It is clear that it is difficult to have a trading code that could take place for a long time exactly as intended by its designers. On the other hand, this code could well be profitable on certain financial instruments (Crypto, Forex, Shares or Indices) while checking it beforehand on backtest at different timeframes. Example: BTC / USD at TimeFrame = 20min and 2 minutes; EUR / USD at TimeFrame = 100 ticks or 15 30 45 min or 1 hour; DAX, etc. NB: There is the possibility of being able to improve it by the professionals that you are and to share …

DEFPARAM CumulateOrders=False

//CCI strategy with limit threshold for input or output signal

Once Quantite = 1 //(1*PipValue)

Once Interval = 55

Once SeuilCCI = 170 //(OK at: 100,150,'170',180)

indicoteNegatif = CCI[Interval](Close) < -SeuilCCI

indicotePositif = CCI[Interval](Close) > SeuilCCI

indicator1 = CCI[Interval](Close)

indicator2 = Highest[7](CCI[Interval](Close[1]))

indicator3 = Highest[6](CCI[Interval](Close[3]))

c1 = (indicator3 < indicator2) AND (indicator2 < indicator1)

c2 = (indicator3 > indicator2) AND (indicator2 > indicator1)

REM BUY

IF indicoteNegatif AND c1 THEN

BUY Quantite SHARES AT MARKET

ELSIF LongOnMarket AND indicotePositif THEN

EXITSHORT AT MARKET

ENDIF

REM SELL

IF indicotePositif AND c2 THEN

SELLSHORT Quantite SHARES AT MARKET

ELSIF Not LongOnMarket AND indicoteNegatif THEN

EXITSHORT AT MARKET

ENDIF

Thanks…

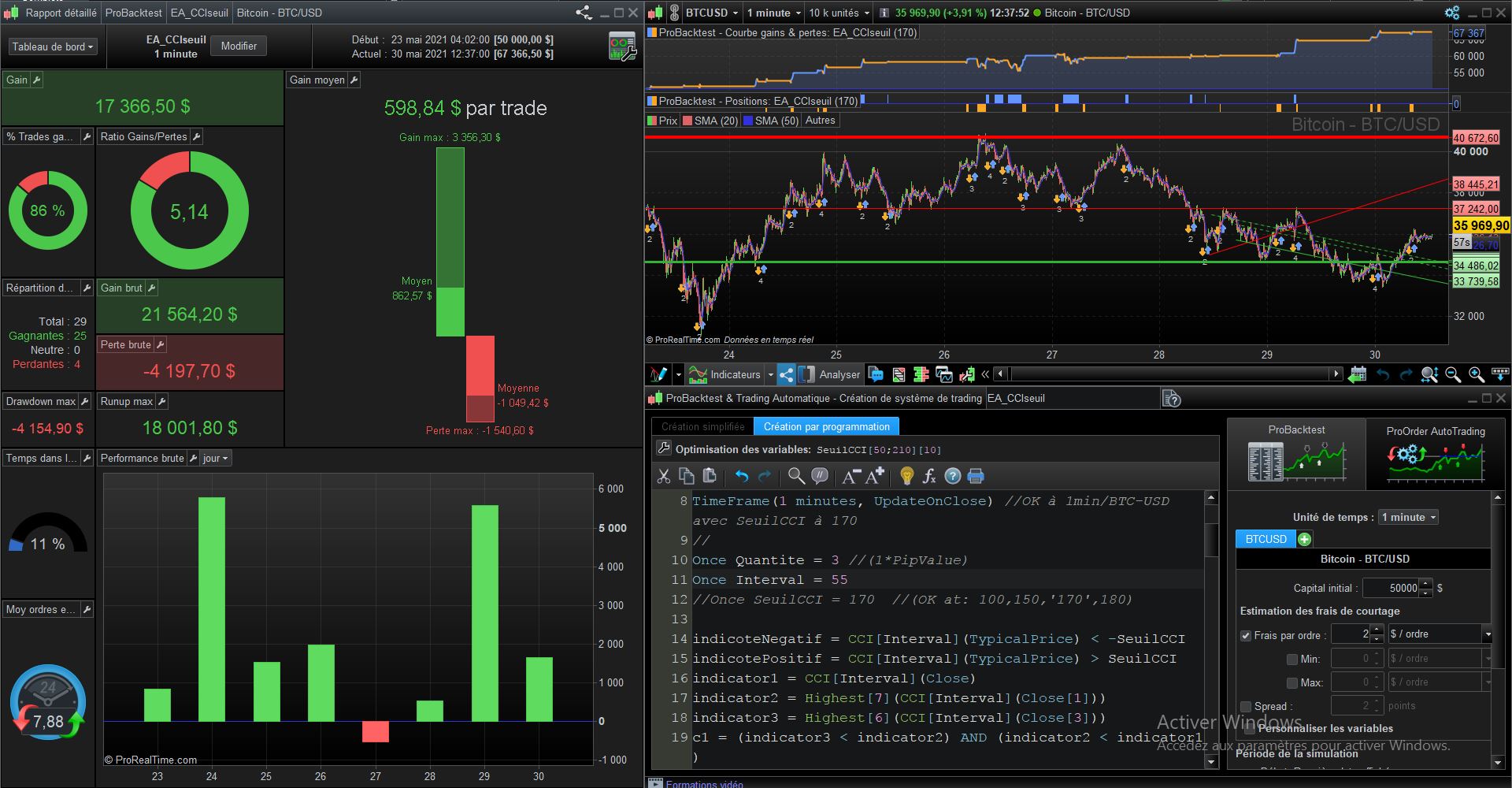

I modified it by using MTF (1h TF for the setup & entry + 5m TF for the trailing stop):

DEFPARAM CumulateOrders=False

//CCI strategy with limit threshold for input or output signal

timeframe(1h,UpdateOnClose)

//

Once Quantite = 1 //(1*PipValue)

Once Interval = 55

Once SeuilCCI = 170 //(OK at: 100,150,'170',180)

indicoteNegatif = CCI[Interval](Close) < -SeuilCCI

indicotePositif = CCI[Interval](Close) > SeuilCCI

indicator1 = CCI[Interval](Close)

indicator2 = Highest[7](CCI[Interval](Close[1]))

indicator3 = Highest[6](CCI[Interval](Close[3]))

c1 = (indicator3 < indicator2) AND (indicator2 < indicator1)

c2 = (indicator3 > indicator2) AND (indicator2 > indicator1)

REM BUY

IF indicoteNegatif AND c1 THEN

BUY Quantite SHARES AT MARKET

ELSIF LongOnMarket AND indicotePositif THEN

EXITSHORT AT MARKET

ENDIF

REM SELL

IF indicotePositif AND c2 THEN

SELLSHORT Quantite SHARES AT MARKET

ELSIF Not LongOnMarket AND indicoteNegatif THEN

EXITSHORT AT MARKET

ENDIF

//

Timeframe(default)

//

// Nicolas' trailing stop code, slightly modified to:

//

// - acount for minimum distance required by the broker for pending orders

// - start trailing not only from the first bar, but from any later bar

//

IF (BarIndex - TradeIndex) >= 0 THEN //start from the first bar or a later one

trailingstart = 20 //20 trailing will start @trailinstart points profit

trailingstep = 10 //10 trailing step to move the "stoploss"

distance = 10 //10 pips distance from caurrent price (if required by the broker)

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

IF LongOnMarket THEN

IF (close + distance) > newSL THEN

SELL AT newSL STOP

ELSIF (close - distance) < newSL THEN

SELL AT newSL LIMIT

ELSE

SELL AT Market

ENDIF

ELSIF ShortOnmarket THEN

IF (close + distance) < newSL THEN

EXITSHORT AT newSL STOP

ELSIF (close - distance) > newSL THEN

EXITSHORT AT newSL LIMIT

ELSE

EXITSHORT AT Market

ENDIF

ENDIF

ENDIF

ENDIF

//*********************************************************************************

Thank you very much RobertoGozzi

The code worked well with the gains and loss limitation.

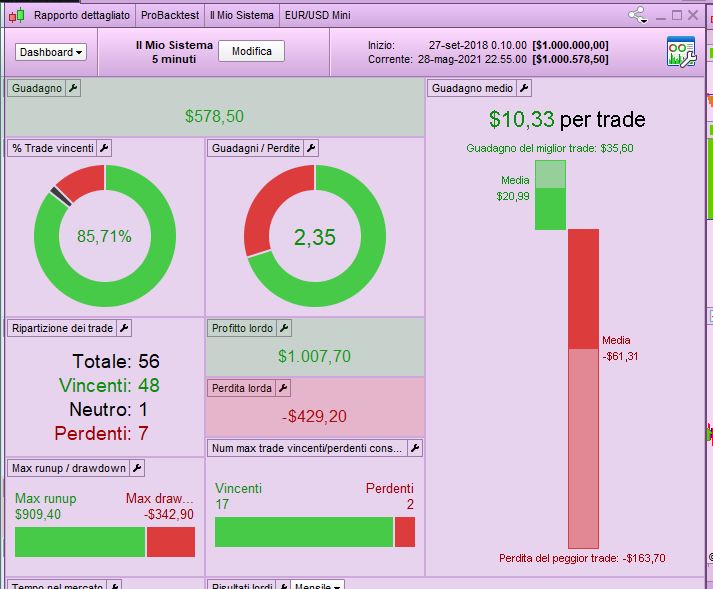

NB: The CCI Threshold and TimeFrame parameters should be adjusted for each financial asset.

Here are the best results obtained with the optimal values of the 2 adjustable parameters:

– For BTC/USD ==>

CCI threshold = 170

TimeFrame (1 minutes, UpdateOnClose)

– For EUR/USD ==>

CCI threshold = 140

TimeFrame (3 minutes, UpdateOnClose)

– For GBP/USD ==>

CCI threshold = 170

TimeFrame (10 minutes, UpdateOnClose)

– For USD/CHF ==>

CCI threshold = 100 and 120

TimeFrame (3 minutes, UpdateOnClose)

Even more, it would be necessary to define the values of Stop and follower, as for example:

trailingstart = 150 // 20 trailing will start @trailinstart points profit

trailingstep = 15 // 10 trailing step to move the “stoploss”

distance = 15 // 10 pips distance from caurrent price (if required by the broker)

Thanks…