Hi Vonasi,

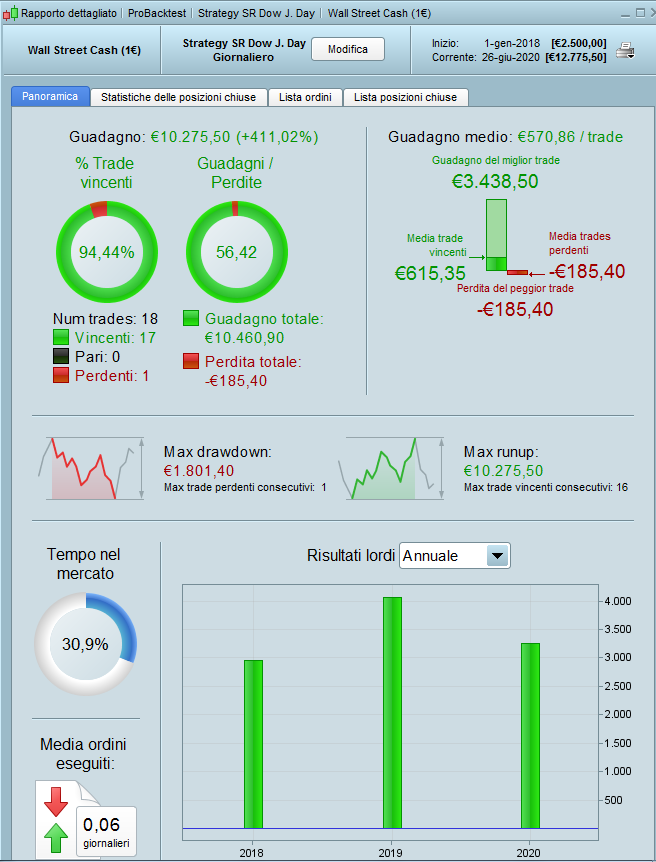

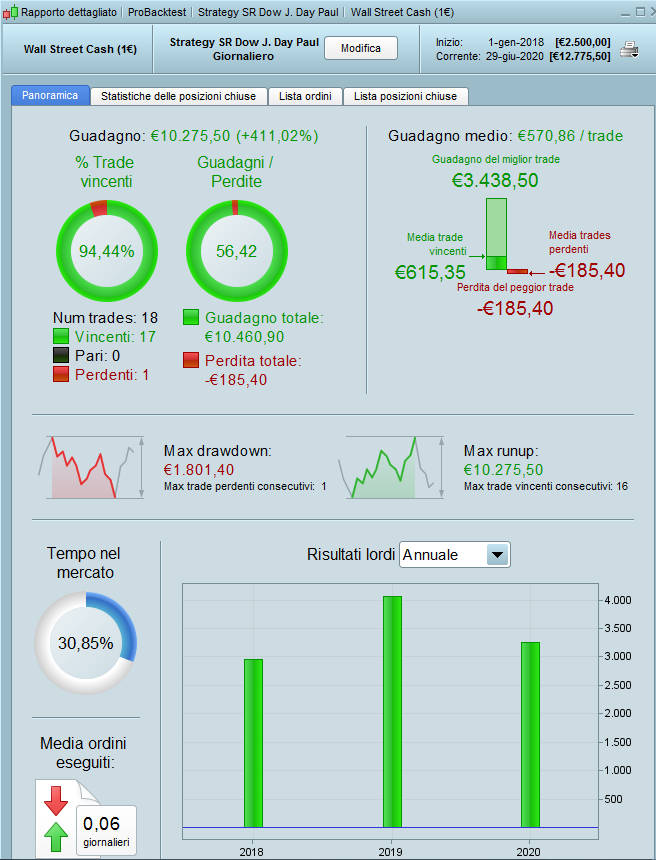

When I make the optimizations of my trading systems I ALWAYS stop in December 2017 for any Time Frame, so the computer cannot know beyond that date what happened …. in the attached graph it starts Without the time-based sale from 1 January 2018. …… clearly I try to have the odds in my favor certainty does not exist in anything …..

I thank you for your work and I wish you a good evening …

Paul

PaulParticipant

Master

the set target profit needs to be straight below the buy order because it uses average range & close.

It can not be put on the bottom. It’s placed correct and uses the close when conditions are true to go long.

however, you do not use not longonmarket, so, if your are long and conditions are true to go long again are ignored (because DEFPARAM CumulateOrders = false) , it updates the target with the new close of that bar which is incorrect. To have it correct I think you have to use not longonmarket?

If you add not longonmarket performance goes down, however, if you take every signal when in a long and losing position to close & reenter again long, it’s much better.

here again a but, because not sure why the code below makes such a difference.

if condbuy[1] then

buy positionsize contract at market

SET TARGET PROFIT 5* averagetruerange[1](close)

endif

or

if condbuy[1] then

buy positionsize contract at market

SET TARGET PROFIT 5* averagetruerange[1](close)[1]

endif

// Strategy SR Dow J. Day indicator by roberto gozzi

DEFPARAM CumulateOrders = false

once tradetype = 2 // [1]long & short; [2]long only; [3]short only

once reenter = 0 // [0]off; [1]reenter based on positionperftype

once positionperftype = 0 // [0]perf<>ppv; [1]perf<ppv; [2]perf>ppv

once positionperfvalue = 0

indicator1 = ADX[10]

indicator2 = ADXR[14]

c2 = (indicator1[1] > indicator2[1])

indicator11 = ADX[10]

c1 = (indicator11[1] >= 15)

c30 =TR(close)>25

ONCE PrezzoC = 0

ONCE PrezzoB = 0

ONCE PrezzoA = 0

Prezzo = CALL SRtest

IF Prezzo > 0 THEN

PrezzoA = PrezzoB

PrezzoB = PrezzoC

PrezzoC = Prezzo

ENDIF

positionsize=1

LossMonth =200

once StopMonth=1

IF Month <> Month[1] THEN

ProfitMonth=strategyprofit

StopMonth=1

endif

If strategyprofit<=ProfitMonth-LossMonth then

StopMonth=0

endif

Cond = PrezzoB > PrezzoA AND PrezzoB > PrezzoC

condbuy=StopMonth=1 and close CROSSES UNDER PrezzoB AND C2 AND C1 AND C30 AND Cond > 0

// CONDBUY=CONDBUY AND NOT LONGONMARKET

condsell=1

ctime=1

// entry criteria

if ctime then

if (tradetype=1 or tradetype=2) then

if condbuy then

buy positionsize contract at market

SET TARGET pPROFIT 5* averagetruerange[1](close)

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and not shortonmarket then

sellshort positionsize contract at market

endif

endif

if reenter then

if positionperftype=1 then

positionperformance=positionperf(0)*100<-positionperfvalue // in loss

elsif positionperftype=2 then

positionperformance=positionperf(0)*100>positionperfvalue // in profit

else

positionperformance=((positionperf(0)*100)<-positionperfvalue or (positionperf(0)*100)>positionperfvalue) // in loss or profit

endif

if (tradetype=1 or tradetype=2) then

if condbuy and longonmarket and positionperformance then

sell at market

endif

if condbuy[1] then

buy positionsize contract at market

SET TARGET PROFIT 5* averagetruerange[1](close) // or [1] at the end?

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and shortonmarket and positionperformance then

exitshort at market

endif

if condsell[1] and not shortonmarket then

sellshort positionsize contract at market

endif

endif

endif

else

if longonmarket and condsell then

//sell at market

endif

if shortonmarket and condbuy then

//exitshort at market

endif

endif

If longonmarket and (barindex-tradeindex)>=43 then

//SELL AT MARKET

ENDIF

Trailinglong = 2* averagetruerange[5](close)

Trailingsteplong = 5* averagetruerange[1](close)

TGL = Trailinglong

STPL = Trailingsteplong

if not onmarket then

MAXPRICE = 0

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL then

PREZZOUSCITA = MAXPRICE-STPL

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

SET STOP %LOSS 8

however, you do not use not longonmarket, so, if your are long and conditions are true to go long again are ignored (because DEFPARAM CumulateOrders = false) , it updates the target with the new close of that bar which is incorrect. To have it correct I think you have to use not longonmarket?

Well spotted Paul. When I added my SEB testing code to the strategy I encased the STOP and TARGET orders in an IF NOT ONMARKET condition so that I could count all possible trades outside of that condition – so my version did not behave the same as the original. I should try to find time to retest with the varying stop and target orders. Bit busy at the moment as leaving the harbour to go sailing for the summer in a few days time and so lots of jobs to do – including hours and hours of fixing my back-up navigation laptop. Who would think it could be so difficult to get a netbook working on XP!

Hello Paul,

The operation from 1 January 2018 is identical …. and it is the only important thing …… if we had put in real since that date in both ways we would have had the same results.

Thank you

(I am attaching the graph of your variant from January 2018.)