

SRs = 8

// --- icihmoku support and resistance

kijun = (highest[26](high)+lowest[26](low))/2

SSB = (highest[52](high[26])+lowest[52](low[26]))/2

kijunp = summation[SRk](Kijun=Kijun[1])=SRk

ssbp = summation[SRs](SSB=SSB[1])=SRs

if kijunp then

kijunPrice = kijun

endif

if ssbp then

ssbPrice = SSB

endif

if kijunprice = ssbprice then

SRlevel = kijunprice

if SRLevel > Close then

ResLevel = SRlevel

elsif SRLevel < Close then

SupLevel = SRlevel

endif

endif

Néanmoins codé tel quel, j’ai l’impression que ça ne trace les SRlevel que lorsque kijunP et SSBp sont strictement = à SRk et SRs.

je n’arrive pas à codé une alternative ou il faut Min SRk pour Kijunp et Min SRs pour SSBp.

une idée?